William Priest, CFA – CEO, Co-CIO and Portfolio Manager at Epoch Investment Partners, Inc. (Epoch) provides his insights on why the current market environment may be detrimental for passive investors. Epoch is the investment manager of the Grant Samuel Epoch Global Equity Shareholder Yield Funds.

On an October Sunday many years ago, when my family lived in the leafy New York suburb of Union County, New Jersey, I was driving to a civic event, and likely to arrive a bit late. I started to make the left turn into the parking lot, but to see just how late I might be, I glanced to my right to see if people were still waiting outside the building. Thus distracted, I banged into a large bucket filled with concrete, holding a sign that prominently read: “NO LEFT TURN ON SUNDAYS.” A traffic cop, a very good-natured one, slowly walked my way and asked, “How big a sign do you need, fella?”

That moment comes back to me when I observe strange situations, with flashing red lights and other “danger ahead” signals that no one seems to notice. Today’s markets present two such prominent signs, which lead us to draw up a sign of our own, on the debate over the merits of passive investing.

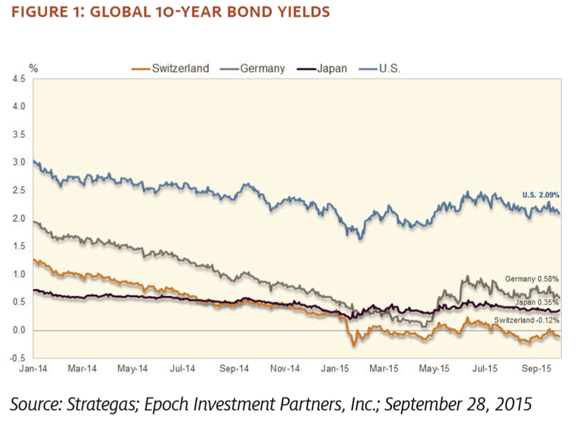

We start with a comment from James Grant, published in the May 15th issue of Grant’s Interest Rate Observer. “Great bond bull markets don’t come around all the time,” he notes: “In fact, there have only been three in America over 150 years — 1865 to 1900, 1920 to 1946, and 1981 to the present.”

In words too precious to paraphrase, he states: “In the nature of things, bull markets end at extremes of valuation…marked by the metallic scraping sounds of conservative fiduciaries searching for suitable income-producing investments in the bottoms of barrels… In no previous modern interest-rate cycle did short-dated sovereign yields make their lows at less than zero or the 10-year German Bund touch its low at just five basis points above zero.”

To which we add — in the lingo of traders — if this pricing is not nuts, it is certainly abnormal, and qualifies as a “danger ahead” sign (Figure 1 below).

Grant illustrates with a case study on the dangers, ex-post, of reaching for high yield in a market of zero interest rates:

“On the systemic mispricing of debt”[1] – How a $50 million loan to RadioShack turned into an $81 million gross impairment was the featured topic on the May 7th earnings call of Fidelity & Guaranty Life of Des Moines, Iowa (FGL on the Big Board).

Stage one was that $50 million plain-vanilla credit, the company explained. Stage two involved a $63 million equity tranche in a collateralised loan obligation, of which a certain portion was invested in RadioShack debt — nothing vanilla here.

Stage three concerned a $33 million investment in a reinsurance vehicle that also came equipped with RadioShack exposure. Diallers-in listened as chief financial officer, Dennis Vigneau, summed things up.

“Following extensive evaluation analysis…,” said Vigneau, “the $50 million loan participation was impaired by $35 million, or 70% to a fair value of $15 million. Next, the $63 million CLO investment, which was partially exposed to RadioShack, was impaired by $25 million, or approximately 40%, to a fair value of $38 million. And lastly, the $33 million preferred stock investment… was impaired by $21 million, or 64%, to a fair value of $12 million. In total, these impairments were $81 million gross….”

Fidelity & Guaranty Life, an off-shoot of the old U.S.F. & G., of Baltimore, is the firm that “helps middle-income Americans prepare for retirement,” or so claim its copywriters. If so, the life insurer’s investment department, with its RadioShack trifecta, itself needs help. Certainly, it gets none from the world’s central banks — or, as far as that goes, from the post-1981 interest-rate zeitgeist.

The second danger sign comes to us from the fast lane of the equity markets – a broker’s research note to which financial history may assign the label “What were they thinking?” (Readers over 50 years of age will likely nod in agreement with our assessment; those under 30 may think we are nuts.)

Tesla Motors, a maker of high-priced electric sports cars, shows no current profits – a trend its management seems confident will continue through this decade. Hungry markets have nonetheless handed over huge sums to finance Tesla’s hungry operations, including an August equity offering for over $700 million[2], after debt and equity sales in May 2013 of about $1 billion.[3]

In response to the first quarter 2015 earnings conference call of Tesla Motors, Adam Jonas, Morgan Stanley’s chief analyst of the industry now known as “Autos and Shared Mobility,” doubled down on his overweight opinion on the stock, and posted a price target of $280 per share (versus its price then of $237, and $260 on September 17th). Pay special attention to one line bolded at the end of the first paragraph.

…If we were to go back in time two years and tell you that in 2015 Tesla would be burning nearly $1.5 billion of cash and have all but ruled out GAAP profitability before 2020, we might have forgiven you if you thought the stock could be well below $100/share…Elon and the team may be getting by on monetizing the imagination of the investment community. But the thing some may be underestimating is: Imagination is real.

…Demand for Tesla’s stationary storage products has been “crazy off the hook” in the first five days following the introduction. These products may not have any meaningful contribution to Tesla’s revenue for at least two or three years – but this may not stop analysts from attributing many billions of dollars to the company’s long-term valuation…

…It is clear to us that there is nearly a uniform acceptance of the situation and a calmness and confidence around the company’s ability to address cash needs…

…Cash burn of $558mm… was well above our forecast of $330mm of burn in the quarter… with the rest due to a substantial rise in working capital including rising in-process inventory. The inventory rise may need further explanation to investors who could equate the development with slowing demand for Model S…

…A successful launch/ramp [of the Model X] into 4Q can make a very significant difference in determining whether Tesla burns $1bn this year (we think a best case) or more than $1.5bn this year (a bear case). In any case, we believe Tesla may find a capital intervention desirable if not absolutely necessary…

…We’d strongly advise investors to take down 4Q and full year deliveries to allow for greater execution risk for Model X…

…Easily two thirds of the call was devoted to Tesla energy, Powerwall, and the stationary storage opportunity. This is great, but it potentially masks some very important up-front liquidity needs of the company that investors will want to pay very close attention to…[4]

Tesla Motors may have ambitious plans, but behind this buy recommendation lies a company with enormous cash flow challenges, both present and future. The greatest support the analyst seems to have for his bullish case is that “Imagination is real.” He must be kidding us. Cash flow is real; one cannot spend imagination.

Returning to James Grant, he states: “The mispricing of biotech stocks or corn and soybeans is of no great consequence to financial at large. Interest rates are another matter. Universal prices, they discount future cash flows, calibrate risk and define investment hurdle rates. Interest rates are the traffic signals of a market economy… and since 2008, they have mainly been green.”[5]

Seven years of low interest rates have heavily influenced corporations’ capital allocation. Recall that there are only five possible uses of free cash flow, and they can be placed into two buckets — capital reinvestment and capital returned to shareholders.

Cash dividends, share buybacks, and debt repayments are all forms of the latter. Low interest rates encourage corporations to borrow and apply the proceeds to buy back shares — an opportunity that prudent managements should take advantage of, assuming the rate math works and they lack promising projects to invest in.

Accordingly, this year’s share buybacks and cash dividends of US corporations will likely exceed $1 trillion — over 6% of US GDP. Merger and acquisition activity is startlingly high as well: through September 18, the value of global deals over $10 billion reached $1.19 trillion, surpassing the previous record set during the internet bubble in 1999.[6]

The parade of M&A activity will surprise everyone as this year winds up, pushed to such heights by our central bankers (many of whom are on the short lists to join banks and investment firms, after completing their tours of “responsible duty”).

Now we turn to a story of low interest rates with what we expect will be a more constructive outcome. Consider the August acquisition of Pall Corporation, a maker of filtration products, by technology company Danaher Corporation. On the surface, Danaher paid what appeared a ridiculously high price, but seen through the lens of its cost of capital, their decision is likely to have a very positive outcome.

Danaher estimated its marginal cost of capital for this acquisition to be around 2%, and anticipated the prospective return of the acquisition to approximate 9%. Thus this deal is accretive to the firm’s valuation for the incremental return on the capital deployed exceeds the firm’s marginal cost of capital. This transaction extends Danaher’s outstanding record of value-enhancing acquisitions.

Stories of high-yield train wrecks and buy recommendations founded on imagination bring us to our own warning sign, regarding passive investing. More than half of the return of the S&P 500 for the three years ending in December 2014, and more than 75% of the return to the MSCI World index, were brought about by an expansion in price-earnings ratios, rather than increases in earnings or cash flow. And what was the force pushing those valuations higher? Low interest rates fuelled largely by quantitative easing, of course.

We drive our stake into the ground. We at Epoch are firm believers in active investment, because our clients have won over time, in terms of both total return and risk-adjusted return. With the global economy faltering once again, the markets may be about to enter another one of those periods where stock selection is crucial, and naysayers on the value of active management may see their passive portfolios underperform for a while, perhaps substantially.

Understanding the principles of capital allocation, and finding the winning firms that know how to create shareholder value, will win. Knowing where the potholes lie will be even more valuable in a difficult market.

Now, it’s probably not fair to condemn all of passive investing with two extremes-of-the-markets anecdotes like RadioShack and Tesla. (And at the moment, only Tesla is in the Russell 1000; RadioShack is off the radar.)

But keep in mind the basic principle of indexing: an investor has a bit of every company, irrespective of its fundamentals. Case in point: at the end of August, in the MSCI USA Investable Market Index, which includes the 2,500 largest US stocks, 18% of companies had shown negative earnings per share for the latest twelve months. (That’s after a fairly long economic expansion, when companies should be looking their best.)

Through indexing an investor can wind up owning a lot of undesirable names which an active manager would be likely to screen out. My partner and co-CIO David Pearl states a simple truth: “A company with little or no debt that generates free cash flow each and every year cannot go broke.”

However, “broke” will be embedded in the future of those passive strategies that invest in everything under the sun – including the effects of QE in the search for yield, and the level of the market’s “imagination.”

Notwithstanding the Fed’s decision to wait on raising interest rates, P/E ratios are likely to retrace some of their rise in the 2012-2014 period, reflecting slower global growth and/ or eventually a rise in interest rates. Investors will need more than just passive management strategies to stay ahead.

———–

[1] Grant’s Interest Rate Observer, Vol. 33, No. 10, May 15, 2015.

[2] “Tesla’s tally from stock offering: $738.3 million,” MarketWatch, August 19, 2015

[3] “Tesla Motors raises more than $1 billion from debt, equity,” Reuters, May 17, 2013

[4] Tesla Motors Inc: ‘Off the Hook’: More Money, More Spending, More TAM, Morgan Stanley, May 11, 2015

[5] Grant’s Interest Rate Observer, Vol. 33, No. 10, May 15, 2015.

[6] “Value of megadeals this year beats dotcom-boom record to reach $1.2 trillion.” Financial Times, September 19, 2015.

———-