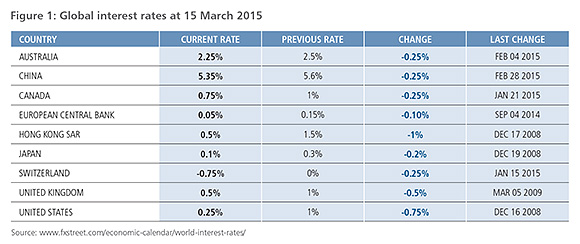

Although there are rumblings from the US Federal Reserve about increasing interest rates, as illustrated in Figure 1, interest rates of most developed economies remain at all-time lows.

The most recent interest rate move in Australia was downward and there is expectation of further cuts in the coming months. While this is great news for those paying off a mortgage, it can spell hardship for retirees reliant on interest income from cash accounts or traditional defensive investments.

Global equities for income?

Global equities generally aren’t top of mind when it comes to investing for income. Consider:

Despite this seemingly low average yield (albeit higher than the current cash rates in the US and UK), equity dividends can be an attractive complement to other forms of income. By focusing on a global equity dividend yield strategy, investors can access a wider opportunity set to capture more dividend-paying companies and higher yields.

What is global equity shareholder yield?

A global shareholder yield strategy is underpinned by the fundamental principle that a business – any business, in any industry and in any geography – has exactly five possible uses of free cash flow (defined as those funds available for distribution to shareholders after all planned capital spending and all cash taxes) to preserve the existing cash-flow-generating capacity of its current collection of assets. The five uses are:

- Invest in organic growth projects that deliver a return on capital above the firm’s weighted average cost of capital.

- Invest in strategic mergers and acquisitions that deliver a return on capital above the firm’s weighted average cost of capital.

- Pay cash dividends to shareholders.

- Retire debt obligations.

- Repurchase shares.

From this perspective, a company that has free cash flow left over after funding all internal and external projects that meet return on invested capital (ROIC) hurdles has a fiduciary obligation to return that excess free cash flow to the owners of the business – the shareholders.

This two-part article will focus on two key components of shareholder yield – dividends (part 1) and share buybacks (part 2).

Are dividends enough?

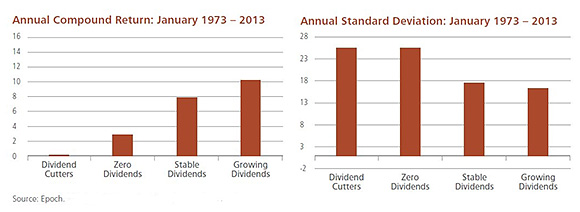

Dividends are back in fashion, with the virtues of dividend payers increasingly highlighted by the financial press. Over long periods, companies that pay dividends have outperformed those that do not. And, as illustrated in figure 2, they did so with considerably less volatility.

Figure 2: Company dividend strategies and effect on risk and return

Considered a sign of corporate health, dividends typically reflect the ability of a company to make money with some consistency. Dividends also indicate that management is attentive to shareholders and confident in the prospects for the business.

However, investors need to understand how the dividend is being paid and where it fits within the capital allocation policy. Otherwise, the blind pursuit of dividends for their own sake can be financially hazardous.

Investors need to know where dividends come from. Are they getting a return on their capital, or a return of their capital?

The only way to be sure is to learn how much free cash a company generates. The next, and more difficult, step is to gain confidence that cash can be produced with transparency and consistency. Another readily seen example of a pitfall for dividend strategies is the emphasis on financials prior to the Global Financial Crisis in 2008.

Investors searching for dividend yields in a low-yield environment were attracted to equities. At the end of 2007 the US financial sector had a dividend yield of 3.4% compared to a dividend yield of 2.0% for the entire S&P 500 Index. Similarly, global financials had a dividend yield of 3.6% compared to a dividend yield of 2.4% for the entire MSCI World Index (source: Epoch Investment Partners). These yields attracted equity investors and caused them to overlook the lack of transparency in how cash was generated.

Investors also need to consider if a dividend is the best use of cash. Effective CEOs and CFOs weigh the benefits of returning cash to shareholders against internal reinvestments and potential acquisitions as part of a capital allocation strategy.

If projected returns for reinvestment or acquisitions exceed the firm’s cost of capital, then they should make those investments. If they do not, then excess free cash flow should be returned to shareholders.

To sum it up, there are only five possible uses of corporate cash: reinvestment, acquisitions, dividends, share repurchases and debt pay downs. Reinvestments and acquisitions should be pursued if the firm expects a return higher than its cost of capital.

Otherwise, the best use of cash is to provide shareholder yield. All three forms of shareholder yield — dividends, share buybacks and debt repayments — are effective forms of returning wealth to shareholders. Each adds more or less value at different points in an economic cycle.

Adopting a broad view by taking all three into consideration can be more rewarding than only focusing on one. Companies that provide shareholder yield, as a result of growing free cash flow and intelligent capital allocation, should outperform over most of the economic cycle.

The following video features the pioneer of the global equity shareholder yield strategy, a unique strategy that can enable investors to derive an above average yield from global equity investments. Bill Priest is the CEO, co-CIO and a Portfolio Manager with Epoch Investment Partners, and author of Free Cash Flow and Shareholder Yield: New Priorities for the Global Investor, which details the underpinnings of a global equity shareholder yield investment strategy. His colleague Eric Sappenfield, Managing Director and Portfolio Manager, also discusses the strategy.

http://www.eipny.com/index.php/S=0/epoch_insights/videos/highlights/shareholder_yield

———-