With elections comes the rise of the populist rhetoric.

Geopolitical risks have spiked and are set to only become more important and unpredictable in 2024, with the highest geopolitical risk in decades compounding economic uncertainty. This is due to election cycles, trade tensions and armed conflicts.

Elections

There is a busy election calendar in 2024, with 40 nations scheduled to go to the polls, including four of the five most populous countries, covering 40 per cent of the world’s population and GDP. Elections bring instability to both domestic developments at the policy level, as well as global consequences. Key dates to watch include:

- February sees presidential elections in Indonesia after a successful decade under Joko Widodo. It’s set to be a three-pronged race, with a potential run off in June and a new government in October.

- March 17 sees Russia go to the polls, with little surprise expected, while Ukraine’s planned March 31 presidential vote is likely to be postponed due to martial law.

- April/May sees India go to the polls, with Modi trying to secure a third term – he is ahead in the polls at this stage.

- June sees European parliament elections and a Mexican presidential vote, which could impact trade and border security with the US.

- In the US, government debt sustainability and fiscal path are set to be key in the November election. Despite this environment, large deficits limit the prospects of fiscal giveaways. A 6 per cent US deficit level would suggest that whoever ends up running for president in 2024 will not be doing so on the promise of major tax cuts. Foreign policy predictability, immigration, infrastructure, the economy and continued aid to Ukraine are also important election topics.

- Sometime in Q4 (unless snap elections are called) the UK goes to the polls. The opposition Labour party is well ahead in the opinion polls and appears set for victory. Higher taxes may be on the cards, with the high levels of public debt. There is a risk that consumers and businesses take a ‘wait and see’ approach to spending and investing ahead of the election.

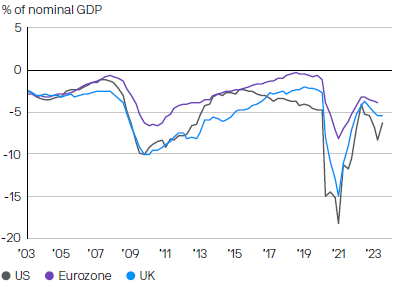

Public sector fiscal deficits

Source: Bloomberg, Eurostat, ONS, US Treasury, JPAM. As at 15 Nov 2023

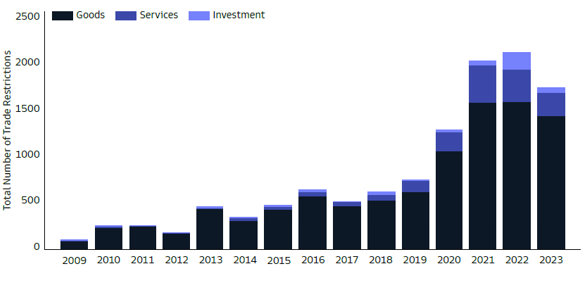

Trade restrictions

Rising geopolitical tensions could trigger further restrictions across the globe, with ‘re-shoring’ critical supply chains and economic security becoming even more front and centre of political powers. These include critical mineral inputs into the supply chains of the green energy transition.

Trade restrictions have tripled since 2017

Source: IMF, Goldman Sachs as at August 23

Conflict

The ongoing Israel-Hamas and Russia-Ukraine wars, and China-Taiwan conflict, could all impact markets in 2024. These continue to have potential impacts on agricultural and energy markets.

- Ukraine is likely to step down as winter progresses and with lower funding from the West, but a negotiated settlement (the only way for a meaningful end to the conflict) seems highly unlikely.

- The Israel conflict is set to become a bigger issue if it is not contained to Hamas (Gaza) and Hezbollah on the southern Lebanese border. That is, if Iran has any direct role, it would impact oil prices much more, both directly and via trade through the Strait of Hormuz (20% of global supplies pass through).

- The China-Taiwan conflict continues to evolve and be front of mind early in the year. The Democratic Progressive Party (DPP) won a historic third successive term in January, but with a minority 40 per cent of parliament (from majority) meaning it will have to negotiate with opposition parties on all legislation and budgets. It remains to be seen if the new relationship between incoming President Lai and Beijing will involve a hardening or softening of approach from either party.

Populism

With elections comes the rise of the populist rhetoric. Populism poses a real threat to democracies for a number of economic, social and governance reasons. From an economic perspective, the key issue is that populism leads to the development and attempted implementation of poor economic policy. This policy gets them elected, but in turn, becomes very hard to implement due to social and economic consequences.

What does this mean for infrastructure?

We remain conscious of the volatile economic environment as well as the 2024 political overhangs, and we’re positioning accordingly. However, macro uncertainty and geopolitical tensions can also create unjustified market volatility and noise. We look to separate the resilience of the infrastructure asset class from this noise, and we remain optimistic about the long-term fundamentals underpinning the infrastructure investment case.

Moving into 2024, we will be monitoring the regional economics and politics closely, and positioning ourselves to best capture these at an in-country level.

Politics is an overhang and noise can be disruptive. We favour those regions that have less exposure to this dynamic, albeit will use any market volatility around the elections as a buying opportunity should it present itself.

2024 is set to be a pivotal year for the global economy, as we move past peak rates, growth moderates, and inflation continues its downward path to central bank target bands. There is still a potential window open for a recession considering the “long and variable lags” of monetary policy transmission.

For now, however, the market is pricing in a goldilocks scenario where inflation settles and growth doesn’t suffer a hard landing. This last mile of disinflation could be harder to achieve than the market is hoping for, meaning that rate cuts start in the second half of the year. Either way, lower rates are a tailwind for long duration infrastructure assets which we forecast to continue to have strong earnings growth driven by multi-decade thematics.