Investment markets and key developments over the past week

Share markets fell over the last week as US/China trade tensions returned with a vengeance. Australian shares were relatively resilient though falling only 0.5%, helped by gains in utilities and property stocks and resilience in resources stocks. The return to risk off saw bond yields decline but commodity prices were mixed with oil and metals down but iron up on ongoing supply disruptions. The $A pushed just below $US0.70.

Trade war back on again (for now). After appearing to make good progress on trade talks this year, President Trump hit the tantrum button and tweeted that the tariffs on $US200bn of imports from China will rise from 10% to 25% (delayed from January) and that remaining imports from China of around $US325bn will be taxed at 25% too. The first of these has now happened with China moving to retaliate and the second may take several months to put in place. President Trump’s move was supposedly in response to China back tracking on much of what had already been agreed and is likely a bit of “Art of Deal” stuff to sound tough and get what he wants. Who knows but its likely that both sides may have become emboldened by better economic data and share markets this year and so have decided to take risks again. Rising geopolitical tensions around North Korea and Iran are probably not helping the issue either.

Taxing all US imports from China at 25% would be a big deal compared to last years tariff hikes in that it will push the average tariff on all US imports from around 3% to around 7.5% which in turn could add around 0.2% to core inflation and detract up to 0.75% from US GDP. Given the flow on to confidence and global growth, hopefully the latest tariff hikes will be short lived, and the extra tranche of tariffs will be avoided. Our base case is that this will be the case and that a deal will be reached – once both sides refocus on the economic costs of slower growth, higher consumer prices and potentially rising unemployment, of which tumbling share markets have provided a reminder this week. This is particularly relevant for President Trump given his desire to get re-elected next year. With Chinese Vice Premier Liu He still in the US for trade talks the latest tariff hikes could be short lived if progress is made in these talks. If this is the case, we should know very soon but the signs so far are that the latest trade talks have not made much progress. So investors need to allow that the trade war could again get worse before it gets better risking further short term weakness in share markets at a time when they were already vulnerable after strong gains this year.

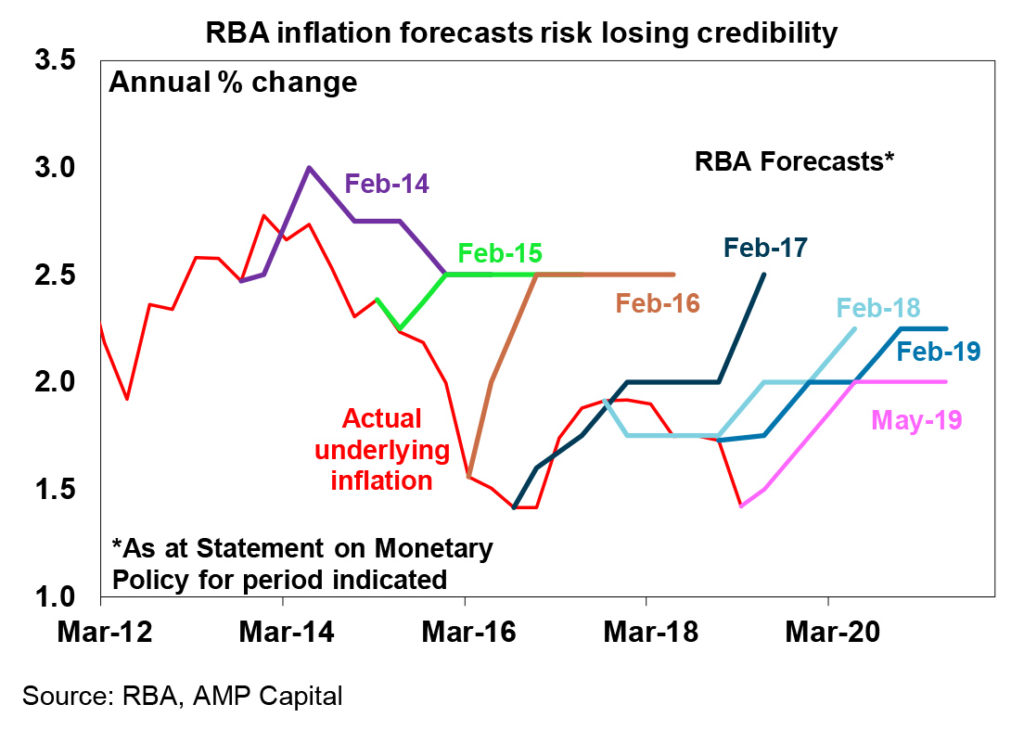

RBA remains on hold, but looks to be getting closer to a cut with an implicit easing bias. We had thought recent disappointments on growth and inflation would tip the RBA over the edge to a cut in May, but it was always a close call. However, it would be wrong to interpret this month’s inaction as a sign that rate cuts are not on the way.

- First, the RBA’s desire to avoid the politicisation of interest rates and the political spin that would have been put on a rate cut probably played a big role in the decision to hold in May (not that they would admit to that!).

- Second, the RBA’s Statement on Monetary Policy has yet again revised down its growth forecasts to now “around 2.75%” and its underlying inflation forecast to 1.75% for this year. Only six months ago growth was forecast to “average around 3.5%” and underlying inflation for this year was forecast to be 2.25%!

- Thirdly, the RBA has effectively lowered its hurdle for a rate cut to be the absence of a further decline in unemployment, from being a rise in unemployment. While rather convoluted the comment in the SOMP that “the ongoing subdued rate of inflation suggests that a lower rate of unemployment is achievable while also having inflation consistent with the target” basically means that NAIRU (or non-accelerating inflation rate of unemployment) is likely lower than the RBA has been assuming and that the level of unemployment consistent with the inflation target is below the current level of unemployment of 5%. Ergo unemployment needs to fall further to get inflation back to target.

- Fourthly, even with the technical assumption that the cash rate will move in line with market pricing for two rate cuts, the RBA only forecasts that inflation will get back to the bottom of the 2-3% target range in 2020-21 and unemployment tracks sideways at 5% out to the end of next year, implying just to achieve this rates need to be cut by 0.5% and that to get unemployment lower in the next 18 months and inflation confidently back into the target range rates may need to fall below 1%.

- Fifthly, the RBA’s observation that short term funding costs for the banks have come down and yet average mortgage rates haven’t suggests that its sees scope for the banks to cut mortgage rates suggesting that it expects that all or a significant portion of rate cuts will be passed on.

- Finally, the RBA is on record in the minutes to its last meeting as saying that lower rates could still help the economy.

Given our own expectations for unemployment to rise to 5.5% by year end and underlying inflation to remain lower for longer we remain of the view that the RBA will cut the cash rate twice this year to 1% by year end, with the risk being that they may have to do more. The first move could come as early as next month.

The basic problem for the RBA remains that inflation has been undershooting its forecasts and the 2-3% target for around five years now. The longer this persists the more it will lose credibility, seeing low inflation expectations become entrenched and risking a slide into deflation in the next economic downturn.

Meanwhile across the Tasman the RBNZ looks to be taking a more forward-looking approach to monetary policy, having cut its official cash rate in the last week after revising down its inflation forecasts and in anticipation of slower jobs growth.

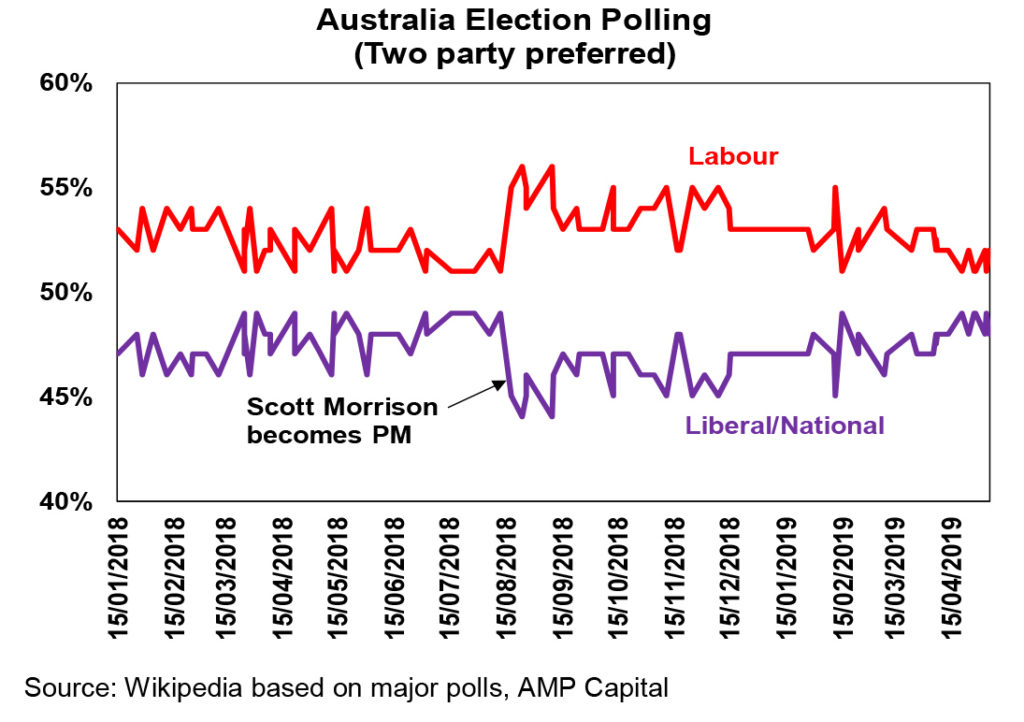

Its now only one week to go to the Australia Federal election. The last week of campaigning has simply confirmed the significant policy differences between the major parties with Labor proposing a more interventionist approach to the economy compared to the Coalition – in terms of tax, spending, climate policy, regulation and industrial relations. The polling gap narrowed through March and April but still favours Labor.

Major global economic events and implications

US job openings, hiring and quits remained high in March and the trade deficit deteriorated a bit but producer price inflation remained benign. US March quarter earnings reports are now 90% done. 76% have beaten on earnings by an average 6% and 56% have beaten on sales. Earnings growth started the reporting season with expectations for a 2% fall on a year ago but looks like ending up around +3%.

Whatever happened to Brexit? Well nothing. They still can’t agree and so the UK will be participating in EU parliamentary elections on 23 May which will likely show strong support for pro remain and pro Brexit parties.

Chinese data was a mixed bag with stronger growth in imports suggesting strong domestic demand, but weaker exports and another pull back in total credit. However, abstracting from monthly volatility, momentum in exports and credit growth is still trending up after bottoming late last year or early this year. Meanwhile inflation rose to 2.5% year on year in March but this was driven by higher pork prices with core inflation falling to 1.7%yoy suggesting inflation is not posing a problem for policy stimulus. Speaking of which policy stimulus continued with the PBOC cutting reserve requirements for targeted small banks.

Australian economic events and implications

Australian data was on the soft side domestically but there was some good news regarding trade. Retail sales came in better than expected for March after strength in February, but it was due to higher food prices, with March quarter retail sales going backwards pointing to another weak quarter for consumer spending. Meanwhile, ANZ job ads slipped again in April and are now down 5.6% year on year and the Melbourne Institute’s Inflation Gauge for April slipped to 1.8%yoy with the underlying measure falling to 1.3%yoy. However, in good news for the economy the trade surplus remained around record levels, but the improvement in the March quarter looks to have been due to gains in export prices with net exports contribution to GDP growth looking basically flat. But higher export prices will add to national income via the terms of trade which in turn will likely drive the budget into surplus for this year.

What to watch over the next week?

Apart from the US/China trade issue, President Trump is also due to make a decision regarding auto tariffs by May 18 but this may be delayed given ongoing talks with the EU and Japan and auto tariffs face wide bi-partisan opposition in Congress. On the data front, consumer spending is likely to be the focus in the US in the week ahead with retail sales data due Wednesday likely to show a modest rise in April after March’s surge. In other data expect continuing strength in small business optimism (Tuesday), a small rise in industrial production and a further improvement in home buyer conditions (both Wednesday) and a solid bounce in housing starts (Thursday). Manufacturing conditions surveys for the New York and Philadelphia regions will also be released.

Chinese activity data for April to be released Wednesday will be watched for further improvement after the pick up seen in March. Industrial production is likely to slow back a bit but retail sales and fixed asset investment are expected to hold on to recent gains if not improve slightly further.

In Australia, apart from the focus on Saturday’s election, jobs data to be released Thursday will attract even more than usual attention given the importance the RBA has attached to a further improvement in the labour market as a key to getting inflation up and heading off rate cuts. We expect to see a 12,000 gain in employment but unemployment rising to 5.1%. March quarter wages data to be released Wednesday will also attract a lot of interest but is expected to have remained subdued at 0.5% quarter on quarter or 2.3% year on year. Meanwhile, March housing finance (Monday) is expected to show a 0.5% fall after February’s bounce, the NAB’s business conditions survey will be released Tuesday and consumer confidence will be released Wednesday.

Outlook for investment markets

Share markets – globally & in Australia – have run hard and fast from their December lows and are vulnerable to a further short-term pullback. Geopolitical uncertainty around trade, North Korea, Iran and still mixed global economic data could be the drivers. But valuations are okay, global growth is expected to improve into the second half and monetary and fiscal policy has become more supportive of markets all of which should support decent gains for share markets through 2019 as a whole.

Low yields are likely to see low returns from bonds, but government bonds remain excellent portfolio diversifiers.

Unlisted commercial property and infrastructure are likely to see a slowing in returns. This is particularly the case for Australian retail property. However, lower for even longer bond yields will help underpin unlisted asset valuations.

Our base case is for national capital city house prices to fall another 5% or so into 2020 on the back of tight credit, rising supply, reduced foreign demand, price falls feeding on themselves and uncertainty around the impact of tax changes under a Labor Government. An earlier rate cut in May could bring forward the bottom in house prices as in the last two cycles they bottomed four months or so after the first rate cut.

Cash and bank deposits are likely to provide poor returns as the RBA cuts the official cash rate to 1% by year end.

The $A is likely to fall further into the $US0.60s as the gap between the RBA’s cash rate and the US Fed Funds rate will likely push further into negative territory as the RBA moves to cut rates. Excessive $A short positions and high commodity prices will likely prevent an $A crash though.

By Shane Oliver