Stephen Colwell

Years before he became a billionaire hedge fund manager, William “Bill” Ackman, founder of Pershing Square Capital Management, trekked 10,000 kilometres to go fishing. Although Ackman had never fished a day in his life, the trip was a success due to his guide, Oliver White.

While White had no prior knowledge of the investment industry, his ability to find fish was key to impressing Ackman. Drawing upon a wise teaching of legendary investor, Charlie Munger, “the first rule of fishing is fish where the fish are”, Ackman offered White a role in his investment team.

Where’s the best place to fish in Australian equities?

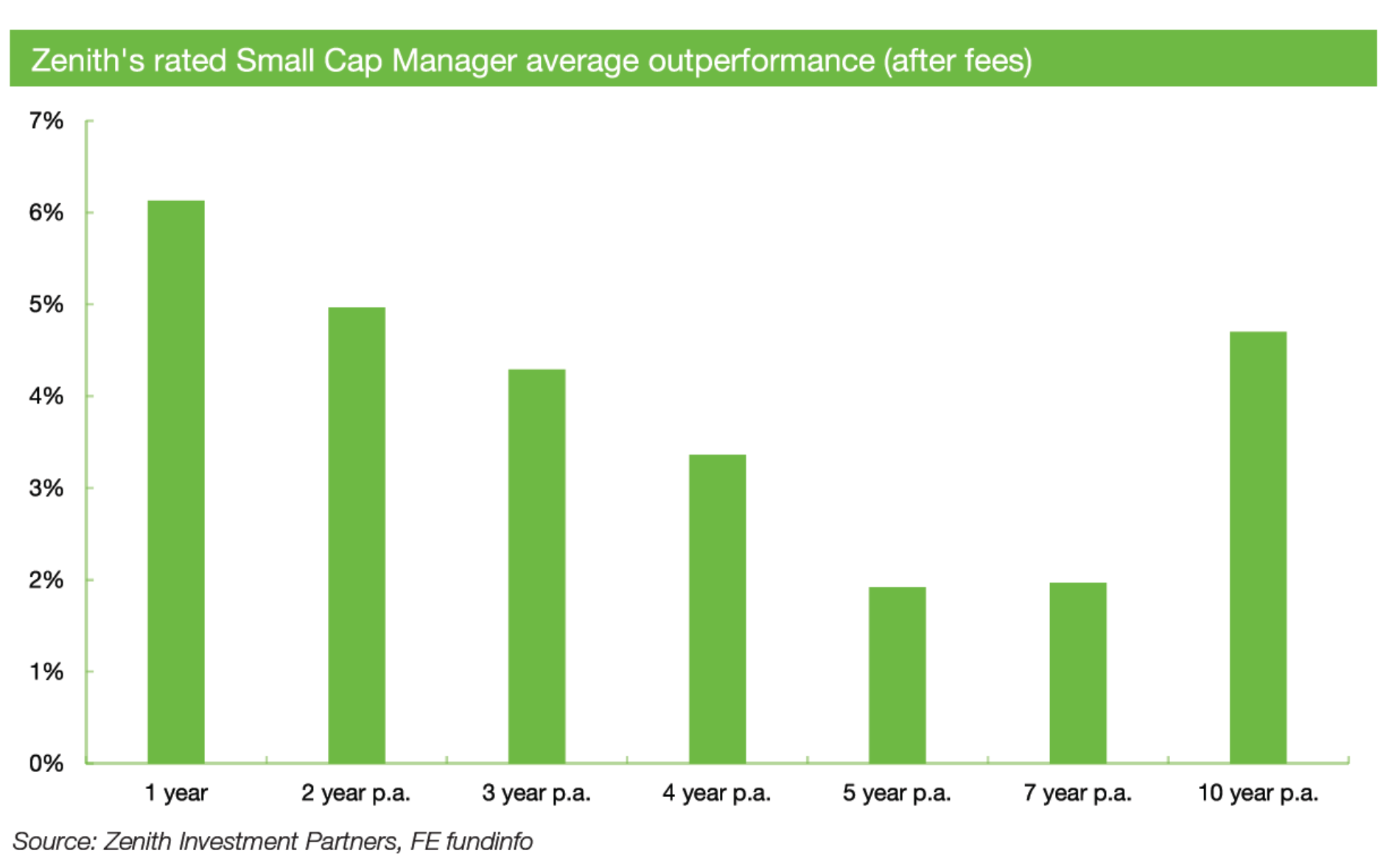

The best fishing spot for active managers is the Australian small cap pond, which is represented by the S&P/ASX Small Ordinaries Index. A diverse and under-researched opportunity set gives an active manager the best chance of outperforming. The chart below highlights the persistent outperformance profile of our rated small cap managers.

What’s accelerated this outperformance in recent years?

The Australian small cap universe is dynamic and diversified, and increasingly so. Over the past five years, constituent changes for the small cap index have gradually increased, reaching a peak of 55 in 2021.

We also found that over 50% of constituents in the small cap index were not there five years ago, equating to over 100 new opportunities for investors. That’s a lot of new fish! The refresh rate was almost double that of the large and midcap benchmark, as represented by the S&P/ ASX 100 Index over the period.

Where are the new fish coming from?

These new opportunities can come from a variety of channels, including initial public offerings (IPOs), whereby a company issues its shares publicly on an exchange. Over the past five years, investors have seen an average of 110 new companies list per year, which are typically opportunities that fall within small and microcap managers’ universes, due to liquidity and size constraints.

The 12 months to 31 December 2021 were particularly busy for IPO activity on the Australian Stock Exchange with almost 200 companies listing, more than doubling that of 2020.

Another channel for new opportunities is through index constituent changes. Specifically, microcap companies graduating to small caps and midcaps falling into small caps. More on this later.

A third channel is through corporate activity, which generally comes in the form of emerging and smaller companies being acquired. When stocks are removed from the index, it’s replaced at the next index reconstitution, leading to further opportunities for active investors.

Afterpay is a great example of a company that passed through all the channels above. It was listed in 2016 and grew rapidly, which led to it eventually being promoted to the large cap index. In 2022, it was acquired by US payment giant, Block (formerly known as Square).

Plentiful fish = strong excess return

The law of active management suggests that managers are better positioned to generate excess returns with greater investment breadth, holding all else equal. That is, the higher the ‘effective’ number of holdings in an index, the greater the investment breadth.

The chart below shows the change in the effective number[1]of stocks within the small cap index over a five-year period to 31 December 2021.

Although the small cap index typically comprises approximately 200 stocks, the diverse nature of the index results in an effective holding of 148 equally weighted stocks, as at 31 December 2021. Compared with five years ago, when the effective number of holdings was 128, there’s been a material increase in breadth and diversity in the index, which improves an active manager’s ability to generate outperformance.

How does this compare to large caps?

Taking the S&P/ASX 50 Index as a representation of large caps, we find that the dynamics are very different.

The effective number of stocks within the large cap index was 23 (or approximately 45% of 50 stocks in the index) in 2021, which remains virtually unchanged since 2017.

You’re promoted!

How do stocks perform when they get promoted from the small cap index to the midcap index?

The chart below shows the one, two and three-year median outperformance of stocks graduating from small caps (S&P/ASX Small Ordinaries Index) to midcaps (S&P/ASX MidCap 50 Index).

Over a one-year period, promoted stocks experienced a median outperformance over the small cap index of over 6.0%. We believe this short-term outperformance is driven by structural reasons, such as continued momentum from passive index funds buying as stocks enter mid and large cap indices.

However, promoted stocks typically underperformed following the initial 12-month period, which we consider to be underpinned by structural issues.

The small cap fund manager universe in Australia is significantly more mature than its midcap counterpart. This dynamic has the effect of leaving promoted stocks stranded, no longer available to small cap funds and unable to be supported in a material manner by midcap funds.

To remain true to label, small cap funds are typically mandated to divest stocks that get promoted within a certain time frame, which is generally set at 12 months. We believe this time frame ensures that small cap funds remain true to label and allows investors to benefit from the capital gains discount.

Oh, and you’re demoted…

If promotions result in short-term outperformance, is the opposite true for demotions?

We found that this assertion is false for midcap stocks that are demoted. The chart below shows the performance profile of demoted mid cap stocks.

Over a one-year period, demoted stocks experienced a median outperformance over the small cap index of over 10%. There’s an immediate tailwind associated with small cap funds becoming eligible to buy these companies once again, especially given demoted stocks can (and often do) have a meaningful weight in the benchmark.

Australian small caps – the place for active managers to fish!

After putting in 100-hour work weeks at Pershing Square Capital Management, White moved back to the Bahamas, seeking the best fishing waters in the world.

Using his newly acquired skills, he found an old, dilapidated hotel, and made his vision to build a fishing lodge a reality. With Ackman as his backer, White created a highly profitable business, hosting high profile visitors and the ESPN fishing show, Pirates of the Flats.

The playbook for our rated Australian small cap managers is similar – fish for attractive opportunities in some of the best waters in the world.

By Stephen Colwell, Senior Investment Analyst

———-