Key takeaways

- The healthcare sector continues to be supported by strong long-term growth drivers, presenting overall as good value compared to history.

- The healthcare suppliers’ sub-sector, including equipment distributors (i.e. device suppliers) offer the best growth prospects, while we believe healthcare provider companies (hospitals, pathology) face challenges.

- Yarra views ResMed as a top investment pick within the healthcare sector despite the hype around weight loss drugs.

The healthcare sector isn’t just a refuge for cautious investors—it’s a thriving arena of innovation, growth and potential. As healthcare stocks become more appealing on lower multiples, the sector’s allure is undeniable, yet discerning true value requires more than a glance at current valuations. Amidst a complex environment, ResMed emerges as a standout candidate, offering compelling reasons to take a closer look.

From an investment viewpoint the healthcare sector is a multifaceted and evolving field, encompassing a wide range of businesses—from those supplying medical equipment and devices to those offering healthcare services and facilities, as well as companies advancing biotechnology, pharmaceuticals and technology. Historically, this sector has consistently outperformed the broader market, though it usually commands a valuation premium. Currently, valuations in healthcare are relatively low as the sector continues to recovery from Covid-disruptions, hinting at potential opportunities emerging.

Over the past decade, ASX healthcare sales and earnings have surged at [three times] the annual rate of ASX Industrial companies, making it an attractive sector and highlighting its quality attributes. Consensus forecasts predict 16% earnings growth for FY25, although we believe this projection may be overly optimistic.

While we are currently underweight in the sector overall, we currently see several promising opportunities within the sector. Specifically, we see opportunities in the Suppliers sub-sector, which appears particularly appealing. Conversely, we remain cautious about the Providers and Biotech subsectors due to margin recovery challenges and elevated expectations.

Challenges in healthcare: Why we believe providers and biotech will struggle

With inflation remaining high, companies in the Providers subsector—those offering healthcare services—are grappling with rising operational costs, in particular labour cost inflation. These firms typically lack the pricing power to pass on those higher costs, leading to squeezed margins. This struggle is evident in the last earnings updates from companies such as hospital group Ramsay Healthcare (ASX) and pathology leader Sonic Healthcare (ASX), and we expect will feature in upcoming results.

In the Biotech subsector, we see a slightly different picture. In the case of CSL, we note expectations are already elevated around the business’ ability to return margins from its global blood plasma business back to pre-Covid levels over the next few years. Moreover, of the 16 research analysts that cover CSL, 12 rate the stock a ‘buy’ or a ‘strong buy’ (only 1 is a ‘sell’) leaving less opportunity for positive surprise.

Suppliers: Capitalising on post-Covid demand and device access

Our primary focus is on the Suppliers part of the healthcare sector, comprising a number of quality business that have faced temporary disruption or stock over-reactions. Unlike the Providers, who struggle with limited pricing power, and Biotech companies where forward expectations are already elevated, Suppliers are experiencing different challenges. This sector, including Cochlear implants and ResMed CPAP machines, is benefiting from the ongoing normalisation in patient demand post-Covid, with evidence of stronger market share participation and improving practitioner availability.

Weight Loss Drugs: A lesser threat to ResMed’s market opportunity

Last year, weight loss medications including Ozempic captured headlines for their potential impact on obesity, overshadowing other significant healthcare developments. As excitement surged around these new market favourites, established healthcare stocks were largely overlooked and some were sharply sold off due to speculation about a transformed healthcare landscape. ResMed (ASX), known for its devices treating obstructive sleep apnoea, was one such latter example. The company saw notable volatility, including two steep selldowns, as investors worried that weight loss drugs might reduce the need for its products by improving sleep quality for those with obesity-related sleep issues.

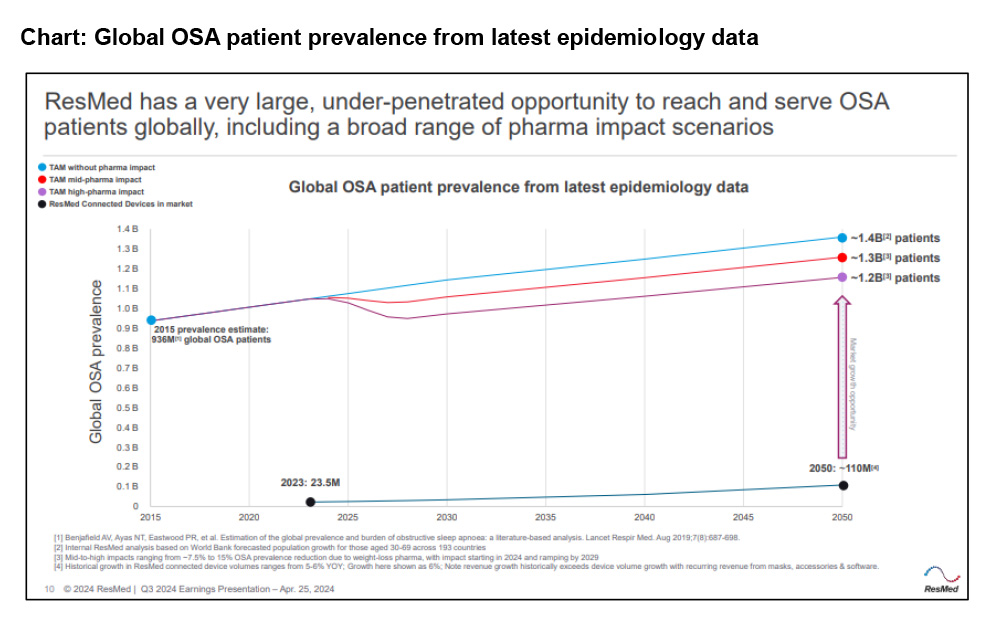

As the initial excitement about weight loss drugs waned and ResMed’s share price stabilised, it became apparent that the anticipated threat to ResMed could be well managed, and weight loss drugs could prove to be more complementary for CPAP demand, rather than replacing it. Additionally, well less than half of CPAP users in the US are non-diabetic and obesity driven, leaving a significant market for ResMed’s devices in what remains a significantly under-penetrated market. Moreover, a recent study of 660,000 patients revealed that GLP-1 users were actually 10.5% more likely to start CPAP treatment and had higher resupply rates over one and two years.

It is also worth noting the real-world challenges around weight loss drug adherence. Numerous studies to date point to 12-month adherence rates being well below 50% driven by a combination of affordability (obesity-driven users typically pay around US$12,000 outof-pocket in the US) and side-effect concerns. Side-effect risk was highlighted in July following the release of analysis from doctors at Massachusetts Eye and Ear, a Harvardaffiliated hospital, that pointed to potential heightened risk of vision loss from weight loss drugs.

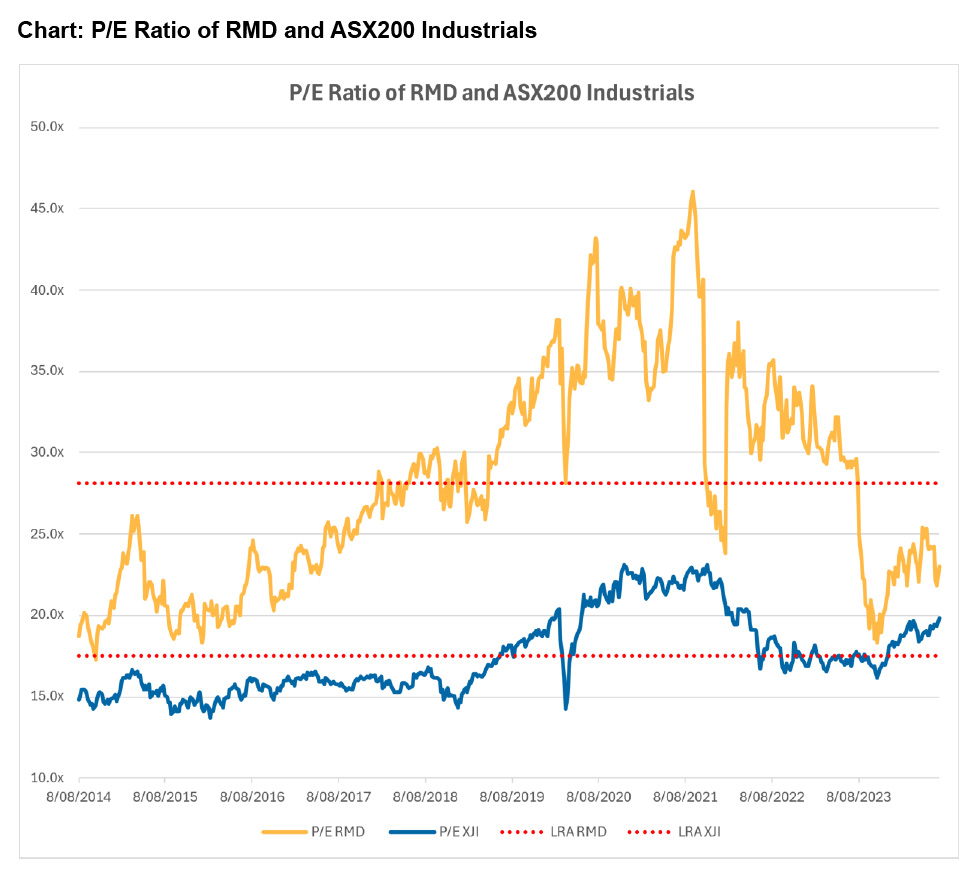

Examining ResMed’s market position, it stands out with few true competitors, the main one being Philips, which continues to deal with a product recall which was first announced in mid-2021. Uncertainties persist regarding when Philips will re-enter the US market with a sleep apnoea device and the extent of operating constraints and compliance oversight once the regulator does permit them to return to the market. In terms of ASX peers, ResMed appears attractively priced at around 23x earnings, materially below its 10-year average of 28x earnings. In contrast, the ASX200 Industrials currently trades at approximately 19.8x earnings, meaningfully above their 10-year average (17.5x earnings).

Given ResMed’s robust standing in the sleep apnoea market as the clear market leader, its expected sales resilience despite the rise of GLP-1s, and the renewed demand for ventilators and masks post-Covid, we continue to maintain an overweight position in our portfolio. Word count: 806

By Marcus Ryan, Deputy Portfolio Manager, Broadcap Equities