Not long ago, negative interest rates were a novelty. The idea that an investor might pay someone to borrow their money was viewed as both radical and nonsensical.

Today, ultra-low, or negative interest rates have become the norm in many developed markets. More than $12 trillion of bonds yielded less than zero at the beginning of September 2016. The journey has produced stunning returns, as lower rates have propelled bond prices higher. But like so many journeys, the destination – characterised by low rates, slow growth and paltry potential returns – is a much less inviting place. Market participants are witnessing their historical framework upended and losers will greatly outnumber the winners as the positive effects of low rates fade.

Sovereign bond returns, both in nominal and real terms, will be lower. Indeed, investors in negative yielding bonds are virtually guaranteed a negative nominal return on securities held to maturity. Also troubling for investors are the reasons for today’s low yields. Markets have largely given up on a rebound in growth, instead pricing in a prolonged period of weak productivity and unexciting prospects. And although we find bonds to be overvalued, the “lower for longer” argument remains deep-rooted and may not be reversed for some time. If low rates are a persistent feature, just who are the biggest losers? The groups most harmed by today’s unprecedented policies include the following:

- Savers, as both lower income returns and the slower pace of compounding will sharply reduce future returns.

- Life insurance companies, as many have made return promises in excess of market yields.

- Pension plans, as lower discount rates are forcing funding gaps to balloon.

- Investors seeking portfolio diversification, due to the dissipating potential of bonds to provide effective diversification as yields approach a zero percent lower bound.

- Policymakers, as rates have approached levels that reduce the effectiveness of traditional monetary policy tools.

Savers face a new reality

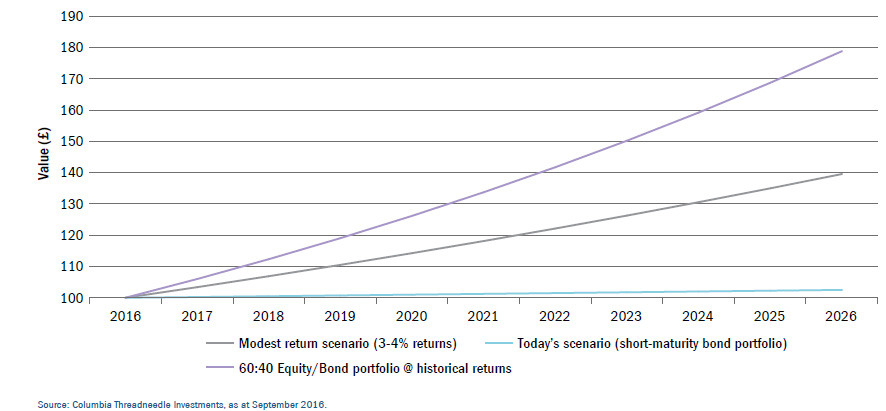

Although falling yields can produce robust returns from bonds, permanently lower yields do not. Too often, this is viewed only in a short-term context. An important corollary to ultra-low returns, however, is that the magic of compounding disappears. Savers are underappreciating the impact of replacing the “miracle of compounding” with the “curse of compounding”. They are making faulty assumptions that returns will normalise, allowing a repeat of the 6-8% returns of yesteryear. They further fail to recognise that a persistent low return environment hinders not only annual returns but destroys the cumulative effect of savings. For those that put aside $25,000 and earn a return of 8% per year, the value of those savings will grow to $79,300 in 15 years, assuming returns are reinvested. But that same $25,000 earning only 3.5% per annum grows to only $41,800 in the same period. And for those investors sticking to the safety of short-dated bonds, returns will be <1.0% in most sectors. The nest egg in 15 years will have grown to only about $28,000, and it would take more than a century for assets to double!

The curse of compounding: Low rates will undermine the virtues of saving

Growth in the value of £100 under different rates of return

Return expectations have not adjusted to this new reality. Investment frameworks still reflect a belief that returns will revert to long-term averages. This is inconsistent with starting valuations, the level of potential GDP growth and productivity, and the already sky-high profit share of GDP. Investment returns are likely to be materially lower in the next two decades.

What does it mean?

Savers will need to save more and work longer. Assuming an equity return profile more in line with nominal global growth of 4 to 6%, an average worker will need to work for another ten years to accumulate the same nest egg as before. The make-up of investment portfolios will also change. A demand for greater flexibility, a focus on loss mitigation will all feature in investment plans, allowing for an array of new products.

Insurance companies: a recipe for trouble

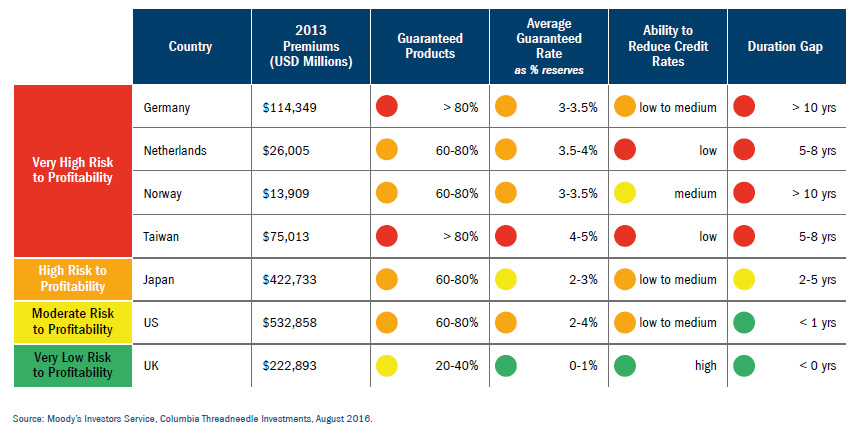

The following is not a good business model: 1) offer savers a guaranteed income return; 2) build in little ability to walk away from, or alter the terms of, those promises; 3) maintain a large maturity mismatch, in which the length of the guarantees exceeds the average length of assets; and 4) watch interest rates tumble to record lows. Sadly, this is what many in the life insurance and annuity businesses have done, and they emerge as an industry heavily disadvantaged by today’s rate environment. Life companies in Germany, the Netherlands, Norway and Taiwan are in a particularly difficult situation.

Life insurers face significant headwinds

Levels of risk in major life insurance markets

What does it mean?

In a best case outcome, life and annuity companies will experience lower profitability and ROE. A more likely case is that we begin to see insolvencies rise amongst smaller and weaker players. We expect 10-20 business failures per annum over the next two years. This should not create a crisis, but it will lead to lower returns and occasional stress in a systemically important industry.

Pensions are licking their wounds

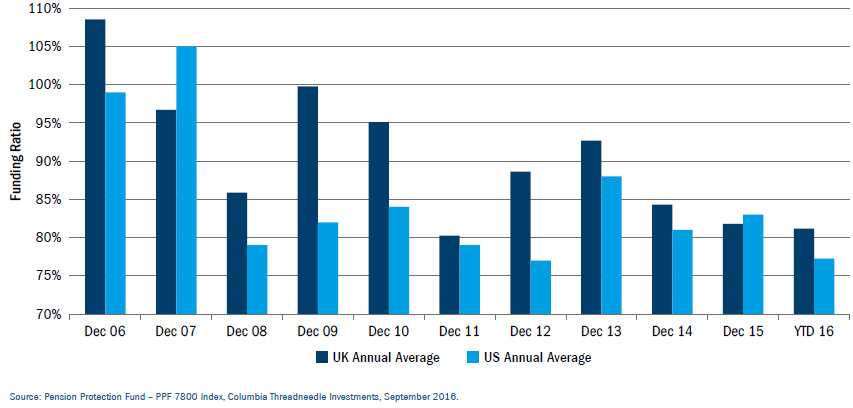

Plunging rates have exposed the underfunded status of defined benefit pension plans. Pensions are designed to cover a liability stream in which they pay retirees fixed sums, often for long periods of time. This is easy to offset by purchasing long-dated assets that generate a similar, or higher, income stream. This model breaks down if pension plans own too little bond risk and rates fall, which is precisely what has happened. Lower rates have boosted the present value of liabilities more than assets have risen, leaving pensions underfunded. Across markets such as the UK and US, more than 75% of pension plans find themselves with liabilities in excess of assets. The gap closed Q3 at record levels.

Pension liabilities are rising much more quickly than assets

Funding Ratio (assets/liabilities)

This understates the problem. Many non-corporate plans are in even worse condition and the use of unrealistically return expectations and overstated discount rates is widespread. Adopting realistic assumptions paints a picture in which US corporate pensions are underfunded to the tune of $600 billion. UK corporations, following the post-Brexit plunge in rates, are in a £960 billion hole on a full buy-out basis. US public pension plans likely face a mammoth $3.3 trillion shortfall, assuming plausible numbers.

What does it mean?

A pension crisis is lurking, but the near-term risk appears manageable. Unfunded pension obligations are akin to other liabilities such as debt, and companies are effectively becoming more levered through the deteriorating funding status. The bad news is that this issue is now large enough to remain an important factor in driving equity and bond valuations. It also portends the occasional failure of struggling companies without outsized pension holes. The good news is that most of these liabilities do not come due for years, relieving near-term pressures. The crisis, like most debt crises, will likely explode in the next recession. A decline in profits will further weaken pension-adjusted leverage metrics, and equity holdings within the pension plan will likely decline, exacerbating the pain. On the public side, bankruptcy is likely to become a more compelling option, requiring careful selection within the municipal bond arena in the years to come.

Seeking traditional portfolio diversification?

Count yourself among the losers

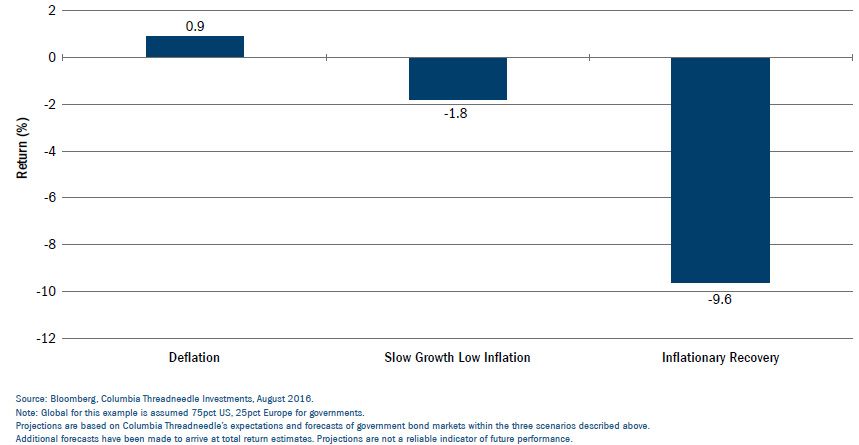

Investors seeking a diversified, risk-managed portfolio have typically looked to fixed income to provide diversification and balance holdings of equities and other risky assets. Bonds tended to move higher in value when risky assets moved lower. With rates so low, there is limited ability for rates to fall still further. This weakens the role of bonds as a hedging instrument. The chart below illustrates likely total returns for G4 government bonds under different economic scenarios:

Strong returns: You can’t get there from here

Twelve-month total return projections for G4 government bonds

Yields at zero simply do not offer the potential for strong returns. If you are looking for good returns from high-quality bonds, you can’t start from here. And if the equity portion of your portfolio declines by 20%, it will not be possible for fixed income to do the heavy lifting.

What does it mean?

Investors will focus on making their bonds work harder. This requires higher-risk portfolios designed to extract true alpha. It will likely mean the “search for yield” continues. It should ensure a continued focus on flexible products, multi-asset products and solutions that combine risks in a more intelligent way. Finally, it means that the widespread belief in the traditional balanced portfolio may prove to be disappointing. A portfolio of 60% equities and 40% bonds, for example, may not provide the diversification expected in a severe market correction.

Central banks miss their target

Central banks are running out of ammunition. They have cut interest rates but have failed to resuscitate growth. Central bank options are clearly limited, and even those that are available are likely be highly unpredictable. Policymakers have created a riskier environment, while failing to achieve their desired outcome. As they fumble to find a solution, it has also revealed that they too are struggling with answers. Credibility is waning.

What does it mean?

Central banks have few policy tools left that are likely to achieve the desired outcomes. Monetisation of debt is one option that will be considered by some, particularly Japan. Ultimately, it may prove to be the turn for fiscal policy to do the heavy lifting. This will take time, and may not be a panacea if improperly implemented. Expect more volatility, as markets may begin to question the efficacy of policy.

Challenges ahead

The “lower for longer” era is not without costs and side-effects. The principal side-effects were always understood to be positive. Low rates should spur credit creation. Low rates should make it more appealing for consumers to forego savings and consume. Low rates were supposed to make investment returns more compelling relative to cost of capital and boost capital expenditure. And low rates and QE should foster portfolio rebalancing, allowing investors to sell safe havens and reinvest in riskier assets, keeping the self-reinforcing dynamic aloft.

Some of these expected side-effects never fully materialised, and some of them are simply exhausted themselves. New tools are required. In the meantime, we are left with record low rates. The longer we are in this environment, the more painful it will become for many market participants.

By Jim Cielinski Global Head of Fixed Income