Shane Oliver

Key points

- US protests are only an issue for investment markets if they significantly impact economic activity.

- Global and Australian recovery will boost bond yields and there is good reason to believe that (after yet another false ending) the now nearly 40-year super cycle decline in bond yields may be at or close to over.

- But the end of the bond bull market is likely to be gradual and so shares and real assets are likely to still see some benefit from a search for yield.

Introduction

New years often start with a few events to challenge any calm investors may have achieved over the Christmas/New Year break. Some of these prove short lived like the global growth scare at the start of 2016 or the US inflation and interest rate scare in early 2018. Others have a more lasting impact such as the coronavirus pandemic. This year we have seen the year start with an attempted “insurrection” by a mob of Trump supporters and a sharp back up in bond yields. This has all come at a time when share markets have become a bit vulnerable to a correction after a strong run up. The rise in bond yields begs the question whether we have at last seen the end of the near 40-year bull market in bonds. But let’s first have a look at US politics as it will likely impact where bond yields go.

US protests largely ignored by markets

As disturbing and dramatic as recent events have been in the US – with President Trump provoking a mob of armed supporters to march on the Capitol leading to several deaths and some chanting “hang Mike Pence”, then Trump telling them “we love you”, all leading to him being impeached for a second time with even many Republican supporters turning against him – they had little impact on investment markets. And even as the protests by Trump supporters continue around Joe Biden’s inauguration, they are unlikely to have a big impact. This is because unless there is a significant disruption to economic activity and/or the sound working of the political process then they are of little relevance to investment markets. This was also the message from the Black Lives Matter protests in mid-2020 (not that they are really comparable) and past incidents such as the 1995 Oklahoma City and 1996 Atlanta Olympic Park bombings as well as numerous other terrorist attacks (bar 9/11 which was on a far greater scale). More fundamentally it seems that every so often the US goes through a catharsis only to emerge stronger – the Civil War, the Great Depression and the 1970s come to mind. There are three reasons for optimism.

- First, US democratic institutions held firm – with electoral officials, judges and politicians giving precedence to the law and their duty as opposed to their political allegiance (think Georgia Secretary of State Brad Raffensperger).

- Second, the violent invasion of the Capitol highlighting a lack of respect by Trump and his supporters for US institutions and how this leads to violence has likely further alienated mainstream Republicans (many of which see the GOP as the party of law and order) and Americans.

- Finally, it puts more pressure on the Biden Administration to do something about the drivers of extreme social division and polarisation in the US – such as inequality. This is something Trump tapped into to get elected but didn’t address. And the Democrat clean sweep with control of the Presidency, House and now the Senate gives them scope to do this. Maybe it’s necessary to save capitalism from itself! Which over time will likely mean higher bond yields.

Bonds 101

It’s first worth a quick refresher on how bonds work. If the government issues a bond for $100 and agrees to pay $3 a year in interest, this means an initial yield of 3%. The higher the yield the better, but in the short term the value of the bond will move inversely to the yield. If growth or inflation slows and the central bank cuts interest rates, investors might snap up the bonds paying $3 till the yield is pushed down to say 2%. In the process, the value of the bond goes up giving a capital gain. This is what’s happened in recent decades and explains why bonds have had good returns despite ever lower bond yields. But if growth or inflation pick up and bond yields rise, investors suffer a capital loss. And if you buy a bond yielding 2% and hold it for its term to maturity (say 10 years) the return will be 2% pa!

A bit of context around the big picture in bond yields

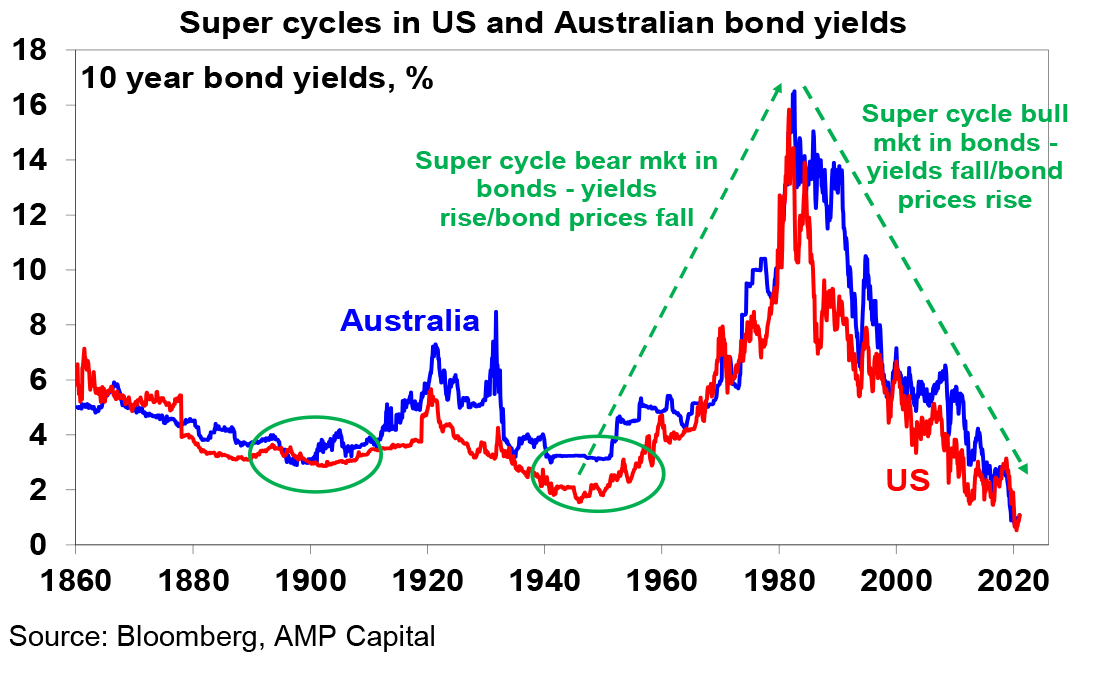

The next chart shows US and Australian bond yields from 1860.

Since the 1940s there’s been two secular moves in bond yields:

- A near 40 year super cycle rise in yields into the early 1980s driven by rising inflation on the back of expansionist economic policies after the Great Depression and WW2, monetary financing of the Vietnam War, rising commodity prices, protectionism and slowing productivity along with rising economic uncertainty resulting in higher real yields.

- A near 40 year super cycle decline in bond yields from the early 1980s on the back of a sharp fall in inflation driven by aggressive inflation fighting central banks in the early 1980s and 90s, supply side reforms, globalisation, lower costs and increased competition flowing from digitalisation, rising inequality depressing spending, spare capacity and reduced worker bargaining power with worries about deflation in recent times combined with safe haven investor demand for bonds, rising demand for safe income yielding assets as populations age & central bank bond buying since the GFC.

Since their record lows at the height of the pandemic driven market panic in March/April, 10 year bond yields have risen in the US from 0.5% to 1.09% and in Australia from 0.6% to 1.08%, with the latest leg in the last few weeks. The drivers have been economic recovery, increasing optimism about a further recovery as vaccines are deployed with the likelihood of more stimulus in the US following the Democrats gaining control of the US Senate. Surveys of US investors now show inflation and higher rates as bigger concerns than coronavirus.

However, the bond bull market since the early 1980s has seen several reversals associated with cyclical economic upturns only to see the declining trend resume. There have been numerous attempts to call the end of the super cycle bond bull market (including from me!) only to see new deflationary shocks – the GFC, the Eurozone debt crisis, the 2015-16 global growth scare, US trade wars – push yields even lower. In this context, the recent rise in bond yields is just another uptick in a long-term downtrend. In fact, higher bond yields and steeper yield curves are perfectly normal in cyclical economic recoveries.

We may be at/close to the end of the bond bull market

However, more fundamentally, a range of factors suggest we may have seen/come close to the bottom in the 40-year super cycle decline in bond yields and that the trend may shift up:

- Central banks are now throwing everything at boosting inflation – much as they did in the early 1980s in trying to get inflation down. This is evident in massive money printing and central banks committing not to raise rates until inflation is sustainably at target with tolerance for an overshoot.

- Massive fiscal stimulus provides an avenue for rising money supply to boost spending and hence inflation in contrast to last decade when easy money was offset by fiscal austerity.

- The political pendulum in Anglo countries is swinging back to the left with more intervention in the economy – in the US under President Biden this is likely to focus on reducing inequality (which is positive for spending) and policies designed to shift power back to workers from companies.

- Globalisation is starting to reverse – reflecting a desire to bring the production of some things back onshore to protect supply chains along with tensions with China.

- Bond yields around zero seem to have hit a bit of a natural barrier and the bond bull market is now long in the tooth.

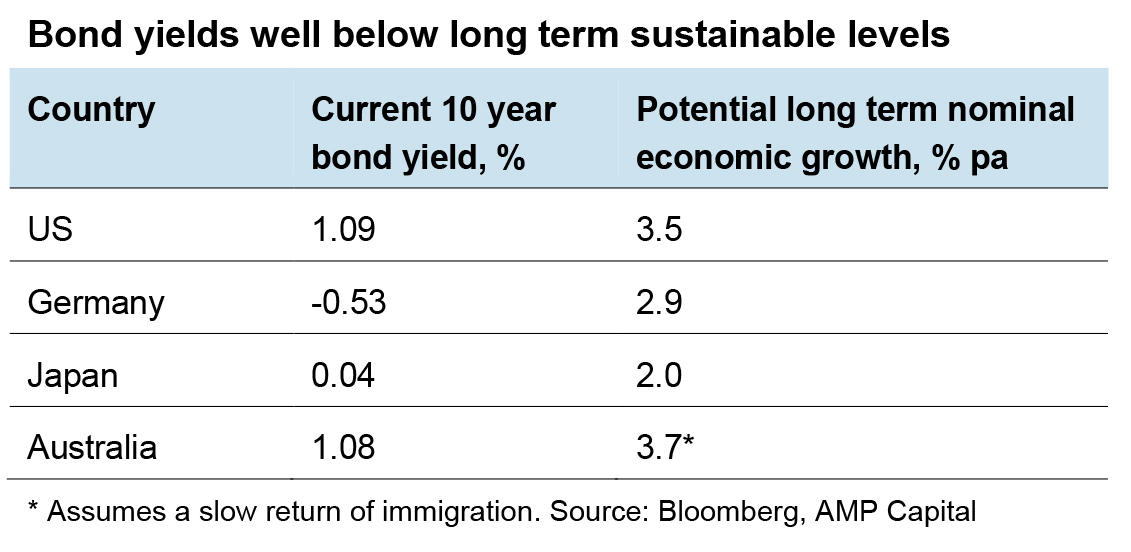

- It’s hard to see negative or near zero interest rates being sustainable on a very long-term basis. Over the long-term nominal bond yields tend to average around long-term nominal GDP growth. Even on the basis of our conservative long-term nominal economic growth expectations, 10-year bond yields are well below sustainable levels.

- Finally, the crowd is very long in bonds as indicated by cumulative inflows into US bond funds & ETFs as opposed to equity funds and ETFs. These positions could be shaken if bond yields rise significantly leading to capital losses.

But a rising trend in yields is likely to be gradual

The end of the four-decade super cycle decline in bond yields will likely be gradual and unfold over several years:

- Historically, bond yields have gone through a base building process over several years after a long-term downswing as it takes a while for growth and inflation expectations to turn back up. See the circled areas for US and Australian bond yields in the earlier chart.

- While growth will likely bounce back this year, spare capacity – evident in still high levels of unemployment and underemployment – remains high and will keep wages growth weak limiting any pick up in underlying inflation over the next year or two, even though commodity prices are up.

- Major central banks and the RBA in Australia remain a long way off from starting to tighten so global monetary policy will remain easy for a while yet.

- Inflation expectations are anchored at low levels, in contrast to the 1970s and in 1994 – which makes it harder for short term price spikes to turn into permanently higher inflation.

- Finally, central banks will not be powerless to deal with above target inflation when it eventually comes. In fact, high debt levels mean that interest rate increases will now be more potent than they used to be – so the RBA won’t have to raise rates as much to control inflation as in the past.

Implications for investors?

There are several implications from an eventual end to the bull market in bonds. Firstly, expect mediocre returns from sovereign bonds as they will no longer be boosted by declining yields driving capital growth. 10-year bond yields of 1.1% in Australia imply bond returns over the next decade of just 1.1%! And in the short term, rising bond yields will mean capital loses.

Secondly, higher bond yields will impact share market returns as they make shares more expensive. Shares will be okay if the rise in bond yields is gradual and so can be offset by rising earnings – as we expect this year – but a large, abrupt back up in bond yields will be more of a concern.

Thirdly, a bottoming in bond yields will favour share market sectors that can benefit from economic recovery via higher earnings – like industrials, banks and resources stocks.

Fourthly, for real assets like unlisted commercial property and unlisted infrastructure, the search for yield may still support investor demand unless bond yields rise aggressively. But both sectors still have some issues to work through from the pandemic reducing demand for shops, offices and airports.

And for home borrowers we are probably at or close to the bottom in fixed mortgage rates in Australia.

By Dr Shane Oliver, Head of Investment Strategy and Chief Economist