Balaji Venkataraman

Investors face a new bond market landscape. The investment strategies that previously provided attractive performance potential may not be well suited for today’s market.

For example, since the Great Financial Crisis of 2007-2009, many fixed-income investors have favored funds from Morningstar’s® Core Plus category. These funds typically consist of a core base of Treasury, investment-grade corporate and mortgage-backed bonds supplemented with higher-risk/higher-return-potential securities. In the low interest rate environment following the crisis, these strategies gave investors the prospect of attractive returns and yields.

Higher rates and higher inflation highlight investors’ concerns

Today’s climate is clearly different. Interest rates are notably higher, and inflation remains above the Federal Reserve’s (Fed’s) target rate. Furthermore, Fed policy sits in a holding pattern, with the target short-term lending rate hovering at its highest level in 23 years.

Ultimately, we expect the extended era of high interest rates and inflation to weigh on the economy, triggering a period of below-trend growth. We believe this environment requires dynamic duration and risk management to meet investors’ fixed-income objectives.

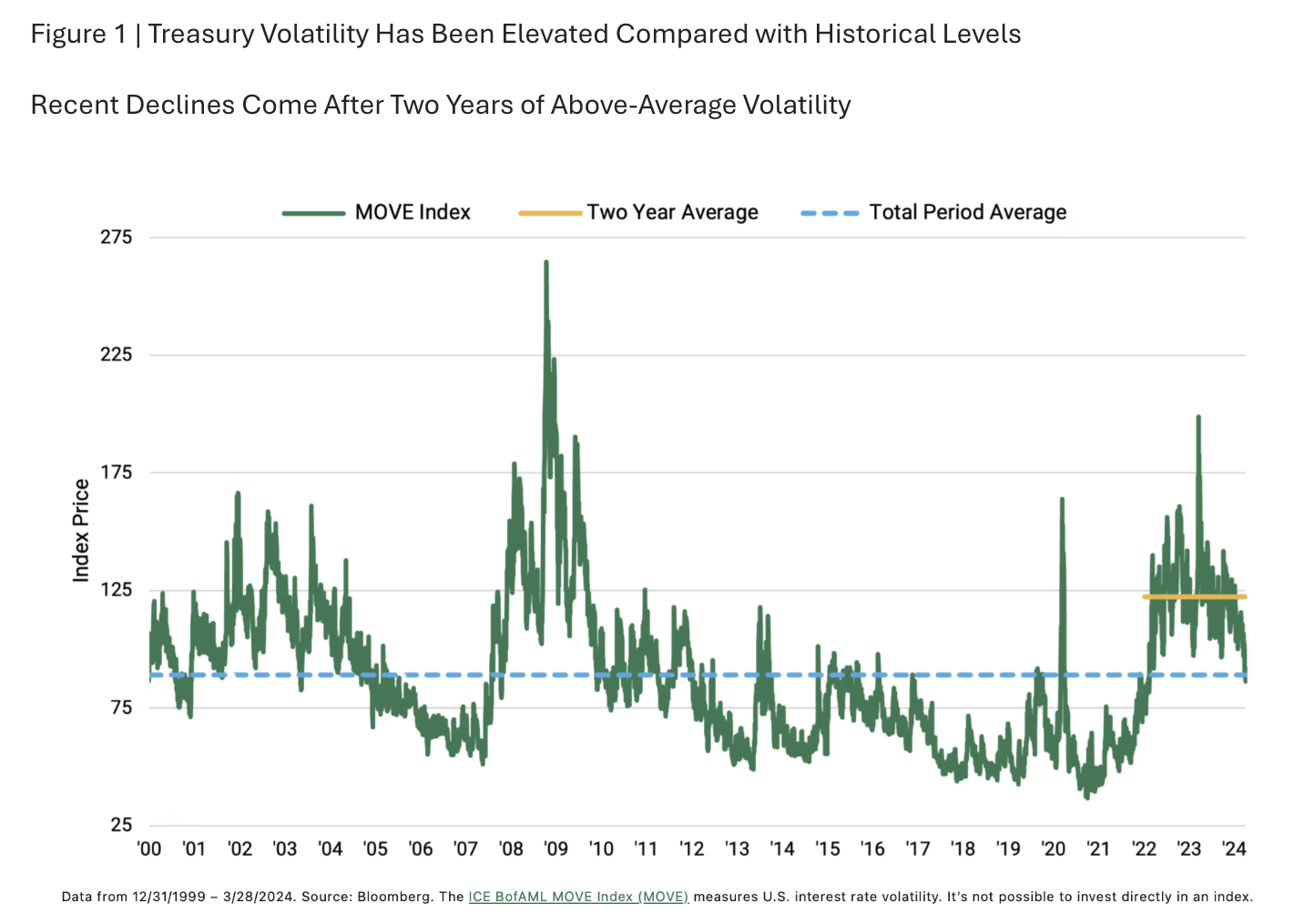

Interest rate volatility has emerged as a leading risk to bond investors

Fixed income is in a decidedly new regime, where yields have been broadly higher. But, at the same time, interest rate volatility has remained elevated, as Figure 1 illustrates. Because its duration is linked to the Bloomberg U.S. Aggregate Bond Index, the core plus strategy has exposed investors to this heightened rate volatility.

New bond market Bbackdrop, new alternatives for bond investors

Given this backdrop, we believe it may be time for investors to rethink their fixed-income approach. In our view, today’s economic and market environments demand a fixed-income option that nimbly and dynamically manages duration and credit risk. We prefer this approach over the traditional core plus strategy, which is typically less dynamic and often has longer duration and high credit risk.

Rate volatility has dominated fixed-income performance

According to Morningstar, the average core plus fund had an effective duration of 6.2 years as of December 31, 2023. In the three-year rising-rate period that ended December 31, the Morningstar Core Plus category average delivered an annualised return of -3.22%.[1] Over the same period, the 10-year Treasury note, which, unlike the core plus category, isn’t exposed to credit risk, delivered an annualised return of -5.93%.[2]

These performance results indicate the duration component of the average core plus fund dominated the credit components. The credit components only slightly supported investors during the duration-led return drawdown. This wasn’t ideal for investors who largely expected their fixed-income allocation to provide diversification and help manage risk.

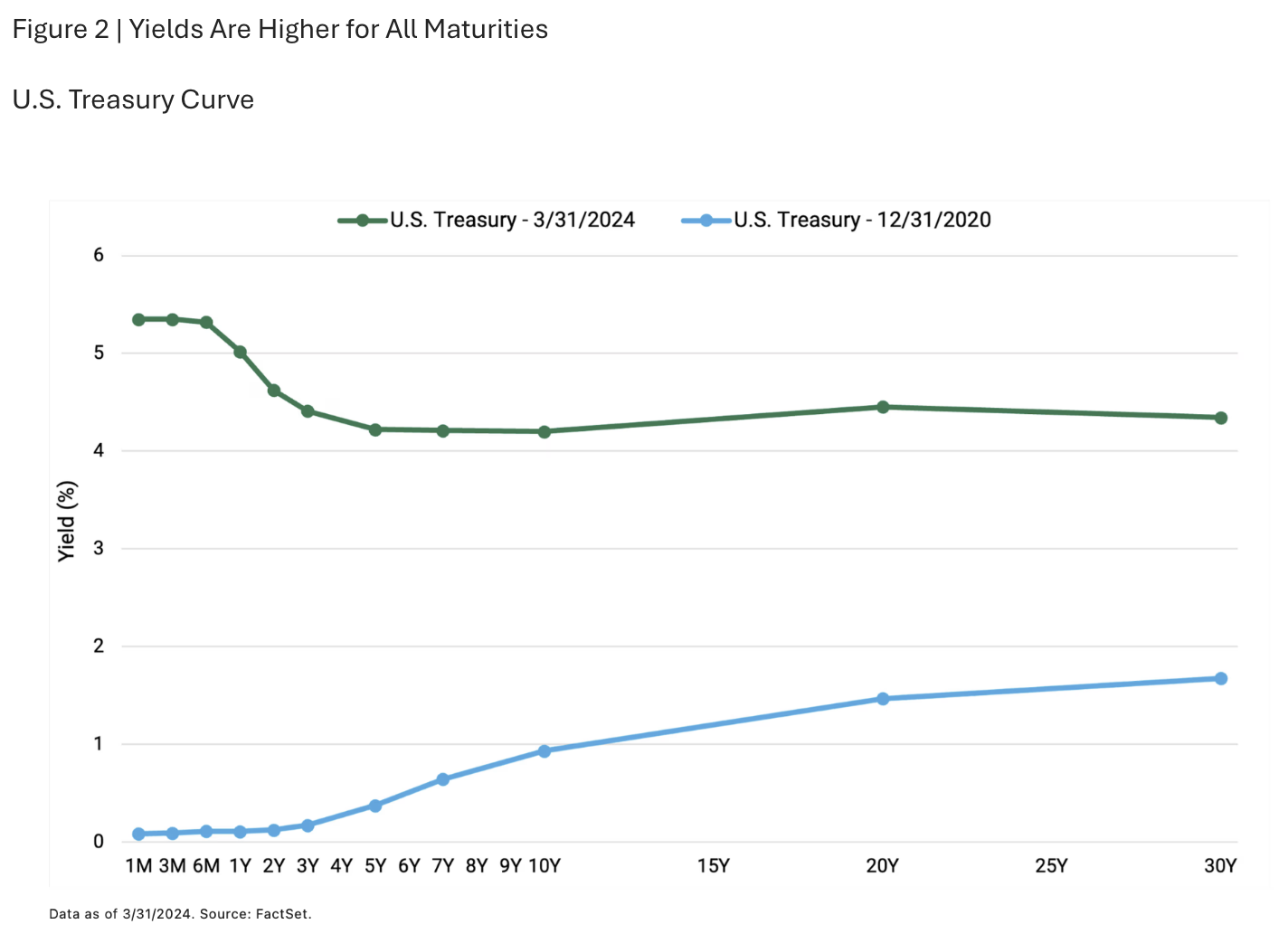

Yield has remained plentiful across the curve

The good news for fixed-income investors is that yields are generally higher across the yield curve. Figure 2 demonstrates how yields of all maturities have increased since the end of 2020.

Given this backdrop, we have found ample opportunities to pursue return and yield without stretching to core plus-like duration levels. Our research suggests that average bond yields could remain higher over the next 10 years than during the 10 years following the financial crisis. As a result, we expect to see more opportunities to enhance return and yield potential than in the prior low-yield environment.

But with the Fed approaching an inflection point — and given the normal course of economic and financial cycles — we also expect interest rates to be volatile. Accordingly, opportunities across fixed income will likely be changing, perhaps quickly.

Spotlight shines on securitised sector

For example, we have recently found more value in the securitised sector than in the corporate credit and government bond sectors. We believe we have uncovered high-quality asset-backed securities with attractive characteristics versus the Bloomberg U.S. Aggregate Bond Index, potentially creating a better outcome for investors.[3]

In our view, the more constrained opportunity set of benchmark-focused core plus strategies has led to a subpar experience for investors. We believe investors should consider a more dynamic fixed-income strategy not beholden to benchmark characteristics.

Multisector income: a nimble, diversified option for today’s market

American Century Multisector Income pursues a highly dynamic approach, diversifying risk across fixed-income sectors and the credit and duration spectrums. The portfolio isn’t bound to the Bloomberg U.S. Aggregate Bond Index’s total duration. The portfolio’s typical duration has been three to five years, well below the index’s typical range of five to seven years.[4]

We take a highly disciplined approach to risk-taking, investing only where our conviction levels are strongest on a relative basis. This strategy strives to deliver higher returns than the Morningstar Core Plus category average with less return volatility.

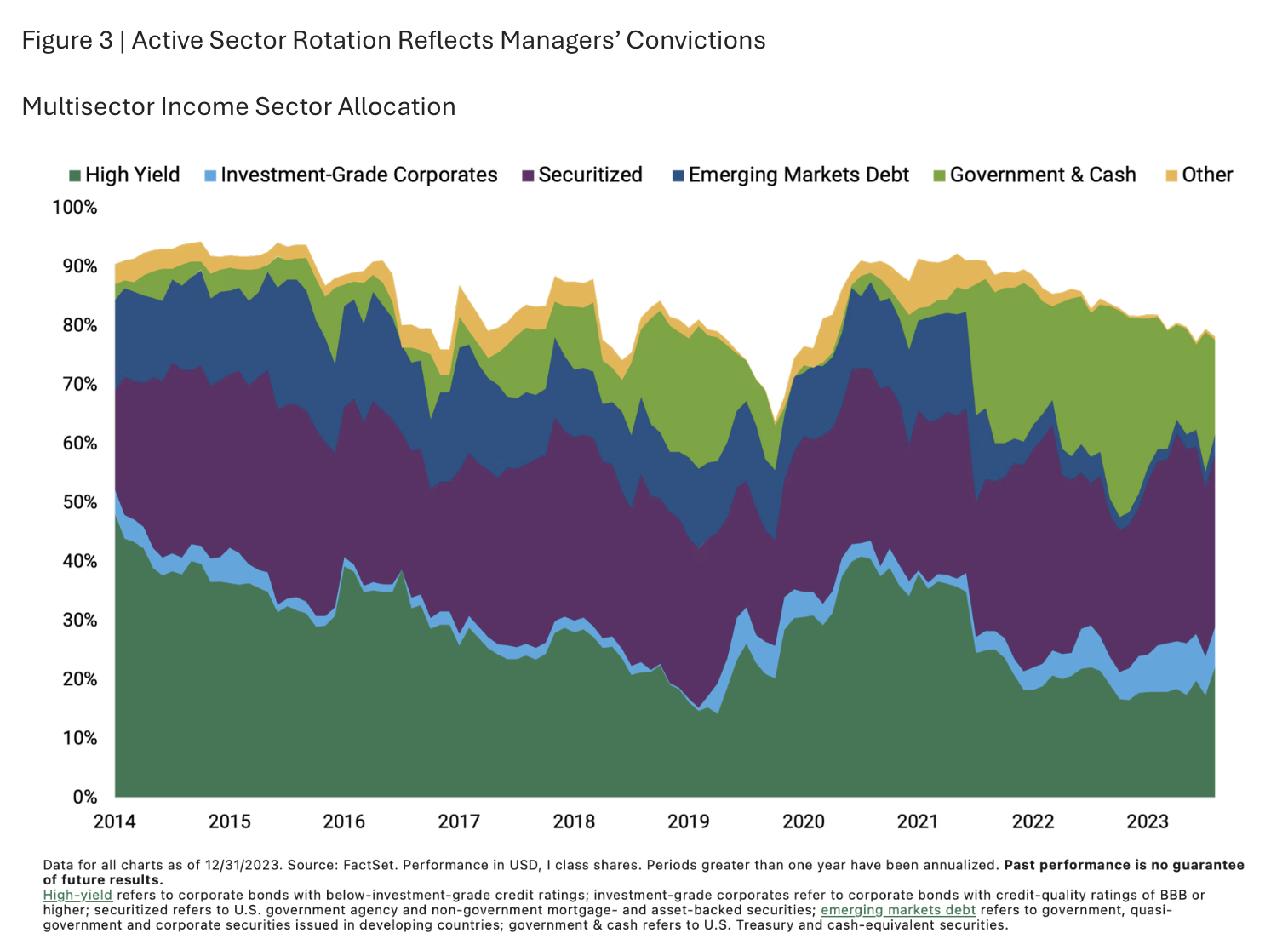

The flexibility to emphasise opportunities and avoid potential pitfalls

Absent benchmark constraints, we can also tailor credit exposure based on what we believe are the market’s best opportunities. For example, we may avoid less compelling sectors with unattractive risk-adjusted return potential, even if the index holds them. Figure 3 depicts how the portfolio’s investment mix has changed over the years.

Many of our peers have single-sector specialization.5 For example, some may be securitised specialists, while others focus on corporate bonds. In our view, these concentrated skill sets translate to more static and less diversified portfolios.

Conversely, we believe our depth and breadth of cross-sector capabilities highlight various opportunities across the broad fixed-income landscape. Conviction dictates our sector weightings, and we emphasise those we believe have more attractive return potential and risk characteristics.

Keeping liquidity in focus

We also understand the importance of portfolio liquidity. For many investors, fixed-income allocations may serve as a source of liquidity.

Accordingly, we don’t purchase private credit, we limit opaque derivatives in the portfolio, and we don’t employ leverage. When funds engage in these practices to amplify yield, they also amplify risk and illiquidity. These tactics are unnecessary, in our view.

Accordingly, our goal is for Multisector Income to deliver a solid all-weather fixed-income asset allocation solution.