The global economy has stayed true to its improving course with survey and activity measures edging higher. However, how much of the upturn is now in the rear view mirror? We typically focus on conditions in the US, as its economic activity tends to lead the global cycle.

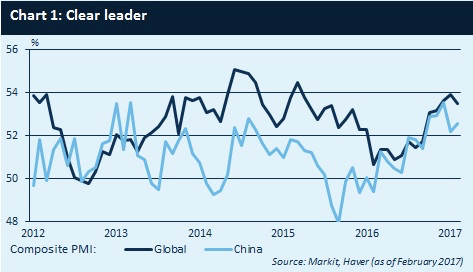

Here, the outlook remains favourable even if activity is lagging expectations in Q1, while a potentially stimulative fiscal approach waits in the wings. A more intriguing facet of the current pick-up has been the leading nature of Chinese data (see Chart 1).

That sentiment pre-empted improvement elsewhere reflects Beijing’s interventionist instinct.

After a growth wobble in 2015, policymakers reversed course on a series of reforms and boosted spending through budget increases, more lending to local government financing vehicles and the launching of a municipal bond market. In addition, credit conditions eased with interest-rate cuts while housing policies were loosened.

This coordinated effort was designed to reassert Beijing’s authority over the trajectory of domestic growth.

However, by coinciding with stronger developed market demand it amplified a global growth phenomenon. Unfortunately, the stimulus is unlikely to be sustained. Firstly, conditions in China no longer warrant such counter-cyclical measures, with sentiment and activity much improved.

Secondly, the abandoned reforms remain critical to prevent systemic risks, even if they pose a risk to growth in the near term. A more balanced approach from Beijing need not slow global growth if the nascent rebound in domestic demand in other emerging markets continues.

Recessions in Russia and Brazil have alleviated, while higher prices have supported consumption among commodity exporters.

EM import volume growth has surged to the highest level since April 2013, while service PMIs have surged. Whether favourable EM domestic demand trends can be sustained in the event of a more rapid slowdown in China remains to be seen, given the numerous linkages through trade and the commodities complex.