A better understanding of the in-home care system and home equity can be utilised to help your clients.

Australians have long regarded their home as their castle. And for many retired Australians, home is also a safe haven, something that has become increasingly apparent since the COVID pandemic reached our shores in 2020. This, coupled with the findings from the Royal Commission into Aged Care Quality and Safety – and the stories emerging from aged care during COVID – have reinforced the desire to stay at home and age in place.

Ageing in place means your client remains in their own home, retaining independence and autonomy, as they age and their health needs change. Lots of benefits come from doing this. A familiar home improves perceptions of security, helps to maintain social connections and provides access to services and proximity to family and friends.

Of course, ageing in place can also take place in a new home your client has downsized to, or even in a retirement village or residential care community that provides a homelike environment. However, for most older Australians, their family home is where they are and where they want to stay. The benefits of ageing in place at home don’t just include comfort and familiarity, but it also means retaining the largest financial asset many people ever own.

So, how can advisers help their retired clients – or their clients’ parents – fund their in-home care needs?

Government funded care

At 84%, the majority of Australians receive government funded aged care in their own home. The government’s Aged Care Data Snapshot[1] shows a total of 1,196,106 Australians were receiving government funded aged care at 30 June 2021. Of that number, 15 percent received an in-home care package (HCP) and 69 percent received Community Support at Home (CHSP).

Both of these services offer a level of care in the home.

CHSP

CHSP generally provides one to two services to older Australians, worth a maximum of $8,000 per annum. It provides ‘entry-level’ support for those who need some help to stay at home. If a client needs some home assistance, the service providers work with them to maintain their independence.

CHSP services may include[2]:

- social support – social activities in a community-based group setting

- transport – help to get out and about, for shopping, appointments or medical services

- services provided at home may include:

- domestic assistance – household jobs such as cleaning, washing and ironing

- personal care – help with bathing or showering, dressing and hair care

- home maintenance – minor general repairs and care of your client’s house or garden; this might include changing light bulbs, replacing tap washers or weeding and mowing

- home modification – minor installation of safety aids such as alarms, ramps or support rails

- nursing care – a qualified nurse makes a home visit for basic medical issues, such as the wound dressing.

HCP

Home Care Packages (HCP) provide access to affordable care services to obtain help and support in the home; the ongoing worth of an in-home care package is a maximum of $58,400 per annum (including extra payments for conditions such as dementia). While the HCP provides similar services to CHSP, the services are more customised to meet your client’s individual needs.

There are four levels of HCP available, depending on the level of care required (figure one). Unfortunately, it’s not uncommon for the recipient to receive funding for a package tier lower than that required, resulting in a funding (or service) shortfall.

The first step toward receiving a government funded HCP is an assessment. According to Kate Lambert, CEO of Daughterly Care, older Australians need the assessment to be accurate, although they typically understate their needs. It’s typically a generational thing, where being stoic and resilient is valued, and living through a depression and world wars have affected their lives and attitude towards money. Often, care and support is perceived as an indulgence.

Factors that lift the level and priority of HCPs include:

- lack of support network

- a carer who is not coping

- an ‘at risk’ elder

- physical issues such as blindness, the inability to feed oneself or being bed bound.

HCP Costs

All older Australians are entitled to some degree of government supported in-home care. Many of your self-funded clients may believe that because they’re self-funded, they would not be entitled to a government subsidised HCP, but they are. However, it’s expected that your clients will contribute to the cost of their in-home care if they can do so. The amount they have to pay will vary according to the level of care and types of services they receive.

If your client needs a higher level of care than the HCP they are allocated, their out of pocket expenses will be higher. This is why the accuracy of the assessment is all important.

There are two types of fees:

- Those where the consumer is expected to contribute; these fees are set by the government.

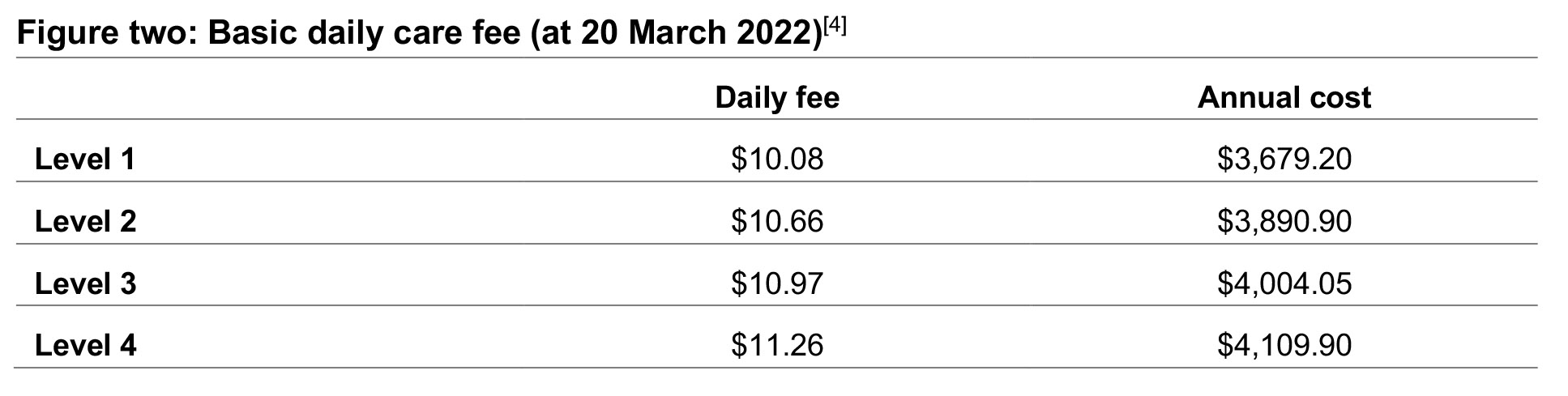

a. Basic Daily Care Fee

The basic daily care fee is a co-contribution to the government funding and is spent on your client’s care. It is calculated daily, paid monthly and charged seven days per week. This fee increases on 20 March and 20 September each year. It’s shown as a daily or annual cost in figure three.

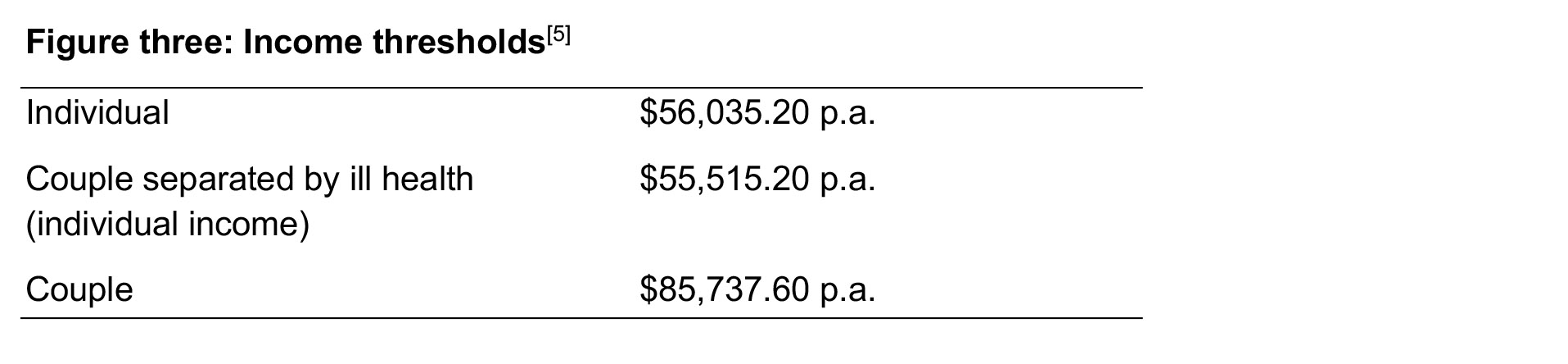

b. Income Tested Care Fee

If an individual or couple meets or exceeds the income thresholds (figure three), they are deemed to be fully self-funded and will be charged the maximum income tested care fee.

For a fully self-funded retiree, the maximum income tested care fee is $11,759.74 p.a. For those on a part pension, it’s a maximum of $5,879.85. Although it’s an income test, some assets like shares and bank accounts are deemed to earn a certain income for this assessment. It also considers and account based pensions, managed investments and debentures. There’s a lifetime payment threshold of $70,558.66.

Kate Lambert recommends that if you and/or your client know that they’re fully self-funded, then they’re going to pay the maximum income tested care fee anyway – so to avoid complex paperwork, it is simplest to tick the box for your client to pay the maximum fee.

- Those paid by the HCP itself, which are deducted from the Government Funding.

a. Case Management Fees

This fee is for managing the care of the client – writing the initial care plan, conducting reviews of the care plan (annually or when the client’s care needs change), selecting and managing the caregivers who service the client.

b. Home Care Package Management Fee

This fee covers the cost of administering the government funding – making sure the client receives the correct funding, paying for the client’s services, keeping the client within budget, providing monthly statements to the client and reporting to the government.

Funding in-home care

If your client wants to age at home, they need to apply for a government subsidised package and be prepared to top up their HCP. Although waiting lists for HCPs have decreased thanks to improved funding, in March 2022 there were more than 62,000 [6] on the waiting list. However, rather than wait, you client can self-fund the care they need.

Even once allocated a package, it’s not uncommon for your client to be offered a package at a lower level than meets their needs. At 31 December 2021, there were 23,779 people who had been offered an interim HCP while they wait for a HCP at their approved level[7].

There are three ways your client could potentially fund their in-home care, either wholly or to make up the shortfall between their allocated HCP and a care program that meets their needs.

- pay for care from existing retirement income streams

- draw on income producing capital assets

- draw on their home equity.

Drawing on income or income producing assets can impact quality of lifestyle and the longevity of retirement income. On the other hand, drawing on home equity can allow your clients to age well in place, access the care they need to remain in their home, without impacting the quality of their retirement income stream.

Using home equity can provide your clients with greater choice and flexibility when it comes to accessing services and selecting care providers. It can fill the gap until your client receives their HCP and, if additional care services are needed that the HCP doesn’t cover, it can pay for those too.

The following case studies illustrate real scenarios where financial advisers worked with Household Capital to establish home equity loans to cover their clients’ in-home care needs and enable those clients to meet their retirement objective, to remain at home and age, comfortably, in place.

Case study one: Jan and Phillip

Phillip (70) and Jan (69) live in their family home worth $3.95 million on Queensland’s sunshine coast. The couple also has $250,000 in superannuation and receive $39,000 per annum from pension and carer’s payments. Phillip has Parkinson’s disease and Jan is his full time carer. Although Phillip has been assessed at a level four HCP, there is still a gap to cover his full care needs and medical expenses. They have three children who are their equal beneficiaries.

To pay for the additional care over and above the HCP, Phillip and Jan have been drawing down on their super, as well as from another reverse mortgage that their financial adviser had provided a strategy for.

They love their home and want to remain there as long as possible, subject to health and the in-home care regime working for Phillip. If the situation arose that Phillip needed to go into residential care, they would consider selling so Jan could downsize. If that happens, they will then repay the loan through which they access their home equity.

The provider of the couple’s existing reverse mortgage no longer provides the product; therefore, they were unable to access additional equity, potentially leaving Phillip and Jan without a future income.

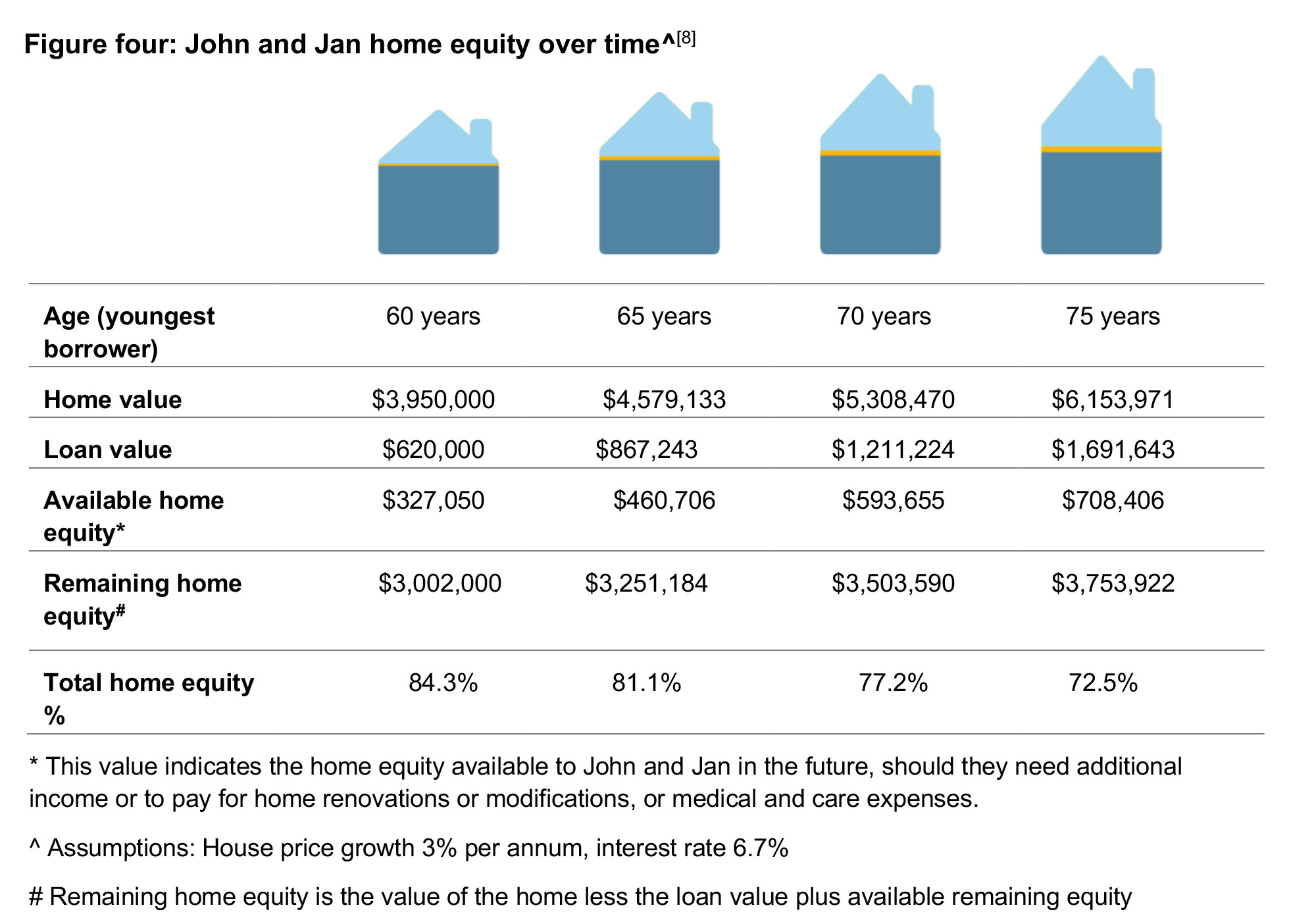

Based on Jan’s age – as the youngest borrower – the couple could access 24 percent of their home’s value, which equates to $924,000. They did not need to borrow this full amount; instead the couple established a Household Loan of $620,000. This was used as follows:

- monthly income stream of $2,500 to pay for care needs and medical expenses, for five years

- contingency fund of $50,000 for unexpected large expenses

- refinance higher rate existing reverse mortgage – $425,000.

Interest is only payable on amounts draw; therefore the monthly income and contingency fund only attracts interest as it is drawn down.

Based on conservative estimates, the profile of Phillip and Jan’s borrowings over time are illustrated in figure four.

Case study two: Ageing in place

Dennis, aged 68, retired early due to ill health. He lives alone in his home in Melbourne’s inner north, valued at $2,860,000. He requires around the clock care.

Dennis retired with significant superannuation assets; however, self-funding his care costs him $150,000 each year, a sum that quickly eroded his income producing assets.

Although Dennis acknowledges there will come a time when he’ll have to leave home for residential aged care, he wants to stay in his own home for as long as possible. He loves classical music and reading, his library housing extensive collections of books, discs and vinyl. He has the support of his children – they want him to be safe, happy and comfortable at home.

Dennis used a Household Loan to borrow an initial sum of $300,000 to fund two years of in-home care. This is drawn on a monthly basis; interest is only charged on the drawn value. He plans to reassess his situation in two years’ time to decide whether to fund a further two years of care.

It’s important to help your client to understand how government funding works and also how to best fund any shortfall. That way, your client will be in a position to age in place and meet their retirement goals. While navigating the system can be challenging, there are a number of support services designed to work with your clients and help them through the labyrinth.

Working with your client to support them through this complex process – whether for them or their parents – will reinforce the importance of your role as a trusted adviser.