It seems that each day new statistics are released that highlight the housing affordability crisis. While Sydney and Melbourne are leading the pack, most Australian capitals are moving beyond the reach of first home buyers.

How can your clients help their children realise the great Australian dream of home ownership without having to sacrifice their own standard of living? In this article, Centuria explores the use of investment bonds as a strategy for your clients to help their children get a foot on the property ladder.

The housing affordability crisis

It’s no surprise housing affordability is in the news daily and receives political attention at both the state and federal levels of government.

To illustrate, statistics released on the day of writing by Domain Group, Melbourne house prices have jumped $100,000 in the year ended 30 June 2017, with the median now sitting at a record $865,712 – it broke through the $800,000 barrier just six months earlier.

Regional areas may have cheaper housing, however there are other issues to consider with such a move, such as the availability of employment opportunities. Given the high unemployment rates in many regional towns, such a move is not always an option.

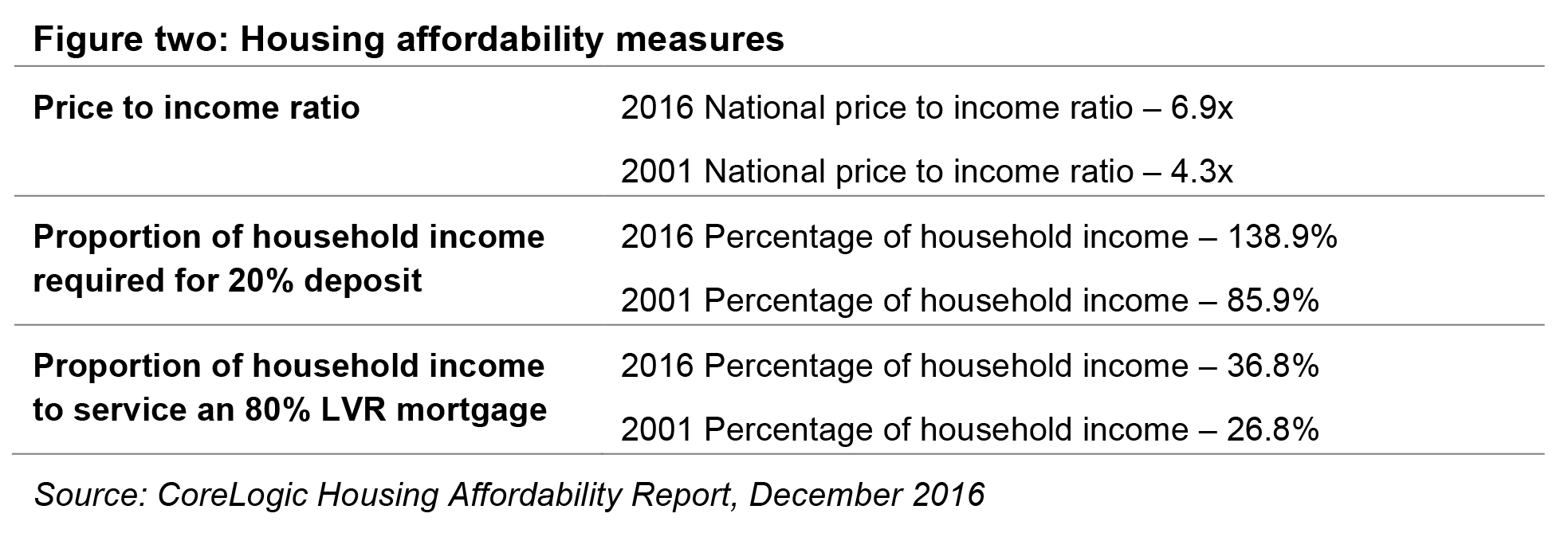

CoreLogic’s 2016 report into housing affordability[1] considered three measures of affordability and compared the current data to that collated 15 years earlier (data at September 2016 and 2001).

Growth in household income has not kept pace with growth in the property market. At the same time, the costs of essential items – power, petrol, food, health – have increased. This makes saving the 20% deposit increasingly difficult, in a market where the goalposts constantly shift.

As housing affordability continues to decline, the size of the average home loan has increased; as illustrated in figure two, this means a greater proportion of household income is required to service a mortgage. Bearing in mind that interest rates are at historical lows, this will increase further once the Reserve Bank moves to increase rates.

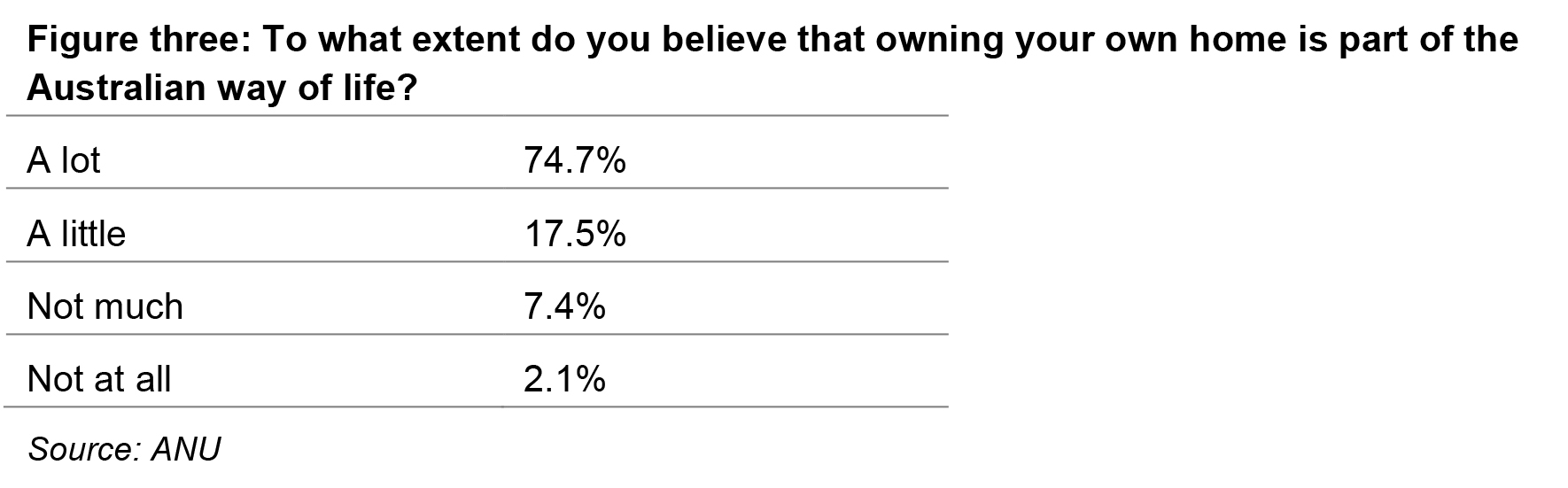

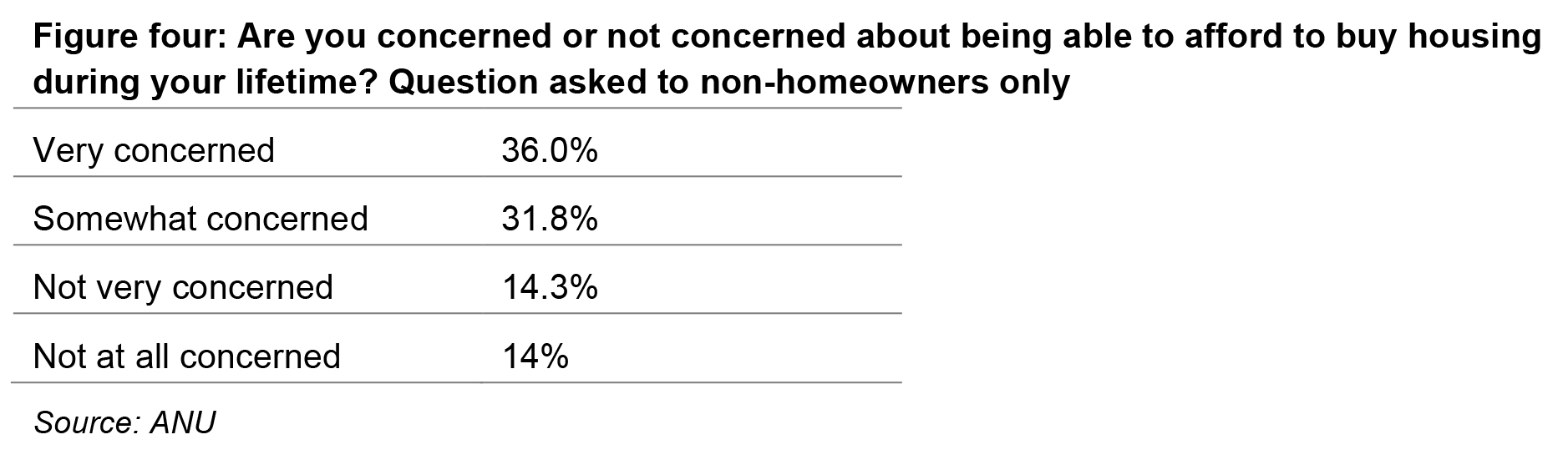

Is home ownership still the great Australian dream?

According to research undertaken by Australian National University[2], in which it polled over 2,500 Australians, home ownership remains a national aspiration.

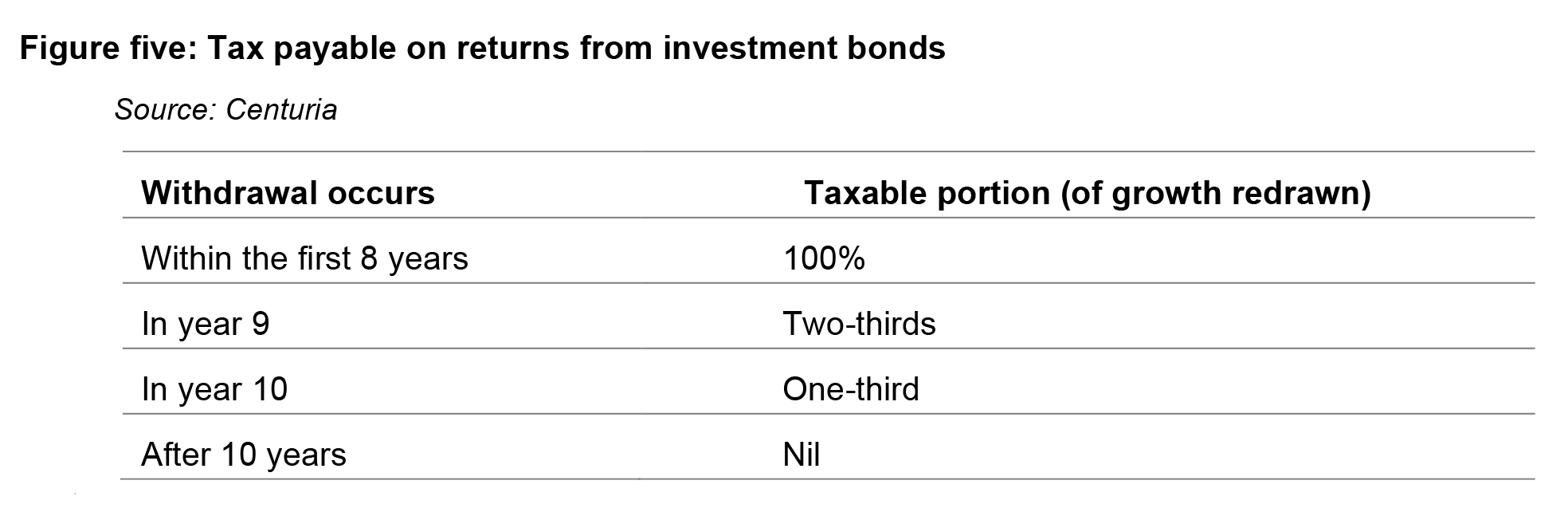

No annual tax reporting

As long as the client’s money remains invested, the manager of the investment bond will pay tax on investment earnings; there is no requirement for your client to declare those earnings in their annual tax reporting.

No limit on investment amount

There is no limit on the amount that can be invested to establish an investment bond. Investors can make subsequent investments up to maximum of 125% of the previous year’s contribution without restarting the ten-year period. Additional investments can be made annually or as a regular contribution. This way, parents can initiate an investment bond to help their children save toward a home, and make either regular or ad-hoc additional contributions.

Transfer of ownership

The ownership of the investment bond can be easily assigned or transferred at any time. The original start date is retained for tax purposes.

Beneficiaries

Investment bonds provide investors with freedom to nominate anyone as a beneficiary in the event of their death. As an investment bond falls outside of the estate, it is not distributed according to the will, nor is it affected if the owner dies intestate.

Paid tax-free to nominated beneficiary/ies

Once the ten-year investment period ends, or in the event of the death of the investor, the investment bond is paid tax-free to the nominated beneficiary/ies.

Case study

Matthew and Lisa are a hard-working professional couple with a 15-year-old daughter, Abbey. They have been concerned with talk of rising property prices and the difficulty for first home buyers to afford a property. They have set a goal of being able to assist Abbey with the purchase of a property by funding her deposit.

Based on the national median apartment price of $546,422, a 20% deposit of approximately $110,000 would be required to purchase an apartment without paying lenders mortgage insurance.

Mathew and Lisa have saved $25,000 in a cash account for Abbey. Both parents are paying the highest marginal tax rate, and want to be able to access the investment in 10 years’ time when Abbey reaches age 25 and is ready to take on the responsibility of a mortgage.

Matthew and Lisa consider other options, such as gifting or loaning the deposit to Abbey, or being guarantor and signing as joint borrowers on Abbey’s loan.

Their financial adviser explains the advantages and disadvantages of each option, and recommends they invest the $25,000 into the growth option of an investment bond. As well as the tax benefits of using an investment bond, Matthew and Lisa can make additional contributions up to $31,250 (125% of the initial $25,000 investment) each year.

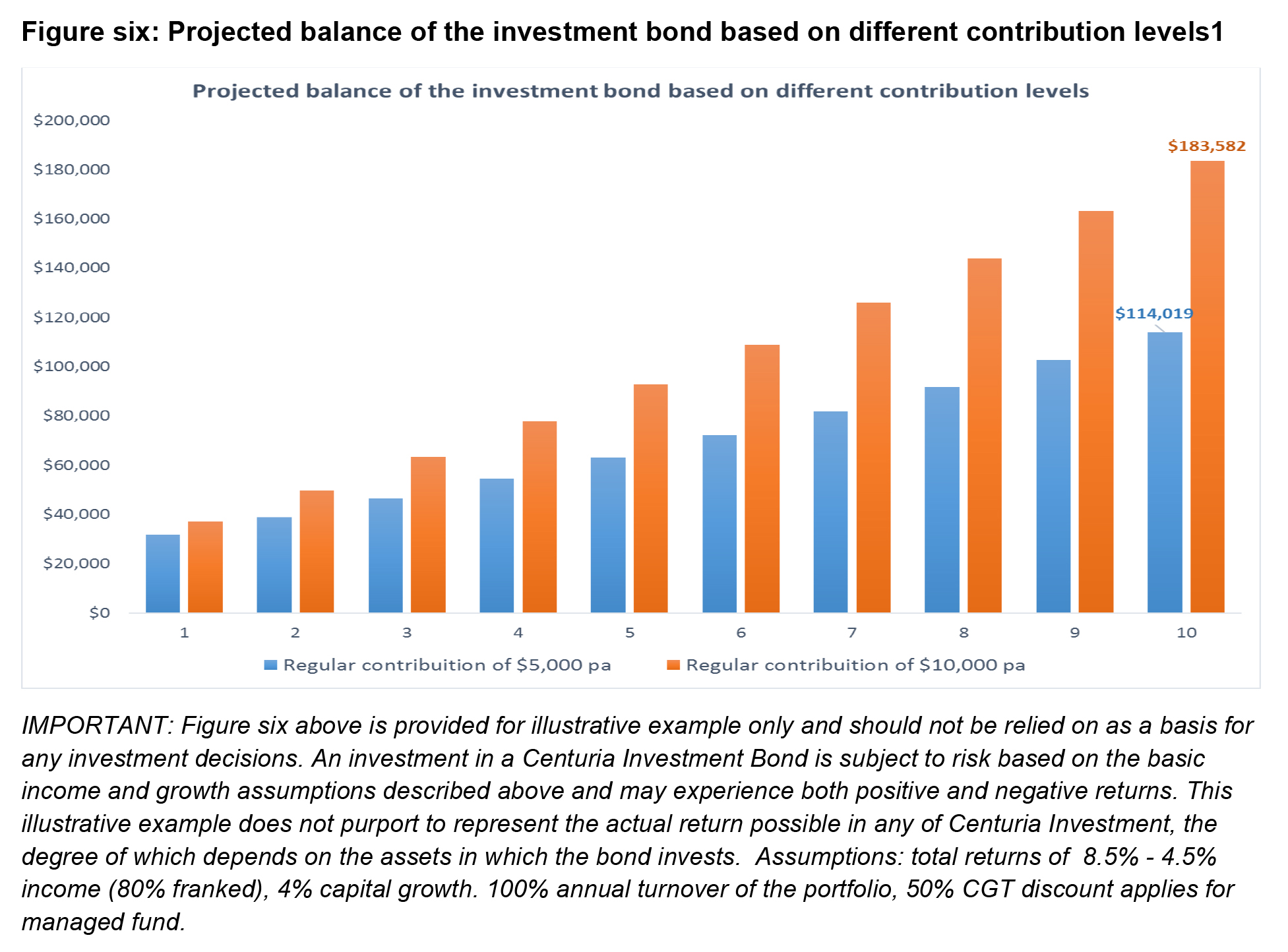

Matthew and Lisa believe they can afford to add between $5,000 and $10,000 to the investment each year over the 10-year period. As illustrated in figure six, a regular contribution of $5,000 per annum, on top of the initial investment of $25,000, over the 10-year period would result in a tax-free deposit of $114,019; a $10,000 contribution would provide a tax-free amount of $183,582.

Investment bonds are a unique and useful investment vehicle. No other investment provides exposure to a range of underlying investment options with no tax liability on maturation after 10 years. It’s the ideal time span for parents to save a contribution toward their children’s first home; after all, even if the property bubble does deflate, on a relative basis, house prices in Australia are likely to remain high for many years to come.