Bond markets were once the world’s most liquid. Today, trading even $5 million in bonds can be difficult. In the bond market, a narrow bid/ask spread signifies a liquid bond market. The narrower it is, the more liquid the market; conversely, a broad bid/ask spread indicates less liquidity in the market.

In 1986, global bond houses would offer a US$1 billion ‘locked market’ in the most liquid government debt – in other words, bond transactions with no bid/offer spread. According to veteran bond investor Scott Weiner, a Managing Principal with global fixed income house Payden & Rygel, in those days it was common to trade US$1billion of US Treasuries (10 year bonds) in one day.

Fast forward to today where it is often hard to trade as little as $5 million in corporate bonds during market hours on a normal trading day, and bid/offer spreads can vary wildly.

In the bond market, liquidity refers to the ability for buyers and sellers to transact quickly, in volume, with minimal price impact and little price differential between the two sides of the market. For the secondary corporate bond market, the US Treasury has laid out four key components to liquidity. [1]

- Tightness – the bid-ask spreads, or the gap between willing prices for transaction

- Depth/availability – size of transaction absorbable without affecting price, and overall supply

- Immediacy – the speed a trade order can be fulfilled

- Resiliency – ease with which prices return to normal

Why is liquidity an issue?

In an illiquid market, the wide variance of bid/offer spreads can erode returns. Where the yield on a long-dated bond is already at all-time lows, a high spread on either end of the transaction can take that low yield into negative territory. Add in the management fees of an average bond fund, and there is no compelling reason to invest. Investors in managed funds may also find that in an illiquid market, managers hold more cash to ensure they can meet redemption requests. With cash rates at all-time lows – minus management fees – it’s not a compelling story.

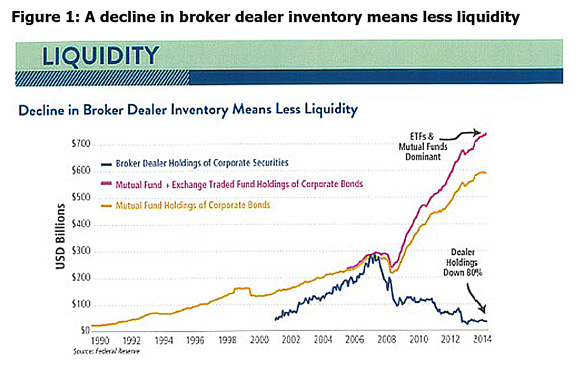

On top of that, scarcity of bonds has resulted in most stock being in the hands of other asset managers rather than broker dealers, the group that traditionally ‘makes the market’ in bond stocks.

But it’s not just the lack of liquidity that’s keeping bond investors awake.

Scarcity

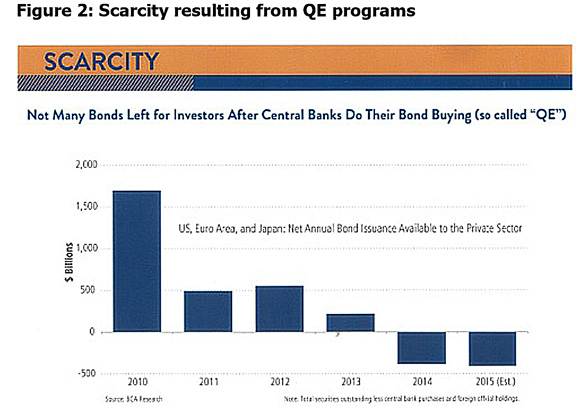

As already eluded to, scarcity is one of the issues impacting liquidity. From December 2008 to 2012, the US Federal Reserve undertook three rounds of Quantitative Easing (QE), during which time it repurchased more than US$1,600 billion in agency mortgage backed securities and agency debt, as well as US Treasuries with six to thirty years’ maturity.

During QE2, at the same time the US Federal Reserve was buying longer-dated bonds, it was a seller of shorter-dated securities. The European Central Bank is now in the throes of its own QE program. As illustrated in Figure 2, there’s little left for investors.

Transformation

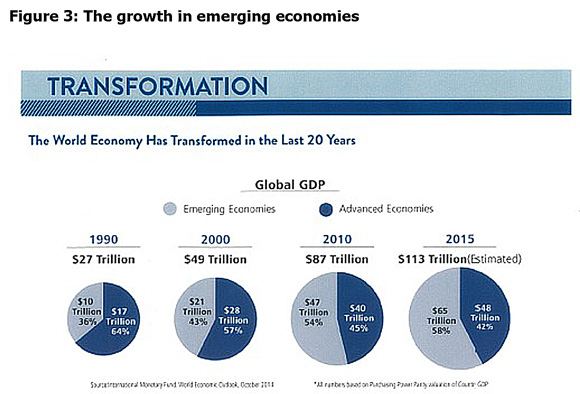

The global investment landscape has been evolving. Emerging market GDP has been growing and, as illustrated in Figure 3, is predicted to outpace its developed markets counterparts this year. At the same time, emerging markets debt has emerged as a discrete asset class. However, not all investment mandates permit investment outside developed markets, putting further pressure on available stock.

Disinflation

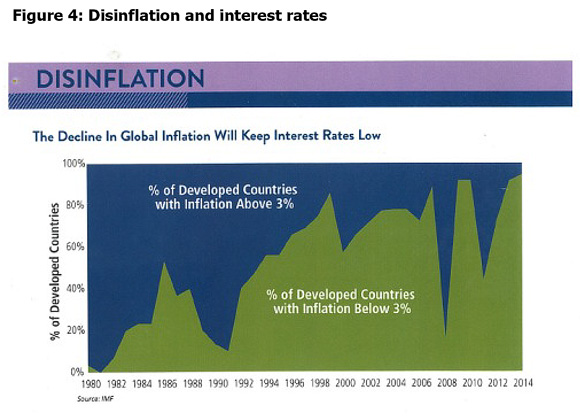

There has been a lot of debate about disinflation – is it a transitory phenomenon or is it here to stay? Historically, when an economy experiences deflation or disinflation, the relevant central bank keeps rates low to stimulate the economy.

A recent presentation by LA-based fixed income investors Payden & Rygel expressed the firm’s view that low inflation is more persistent than the US Federal Reserve has indicated, however does not believe this will necessarily delay an anticipated increase in interest rates, although it may result in a slower cycle of increasing US interest rates.

Managers of traditional benchmark aware bond portfolios have a few good reasons for sleepless nights. It’s hard to get the right stock. Illiquid markets make it harder to transact to fund withdrawals, which can result in funds holding more cash than they might otherwise – and with cash rates so low, that will not add much value for investors.

Traditional bond investors who are typically overweight longer-dated bonds may well be nervous about ongoing disinflation, which will eventually be followed by a tightening cycle that will see them become more exposed to duration and credit risk. At the same time, these investors may be bound by mandates that prevent them from harnessing the opportunities offered by emerging market debt.

The solution is not to avoid fixed income. Rather, search out strategies that can invest in the full spectrum of fixed income assets, of both long and short duration, that can harness the power of the ‘pull to par’ effect as the bond approaches maturity. Strategies with more flexible mandates, that aren’t necessarily bound to long-dated, developed markets securities and that aim to deliver a positive return, whatever the market conditions.

————–

[1] “Assessing Fixed Income Market Liquidity: Presentation to the TBAC (Treasury Borrowing Advisory Committee).” US Treasury. July 2013.