Consumer spending in the euro area is now growing at its fastest since 2007. Lower oil prices have helped but are only part of the story, in our view. There’s also been a steady improvement in labor income growth and consumers are finally willing to borrow again. Both factors should underpin consumption, and the recovery more generally, when the boost from lower oil prices starts to fade.

With sluggish emerging-market growth damping the stimulus from a weak euro, the euro-area recovery is unusually dependent on consumption. Fortunately, recent data suggest the consumer revival is still on track and we think there are good reasons to expect the positive trend to continue.

This is true even though data released this week showed car registrations tracking sideways in the second quarter. In our view, this should be seen in the light of the strong gains posted in the previous two quarters, when registrations rose by a combined 6.6%. Not to mention the fact that June’s reading was the highest since December 2011 and 18% above the low reached in January 2013 (though still 23% below the precrisis peak).

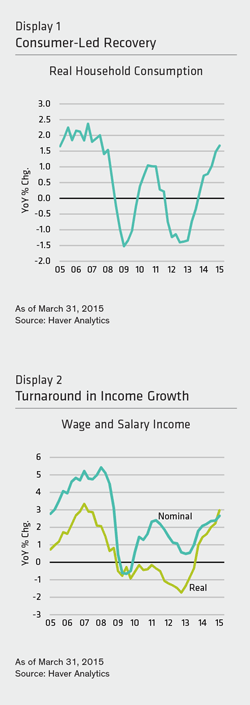

In addition, retail sales remain on a steady upward track, with the April/May average 0.6% higher than in the first quarter. All told, we expect consumer spending to post another solid gain of 0.5% in the second quarter. If this is correct, it would push annual growth up from 1.7% in the first quarter of the year to 1.9% in the second—the fastest growth rate since the third quarter of 2007 (Display 1).

Not Just About Oil

It’s tempting to assume that the recent pickup in consumer spending is all about oil. But it’s not. Clearly, the lower oil price has been an important factor in recent months, helping to propel real wage and salary income growth up to an annual 3.0% in the first quarter, very close to the precrisis high (Display 2). But the turning point for consumption happened long before the collapse in the oil price. And it was underpinned by a recovery in nominal wage and salary income growth, which has risen from 0.5% in the first quarter of 2013 to 2.7% now.

The bulk of this improvement has been driven by a turnaround in employment growth—contracting at an annual rate of 0.9% at the beginning of 2013 but rising by 0.8% now. However, there are also signs that wage growth is starting to pick up. And not just in Germany. Even in the periphery, where wage growth has been under intense downward pressure in recent years, there are signs that wage growth is finally creeping up.

Borrowing Returns

The recovery in consumer spending has also been supported by a pickup in credit growth. In the first five months of the year, consumer credit increased by €3.2 billion, compared with a decrease of €2.9 billion in the same period last year and €8.1 billion in the first five months of 2013. In annual terms, the growth rate of consumer credit remains quite soft, at 0.5% in May. But this is the fastest growth rate since March 2009 and a big improvement on the sustained declines seen in the interim.

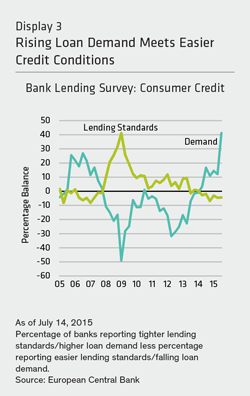

The recent improvement in credit growth suggests that consumers have become less cautious and are finally willing to borrow again. There is strong evidence to support this in the European Central Bank’s latest bank-lending survey. Not only does this show that banks have loosened lending standards significantly in recent quarters—thus boosting the supply of credit—but also that the demand for consumer credit has shot up to the highest levels since this survey began in 2003 (Display 3).

The recent improvement in credit growth suggests that consumers have become less cautious and are finally willing to borrow again. There is strong evidence to support this in the European Central Bank’s latest bank-lending survey. Not only does this show that banks have loosened lending standards significantly in recent quarters—thus boosting the supply of credit—but also that the demand for consumer credit has shot up to the highest levels since this survey began in 2003 (Display 3).

So while the decline in the oil price has clearly provided an important boost to euro-area consumption, it’s certainly not the whole of the story. There’s also been an improvement in underlying fundamentals which should underpin consumption, and the recovery more generally, when the boost from the oil price starts to fade.

By Darren Williams, Senior European Economist, Global Economic Research, AB

———