Concerns that food and oil prices may soon reverse their downtrend, potentially derailing a nascent monetary easing cycle in Asia, are likely overdone. Central banks, in our view, are likely to remain focused on the downside risks to growth, given the slackening domestic demand and sluggish exports.

In our view, though, slackening domestic demand in most economies suggests that there wouldn’t be much second-round transmission of inflation, even if oil and food prices were to rise. Central banks are likely to look beyond any noises in the consumer price index (CPI) and view the slowdown in economic growth as a more pressing issue in the coming quarters.

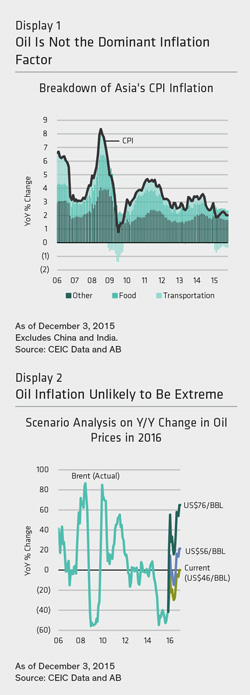

Oil Is Not the Dominant Factor

Of the two potential inflation-igniting factors, crude oil may be more prone to higher volatility in the months ahead owing to the geopolitical uncertainties in eastern Europe and the Middle East. However, oil prices, on their own, are unlikely to reverse the disinflation trend.

Looking into the components of inflation in Asia, oil prices—more broadly categorized as “transportation costs” in the CPI basket—have not been the main driver of headline inflation in the past (Display 1).

In fact, oil has contributed less than one percentage point to CPI inflation since the global financial crisis, although its weakness in recent months has trimmed about 0.5 percentage point from CPI inflation. A simple scenario analysis shows that even if Brent crude oil rebounds to US$76 per barrel—the top end of the market’s expectation—its inflationary impact would only be similar to that in 2011, when it added about 0.7 percentage point to the headline CPI (Display 2).

Meanwhile, if Brent stayed at US$56—the median forecast in the market—its impact on the CPI would be marginal. If Brent stays at the current level of around US$46, it will remain a drag on the CPI for most of 2016. Overall, the net effect of oil prices on the CPI is likely to be modest in the months ahead.

Food inflation could have a greater impact on Asia’s CPI inflation owing to the composition of the price index in most countries.

The market has been wary of El Niño—a meteorological condition caused by oscillations in ocean surface temperatures—since the second quarter. Indeed, the El Niño/Southern Oscillation (ENSO) index has hovered at elevated levels.

But, as we discussed earlier in the year, any impact on food inflation depends on the microclimate of the crop growing regions. There is no direct relationship between the ENSO index level and the severity of food inflation. Moreover, crop inventory is more abundant than during the past episodes of food inflation (see “Too Early to Worry About El Niño as Downside Risks to Growth Persists,” Asian Perspectives, July 17, 2015).

The potential impact of warm and dry weather on food costs is worth continued monitoring. But in recent months, prices of key crops such as rice, corn and wheat have drifted lower, reflecting the receding risks to supplies. Also, food prices in Thailand have declined again, dragging down CPI inflation, after a brief rise due to a drought over the summer.

Weak Demand in Focus

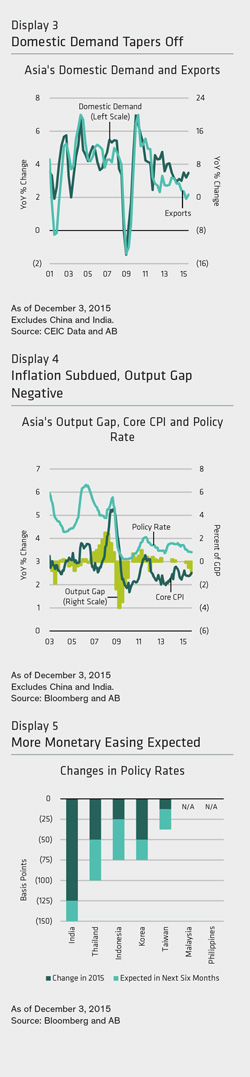

The big difference between now and 2011—when a jump in food and oil prices prompted a monetary policy response—is the trajectory of domestic demand, as the economies today are in a very different growth-cycle stage. With a debt overhang and fiscal conservatism prevailing in a number of Asian countries, domestic demand growth has continued to taper off in recent years. Many countries are also seeing their manufacturing sectors come under pressure from slower exports (Display 3).

From the monetary authorities’ perspective, core inflation remains at cyclical lows (Display 4), and the negative output gap has been widening—implying that their economies are running below their potential growth levels. Therefore, central banks are likely to look beyond any short-term noises in the headline CPI and keep growth their priority.

Bottom Line

All in all, slackening growth and subdued core inflation should remain supportive of local-currency bond markets. We believe that the monetary easing cycle in Asia has more room to run, especially in Thailand and Indonesia (Display 5). The key uncertainty is the potential currency market volatility that may result from an interest-rate increase by the US Federal Reserve, which could dampen foreign investors’ appetite for exposure to Asia’s local-bond markets.

By Vincent Tsui, Economist, Global Economic Research and Anthony Chan, Asian Sovereign Strategist, Global Economic Research, AB

———-