Investment markets and key developments

Share markets saw a bit of relief in the past week – bouncing of oversold lows helped by less hawkish than feared comments from the ECB and Fed, a further pullback in US bond yields, improved outlooks from some US retailers and airlines and M&A activity. This left the US share market on track for its first weekly gain after seven weeks of falls, and European, Japanese and Australian shares also rose. In Australia, gains in resources and financials offset falls in telcos, consumer staples and IT stocks. Bond yields fell in the US and Australia but rose in Europe. Oil and copper prices rose, but iron ore prices fell. The risk on tone helped the $A rise as the $US fell.

Rate hikes continue but with mixed messages from central banks.

- At the hawkish end the RBNZ raised its cash rate by 0.5% taking it to 2% and significantly revised up its forecasts for the cash rate to a peak of 3.9% next year all clearly aimed at slowing demand and keeping inflation expectations down. With the NZ economy already slowing though the RBNZ may be starting to get a bit too extreme (as it often does) and so may reach a peak in its cash rate earlier and lower than its currently projecting.

- The Bank of Korea hiked its cash rate by 0.25% to 1.75% and remained hawkish too although maybe not as much as the RBNZ.

- ECB President Lagarde pre-announced near-term monetary policy moves with the end of quantitative easing early next quarter, a rate hike in July and the end of negative rates by September. While this was unusual it looks designed to reduce uncertainty around monetary policy. Lagarde also pushed back against ECB Council members arguing for 0.5% hikes saying “we don’t have to rush.” This helped boost Eurozone shares.

- The minutes from the Fed’s last meeting indicated that after two more 0.5% hikes it would be well positioned to assess the impact and need for more policy moves later this year. The market interpreted this as indicating that the Fed is prepared to be flexible, opening the possibility of a pause later this year.

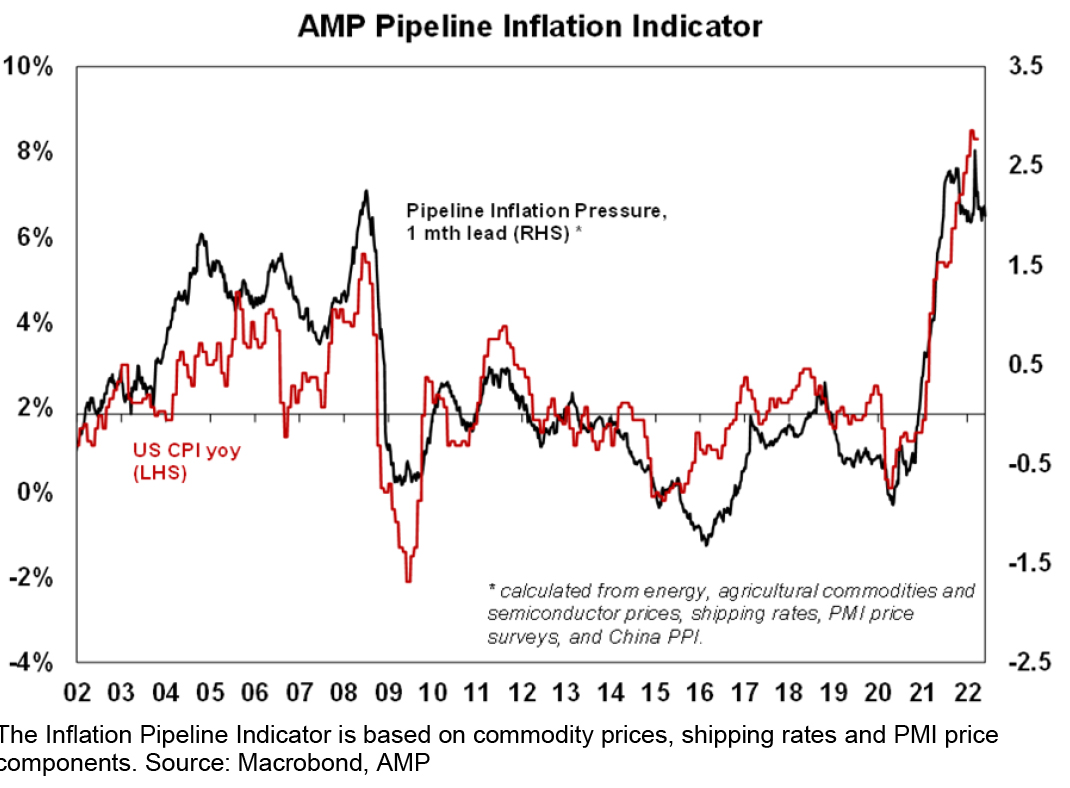

Of course, it is dangerous to read too much into central bank comments either way. Just over 6 months ago the Fed was saying it could be patient in removing monetary stimulus and the RBA was indicating a rate hike was unlikely before 2024. Ultimately central banks are data dependent. And they want to see clear evidence that inflation is cooling. There are some positive signs on this front though: business surveys are reporting improving delivery times, reduced backlogs and some topping in input and output price pressures; US retailers have seen an increase in inventories presumably as spending rebalances back to services and production catches up; there are some signs of a slowing in hiring in the US with initial jobless claims starting to trend up, Amazon saying its gone from understaffed to overstaffed and giving up space and Lyft pausing hiring; wages growth in the US looks to have peaked late last year; and our Pipeline Inflation Indicator continues to point to a peaking in US inflation.

At this stage it’s a bit too early to relax though. Rising oil and hence petrol prices are a fly in the ointment of the “peak inflation” view and commodity prices generally still look strong. This could be accentuated if Europe bans Russian oil (as looks likely) and there is a disruption to Russian gas flowing to Europe. Even if US inflation has peaked it will take a while before its fallen back to levels where the Fed can relax.

And in Australia inflation probably won’t peak until later this year with petrol prices back up, household energy bills set to rise significantly on the back of higher wholesale power prices from earlier this year (this has been well known for a while but will start to show up in power bills from July) and supermarkets warnings of still rising prices.

At the same time shares are yet to see clear signs of a wash out bottom – with VIX and put/call ratios yet to reach levels seen at past major share market bottoms. The bottom line is that while we remain optimistic that recession will be avoided in the next 18 months and so shares can rise on a 6-12 month view, shares are still at risk of more downside in the short term (notwithstanding that the current bounce may have further to go).

Australia’s new Government and fiscal and monetary policy. The new Australian Labor Government still appears to be edging toward governing in its own right, although there is still a possibility it may have to rely on independents or minorities and will have to rely on the Greens in the Senate (or moderate Liberals!).

- A lesson from the election is that the Australian electorate is decidedly centrist – go too far to the left or right and you get kicked out (ALP under Whitlam, LNP under Morrison) or don’t get elected to govern (LNP under Hewson, ALP under Shorten). And in this regards the army of mainstream, often Liberal party voters behind the “teals” is evidence of this. So, if the new Government wants to be more than a one term wonder then it has to govern from the centre.

- In this regard, the new Treasurer’s warnings that the “dire” budget position and “skyrocketing” inflation mean that it cannot afford extra spending and may have to delay some commitments provide confidence that it will manage the budget responsibly. Higher commodity prices and lower unemployment still point to better budget numbers in my view but the deficit and debt projections are still too high and rely over the medium term on optimistic productivity growth assumptions. And high inflation argues for smaller deficits to take pressure off interest rates. So it makes sense for the new Treasurer to damp down expectations for more spending. Expect more budget savings to be found by the time of the October budget. Similarly, the Government’s desire to avoid deals with the Greens to change its policies also indicate a desire to govern from the centre.

- Attention is now turning to the review of the RBA and fortunately the RBA’s independence does not appear to be in question – if it was it would be a real disaster given the risks on inflation. There is no reason to change the RBA’s full employment and price stability objectives as they are like motherhood. Nor should the 2-3% inflation target be changed – raising it now would just add to inflation risks and lowering it would risk deflation in a downturn. But there is a strong case for it to be reaffirmed publicly by a review. There is also a strong case to include more professional economists on the RBA board and more representatives from the labour welfare movement. A big risk would be a populist push to load up the RBA’s objectives with other considerations such as house prices, equality and climate. This would just muddle the RBA given its limited policy tools. Such objectives are the responsibility of government which has a broader array of policy tools.

Coronavirus update

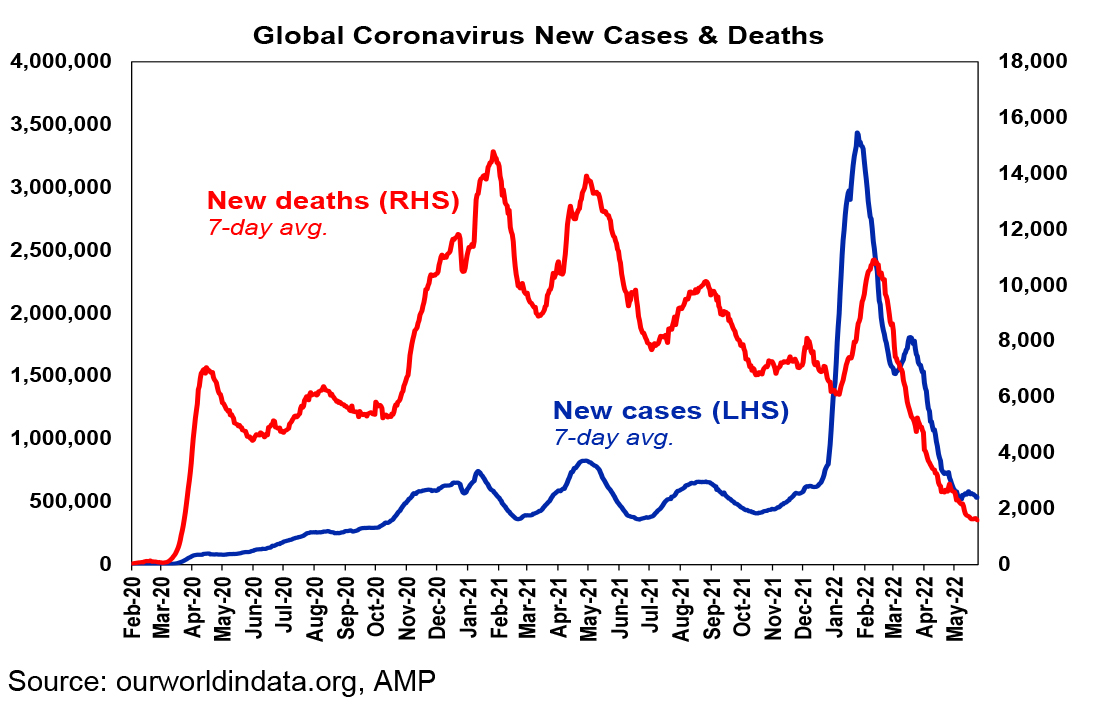

New global Covid cases fell slightly over the last week with a further decline in Europe. New cases continued to trend down in China and have now rolled over in South Africa again.

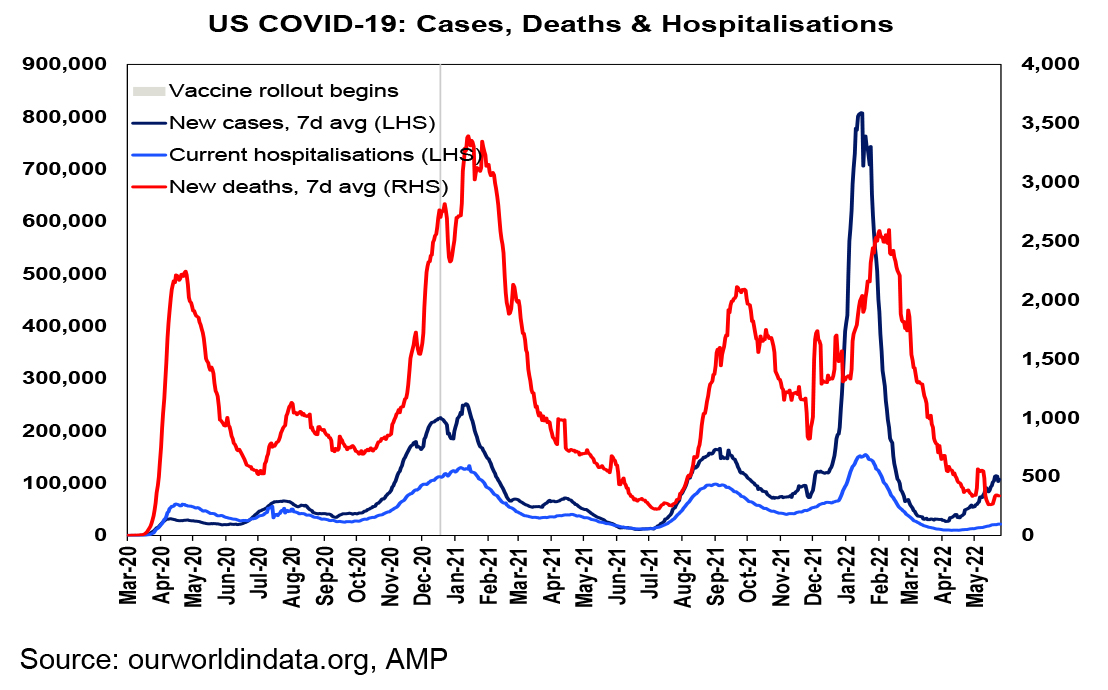

While the US is seeing a rising trend its relatively mild and hospitalisations and deaths (which are not affected by people not reporting) remain subdued.

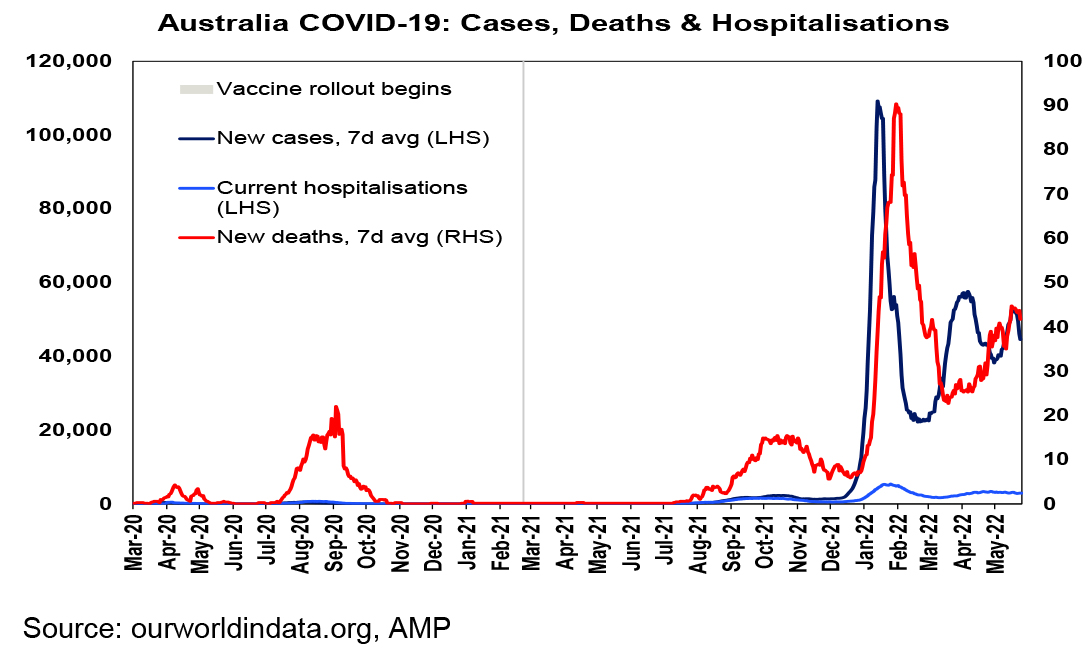

The recent rise in new cases in Australia has rolled over again and hospitalisation and death rates remain low compared to pre-Omicron waves.

Monkeypox does not look like becoming the new Coronavirus. While the spread of cases outside Africa is causing concern compared to Covid it’s not as easily transmissible (requiring contact), there are vaccines against it with the Smallpox vaccine around 85% effective in preventing Monkeypox infection and there are treatments for it.

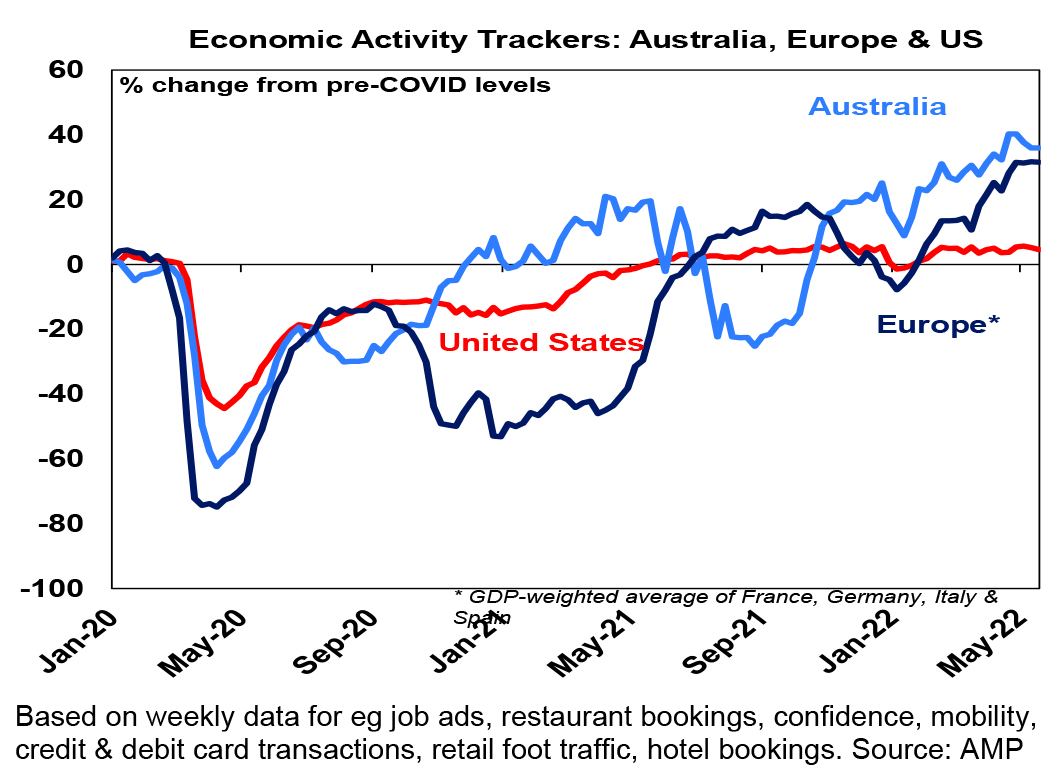

Economic activity trackers

Our Australian Economic Activity Tracker was little changed over the last week but remains strong. Our European Tracker was little changed but the US fell a bit. Given the rising risk of recession our Economic Activity Trackers are worth watching as they are based on weekly data and so give a timely guide.

Major global economic events and implications

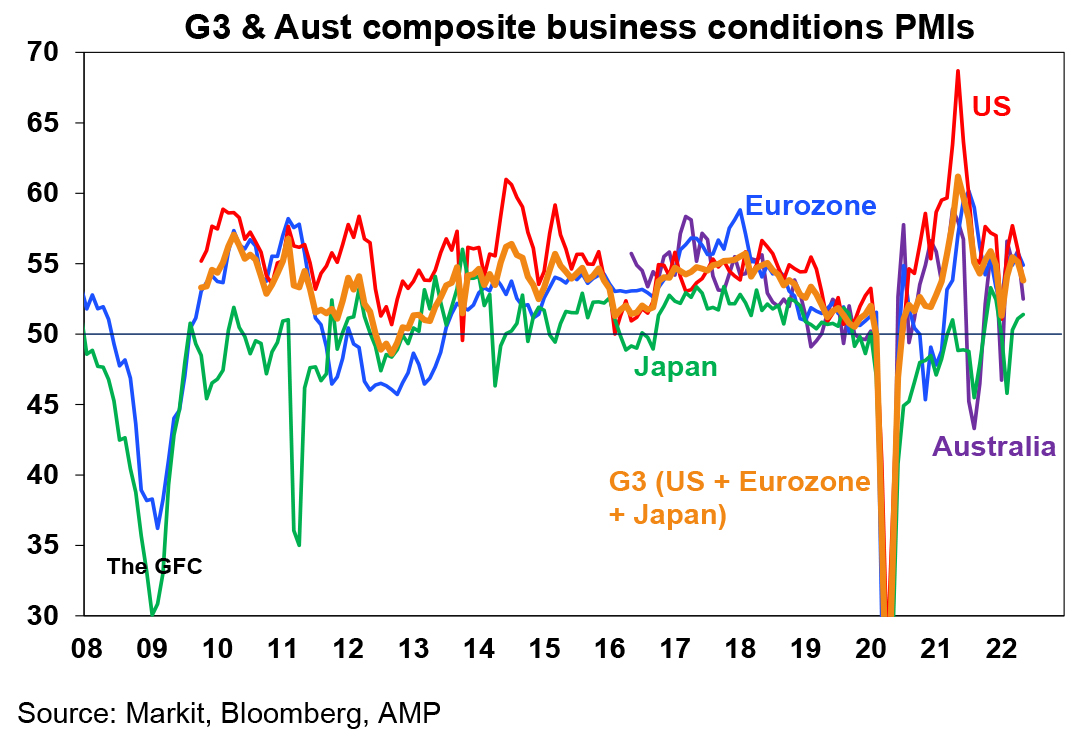

Business conditions PMIs remain strong but slowed a bit further in May with a rise in Japan but declines in the US, UK, Europe and Australia. The G3 average composite PMI fell 1.3pts but to a still strong 53.8.

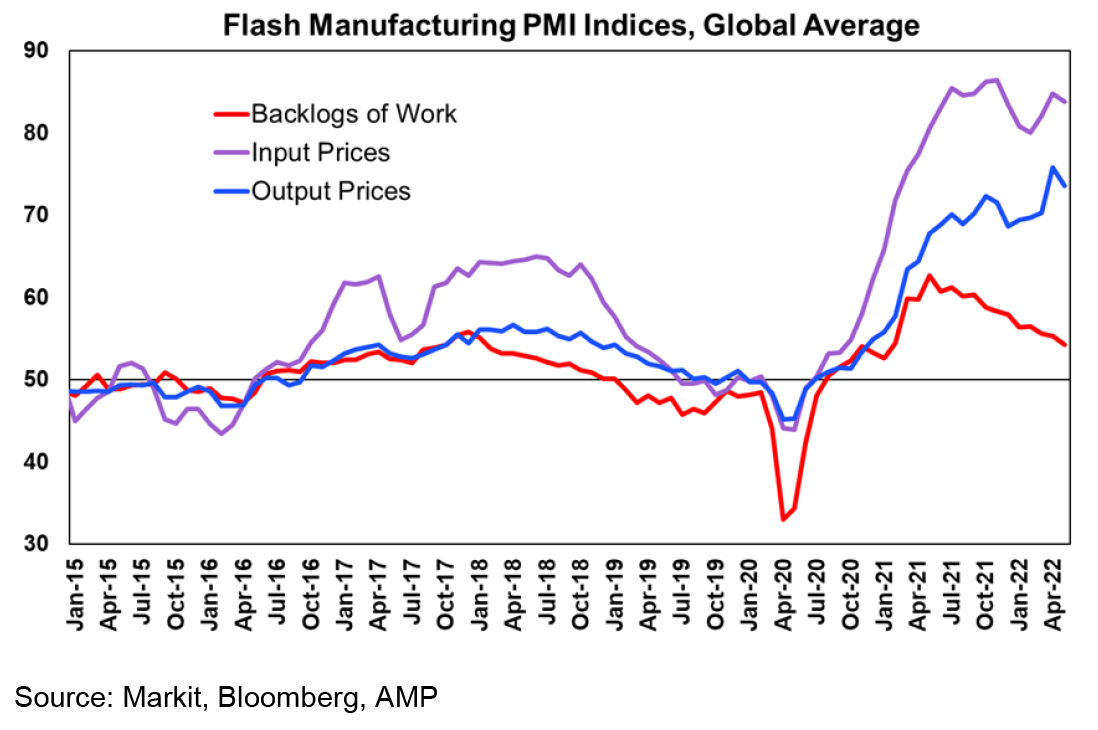

Price measures and work backlogs for manufacturers have eased but remain high.

Apart from the decline in the US business conditions PMI for May other US data was mixed. Durable goods orders rose with continuing solid gains in underlying capital goods orders and shipments pointing to solid growth in business investment. Initial jobless claims fell although the 4-week moving average trending up. But new home sales fell reflecting the impact of higher mortgage rates (and home builders delaying sales) and initial unemployment claims continued to rise pointing to some cooling in the jobs market.

The Chinese Government announced more stimulus measures including additional tax cuts to help support growth. However, the measures were relatively modest with the tax cuts amounting to about 0.1% of GDP. More measures are likely though but so far, there seems to be a confusion between President Xi advocating a focus on zero covid and Premier Li who seems more focussed on boosting growth.

Australian economic events and implications

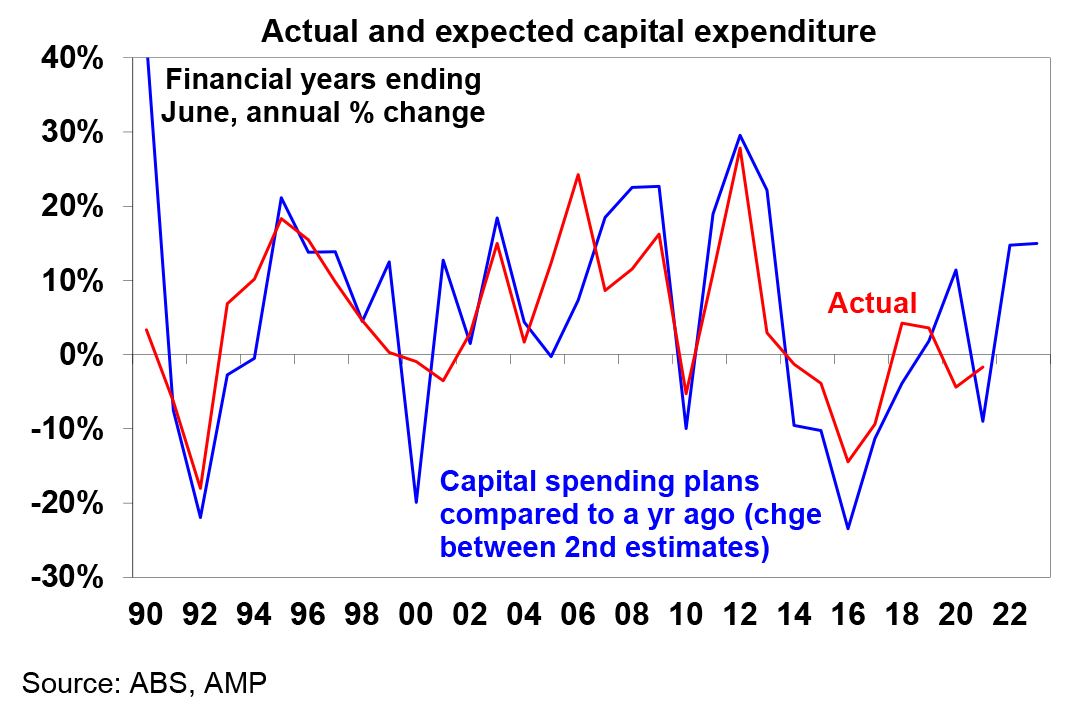

Australian construction hit by supply constraints and floods, but the outlook looks strong. First the bad news. March quarter construction fell 0.9%qoq and this included a fall in dwelling construction as constraints on the supply of building materials and labour impact along with east coast flooding. This weighed down business investment in the quarter which fell 0.3%. All of which is a dampener on March quarter GDP growth. But there was also good news. Plant and equipment investment rose by 1.2%qoq. Business investment plans for 2022-23 rose a solid 12% on 3 months ago and are up 15% on plans for 2021-22 from a year ago pointing to a strong outlook for growth in investment. See the next chart. And there is a huge pipeline of homes that have been approved and commenced but are yet to be completed pointing to plenty of work for home builders still ahead even as housing demand slows with higher mortgage rates and poor affordability.

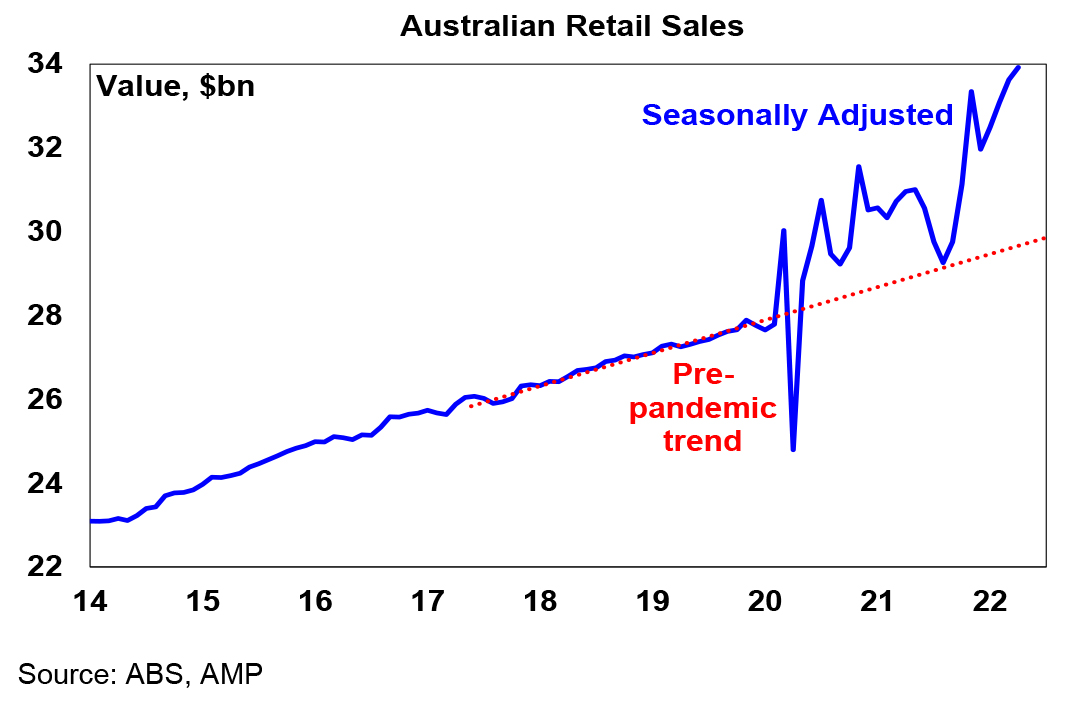

Australian retail sales rose a strong 0.9% in April, taking them to about 15% above their pre-covid trend. This is only partly due to rising prices and mostly reflects the surge in goods demand through the pandemic so it will likely slow as demand continues to rotate back to services. In the meantime, consumers still seem to be spending despite cost of living pressures – helped along by the strong jobs market and excess saving built up through the pandemic.

What to watch over the next week?

In the US, the main focus is likely to be on May job data (Friday) which is expected to show payrolls up 330,000, unemployment falling slightly to 3.5% and wages growth slowing slightly to 5.2%yoy (from 5.3%). In other data, expect house price gains to remain strong but consumer confidence to fall (both Tuesday) and the ISM manufacturing and services indexes (Wednesday and Thursday) to fall slightly.

The Bank of Canada (Thursday) is likely to raise its official cash rate by another 0.5% taking it to 1% with the BoC remaining hawkish citing the risk of higher inflation expectations as well as citing concerns about the global growth outlook.

Eurozone confidence data for May (Monday) is likely to show a further softening, core inflation (Tuesday) is likely to show a further rise and unemployment (Wednesday) is likely to remain at 6.8%.

Chinese business conditions PMIs for May (due Tuesday and Wednesday) are expected to improve a bit but remain weak reflecting Covid restrictions.

In Australia, March quarter GDP (Wednesday) is expected to be flat and up 2.3%yoy, with drags from net exports (which are expected to detract 1.8 percentage points) and dwelling investment, weak growth in business investment and solid growth in public spending and consumption. Note though that this follows very strong growth of 3.4% in the March quarter and domestic demand will still be strong. In other data expect building approvals to show an 8% gain after plunging in March and housing credit growth to remain solid (both Tuesday), CoreLogic data for May to show a 0.3% decline in average capital city prices led by a 1% fall in Sydney and 0.6% fall in Melbourne (Wednesday), the trade surplus (Thursday) to fall back to $8.5bn and housing finance for April (Friday) to fall 0.5%.

Outlook for investment markets

Shares are likely to see continued short term volatility as central banks continue to tighten to combat high inflation, the war in Ukraine continues and Chinese Covid lockdowns impact driving fears of recession. However, we see shares providing reasonable returns on a 12-month horizon as global recovery ultimately continues, profit growth slows but remains solid and interest rates rise but not to onerous levels.

Still low yields & the risk of a further rise in bond yields points to constrained returns from bonds.

Unlisted commercial property may see some weakness in retail and office returns (as online retail activity remains well above pre-covid levels and office occupancy remains well below pre-covid levels), but industrial property is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices are expected to fall as poor affordability and rising mortgage rates impact. Expect a 10 to 15% top to bottom fall in prices over the next 18 months but with a large variation between regions. Sydney and Melbourne prices are already falling.

Cash and bank deposits are likely to provide poor returns, given the still low cash rate of just 0.35% at present but they should improve as the RBA raises interest rates further.

The $A could remain volatile in the short term if Chinese Covid lockdowns persist. However, a rising trend in the $A is likely over the next 12 months helped by strong commodity prices, probably taking it to around $US0.80.

By Shane Oliver