Despite term deposit rates scraping the lowest point in many years, the amount of cash on deposit by Australian investors has increased exponentially since the Global Financial Crisis (GFC) and the Australian government’s guarantee on bank deposits. In this article, Grant Samuel Funds Management examines term deposits, the trends, and the risks investors can face when sitting on the sidelines in cash.

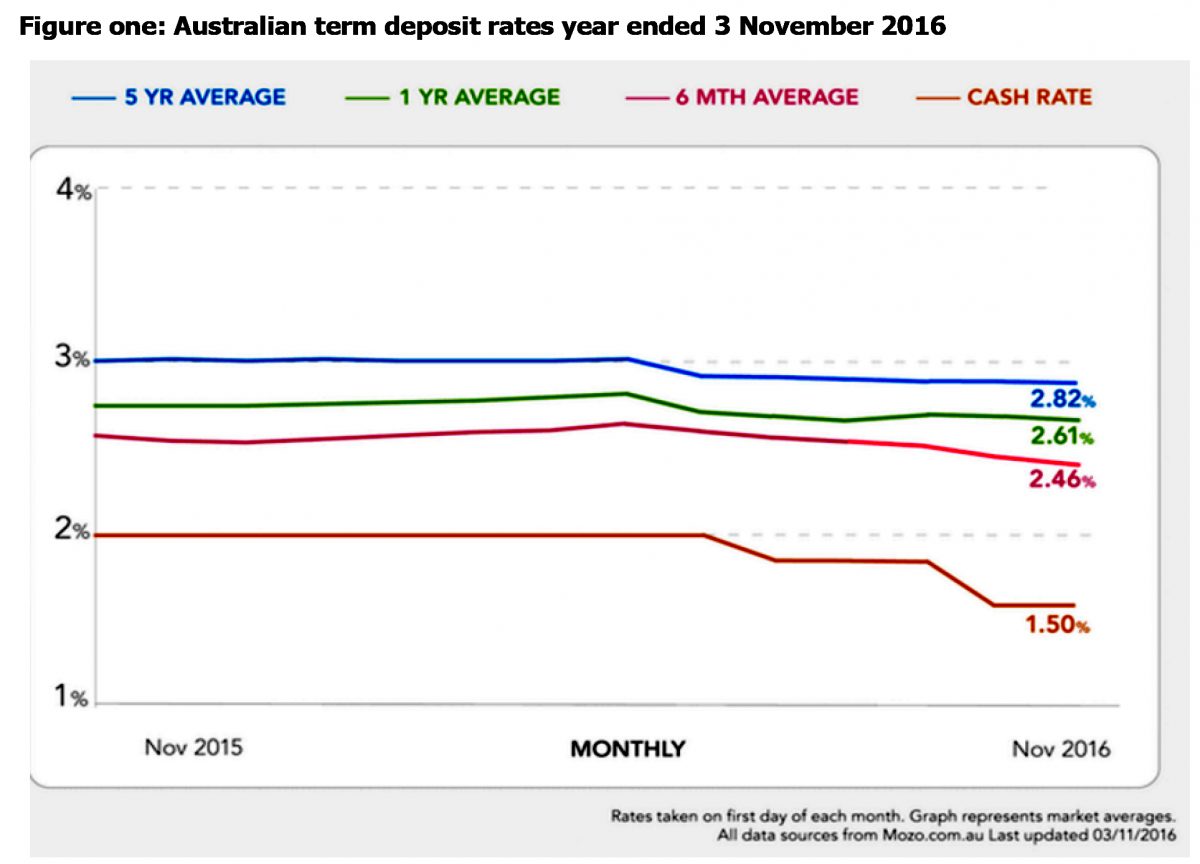

Since the end of the GFC there has been a bull market in equities – this has played out in global markets as well as our domestic market. Despite this, more investors than ever are putting their savings into term deposits, despite some of the lowest interest rates experienced for many years. As illustrated in Figure one, locking funds away for five years (at 3 November 2016) would provide an annual return of just 2.82%.

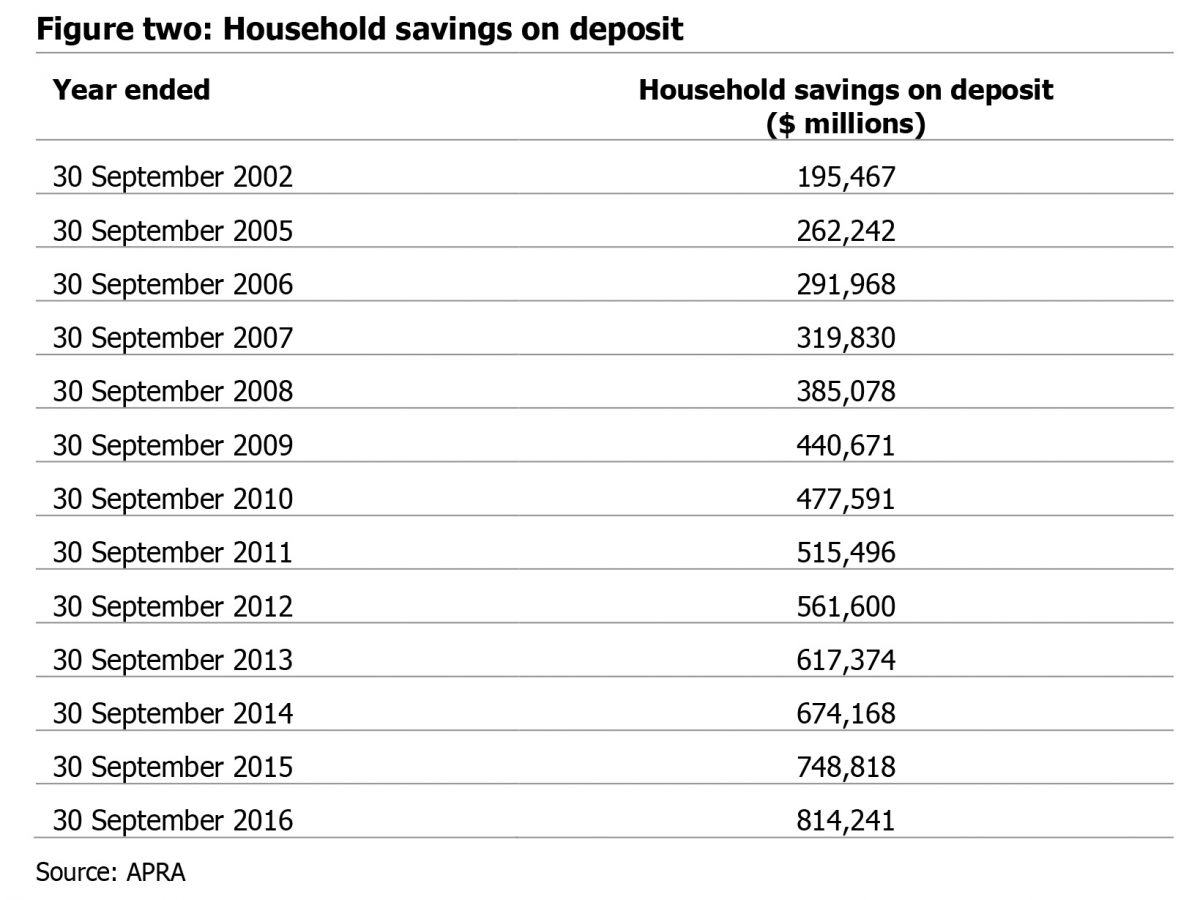

The amazing growth of term deposits The government guarantee may well have contributed to the huge growth in term deposits following the GFC. Statistics produced by the Australian Prudential Regulation Authority (APRA) show significant growth in household savings on deposit. In 2002, prior to the GFC, Australians had $195 billion on deposit; in 2008, the midst of the GFC, this had nearly doubled to $385 billion. Despite positive equity markets since the end of the GFC, this tremendous rate of growth has continued. The latest APRA data (at 30 September 2016) shows Australians having more than $814 billion on deposit.

A similar trend is evident when examining the assets held by Self-Managed Super Funds (SMSFs). Each quarter, the Australian Tax Office (ATO) publishes asset allocation statistics. According to the most recent, at 30 June 2016, cash and term deposits comprised, on average, 25 percent of SMSF portfolios.

What’s the attraction?

A term deposit is a low risk way to invest money, particularly for those investors who are not financial risk takers. Term deposits provide a vehicle to invest savings for a set term and at a fixed interest rate; when interest rates are high, it’s a compelling proposition.

Benefits of a term deposit include:

- Choice of investment term

- Certainty of return

- Amounts up to $250,000 are guaranteed by the federal government

- Unlike a savings account, money on term deposit is difficult to access – this can be of benefit to those who want their capital to be locked away.

What are the downsides?

Although investors like the security of money in the bank, particularly with a government guarantee, there are downsides to this approach. These include:

- Interest rate risk – an investor puts money on deposit for five years and gets the rate shown in Figure one (2.82%). The RBA may move to increase rates in that time, meaning the investor has locked in a lower rate for the duration of the deposit.

- No capital growth – an investor receives income, but no capital growth on the money invested.

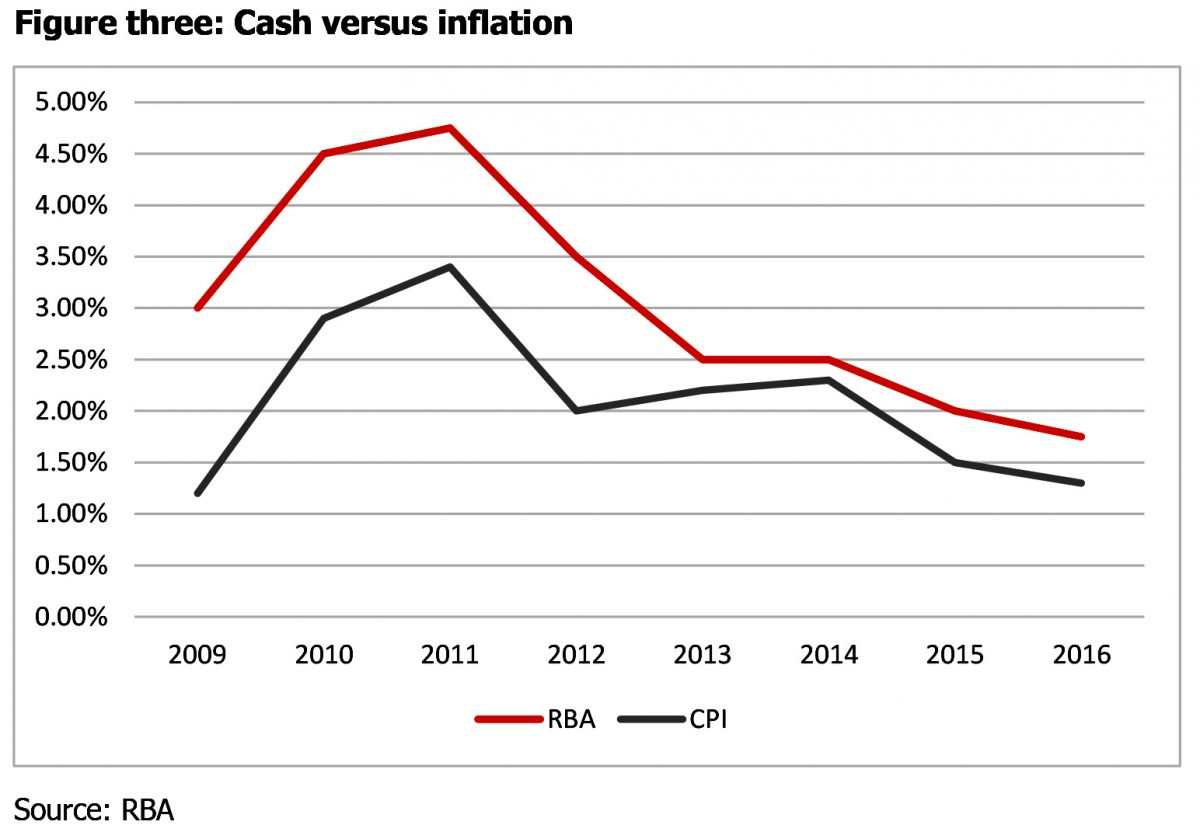

- Inflation risk – the risk that investments and income will lose purchasing power over time as prices increase. As illustrated in figure three, there is a close relationship between the inflation rate and the cash rate. While term deposit rates tend to be higher than the cash rate, the investor still has to pay tax on the income received; depending on their personal tax rate, the return from cash on deposit may barely beat inflation.

With no capital growth potential from cash on deposit and interest rates that barely outpace inflation, the purchasing power of money invested in a term deposit will most likely be eroded.

A basket of goods that cost $100 in 2007 will today cost $123.67[1] – an increase of 23.7 percent over nine years. An important question for investors to answer: on an after tax basis, will cash on deposit keep up with inflation, or will their purchasing power be eroded?

Longevity risk – the risk of investors outliving their savings. Thanks to improvements in living conditions and healthcare, in 2013, males aged 65 were expected to live a further 19.2 years, and females, a further 22.1 years[2] . Keeping savings in cash, which has no capital growth potential, exacerbates the possibility of retirees experiencing longevity risk.

These are not insignificant risks and important considerations for investors, particularly those close to, or in, retirement.

While the capital security of term deposits is attractive to investors, with interest rates so low, it’s worth considering some income generating alternatives, some of which may also have the added benefit of capital growth.

Products such as:

- Equity funds that have income generation as a core objective, particularly those that focus on real income and not simply realised capital gains

- Fixed income funds, particularly unconstrained funds that can invest at the shorter end of the yield curve and are less likely to be negatively impacted by increasing interest rates

- If investors are wary of capital loss, consider those that have a strong risk mitigation strategy, such as an options overlay that can minimise downside risk.

Rates and markets always move up and down; the trick is to find the right mix of strategies to ensure your clients meet their investment objectives. Parking money in the bank is probably not likely to deliver, particularly in this low rate environment.