Dan Miles

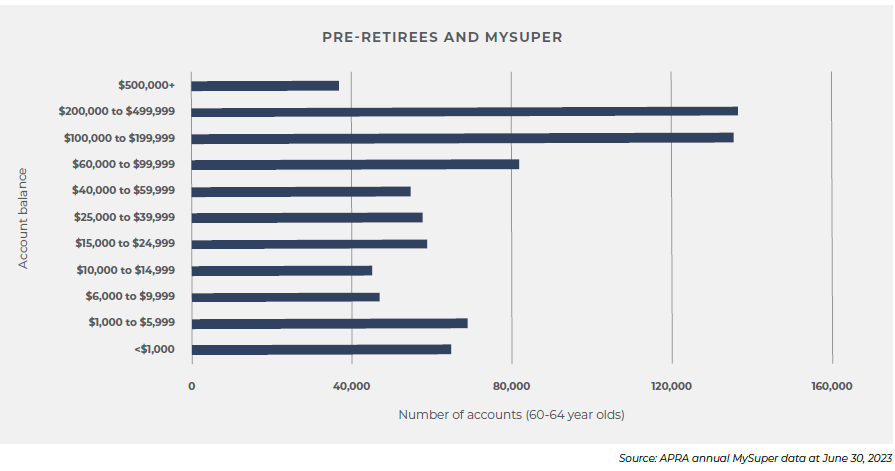

An analysis of APRA data reveals that about 60 per cent of MySuper accounts held by pre-retirees, or those aged 60 to 64 years, had low savings balances below $100,000 – or around 800,000 accounts – not nearly enough to fund a comfortable twenty or thirty years in retirement, even with the age pension, according to Dan Miles, Innova Managing Director and Co-Chief Investment Officer of Innova Asset Management.

Innova’s analysis of the APRA data reveals that 46.4 per cent of the near 1.7-million-member accounts held by 60- to 64-year-old Australians were invested in MySuper funds at June 30, 2023. But a closer breakdown of account balances reveals many had low balances, while 174,000 accounts had superannuation balances above $200,000.

“About 60 per cent of pre-retiree MySuper accounts had low balances of below $100,000, which means many people on such low balances will fall short of what they need to live comfortably in retirement,” Mr Miles said.

“With around 800,000 accounts having a balance of less than $100,000, many older Australians risk having to go without luxuries in what should be their most comfortable years, given the high cost of living and inadequate savings in MySuper funds. A 65-year-old Australian woman today can expect to live another 23.0 years and 65-year-old man another 20.3 years longer[1] Many pre-retirees need higher savings and stronger investment returns to help fund such a long time in retirement,” he said.

According to Mr Miles, the typical advice for a person this age is to lower portfolio risk as retirement approaches, which is something that lifecycle funds do automatically. However, lowering exposure to growth assets may not be good advice for many pre-retirees with low balances. Ironically, those with lower balances may be better served allocating more aggressively because of the security the age pension brings, and their need for better long-term results.

“They need strong returns to help fund decades in retirement, but are more exposed to sequencing risk, or the risk that a market downturn can significantly dent their retirement savings. Investors should seek personal advice on how they can best build their super to meet their needs. The advice doesn’t need to be all-encompassing financial advice. It can be limited to particular areas, such as retirement. This approach can more than pay for the cost of advice,” Mr Miles said.

Australia’ default MySuper funds are among the most aggressive pension investors in the world, allocating 60-70 per cent in growth assets such as equities. But even with such aggressive allocations, older investors with lower balances may be able to invest even more aggressively than default MySuper products with backup from the Age Pension if markets fall.

“However, these are complex calculations that require financial advice. Pre-retirees with substantial savings above $500,000 are more likely to need to protect those assets from the risk of a market downturn. It’s those on lower balances, which are many, as shown by the chart below, who are equally in need of advice.”

Recently released wealth data, ABS Household Wealth Data[2] reveals that household net wealth sat at a record $15.66 trillion in the December 2023 quarter, with wealth boosted by a record level of superannuation assets, which totalled $3.74 trillion, boosted by rising asset values and contributions into pension funds following legislative changes to compulsory superannuation and strength in the labour market.

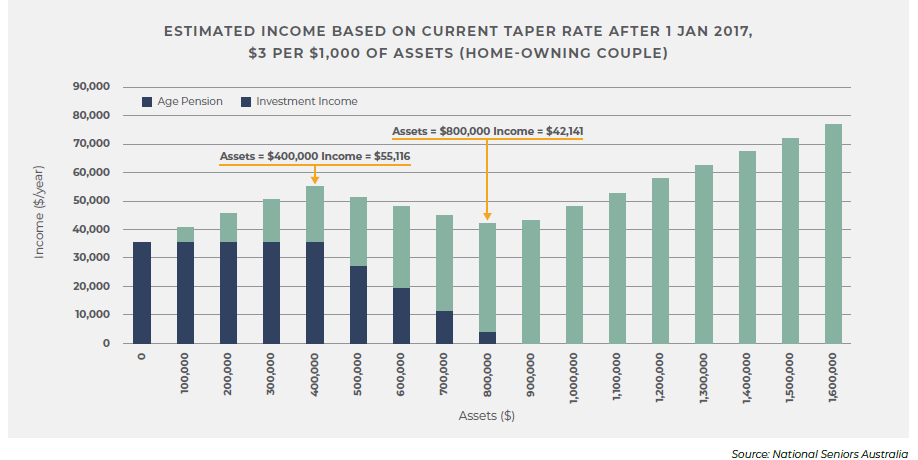

The chart below reveals the extent of the ‘taper trap’ – the region where higher balances actually lead to less income because of the aggressive drop in the age pension. As super savings grow, the value of the government Age Pension is cut by an even greater amount thanks to a quirk in Australia’s retirement system, as shown in the graph below.

————