Tom Goodrich

It’s easy to become overwhelmed at the sheer volume of news, predominantly bad, that bombards us on a daily basis. War, pandemic and recession relentlessly frequent the headlines, with no respite.

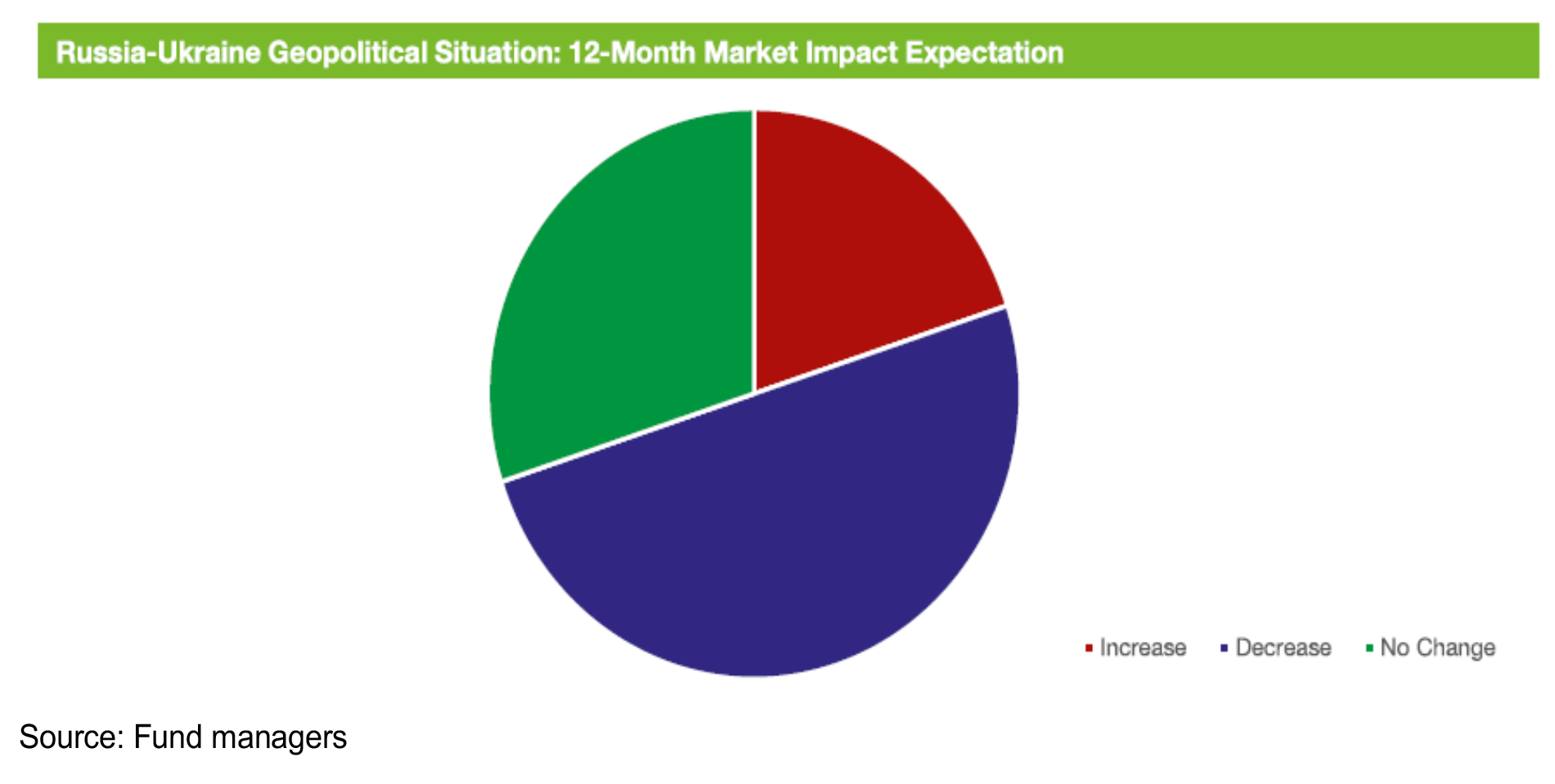

To gain a clear perspective on the state of certain conflicts, without sifting through the thousands of unnecessarily emotive ‘click-bait’ articles that flood news sites, we surveyed Zenith’s rated international equities – emerging markets managers on their perception of the current state of affairs between different countries, beginning with the Russia-Ukraine geopolitical situation.

Contrary to the negative headlines, of the managers that expressed a view, half believe the market impact of the Russia-Ukraine geopolitical situation will decrease over the next year.

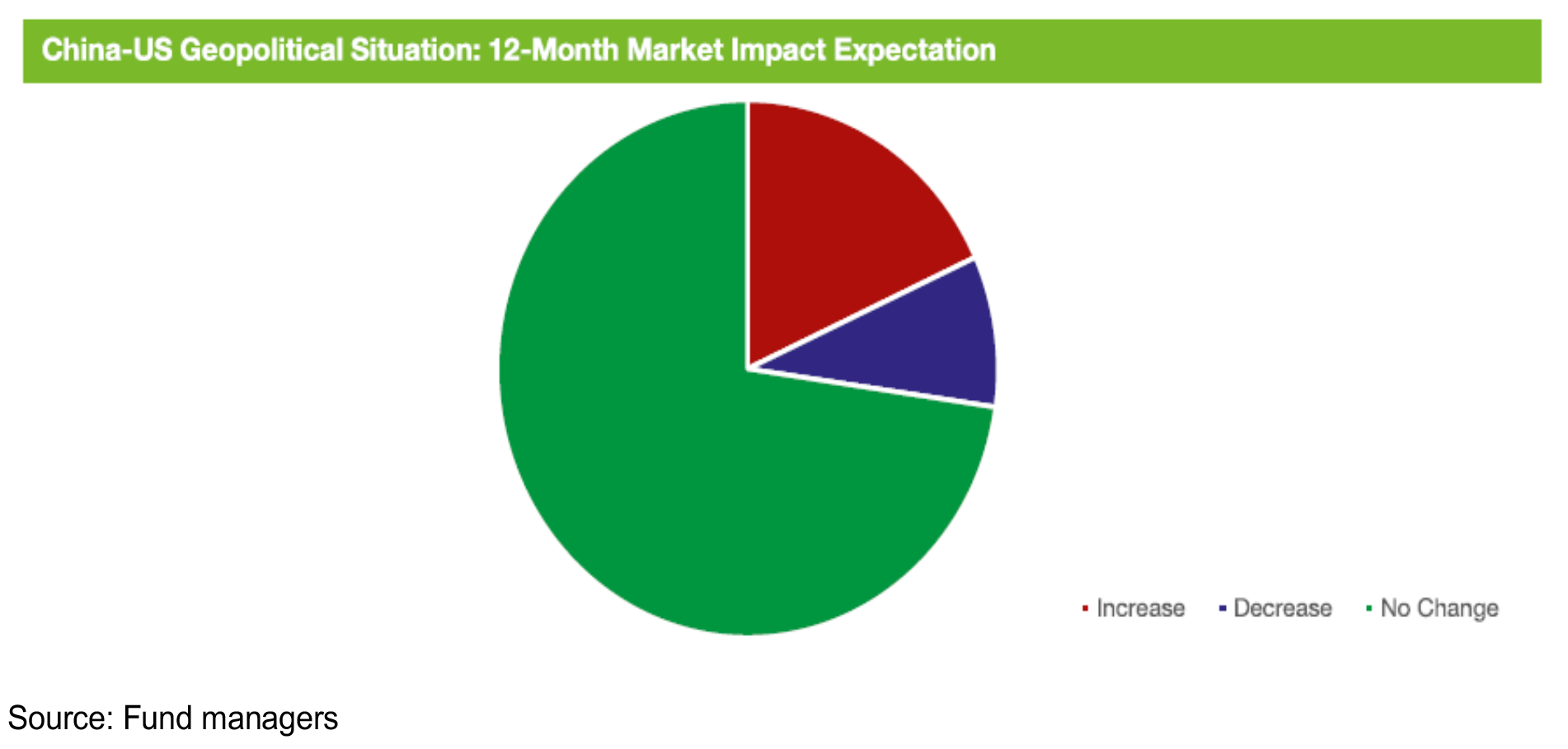

Given the importance of China on global markets and, in particular, emerging markets, we surveyed our rated managers about two topical Chinese geopolitical situations: the China-US situation and the China-Taiwan situation.

The results were not as stark as the Russia-Ukraine survey, with most managers believing the market impact of the China-US geopolitical situation will remain unchanged. Of the managers that believe the market impact will change, the majority believe it will increase.

The number of managers that believe the market impact of the China-Taiwan geopolitical situation will remain unchanged or decrease was split, while a small minority of managers believe it will increase over the next 12 months.

Importantly, for both Chinese-related surveys, most managers believe that the market impact of each of the geopolitical situations will either remain unchanged or decrease, which is contrary to the headline grabbing rhetoric that China is uninvestible.

We’ve seen this movie before…

China is no stranger to equity market volatility, with a major drawdown typically occurring every few years.

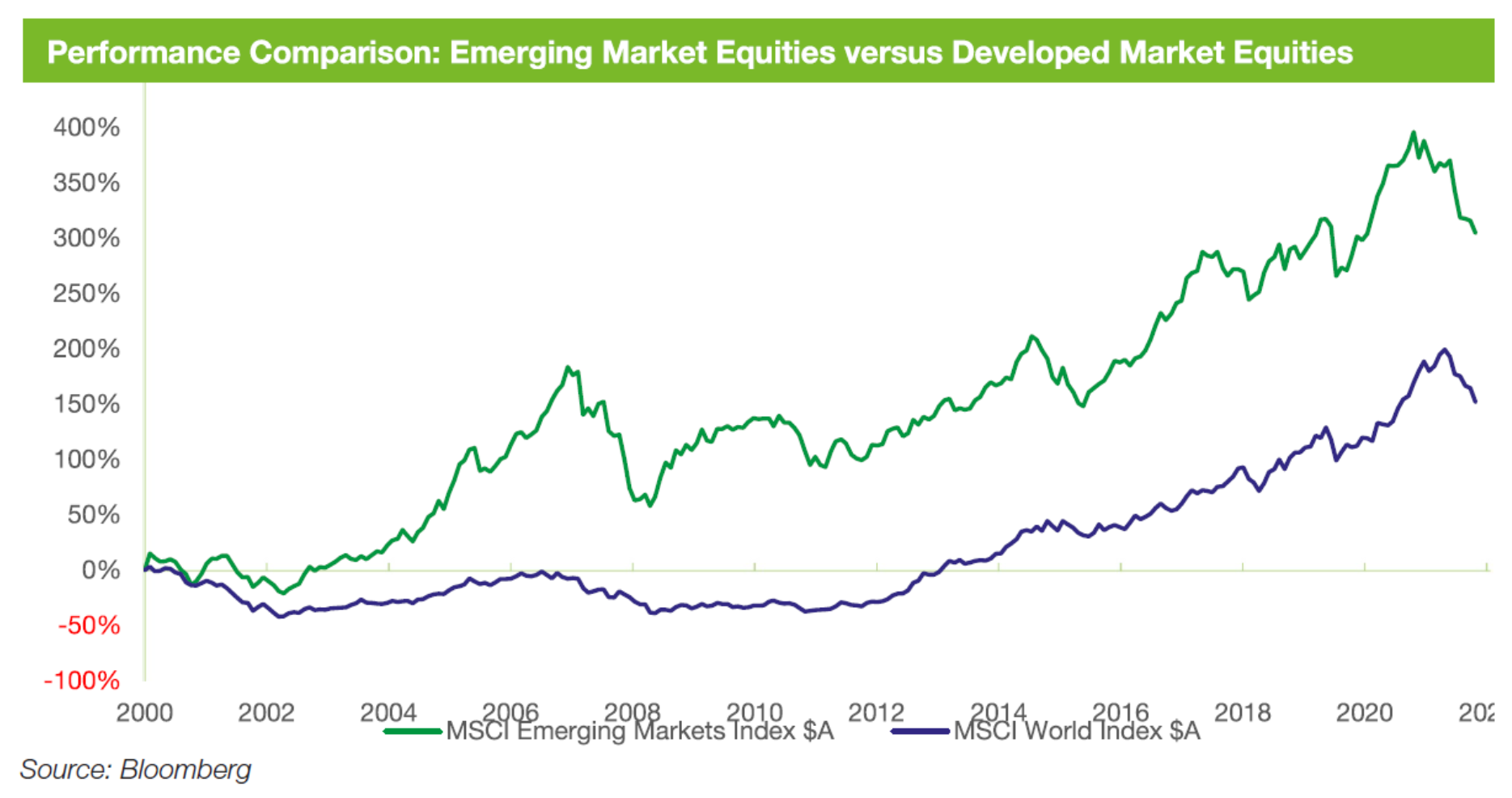

Although Chinese equities (as measured by the MSCI China Index $A) have experienced material drawdowns, they’ve historically recovered. Furthermore, when compared against developed market equities (as measured by the MSCI World Index $A), Chinese equities have materially outperformed over the long term.

Prior to the most recent drawdown, which has been severe, Chinese equities had appreciated 509% since the inception of the MSCI Emerging Markets Index $A(1) in January 2001. From this date to 30 June 2022, which includes the most recent drawdown, Chinese equities have still appreciated 339% and materially outperformed developed market equities, which appreciated 152% over the same timeframe.

- Selected start date chosen to coincide with all three indices analysed in the piece having concurrent data.

Is China uninvestible?

China has become particularly topical over the past couple of years, with many market participants becoming fearful that the Chinese Communist Party (CCP) can make sweeping regulatory changes at the drop of a hat that can send shockwaves through its equity markets.

In July 2021, for example, the CCP made changes to the Chinese education sector that sent the after-school tutoring names into turmoil. In addition, more recently, China’s deflating property market has investors concerned about the broader Chinese economy.

However, actions speak louder than words, so we analysed our rated managers’ holdings over the five years to 30 June 2022 to demonstrate whether they believe China is investible. The below charts illustrate the median active Chinese exposure of our rated managers with the performance of Chinese equities (as measured by the MSCI China Index $A).

As we can see, rated managers have maintained their relative underweight to China over the period assessed. However, the average manager decreased their active exposure prior to the drawdown in Chinese equities, before increasing their active exposure prior to the market rebounding. Although our rated managers remain somewhat conservative on China, given the underweight, it’s clear that attractive investment opportunities are arising within the country.

Is an exposure to emerging markets worth the stress?

Given the apparent inefficiencies, we believe an exposure to emerging markets is highly beneficial. The following chart displays the performance of emerging market equities (as measured by the MSCI Emerging Markets Index $A) against developed market equities (as measured by the MSCI World Index $A) since the inception of the MSCI Emerging Markets Index $A (in January 2001) to 30 June 2022.

Since January 2001, the MSCI Emerging Markets Index $A has outperformed the MSCI World Index $A by approximately 2.3% p.a. On a risk-adjusted basis, emerging market equities have outperformed their developed market counterparts, with each achieving a return/risk ratio of 0.47 and 0.38, respectively.

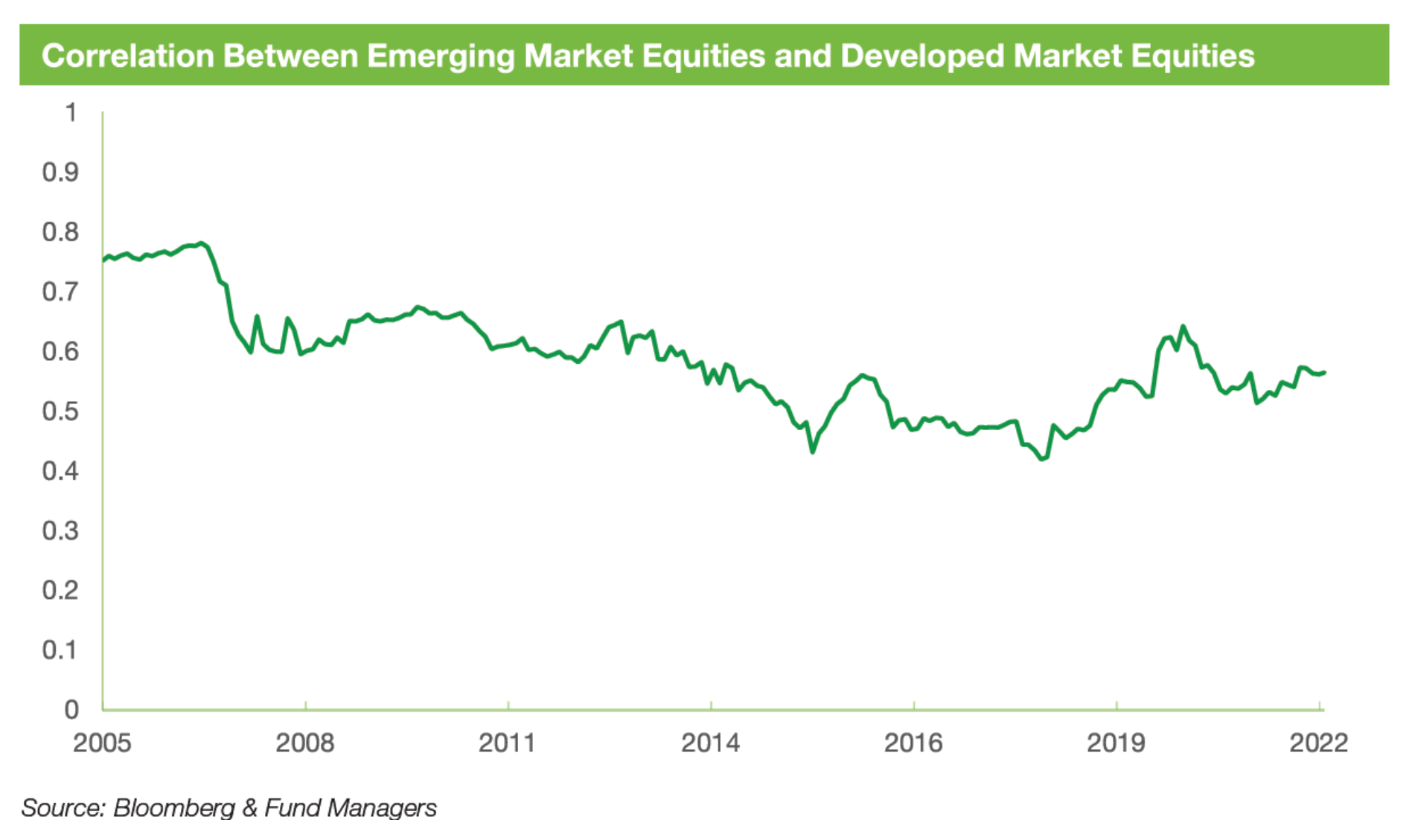

From a diversification standpoint, it’s clear that emerging market exposures complement developed market exposures. The five-year rolling correlation between emerging market equities and developed market equities is shown below.

As we can see, the correlation between the two indices over the long term has been significantly less than one, which leads to diversification benefits when blended in a portfolio. In addition, the benefit of an emerging markets exposure has increased over time, given the negative trend of the correlation over time. Of course, this pertains to index-tracking funds, with no consideration for active management.

A specialist in emerging markets: the key to unlocking superior investment outcomes

Given the specialised nature of emerging markets, we believe a dedicated manager is best placed to capitalise on the apparent inefficiencies.

There is a vast opportunity set available to global investors. The MSCI World Index has 1,513 constituents listed across 23 developed market countries, while the MSCI Emerging Markets Index has 1,387 constituents listed across 24 emerging market countries.

While effective screening tools can reduce the universe to better focus research, we believe a manager that understands the intricacies of emerging market countries and their equity markets is essential.

By Tom Goodrich, Senior Investment Analyst