Craig Swanger

The below is our view of the largest risks facing Aussie investors in 2024. Some of these, such as the rising risk of a property correction in China, were raised during the past year but are now being expanded upon and some are new.

The 5 biggest risks facing Australian investors:

- Top Risk: China slows faster than expected and exports deflation

- Risk number 2: Populist politics and its impact on global trade

- Risk number 3: Market risk and models: Specifically equity market volatility

- Risk number 4: The economic disruption of technology and AI

- Risk number 5: The impact on market volatility of Sustainable Investments.

Top risk: China exports deflation

China has been the growth engine of the world’s economy for nearly thirty years, but now is the source of its largest economic uncertainty.

The growth in China has been significantly fuelled by urbanisation, ie the 320 million people moving to China’s cities, and the related ability of China’s central government to invest in infrastructure and property development to stimulate economic growth in tougher global conditions such as the post-GFC period last decade.

Now the benefits of that investment-fuelled growth have reached their limit. This limit is due to both the urbanisation trend itself, but more specifically that China’s total debt burden has become too high. We touch on this more below.

At the same time, China’s consumer prices are falling too quickly, the property development crisis is worsening and exports are slumping, so stimulus of some sort is required. China’s central government has little option but to try to boost exports.

If global conditions were very strong, this would be difficult but possible. The problem for China is they are attempting to improve exports at the same time that global consumers are spending less.

The implications for investors will be lower inflation and therefore lower interest rates globally. It also puts earnings pressure on the global companies that dominate equity markets’ growth.

Let’s look at the issues forcing China to boost exports as these are typically less understood and therefore less priced into global markets.

China is reaching its debt limits, reducing its options for stimulating growth

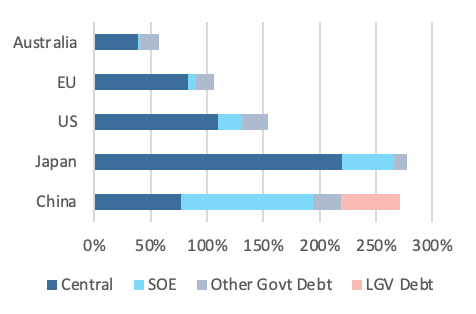

Borrowing by the central Chinese government is not the right measure to watch to understand China’s ability to borrow more to stimulate growth. The debt-to-GDP ratio for the total Chinese government is actually around the same as Japan’s (as shown below).

As a result, we tend to look at total government obligations as shown in Figure 1 below. That is, what debt will the central government be under significant pressure to support in the event of default? For the US, for example, this includes mortgage entities Fannie Mae and Freddie Mac and the US Post, but debt is still relatively centred on US federal debt (as shown in Figure 1).

For China, the total debt obligation needs to include local governments, local government finance vehicles (“LGFV”s) and state-owned enterprises (“SOE”s). It is worth noting that China’s SOEs comprise a massive 40% of China’s GDP, making China’s SOEs around six times larger in output than the whole of Australia’s economy.

As shown below, China’s total debt is approaching 300% of GDP and is largely driven by state-owned enterprises. That leaves Beijing policy makers with little room to move if they, like us, think that stimulus is needed, forcing them to lower centralised borrowing rates, but then they only have the option of combating the US and EU for trade competition.

China’s total debt is around the same as Japan’s

Total debt for China’s economy needs to be carefully compared to other economies. As shown in the left-hand chart, China’s total obligations are actually around the same as Japan’s and around twice that of the US and EU.

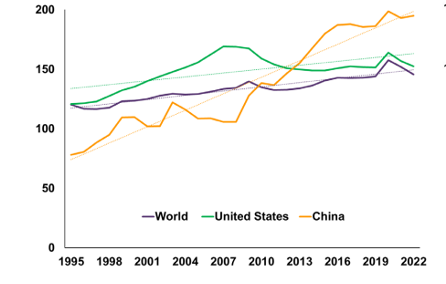

The right-hand chart shows that corporate debt in China, around 68% of which is from state-owned enterprises, surged past global averages since the last global economic crisis. As shown in the left-hand chart, SOEs are the primary source of China’s debt-to-GDP ratio today, so this surge has narrowed its options to stimulate its economy.

Together these charts show the bind that China is now in and the risk that this poses. In our opinion, this is a risk that investors are not being adequately compensated for at present.

Total Debt-to-GDP ratiosKey global economies and Australia, 2022/23

Corporate debt vs GDPChina vs the US and global benchmarks, 2022

The impact on global deflation

China’s property development fixes require control of domestic consumer confidence as they are major investors in Chinese property. Even for the centrally controlled government in China, consumer confidence of 1.4 billion people is very difficult to control.

So it is likely that Beijing’s policy leaders are smart enough not to rely upon turning around confidence in property and will turn to export growth policies, as export markets are the only other sector of the economy that has the scale to fill the gap left by property development.

Therein lies the problem for the world and for China: China’s factories selling to the world means that they will be exporting deflation.

This could take a while to hit the global headlines as deflation, not to mention weaker export earnings, tends to be bad for equities markets, but avid IAM readers will know we don’t tend to be shy about calling out underreporting investment market risks and opportunities.

This is particularly risky for Australia’s growth assets and their investors, but a strong opportunity for investments that will benefit from lower interest rates and increased global competition.

The so-what: Investment strategies to suit

Strategies include switching from high growth assets, particularly regional property and small-cap stocks, to higher quality assets.

The above also implies two likely themes will emerge:

- In the first response, markets will have their typical “flight to quality” reaction, reducing their exposure to high growth markets and increasing hedges and assets perceived to have lower risks. Australia is considered a high-growth (high-beta) country as a whole, so this would mean Australian assets increase in value relative to US assets. This includes the AUD itself. The investment strategies that come from this phase include finding better value in Australian assets, and just avoiding sectors overly exposed to the true source of the uncertainty: China’s growth (avoid iron ore, copper, and assets overly reliant on WA and Qld, the mining states).

- As the dust settles and markets start to focus on the real issues, non-China dependent growth markets will recover. For example, commodity markets such as coal, food and base metals (other than copper) will recover.

Despite the focus on China above, this is not an issue limited to the challenges that China faces. This is a global issue. Lower consumer spending in the US and EU will combine with the under-reported economic issues in China to create lower inflation, lower interest rates, and lower growth expectations globally.

With that said, in 2024 the largest risk for investors is how China will respond when it starts to fall short of its own economic growth targets. Because of past borrowings by parts of the centralised Chinese economy, they have little option but to depend upon export sectors to drive economic growth.

Doing this at the same time that the US and EU consumers will reduce spending is difficult. But this challenge will be made even harder by the impact of 2024’s extraordinary election cycle globally (#2 of the largest risks of 2024). Global trade is a common enemy raised during election cycles, and with nearly half the world’s population represented in elections in 2024, increasing global trade will be even harder.

Unrelated to these issues, two of the longer-term issues also require adjustments over 2024. These are the impact of the digital economic revolution, eg artificial intelligence; and the impact of sustainable investments, ironically positive for commodity prices too.

And final of the five largest themes for investors, market overpricing, is far more short-term. This risk requires immediate repositioning. Equity markets are still priced for perfection, which 2024 is highly unlikely to hold. Due largely to the issues above, “growth” volatility will rise, which will cause more volatility for equity markets in particular.

The overall theme for Australian investors in 2024 is to derisk. Derisking does not mean reducing total risk, but rather it means being smarter about where risks are taken. Risk must always be considered relative to return, so derisking does not mean loading up on cash, government bonds or bank stocks. It means making sure you are getting paid for the risks you take.

The global themes highlighted suggest that there will be higher market volatility, which might lead to some sectors being oversold. For instance, China’s risks are not bad for all commodities, and certainly not as bad for Australia as world markets will initially imply. However, the overselling of Australian assets, including the AUD itself, has occurred with every global market shakeup. Assuming this will happen again, which is a fair assumption, means opportunities to swap growth risk for smarter risk and maintain investment returns.

In short, 2024 is not the year to blindly follow the pack. Rather, it is the year to observe global themes unfold and be ready to take advantage of market mispricing.

By Craig Swanger, Chief investment officer