Five takeouts for advisers to enable a better understanding of dividends in the Australian market context.

A stock-take of Australian equity dividends from an investor’s perspective results in a number of conclusions. Max Cappetta, CEO of GSFM investment partner Redpoint Investment Management shares five key takeouts.

In the year ended 30 June 2022, shareholders were rewarded with more than $90 billion in cash dividend payments, a record level and an incredible turnaround from the previous two years. Further strong dividend payments are expected as we head into the Australian corporate reporting season in August 2022 despite the share price volatility experienced since the beginning of calendar year 2022.

Share prices are more volatile than dividends and, despite current market volatility, Redpoint expects a cash dividend yield of approximately five percent is expected from ASX200 stocks for the 2022-23 financial year. When compared to current term deposit rates of 1.45% for one year[1], dividends should continue to be attractive to investors.

Takeout #1: The valuation readjustment continues

Interest rates are rising back to pre-pandemic levels, a situation that’s more than simply a ‘return to normal. Instead, central banks are fighting an old adversary, inflation, which has been dormant for more than two decades. This means rates potentially need to go higher than would be required for a ‘return to normal’ because they’re an important tool to curtail inflation, both as it is today and expectations for inflation in the future.

Equities are also being repriced for higher interest rates and, as a result, equity prices have declined. The US market has had its worst start to a calendar year in decades, falling approximately 20 percent. The Australian equity market has also fallen, approximately 10 percent year to date.

If inflation is seen to be hitting a peak, then expectations for the crest in this interest rate cycle will soften. If inflation is more entrenched than anticipated, interest rates will most likely move higher to counter it, which will have a knock-on impact on economic growth and equity pricing.

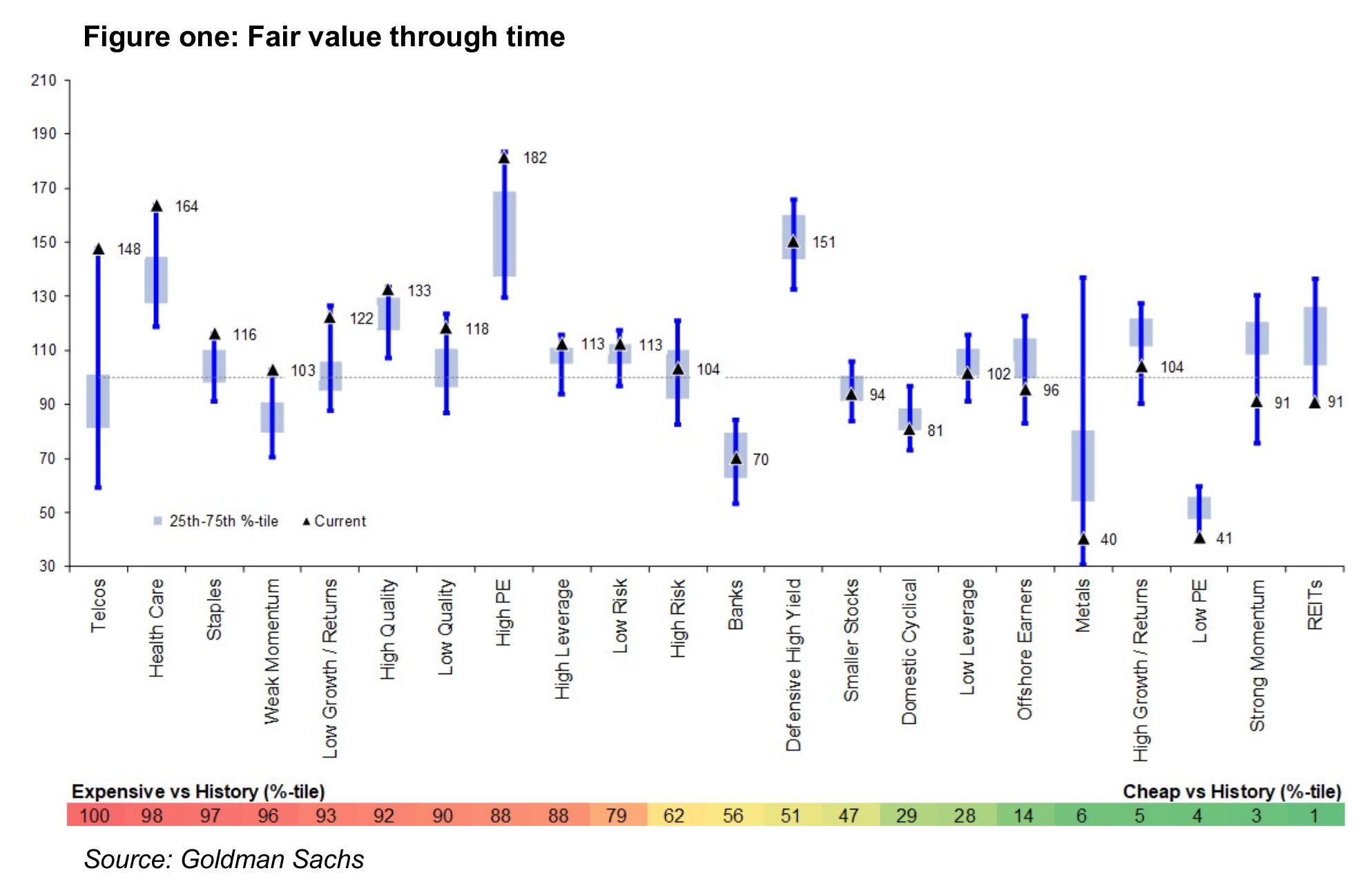

History shows that price adjustments typically overshoot fair value in both directions (figure one). We are now likely close to being at, or still slightly above, an ‘aggregate fair value’. This means a further 10-20 percent overshoot on the downside remains feasible at current estimates of forward earnings. Despite this current valuation readjustment, earnings expectations remain reasonably solid for the 2022 calendar year and 2023 financial year at this stage.

Takeout #2: Earnings and dividend remain robust for calendar year 2022

The Australian economy was able to weather the pandemic better than most due to the unprecedented fiscal and monetary actions of government and the RBA. Listed companies were also conservative in 2020, cutting dividends and hoarding cash, while making good use of the available cheap debt.

Income seeking investors have been well rewarded in financial year 2022 with a record cash dividend harvest of almost $90 billion, almost 50 percent more than the ‘bonanza’ $62 billion paid in financial year 2021. Australian equity income investors were rewarded by iron ore miners and share buybacks, from companies including CBA, NAB, Westpac, Woolworths and JB HiFi. Some companies, such as JB HiFi and supermarket operators were distinct beneficiaries of COVID lock downs and were able to grow revenue, profits and dividends consistently since 2019.

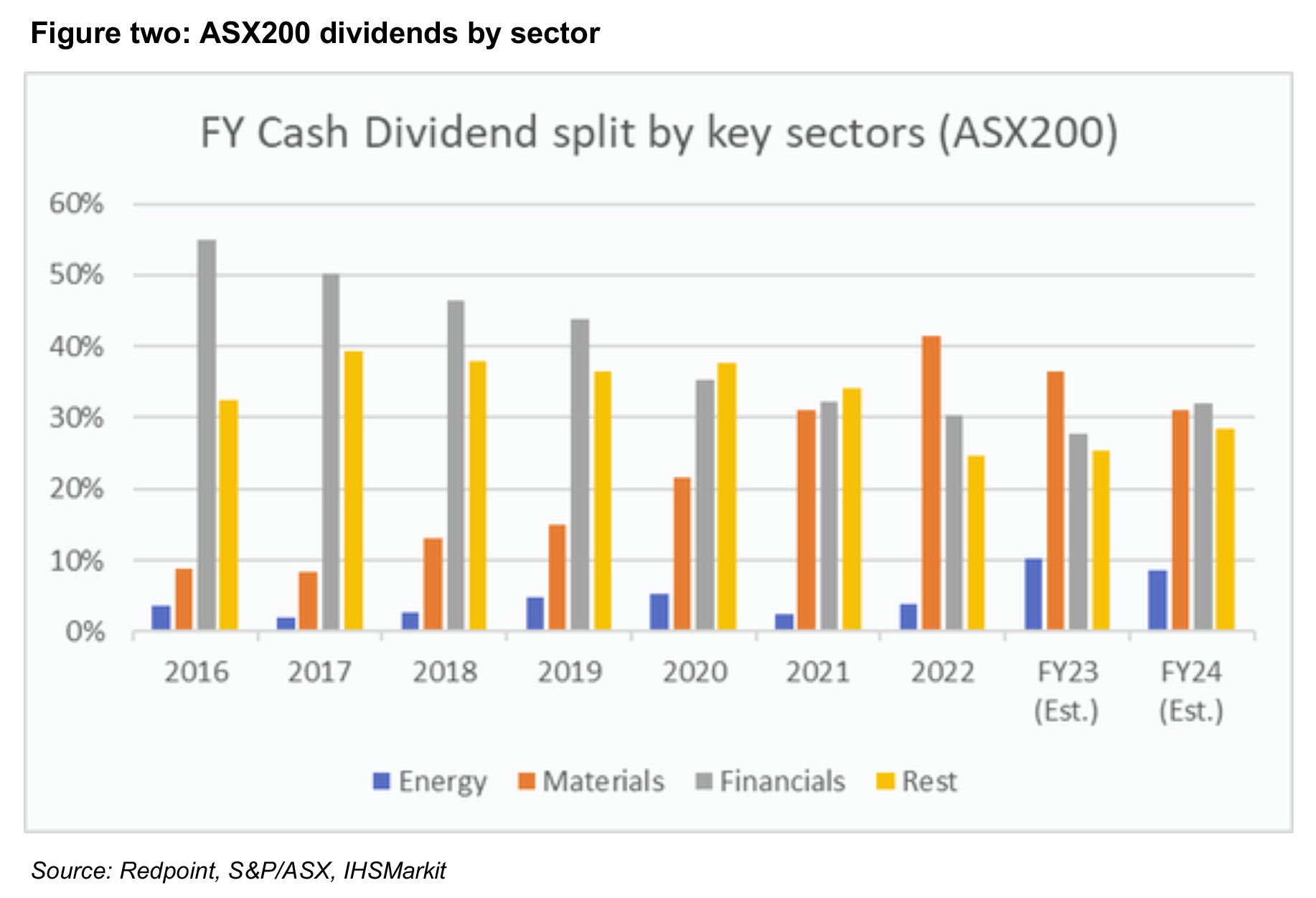

Figure two highlights the enormous cyclicality in dividends by sector over the last seven years and expectations for the next two years.

Looking ahead, 2023 appears as though it will be slightly better again. What’s of greater interest, however, is the underlying dynamics in terms of the industries and companies actually growing their earnings, growing their profits and being able to maintain these dividend payments.

So although the equity markets have dropped in price, there haven’t yet been any strong negative revisions to earnings expectations for financial year 2023 thus far. The upcoming August reporting season is expected to report a robust financial year for 2022, however, it’s all going to be about the forward guidance companies might provide in terms of costs and profitability.

Redpoint forecasts that the materials sector is likely to have a strong year in terms of dividend payments in 2023, but it’s expected to be weaker than 2022. The real standout is the energy sector, the only sector to have posted a positive return on a year to date basis. The pricing of oil and gas, and particularly coal, is driving energy stocks to experience supernormal profits; therefore, they will be the companies with large dividend payments.

Investors need to be mindful of the volatility of commodities and the resources sector; while dividend payments may be attractive this year and next, investors need to look ahead in terms of the profile of those dividend payments in future years as share prices will move ahead of changes in earnings and dividends.

Takeout #3: The 142 opportunity

Inclusive of franking credits, the ASX200 has delivered an attractive yield relative to term deposits over the long term – and especially over the past decade. Driven by underlying economic growth, the resilience and rise in share prices is also a characteristic of dividend payments through time. Furthermore, Australian corporates continue to favour higher payout ratios due to Australia’s policy of attaching tax credits to dividends for the tax paid on profits earned by companies.

This payment of tax credits is what Redpoint refers to as the ‘142 uplift’. Every dollar of fully franked dividend carries with it a 42 cent tax credit that zero tax rate retiree investors can fully reclaim at year end. For every dollar of fully franked dividends a retiree at a zero tax rate earns from a company, they’re actually getting $1.42 worth of value. For every dollar of interest income that same retiree earns from a bank deposit, they get a dollar of interest income. On the flip side, when the investor reclaims their term deposit, they receive their capital in full. The same cannot be said about equities; price volatility means an investor may or may not get back the total amount invested.

Example: If the total return of the Index is 8%, made up from 4% cash dividend and 4% growth, the associated tax credit will be ~1.7% (fully franked) or 1.3% (75% franked). Changing the split to 6% cash dividend and 2% growth still gives the same pre-tax total return of 8% but the tax credit is now 2.5% (fully franked). This 1.2% p.a. higher than holding a passive investment.

This is an additional benefit for retired income investors and opens up a range of investment strategies that combine capture of these valuable dividends and credits along with an active stock selection approach aimed at ensuring that an investor has a diversified exposure to a broad range of companies listed on the ASX.

When one truly appreciates the power of the 142 uplift it becomes obvious that an investment approach that can capture a higher level of franked income while delivering the same overall total return as the ASX200 provides a materially better outcome when compared to investors who simply hold the index or low dividend portfolios and sell assets to fund their annual income needs.

Takeout #4: Headwinds, tailwinds and opportunities ahead

While there has been some volatility in dividends over the last few years, Australian equity income investors are currently well positioned. The largest potential headwind is whether interest rates will be increased to the point where they actually cause a recession.

In such a scenario, investors need to carefully consider how they position their portfolios to ensure they capture both a sufficient dividend yield, which will likely be better than the interest rates offered on term deposits, and also capture reasonable long-term capital growth.

Sentiment and behavioural biases also make share prices fluctuate. Sentiment can cause share prices to be depressed because of expectations or extrapolation of interest rates moving higher and inflation getting out of control. Such sentiment driven price falls can create an opportunity to buy income cheaply because share prices are depressed while the underlying fundamentals for companies remain less volatile.

Importantly, the profitability of companies and industry sectors are cyclical, which in turn drives cyclicality in dividend payments; yesterday’s dividend payers are likely to be different to tomorrow’s dividend payers. After all, last year’s dividend windfall for iron ore miners is expected to fall back in the years ahead as commodity prices cycle with supply and demand. This is where a forward looking approach is important both in terms of identifying the next winners while also having a view on which future dividends may be cut.

One of the major opportunities is demographics, both in Australia and other developed nations, where almost one third of the retirement savings pool will move into the retirement phase over the next 10 years. In Australia, that’s almost a trillion dollars that will move from accumulation to retirement.

Redpoint believes there will be a greater focus on companies paying dividends – and focusing on maintaining a consistent dividend – because that will become attractive to a far greater proportion of investors in the marketplace.

This may in fact become a tailwind; some of these stocks that can maintain consistency of dividend payments may trade at a slight premium because those characteristics will be increasingly in demand.

Many people in retirement have traditionally sought low risk investments, namely cash and term deposits. For example, Australia’s SMSF sector has nearly $150 billion sitting in cash and term deposits, 16.5 percent of the $892 billion in SMSF assets, at 31 March 2022[2].

In the current environment, and potentially for the foreseeable future, the low-risk or no-risk investment has in fact become the low return or no-return investment. When inflation is factored in, cash does not provide a positive return and it becomes challenging to maintain the purchasing power of retirement capital over the longer-term.

For retirees to achieve a growing income stream, as well as ensure that their capital stays in line with purchasing power and inflation, equities are an obvious solution.

Takeout #5: Equity investments are an attractive source of income

Long term purchasing power

Consumer purchasing power is linked to inflation which in turn is driven by the long term average growth in the economy. The earnings – and therefore dividends – of ASX200 companies are determined by these same drivers. History shows that over the long term, dividends grow through time in line with earnings.

In an inflationary environment, equities are considered to provide some hedge against inflation. Most companies can increase the cost of their goods and services to maintain profitability and their ability to pay dividends.

While cash and fixed income investment have a place in a comprehensive retirement income plan, they will be insufficient on their own. Interest rates paid by banks and other similar institutions are determined by the prevailing monetary settings of the central bank. These settings are determined by a range of factors and have drifted lower over the past decade as central banks sought to induce growth and inflation to avoid a Japan like deflationary spiral.

Ultimately cash deposits are capital guaranteed and that guarantee comes at a cost…no capital upside. Over the long term, the total return of the Australian equity market is approximately evenly split between dividend yield and price return.

Dividend yields at 4%+ remain attractive versus cash like investments. The long term uptick in price (even by just a few percentage points) is an important component to maintaining overall purchasing power in retirement, something cash-like investments cannot deliver.

Dividends exhibit consistency

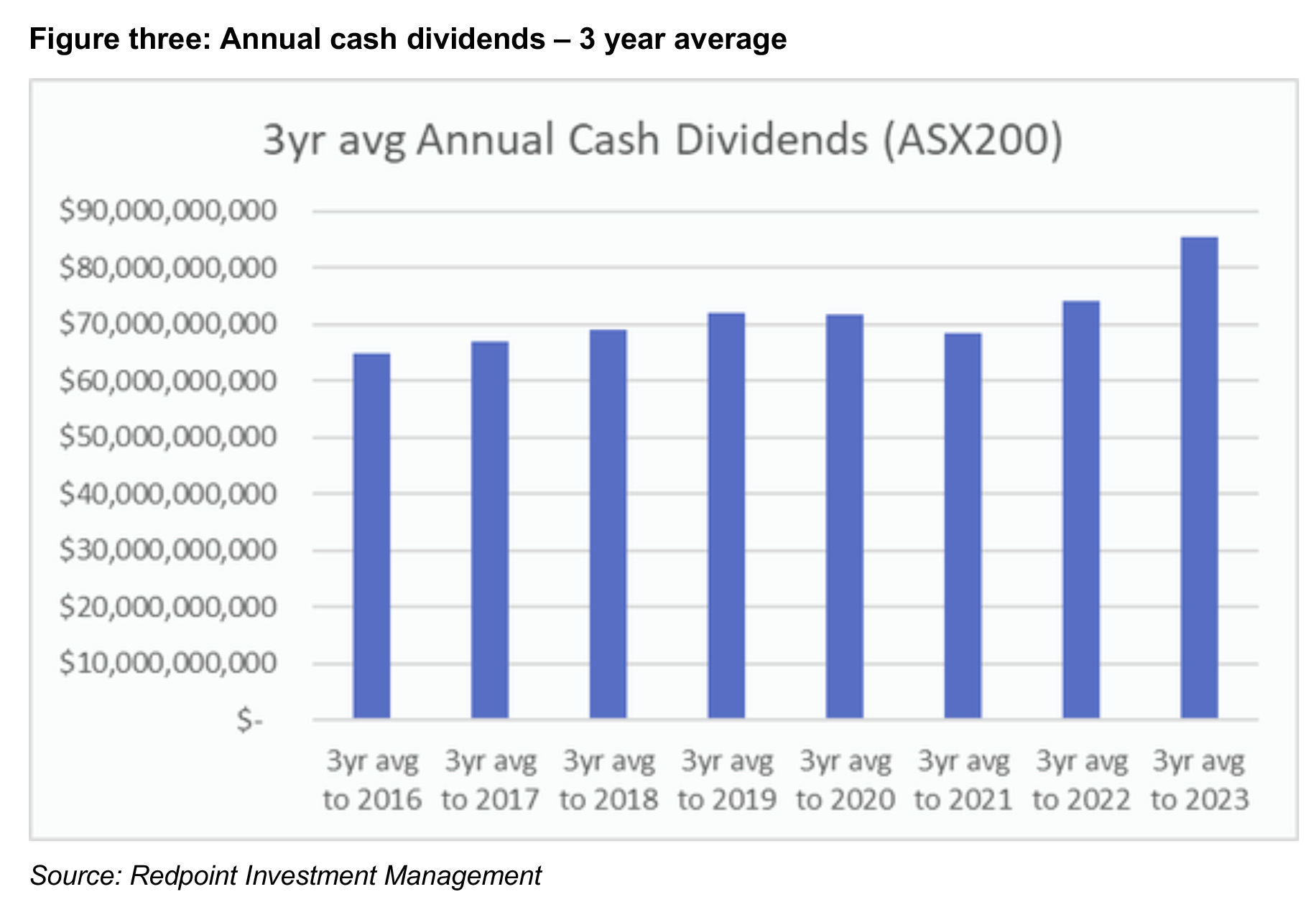

Companies will set payout ratios with flexibility to pay out a higher or lower percentage of their profits each year, which allows them to smooth out the inevitable fluctuations in their profits and cashflows each year. An examination of the volatility of dividend payments by Redpoint found that when averaged across a three year period, dividend payments have been reasonably consistent.

Figure three illustrates that dividend payments have exhibited stability when averaged over a three year period. Lower share prices today point to the ability for investors to purchase a dividend stream for the same price as December 2020 or September 2019.

Capturing a consistent dividend yield from equities cannot be a set and forget endeavour. Building a portfolio from last year’s best-yielding stocks may deliver above average dividend income, but won’t necessarily meet other objectives, such as being able to keep up with inflation and the cost of living for retirees over their entire retirement period. This is because a singular focus on high dividend yield can also be a proxy for companies with low growth potential or corporate stress which may lead to cuts in dividend payments in future. A sole focus on that one concept of yield can also result in a very concentrated portfolio that’s invested in a narrow range of sectors, such as financials and the mining sector at present and this may result in a poorly diversified portfolio which is at risk if those specific sectors perform poorly in future.

Earning income by owning a share of the profits paid as dividends by Australia’s leading companies remains a critical part of a long-term retirement income plan. Taking an active approach which seeks to earn an above average dividend yield coupled with stock selection insights can deliver investors with better long-term results versus owning a passive portfolio and supplementing income needs by selling assets over time. While share prices are volatile in the short term, dividend payments are less so and can provide additional benefits via franking credits for retiree investors.

———-