Investment markets and key developments

Global share markets were mixed over the last week with US shares initially down but then boosted by strong tech sector earnings to be up slightly and Japanese shares rose but Eurozone and Chinese shares fell. Australian shares fell about 0.4% with falls in resources stocks and utilities offsetting gains in telcos, property and IT shares. Bond yields were mostly flat to down, and oil, metal and iron ore prices fell. The $A fell despite a slight fall in the $US.

Shares are at risk of another rough patch. Shares have had a good start to the year – with global shares up 7.7% and Australian shares up 3.7% – and falling inflation is a big positive, but the going may get a bit rough over the next few months. Bank stress is continuing to impact in the US with concerns about First Republic escalating again suggesting the issue may still not be contained, the US debt ceiling issue is starting to hot up, recession risks remain and the period from May to September is often rougher for shares. Australian shares are likely to be caught up in this as the recovery in China is so far less commodity intensive than thought earlier this year which partly explains the local markets relative underperformance so far this year.

Investor concerns about the need to raise the US debt ceiling are likely to escalate. The process will likely be drawn out.

- The passage of a bill in the Republican controlled House by 217 votes to 215 to raise the debt ceiling and cut spending is a positive first step. The bill won’t pass the Senate but shows that House Republicans can get behind legislation on the issue which then sets the scene for House Majority Leader McCarthy to eventually negotiate with President Biden.

- Treasury will also soon provide an update on the so-called X date by which the debt ceiling will have to be increased or else US Government spending will have to be slashed by the around 7% of GDP (ie the size of the US budget deficit). Its likely to be around July but Treasury could err on the side of caution and say it’s in June as the US budget deficit is worsening again.

- Democrats don’t want to cut spending at all as it will add to recession risk ahead of next year’s presidential election but Republican’s want to try and slow the economy down. Ultimately a resolution is likely with a compromise. If not Republican’s will get the blame for allowing the US Government to default on some of its spending commitments which won’t look so good ahead of next year’s election. The 2011 and 2013 episodes showed American’s mostly blamed the Republican’s for the disruption at the time.

- But any resolution is likely to come at the last minute, so markets will likely get more focussed and concerned about it in the months ahead.

- Markets will also worry that spending cuts in the final agreement will weigh on the economy adding to recession risks. Once the debt ceiling is raised markets will also lose the liquidity boost that the US Treasury has been providing since January as it ran down its cash reserves.

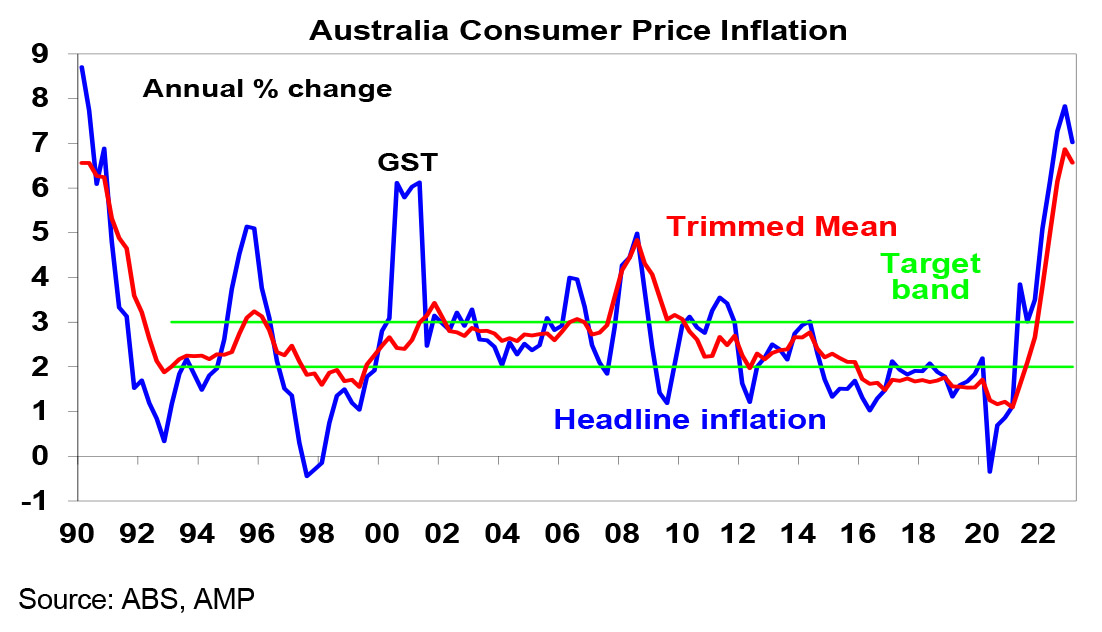

Falling Australian inflation should enable the RBA to remain on hold in the week ahead, but it’s a close call. Following significant falls in inflation in the US, Canada and New Zealand, Australian inflation is now also falling, adding to confidence we have seen the peak. CPI inflation fell back to 7%yoy and trimmed mean inflation fell to 6.6%yoy with both below RBA forecasts. While another RBA hike on Tuesday can’t be ruled out given RBA concerns about wages growth and faster population growth adding to housing related inflation and rising wealth, on balance we expect the RBA to leave rates on hold for May with the faster than expected fall in inflation providing it with greater scope to continue the pause in order to better assess the impact of past rate hikes. Either way, from later this year or early next we anticipate rate cuts to deal with a slowing economy. (See below for more details.)

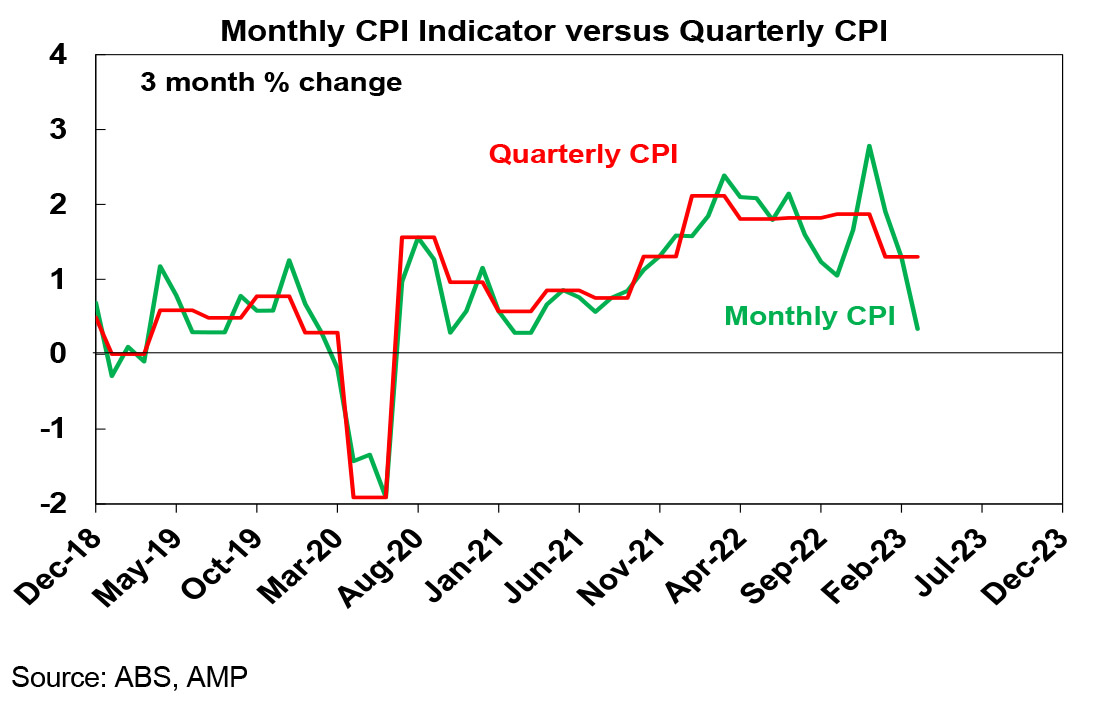

The monthly CPI Indicator continued to fall to 6.3%yoy in March from a high of 8.4% in December. In fact, over the last three months it rose by just 0.3%, its slowest since early 2021

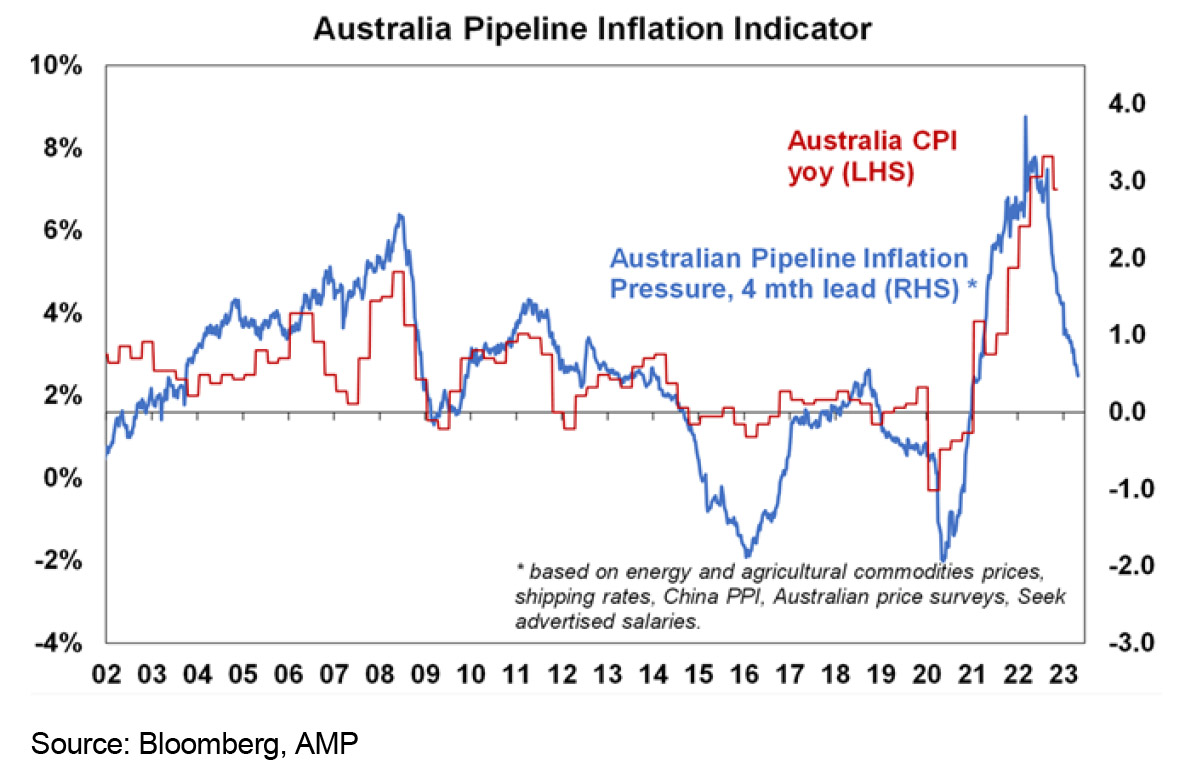

Expect a further fall in Australian inflation ahead. Australia lagged US inflation by about six months on the way up so it’s no surprise that its lagging on the way down. While services price inflation is still rising this is similar to the US experience. Just as good price inflation led on the way up its leading on the way down, with services price inflation likely to follow with a lag, albeit an acceleration in wages growth and rents associated with stronger than expected population growth along with a further spike in electricity costs are an upside risk. Our Australian Pipeline Inflation Indicator continues to point to a further fall in inflation ahead.

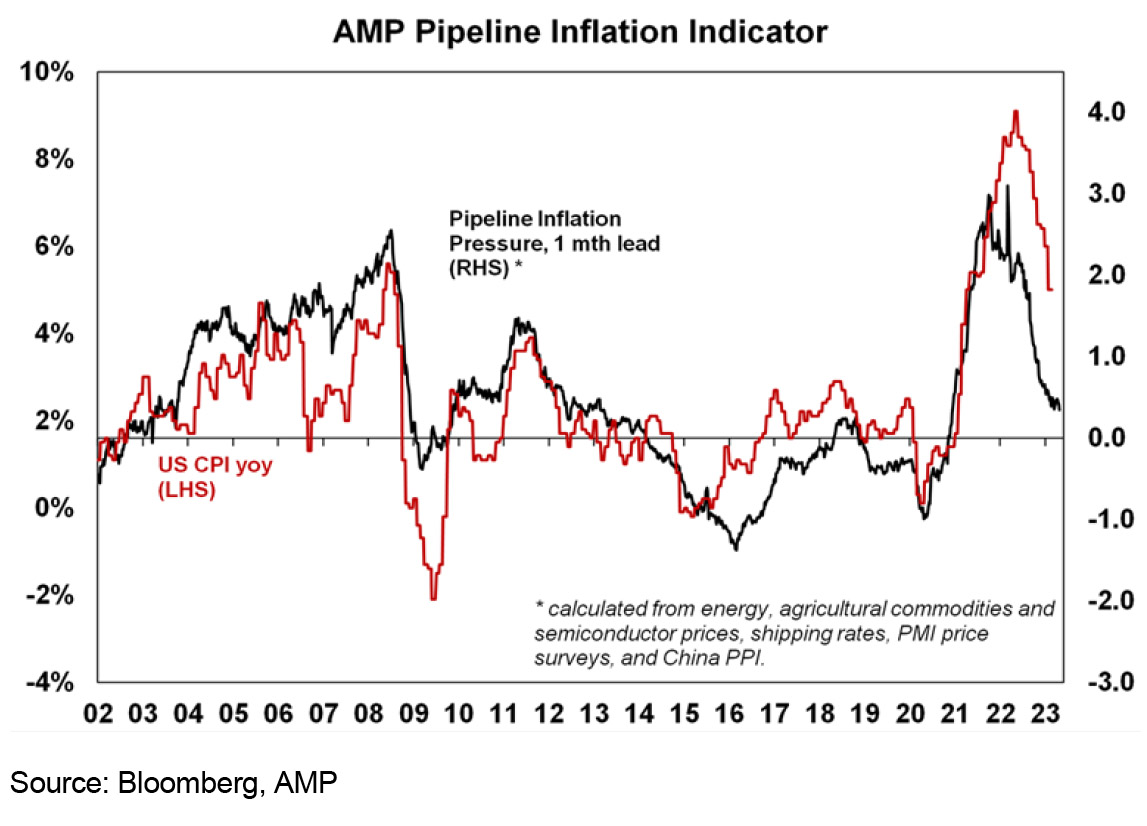

Our US Pipeline Inflation Indicator also continues to point to lower US inflation ahead.

The 2023-24 Australian Budget (9 May) is likely to be mainly about measures to fund the ramp up in structural spending pressures (on defence, NDIS, health and aged care). Key features are likely to be:

- minimal cost of living measures for low to middle income workers (with energy and medicine bill relief) and maybe a bit of an increase in Jobseeker;

- a ramp up in defence spending on missiles and submarines;

- measures to reduce the structural budget deficit (which is around $50bn or 2% of GDP) with a combination of tax increases (which could include an overhaul of the Petroleum Resource Rent Tax, a further cut to tax concessions and maybe a wind back of the Stage 3 tax cuts) with possible spending savings (like limiting growth in the NDIS, increasing deeming rates to limit pension payments & reducing middle class welfare);

- some measures to help boost housing affordability – including tax changes to encourage build to rent;

- lower budget deficits thanks to higher commodity prices and stronger personal tax collections in the short term and budget savings longer term with a 2022-23 deficit around $13bn, a 2023-24 deficit of $25bn and a $2024-25 deficit of $40bn; &

- the 2023-24 GDP growth forecast may be revised down to around 1% from 1.5%.

Coronavirus update

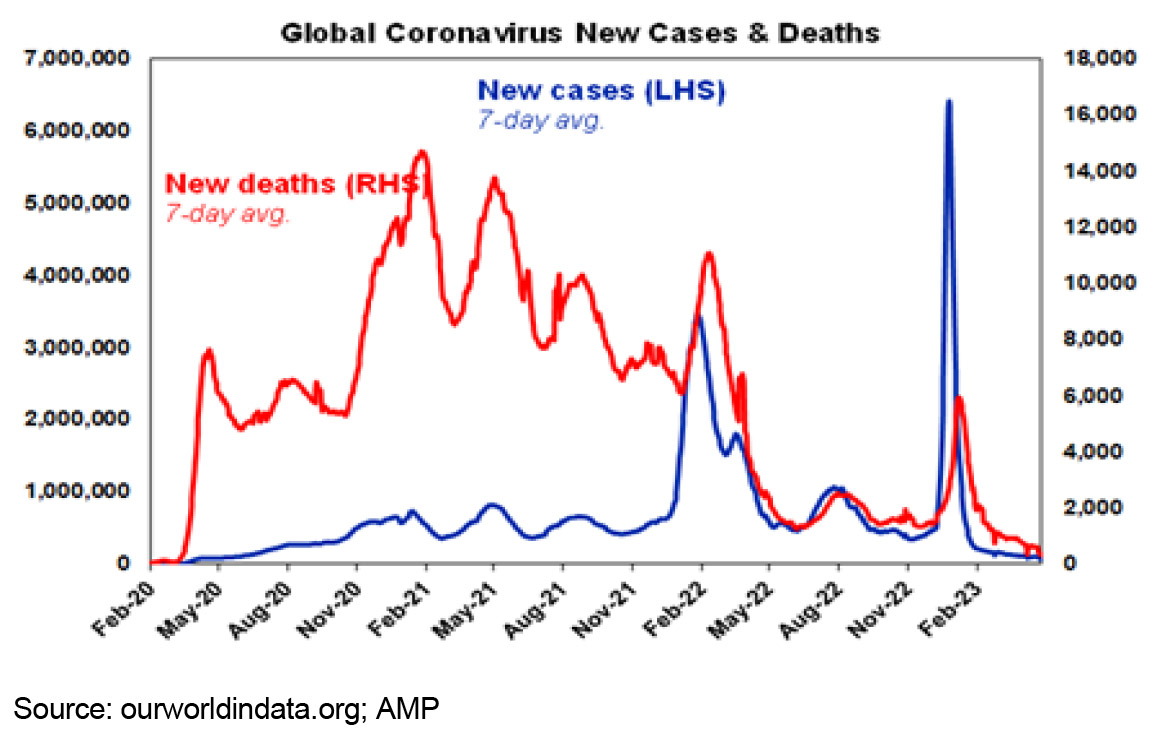

For those still interested…new global Covid cases and deaths continue to trend down. With less reporting the latter is far more reliable than the former. While there is a new variant called Arcturus it’s another Omicron subvariant that looks no more severe but spreads more easily.

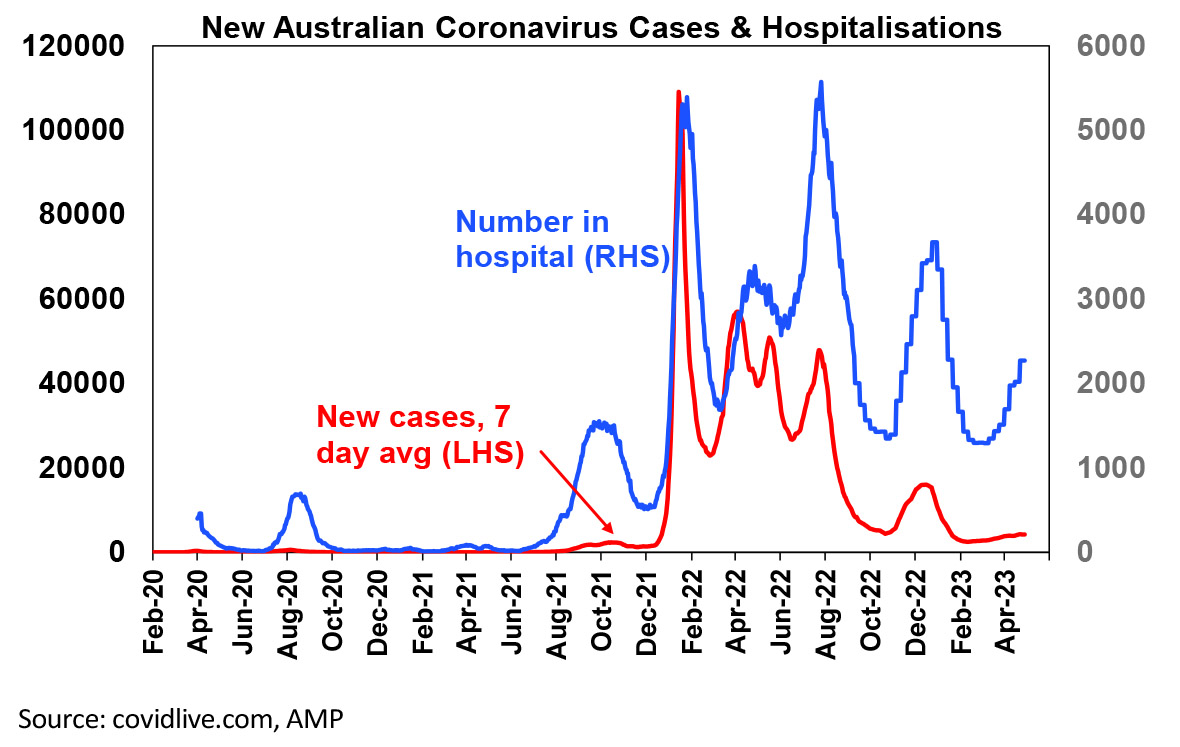

New cases (less reliable with less reporting), hospitalisations and deaths in Australia are up from their February/March lows – but levels are still low.

Economic activity trackers

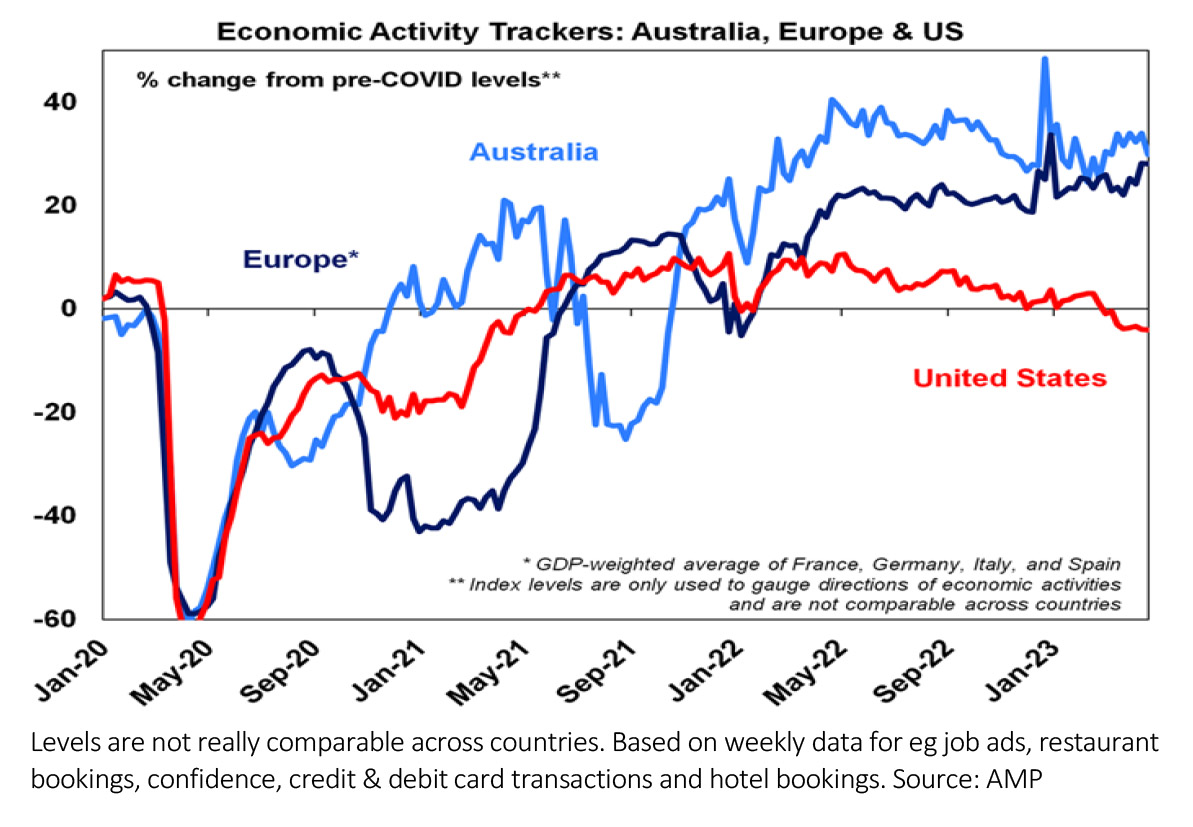

Our Economic Activity Trackers fell in the US and Australia over the last week but were little changed in Europe. Only the US is showing decisive weakness.

Major global economic events and implications

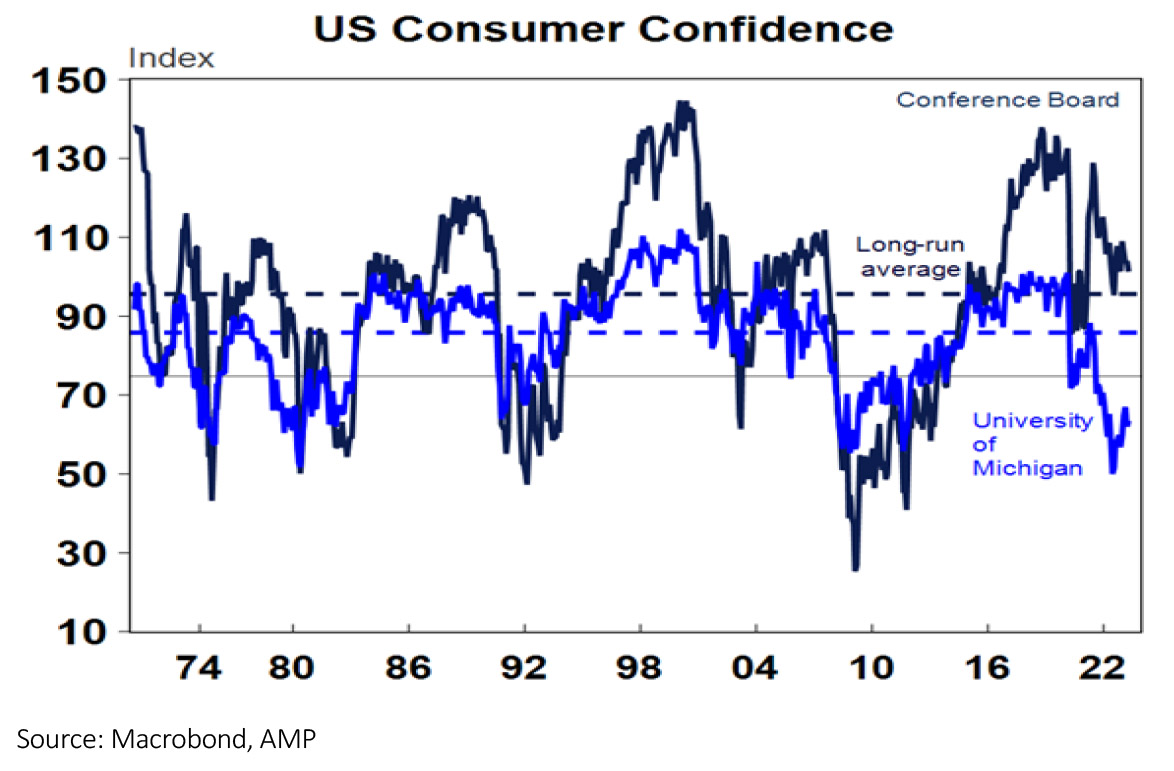

US economic data was mixed over the last week. Consumer confidence fell and underlying capital goods orders and shipments slid further auguring poorly for business investment. But March quarter GDP growth while weaker than expected at 1.1% annualised due to a 2.3 percentage point detraction from inventories indicated that the economy continues to grow with strong growth in private final demand, new home sales rose and home prices rose. Jobless claims fell but remain up from their low.

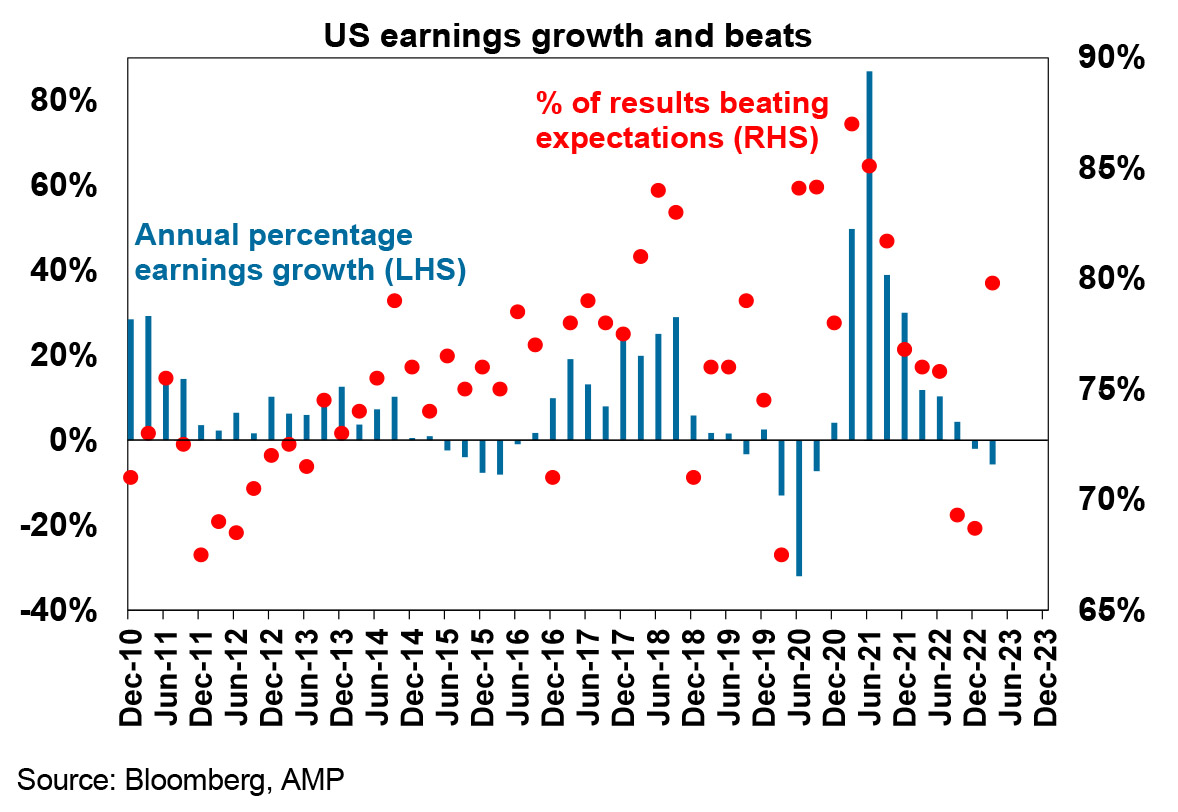

Mostly better than expected US earnings. 52% of S&P 500 companies have reported so far with 80% surprising on the upside which is far better than in the December quarter and above the long-term norm. The average beat is running at 6%. Consensus earnings expectations growth expectations for the quarter have risen from -6.2%yoy to -5.7%yoy. Non-US earnings growth is running around 6.4%yoy.

Eurozone economic confidence was little changed in April and doesn’t seem to be seeing quite the same strength evident in PMIs.

The Bank of Japan left its ultra easy monetary policy unchanged but scraped its dovish forward guidance on rates and announced a review of its policies – suggesting its getting closer to starting to wind back its stimulus (but it might be a slow process). Japanese economic data releases were mixed with stronger gains in retail sales and industrial production than expected but unemployment surprisingly rose to 2.8% and the jobs to applicants ratio fell. Inflation in Tokyo rose in April to 3.5% with core inflation rising to 2.3%yoy.

Australian economic events and implications

Apart from the fall in CPI inflation for the March quarter, producer price inflation slowed further to 5.2%yoy (down from a high six months ago of 6.4%yoy) and import prices fell 4.2% in the March quarter helped by falling global producer price inflation, lower petroleum prices and a stronger $A. All of which helps take pressure of consumer price inflation.

With export prices up by 1.6%qoq though, the terms of trade likely rose in the March quarter and remains very strong pointing to strength in nominal GDP growth and ongoing stronger than expected mining sector tax revenue flowing to Canberra and reducing the budget deficit.

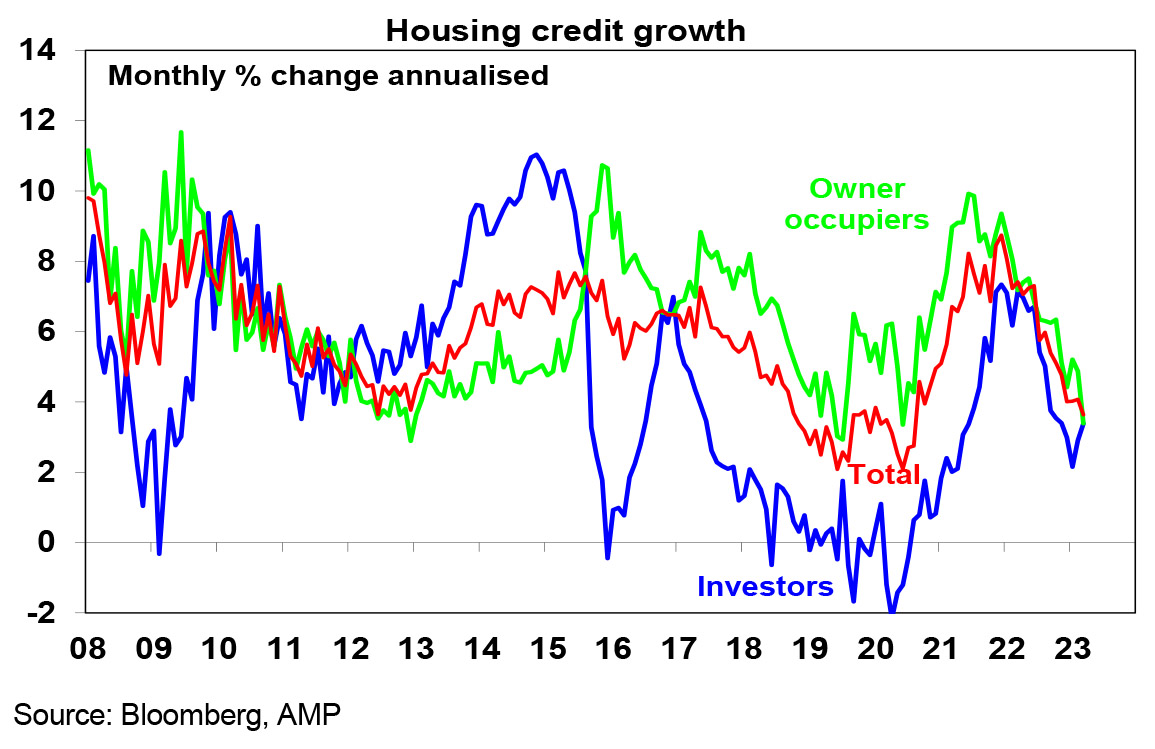

Private sector credit growth showed a further slowing in credit growth to housing and business. But while housing credit growth to owner occupiers continues to slow it has picked up to investors.

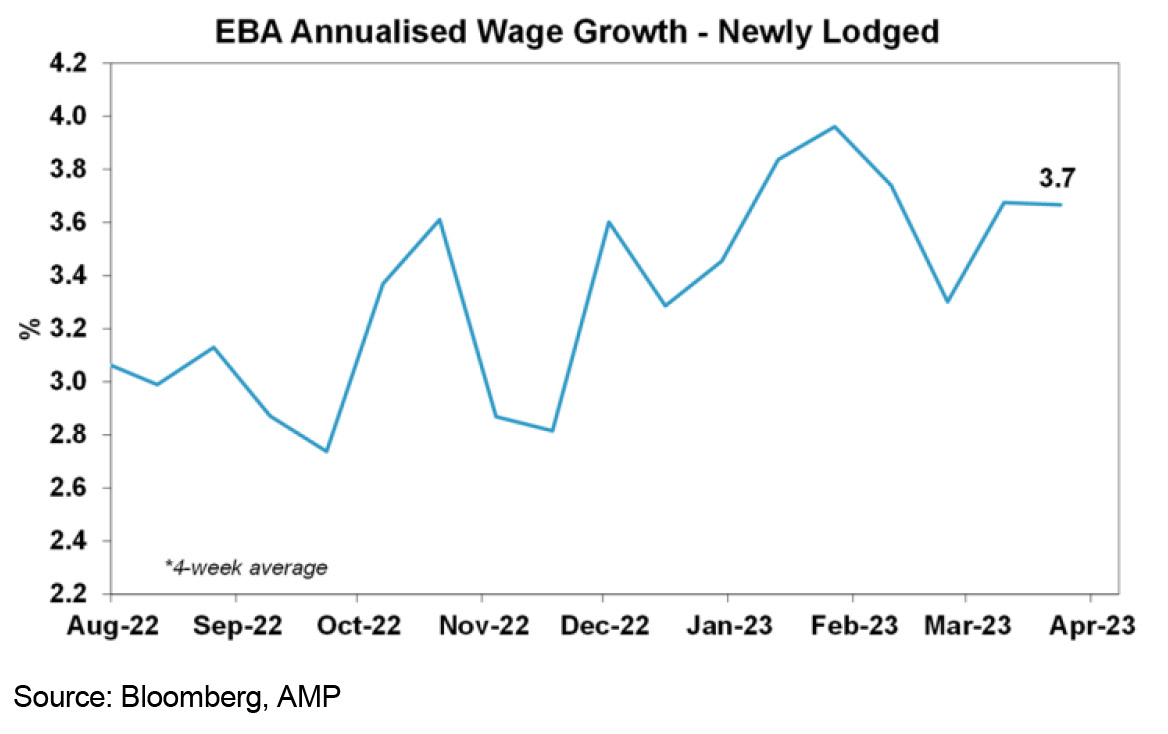

While the still tight labour market and the flow on to stronger wages growth pose an upside risk to the inflation outlook, newly lodged enterprise bargaining agreements are averaging at a moderate at 3.7% in annual wage gains and down slightly from early this year.

What to watch over the next week?

The focus in the week ahead is likely to be on interest rates with the RBA, Fed and ECB all meeting.

In the US the Fed (Wednesday) is expected to raise the Fed Funds rate by another 0.25% to a range of 5-5.25% consistent with comments from various Fed officials that it still has more work to do with inflation still high and the labour market still tight. However, this is likely to be the peak in the Fed Funds rate with the banking stresses doing some of the Fed’s work for it and inflation likely to fall further. It’s a close call though as renewed banking stress in the US could see the Fed decide to leave rates on hold in in the week ahead with the US money market pricing a 72% probability of a hike and continuing to expect rate cuts by year end.

On the data front expect a further improvement in the ISM manufacturing conditions index (Monday), a further fall in job openings (Tuesday), little change in the ISM services index (Wednesday) and a further slowing in payroll growth to 175,000 for April with unemployment rising to 3.6% and wages growth unchanged at 4.2%. US March quarter earnings reports will also continue to flow.

The ECB (Thursday) is expected to raise rates by another 0.25% taking its main refinancing rate to 3.75%, while maintaining a mild data dependent tightening bias. Eurozone inflation data (Tuesday) for April is expected to rise slightly to 7.1%yoy with core inflation unchanged at 5.7%yoy. Unemployment for March (Wednesday) is likely to be unchanged at 6.6%.

Chinese business conditions PMIs for April will start to be released from Sunday and are expected to show a slight easing driven by services after the initial reopening boost but to remain strong overall.

In Australia, we expect the RBA (Tuesday) to leave interest rates on hold for the second month in a row at 3.6%, but maintain its mild hawkish guidance. The fall in March quarter inflation taking it below RBA forecasts at both a headline and trimmed mean level and the steady decline in monthly inflation through the quarter has bought it more time to assess the impact of prior hikes, particularly given that not enough new information has become available since the April meeting. However, it’s a close call and the risk of more rate hikes remains high with inflation still too high and the RBA particularly concerned about the impact of stronger than expected population growth on housing related inflation with rising home prices now starting to reverse the negative wealth effect and upside risks to wages growth. As a result, the RBA is likely to maintain guidance that further tightening “may well be needed” and that “in assessing when and how much further interest rates need to increase” the RBA will look at the global economy, household spending, inflation and the labour market. The money market is now pricing in no rate hike in May and only 40% chance of a 0.25% hike by August.

The RBA’s latest Statement on Monetary Policy (Friday) is unlikely to make any major changes to its forecasts and still show inflation not returning to the top of the target range until mid-2025 but it may revise down slightly its 2023 growth and inflation forecasts but only by 0.25% or so.

On the data front in Australia, expect CoreLogic data for April (Monday) to show a 0.7% rise in average home prices led by a 1.3% gain in Sydney adding to the likelihood that we have already seen the low in property prices as a severe supply shortfall offsets the impact of higher interest rates. The MI Inflation Gauge (Monday) will provide an update on inflation for April, retail sales growth (Wednesday) for March is likely to have remained soft at +0.2%mom, the March trade surplus (Thursday) is likely to have remained high at $12.5bn and housing finance for March (Friday) is likely to be flat to up slightly.

Outlook for investment markets

The next 6-12 months are likely to see easing inflation pressures, central banks moving to get off the brakes and economic growth weakening but stronger than feared. This along with improved valuations should make for better returns this year than in 2022. But there will still be bumps on the way – particularly regarding interest rates, recession risks, geopolitical risks and raising the US debt ceiling.

Global shares are expected to see reasonable returns this year. The post mid-term election year normally results in above average gains in US shares, but US shares are likely to be a relative underperformer compared to non-US shares reflecting still higher price to earnings multiples versus non-US shares. The $US is also likely to weaken further which should benefit emerging and Asian shares.

Australian shares are likely to boosted by stronger economic growth than in other developed countries and stronger growth in China supporting commodity prices and as investors continue to like the grossed-up dividend yield of around 5.5%.

Bonds are likely to provide returns a bit above running yields, as inflation slows and central banks become less hawkish.

Unlisted commercial property and infrastructure are expected to see slower returns, reflecting the lagged impact of weaker share markets and last year’s rise in bond yields (on valuations). Commercial property returns are actually likely to be negative.

While the risks remain high of a further fall in Australian home prices out to later this year as interest rate hikes and slower economic growth impact, the faster than expected return of immigration, very low rental vacancy rates and constrained supply now mean that we have likely already seen the low in prices with a top to bottom fall of 9% to February, as opposed to our forecast for a 15-20% fall out to later this year. As such we have revised our national average home price forecast for this year from a fall of -7% to around flat.

Cash and bank deposits are expected to provide returns of around 3.5%, reflecting the back up in interest rates.

A rising trend in the $A is likely over the next 12 months, reflecting a downtrend in the overvalued $US, the Fed moving to cut rates and solid commodity prices helped by stronger Chinese growth.

By Shane Oliver