In his first CPD article for 2014 Ray Griffin examines the need for advisers to stay abreast of economic and market conditions in order to more effectively set portfolio allocations and the vital need to set clients’ expectations in the real world.

So you’re back at your desk and starting to wind up for 2014 after some time away from the inevitable, accumulated, end of year mental fatigue. Last year was a reasonable year in the markets – no major market-wide collapses at least – and with fingers crossed you’re hoping 2014 will at worst be similar. There’s a new government in Canberra and improving consumer confidence albeit somewhat labile; interest rates remain low and while the December quarter inflation edged up a tad interest rates look stable for the time being. Nevertheless, the RBA still has inflation leg-roped and with glacial like regularity, pockets of good news continue to emerge from the USA and to a lesser extent Europe. But will portfolio construction be that straight forward from 2014 on? And what messages are you giving your clients about the foreseeable future for portfolios?

While portfolio construction and ongoing management is but one aspect of the services provided by an adviser, for many consumers it remains the reason why they seek initial advice and ongoing service. It is, for many, the yardstick by which they measure the value for money they believe they are receiving. So getting portfolio construction right more often than not remains a central part of an adviser’s service offering.

A changing landscape

Although the Australian economy has run counter cyclically to much of the developed world since the GFC, it’s clear that the dream run might be nearing an end if not already over. Trends from the most recent business and consumer confidence surveys point to the private sector looking further down the road than a change of government, low interest rates and Christmas retail sales. It (business) is getting well and truly under the bonnet and finding reasons to be concerned. The rest of the developed world – while less critically situated than five years ago – remains delicately poised between another crisis and a sluggish, elongated, recovery.

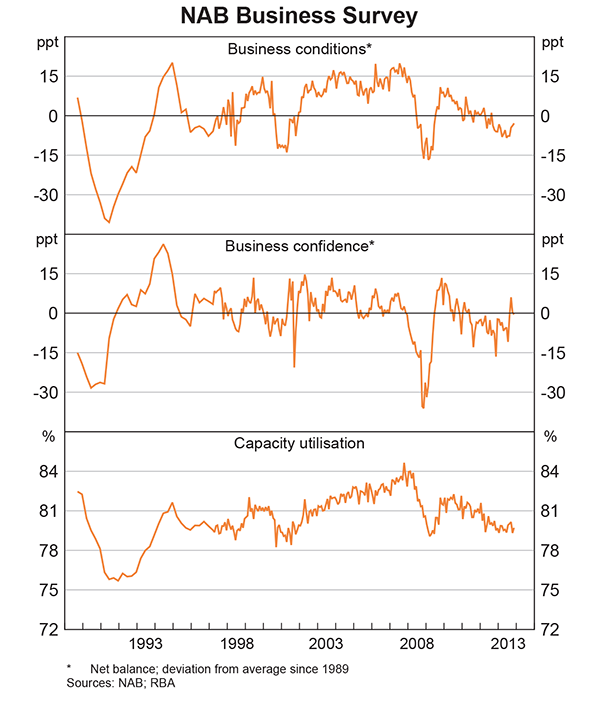

Chart 1: 5 years of a downward trend in business conditions. Is business confidence, after a momentary lift in 2013, now reverting to trend? Source: RBA, NAB.

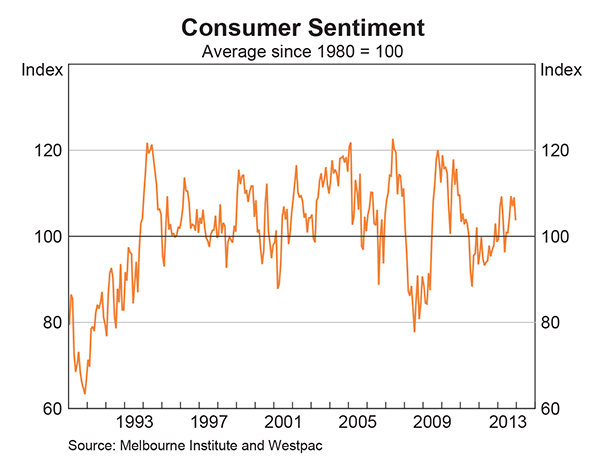

While business confidence surveys have tracked a choppy path since the GFC, over the last three years consumer sentiment measures have been trending upward with associated peaks and troughs. For advisers, the trend differential between consumer and business confidence measures should be noted.

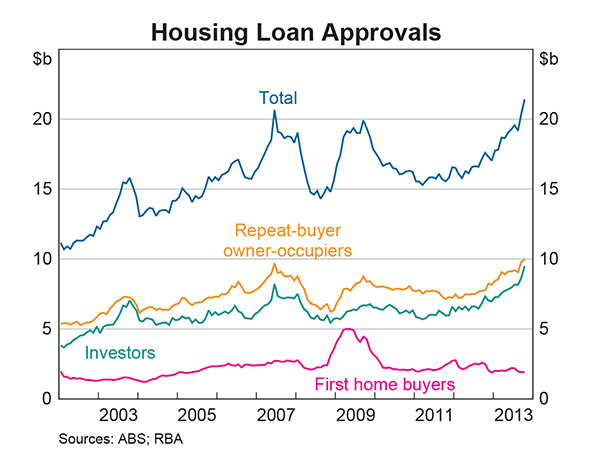

The parallel of confidence between consumers generally and the value of yearly housing finance approvals (Chart 3 below) results in an almost mirror image of data outcomes in recent years. As consumers leave the GFC behind them up go home loan approvals.

Source RBA Chart Pack

While first home buyers, especially those in some capital cities, still appear to be shut out of the market, it’s noteworthy that the value of housing loan approvals appears to have breached the pre GFC peak. In contrast, however, consumer sentiment is yet to reach the pre GFC levels.

Looking at the currency, with the A$ at around $0-90 US and a forecast continued downward trend there might a period of ‘imported’ inflation waiting in the wings which, to some extent, more broadly, should be offset by more competitive pricing of Australian exports.

However, some large companies with decades of drip feeds of government funding, are beginning to sound the retreat while a previously government owned business is now calling for greater protection on international air routes to and from Australia. Calls for increased productivity and an apparent coalescence of labour pressures in the mining, energy, motor vehicle manufacturing, retail and public sectors and it’s apparent Australians that have a job are going to be asked to do even more in their working week.

Added to this palette of conditions is that the ‘asset bubble’ descriptor is being cast about like confetti for certain investment sectors here and overseas.

Welcome to portfolio construction 2014/15/16…

And for your clients this means?

For your clients this means you need to be reviewing your asset allocation models and run some scenario planning across them.

- What if, the A$ fell to under US$0-80 cents? What does that do to your GDP growth expectations? What does it mean for inflation? What are the implications for international assets – should you be recommending higher weightings to get the currency ‘free-kick’? Or should you not?

- What if unemployment rises (e.g. resultant of mass lay-offs in the motor vehicle industry and the knock-on impact through the supply chain), consumption falls and business investment halts?

- What if the A$ finds some buoyancy and the RBA moves rates lower again in an attempt to reduce the relative attraction of Australian interest rates in world markets? What if still lower rates results in a rush of confidence in the housing sector pushing prices higher again and eventually leading to interest rate rises and a further strengthening of the A$?

- What if the recent December quarter inflation data pushes the interest rate levers toward a rate increase?

- What if unemployment were to hit 10% and what if Australia were to enter its first recession in more than two decades?

- What if… by now you should be getting the picture.

Relatively straightforward portfolio modeling spreadsheet techniques should allow you to understand the potential outcomes of these and myriad other future scenarios.

- What happens to your clients’ income returns and what can you do about it within the risk parameters for clients?

- What about portfolio growth? Will there be any and if so what might the risks be?

In investing terms, income and growth (or the lack thereof) are all you’ve got to show clients over any length of time so it’s crucial that you set your clients’ expectations within the realms of feasible outcomes. And this is the most crucial point; while your scenario planning findings might give cause to alter your portfolio asset allocations, it’s what you tell your clients to expect which will impact most greatly on their assessment of the value they receive from you versus what it costs them.

There is an adage: ‘Under promise and over deliver’ and for financial advisers it should be their morning mantra when they settle into each day’s diary of appointments. As an adviser, you have a very large influence on what your clients’ expectations of portfolio performance outcomes will be. Paint a picture too rosy and you’re going to ratchet up the risk of complaints and losing clients if markets behave in a manner different to what your clients are expecting. Paint a picture of the real world conditions and clients will, if nothing else, see that you’re across your brief of looking after their money.

This is not about being pessimistic – far from it. The overriding goal here is to be realistic with your clients. It’s about understanding what you can and cannot influence.

You have absolutely no ability to influence world economic performance and market returns. You, in isolation, have no capacity to alter government fiscal policy. You have no control over world events. You have no ability to rewrite nightly news bulletins that will greatly influence whether or not consumers – your clients – will be confident or pessimistic. You cannot influence investment decisions made by boards of companies. None of these are within your sphere of influence or capability.

What you can do, however, if you stay well informed about the major economic data for Australia and overseas, is form a view as to what might lie ahead for your clients’ portfolios. It automatically follows that if you and your colleagues are forming a ‘house view’ on what might be coming down the investment return pipeline for clients, you can then begin to prepare clients for it.

You can be sure of one thing: clients have a great dislike for surprises on the downside of portfolio returns. However, falling values and periods of weak performance are part of the journey of long-term investors so it’s beholden of advisers to get their clients ready for such times. A disciplined approach to this sees advisers ready their clients with realistic commentary about current conditions, and what might lie ahead, during regular client meetings and presentations and through all written communications.

Walk the walk

That however, is not sufficient – your job is not done until client portfolios reflect the ‘house view’ of the potential economic and market conditions. It’s one thing to be a good, realistic, communicator, but you have to follow through and be a good asset allocator. While allocation models will vary over different client age groups with younger clients having more time to withstand extended periods of major economic and market downturns, all clients need to be given realistic expectations. Young clients listen to daily news bulletins; young clients get nervous about their financial security and young clients don’t like to be surprised.

No surprises for you

And while we’re on the topic of surprises, you should never be blindsided by economic and market events unless they result from acts of terror or sudden outbreaks of war. On this point, even the US’s Central Intelligence Agency had no idea that Iraq was going to invade Kuwait in 1990 so there will always be a risk that events can overtake you and your clients’ portfolios.

That exception notwithstanding however, it is entirely possible for every financial adviser (anywhere in the world) to gain great insight into the Australian and world economy through the monthly publication of the Reserve Bank of Australia’s ‘Chart Pack’. Around 80 charts can be downloaded, at no cost, every month and the information can readily form the foundation of how you and your colleagues develop your ‘house view’ of economic conditions and investment trends. That information along with other sources of data can greatly assist in your asset allocation scenario planning.

It could be argued that the most important thing an adviser can do for all her clients is to be realistic with them. While it is the subject for another paper, it’s arguable to that setting realistic expectations for clients is part and parcel of the ethical conduct expected of a fiduciary.

While that might be so, you cannot be realistic with clients unless you understand what’s happening in economies and markets here and internationally. And you cannot be realistic with clients unless you take that information and develop of view of what could lie ahead for clients and then communicate that to them. While nothing is ever guaranteed to occur, better to be have formed a view and prepared clients than for both you and your clients to be blindsided.

Think about it

And one final suggestion. In professional practice, with all the day to day commercial pressures, the daily random noise of market news and commentary, dozens of emails and phone calls, and now the pressure of social media marketing, it can be difficult to find the time to give proper consideration to what the data is telling you. Take the time to schedule ‘thinking time’ into your month so you really can get an understanding of what’s really going on in the world. Be that an hour or so or an entire morning, it will be a great investment of time in being able to set clients’ expectations in real terms.

Note: The accreditation for this CPD article is no longer current. Please visit our CPD section for current CPD quizzes.