Investment markets and key developments over the past week

Share markets mostly continued to move higher over the last week as growth fears from earlier this year continued to recede and the oil price managed to push higher despite the failure of OPEC and Russia in Doha to agree a production freeze. The pace of gains in US shares slowed but European, Japanese and Australian shares played catch-up with the Australian share market almost getting back to where it ended 2015. Chinese shares fell though on concerns that there won’t be more policy stimulus. Reflecting the “risk on” tone bond yields continued to move higher, most commodity prices rose and the $A reached $US0.78. Even the iron ore price has now hit $US70/tonne – what happened to the global steel glut?

The ability of oil and share markets to rally despite the failure of key producers to agree an oil production freeze is a positive sign. The Doha meeting was mainly about appearances anyway with Saudi Arabia and Russia already at capacity, Iran never likely to participate and many other factors driving the rebound in oil and growth assets since the panic of earlier this year. Regardless of the Doha debacle the oil market is gradually rebalancing as global oil demand slowly climbs and other producers, including the US, are slowing supply.

While we remain of the view that the broad trend in share markets is likely to remain up, the next scare is likely to come as Fed hikes return and bond yields continue to back up, pressuring equity valuations. Markets cycling back and forth between deflation/growth scares and then higher bond yields/Fed scares has been the story of the last few years now!

The New York presidential primary victories for Hilary Clinton and Donald Trump further cement the former as the Democratic presidential candidate but still leave Trump open to challenge at the Republican convention in July. Trump needs to win 53% of remaining delegates to the convention to get a majority but so far he has only been winning 49% so a contested convention could still occur. Interestingly so far he’s only been getting 38% of the popular vote at the primaries so he is still getting less than majority support. The next set of GOP primaries are on April 26, but the June 7 California primary with its 172 delegates may end up being key. So a long way to go yet.

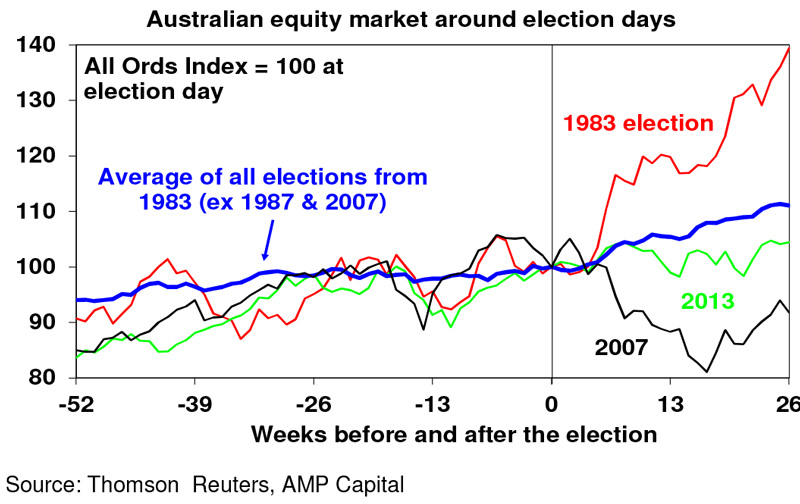

Australia is another step closer to a July 2 double dissolution election with constitutional triggers now in place. Of course it won’t be declared till just after the May 3rd Budget, but just like in 2013 when the election date was announced way in advance (albeit to be changed later) we are now in another longer than normal de facto election campaign. It’s too early to talk precise policy differences between the two alternatives – but it is clear that the Labor Party will focus more on budget repair via various tax hikes (restricting negative gearing, super and the capital gains tax discount) and while the Liberal/National coalition will have a bit of that too it will mainly focus on spending restraint. However, in terms of the near term impact of the election itself the risk is that some spending decisions by households and businesses are put on hold through the election campaign – with a higher risk for long de facto campaigns like this one. Qantas has already suggested this may be happening. However, there is no clear evidence that election uncertainty effects economic growth in election years as a whole. Since 1980 economic growth in election years has averaged 3.7% which is greater than average growth of 3.2% over the period as a whole. That said, growth was below average at 2.3% in 2013 which also saw a long de facto election campaign. In terms of the share market, there is some evidence of it tracking sideways in the run up to elections but on average it has gained 4.9% in the three months after elections – so it’s good to get them out of the way.

It’s hard to disagree with RBA Governor Glenn Steven’s view that there are limits to what monetary policy can do. Monetary policy can help offset cyclical fluctuations in growth but it can’t solve the so-called “secular stagnation” phenomenon. There is a role here for government in removing impediments to growth (supply side reforms of the sort the G20 summit in 2014 supposedly committed too) and encouraging investment in productive assets. The trouble for central banks though is that their mandate is to achieve certain inflation targets over time – usually around 2% – and when these look like being chronically missed on the upside or the downside they invariably have to intervene. Which is what they have been doing in recent times and why “helicopter money” (ie using printed money to directly finance government spending/tax cuts) is being talked about in some countries where other monetary policy options have been exhausted, Japan being a noticeable example. Fortunately we are a long way from that in Australia, where if inflation looks like coming in under target for a lengthy period (which is a risk now) there is still plenty of scope for conventional monetary easing.

Major global economic events and implications

US housing data was a mixed bag with falls in starts and permits but solid readings for home builder conditions and existing home sales. Other US data was also mixed with a fall in manufacturing conditions in the Philadelphia region, but gains in home prices, leading indicators and another fall in jobless claims. March quarter earnings results showed 82% of companies beating on earnings and 59% beating on sales with 25% of S&P 500 companies having reported so far.

No surprise after its huge March effort to see the ECB on hold at its latest meeting, with President Draghi pushing back against German criticism and indicating that it remains ready to do more if needed. Meanwhile, the ECB’s bank lending survey revealed little change in lending standards but solid growth in loan demand.

Chinese property prices continued to increase in March led by Tier 1 cities. While this is consistent with other indicators of improved growth in China, it also warns of renewed measures to slow bubble fears in some Chinese cities.

Australian economic events and implications

It was a quite week on the data front in Australia. Skilled vacancies did fall in March though for the second month in a row suggesting jobs growth may start to slow but too early to read too much into this.

What to watch over the next week?

In the US, the key focus will be on the Fed (Wednesday) which is very unlikely to raise interest again rates again just yet, but may try to start warning the market that another hike is in prospect for the June or July meetings consistent with its dot plot signalling two hikes this year. Recent comments from Fed Chair Janet Yellen stressing caution in raising interest rates suggests that there is close to zero chance of a hike in the week ahead. However, market pricing of just 20% probability of a June hike and just 34% for July seem too low and the Fed may try to raise these probabilities a bit. That said the combination of risks in June around Brexit and Greek debt relief negotiations suggest the Fed may choose to avoid any hike in June.

On the data front in the US expect a gain in new home sales (Monday), a rebound in durable goods orders, continued gains in home prices but flat consumer confidence (all Tuesday), March quarter GDP growth of just 0.5% annualised (Thursday), growth in employment costs remaining low at around 2%yoy, and a slight fall in inflation as measured by the core consumption deflator for March to 1.5%yoy (both Friday). While March quarter GDP growth of just 0.5% annualised is very low just bear in mind the seasonal distortion over the last 20 years that has seen March quarter growth average just 1% annualised followed by June quarter growth of 3% on average. March quarter earnings reports will also continue to flow.

After the Fed on Wednesday the focus will shift to the Bank of Japan (Thursday) where there is some chance of further easing or at least a dovish bias given recent strength in the Yen, soft growth and inflation readings and the recent earthquake. Japanese data for inflation, household spending and industrial production will also be released on Thursday.

Eurozone March quarter GDP (Friday) is likely to show growth of 0.4%qoq, economic confidence data (Thursday) is expected to show a slight improvement after slipping in March and inflation is likely to have remained low in April (Friday).

In Australia, the focus will be on March quarter CPI inflation (Wednesday) which is expected to show an increase of just 0.3% quarter on quarter or 1.8% year on year as lower petrol prices and ongoing weak pricing power offset seasonal increase in prices for health and education. The underlying measures of inflation are expected to rise by 0.5% qoq or 1.9% yoy. Inflation continuing to run at or below the low end of the RBA’s target zone is one reason why we expect another RBA rate cut this year but it would need to be significantly weaker than expected to drive a May rate cut. Data for export and import prices, producer prices and credit will also be released.

Outlook for markets

Expect short term share market volatility to remain high as we head into May (“sell in May and go away, come back on St Leger’s Day”) and the Fed eventually starts to soften markets up for another rate hike. However, beyond near term volatility, we still see shares trending higher this year helped by a combination of relatively attractive valuations compared to bonds, further global monetary easing and continuing moderate global economic growth.

Very low bond yields point to a soft medium term return potential from them, but it’s hard to get too bearish in a world of fragile growth, spare capacity, weak commodity prices and low inflation. Bonds in higher yielding countries like Australia, the US and China are relatively attractive.

Commercial property and infrastructure are likely to continue benefitting from the ongoing search by investors for yield.

National capital city residential property price gains are expected to slow to around 3% this year, as the heat comes out of Sydney and Melbourne. Prices are likely to continue to fall in Perth and Darwin, but price growth is likely to pick up in Brisbane.

Cash and bank deposits are likely to continue to provide poor returns, with the RBA expected to cut the cash rate to 1.75%.

The ongoing delay in Fed tightening and stronger data in Australia pose further short term upside risks for the $A, possibly up to $US0.80. However, any further short term strength in the $A is unlikely to go too far and the broad trend is likely to remain down as the interest rate differential in favour of Australia narrows as the RBA eventually resumes cutting the cash rate and the Fed eventually resumes hiking, commodity prices remain in a secular downswing and the $A undertakes it’s usual undershoot of fair value.

By Shane Oliver, AMP Capital