Advisers need to articulate the value of their role.

Advisers are never more important than during periods of significant change. As the market transitioned from growth to value, change was everywhere, making the need for advice and reassurance with clients greater than ever. This article, proudly sponsored by Russell Investments, examines the value of financial advisers.

The past two years have delivered a challenging environment for investors, with many aspects of life during that time being encountered for the first time…a pandemic, lockdowns and other restrictions. Advisers had to work differently, markets became volatile and life as we knew it changed.

Through it all, financial advisers provided valuable assistance, helping clients review their evolving goals, needs and circumstances. This holistic wealth management requires a deep discovery process, planning and ongoing coordination, not always easy when you deal with clients remotely and anxiety runs high. As priorities and outlooks may have changed over the course of the pandemic, advisers have been keeping their clients were engaged, taking any actions with intent and purpose.

Those advisers who helped their clients remain invested through the turbulence, who helped them prepare for an uncertain future, who worked with them to determine their post pandemic goals, can look back with a real sense of having provided true value.

However, supply-chain issues and inflationary pressures are ongoing challenges. With the backdrop of geopolitical conflicts, central banks raising interest rates and heightened volatility in financial markets, ongoing advice relationships continue to deliver value to clients. Advisers are needed to help investors navigate all the possible changes in their personal and working lives, the evolving geopolitical landscape, and new virtual relationships.

How then, can you best articulate that value? In a recent paper, Russell Investments has detailed the five factors that measure and provide true adviser value to clients:

- asset allocation

- behavioural coaching

- helping clients through choices and trade offs

- expertise

- tax savvy planning and investment.

This article will examine the first two factors; the remaining will be discussed in part two of this series.

A is for appropriate asset allocation

How an individual is invested has a huge impact on achieving their investment goals. Many non-advised investors believe market timing or investment selection are the greatest determinants of portfolio success.

However, the real driver is asset allocation; research suggests that asset allocation drives over 85%[1] of the investment outcome for an individual. Yet, despite being the foundation of successful advice, this critical step of an advice process is often undervalued and underappreciated.

The first well-known study into the determinants of portfolio performance in 1986 found that asset allocation explained, on average, more than 90 per cent of the variation in total return. That same study showed that market timing accounted for an additional 1.7 percentage points in variation of returns, while security selection explained just an additional 4.2 percentage points[2] .

In the superannuation environment, there are generally two types of non-advised investors. Disengaged investors who are defaulted into a one-size-fits-all asset allocation, with very limited or no reference to their personal circumstances or needs. Or engaged investors, who build their own portfolios – which comes with its own risks. Being in an asset allocation that is appropriate to an individual’s personal needs can add value of up to 1.6% p.a.

Risk and reward

Appropriate asset allocation is not just about maximising returns, but also managing risk. In this context, risk means volatility, which is often what causes investors to doubt their investment plan and pull money out of the market, usually at the wrong time.

In periods of steadily rising markets, it can be easy to underestimate the value of a professionally managed portfolio. During these periods, self-directed investment portfolios often drift away from the initial asset allocation. A disciplined approach to portfolio management and rebalancing can ensure a portfolio retains its original asset allocation—and therefore remains appropriate for an investor’s stated goals—while also potentially reducing risk.

Actions you can take to convey the value of good asset allocation to your clients:

- Spend time articulating why getting the right asset allocation can be a key driver of achieving goals and the consequences of getting it wrong.

- Remind clients of the art and science of understanding true risk preferences.

- Use your investment philosophy to demonstrate how you select and implement an appropriate asset allocation to achieve their goals.

B is for behavioural coaching

For many investors, 2020 was their first experience of significant market drops and ongoing volatility. While volatility was somewhat dampened in 2021, it has come back to the forefront in 2022.

These last two years have been a clear demonstration of the importance of remaining invested through thick or thin. An investor who fled for the exits in mid-March 2020 when the pandemic emerged, would have had a difficult time to find the best re-entry point, with no real market “dips” to take advantage of. This is where the value from your behavioural guidance shows up on the bottom line.

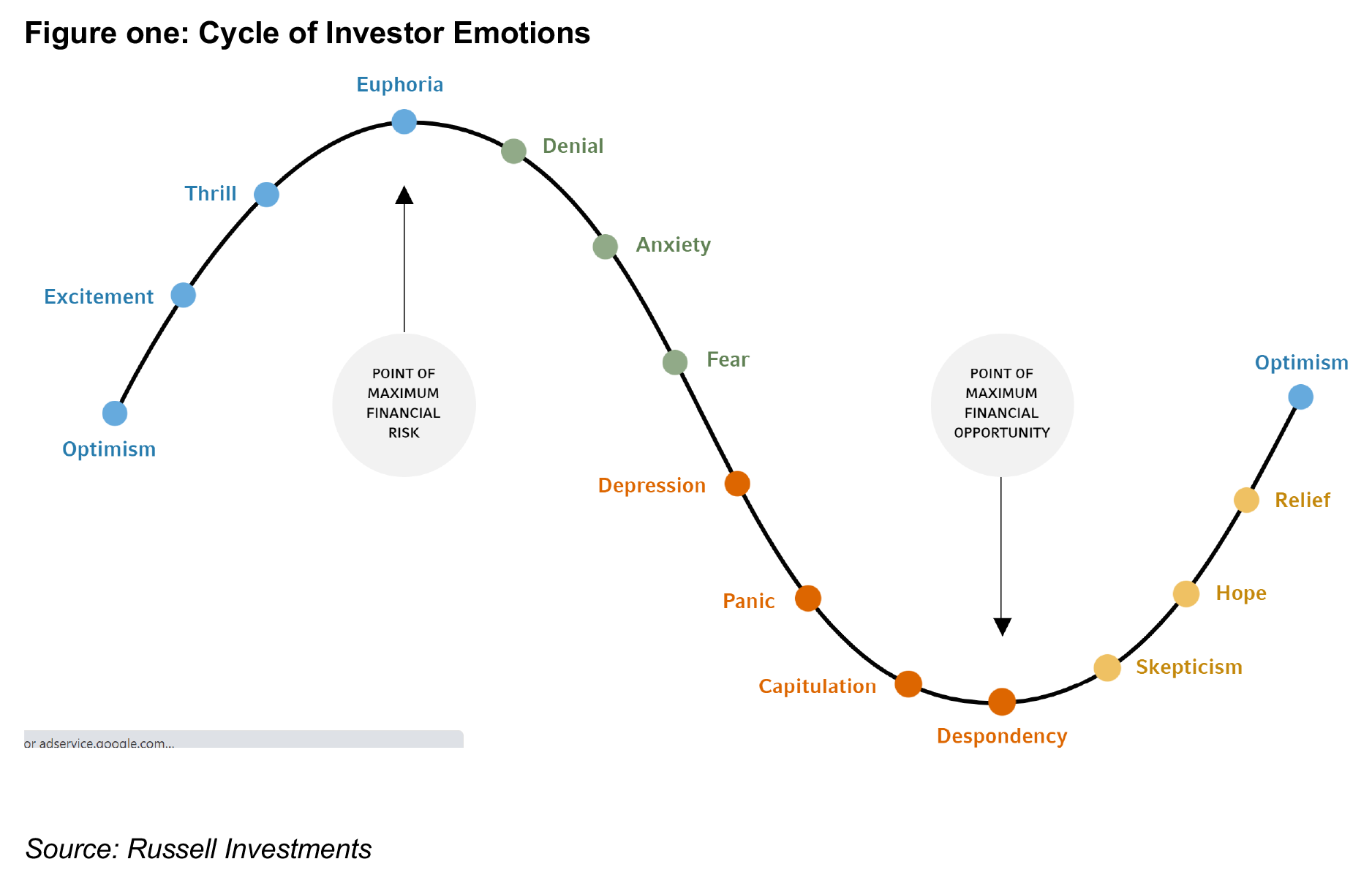

It’s a good time to revisit the Cycle of Investor Emotions (figure one). Recent market gyrations would have most investors fearful and anxious (in the green zone) – there are enough days with markets finishing in positive territory to temporarily buoy emotions, followed by sideways or a downward trajectory. Although there has been a lot of talk about an inflation driven bear market, it’s not following an historical path.

While unadvised investors may make rash decisions in this environment, an adviser can manage their clients’ emotions by explaining market cycles and how they might feel at different points. By educating clients, advisers can provide this ‘behavioural coaching’ to best position clients to ride out the vagaries of financial markets.

Investors typically start with optimism, which sits at the inflection point on the emotional upswing. At this point, investors expect things to go their way, or they expect to receive a return for the risk of investing. Investors go into the markets because they believe they will be able to grow their wealth through their investment choices.

When markets move in the direction the investor had hoped to see, they start to get excited about the possibility of even greater gains. This is when investors start hearing positive news stories in the media, coupled with tips from friends and colleagues, stories about how well their investments have done can mean investors are spurred on. This can be an attractive comfort zone because in such a scenario, investors are running with the herd.

When the momentum continues, investors can find the experience thrilling and begin to anticipate even higher returns – and sometimes start sharing their own tips!

As markets reach the top of the cycle, investors may experience euphoria.

At this point, the uneducated investor starts to believe that they made a smart move to invest when they did and believe that the good times will continue unchecked. In some cases, investors fool themselves into believing they can tolerate higher levels of risk and may begin to trade more frequently or invest in riskier asset classes.

The second phase of the cycle occurs when the market starts to turn. At first, investors watch anxiously to see if the downturn is just a blip. They may believe that things will improve shortly and therefore hang on to their investments. They often try to shield themselves psychologically from the bad news and move into denial.

As the markets continue to fall, denial gives way to fear. Investment values decline perhaps even to the point that investors begin to see losses. Bad news stories proliferate in the media and online. When market losses accelerate, real fear kicks in. Some investors may then turn defensive and switch out of riskier equities to more defensive equities or other asset classes such as bonds.

In the third phase of the cycle, the realities of a bear market come to the fore and an investor may become depressed and desperate

Investors who missed their chance to take profits may try to get their portfolio back into the black by either selling their worst-performing investments or moving into securities that don’t fit their risk profile. When that doesn’t work, panic sets in.

At this point, some investors feel at the mercy of the market and capitulate, pulling out altogether, abandoning investments at precisely the wrong time.

Those who remain invested may become despondent and wonder whether they should ever have invested their hard-earned money in the markets. Interestingly, this is the part of the cycle identified as the point of maximum financial opportunity.

In the fourth phase of the cycle, investors may experience some scepticism when markets start to rise. They often have a sense of caution or worry, wondering if market growth will last.

Though investors are hopeful about continued market increases, they may be reluctant to invest money—even at a point when prices are still relatively low and opportunities are attractive.

Eventually investors come to realise the market is recovering. For those investors who let their emotions rule their investment decisions, the market cycle can begin all over again – unless of course they have good financial advice and understand the cyclicality of the market and the importance of staying the course in the asset allocation recommended by their adviser.

Fear impacts opportunity

Fear can impact opportunity, as highlighted by the following three hypothetical investors’ journeys from January 2020 through to 30 June 2022:

- Investors who remained in the market for the full time period would have seen a $100 investment rise to $111 (blue line in figure two).

- An investor who moved to cash in March 2020 and then returned to the market a few months later at the end of the second quarter, would only have $99 at the end point (orange line in figure two).

- An investor who moved to cash in March 2020 and remained in cash for the entire year, then re-entered the market at the beginning of 2021, would have only $90 at the end point (grey line in figure two).

For many investors, 2020 was their first experience of significant market drops and ongoing volatility. While volatility was somewhat dampened in 2021, it came back to the forefront in 2022. These last two years have been a clear demonstration of the importance of remaining invested. An investor who fled for the exits in mid-March 2020 when the pandemic emerged, would have had a difficult time to find the best re-entry point, with no real market “dips” to take advantage of. This is where the value from your behavioural guidance shows up on the bottom line.

That’s the problem with abandoning an investment plan due to fear. Pulling out of the market when it is volatile can lock in losses and could lead to missing out on any subsequent rally. Without a crystal ball, it’s hard to time the perfect point to get back into the market once you’ve left.

As figure three illustrates, missing out on even a few days of good performance can have a detrimental effect on a portfolio. While markets can be unpredictable, their long-term trend has been up[3].

In fact, without your guidance, investors often buy when markets are euphoric and sell when markets are bearish. There is good value in your ability to help clients stick to their long-term financial plan and avoid the behavioural mistakes that may have them miss out on the market’s best days.

Actions you can take to educate your clients:

- Use a consistent framework for review meetings around when to and when not to make changes to a client portfolio.

- Develop a proactive client engagement plan for different client types and different scenarios.

As market commentators predict ongoing bear markets and market volatility to continue into 2023, it’s a really important time to reflect on the value you bring to your client relationships and ensure they are well prepared to whether the challenges ahead. As long as each client understands the rationale for their asset allocation and how it will meet their financial objectives, they are less likely to reach the levels of despondency – and make poor decisions – in the same way as unadvised investors may do.

———-