Saira Malik

Holiday cheer or new year drear: What will December bring?

For consumers, there are 16 shopping days until Christmas, and for investors, just 12 trading days. In either case, the holiday season is in full swing, and like countless children around the world wishing for something special from jolly old Saint Nick, equity markets are hoping the U.S. Federal Reserve will bring them a comfy-cozy interest rate cut (size 25 basis points, please) at next week’s Fed policy meeting. Market odds currently favour just such a move.

But while equity markets are exuding holiday cheer as they trade at or near all-time highs, public fixed income investors appear more reserved, preparing for a higher-for-longer interest rate environment as the bond yield backup that followed the Fed’s first rate reduction in September remains intact. Unexpected economic resilience in the wake of that cut makes it difficult to divine the direction and pace of monetary policy. Last week’s release of consensus-topping U.S. nonfarm payrolls for November offered the latest evidence of labour strength, as job creation rebounded from a weak October marred by disruptive hurricanes and worker strikes. Meanwhile, wage growth remained steady at +4.0% year-over-year.

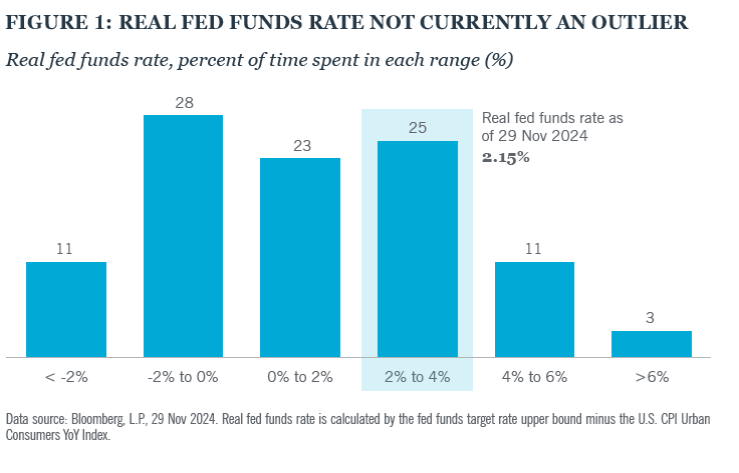

On balance, we think investors needn’t be overly concerned that the Grinch or Scrooge will derail the Fed’s sled this December. It’s also worth noting that the current level of the real fed funds rate is not an outlier relative to history (Figure 1). So even if a beloved flying woodland creature with a storied illuminative nose were waylaid, this investment season still offers sound portfolio allocation ideas that can counter the potential chill of a higher-for-longer rate environment.

Portfolio considerations

The U.S. economy is approaching 2025 on solid footing, with GDP growth above expectations and the employment market remaining resilient. We expect the Fed will continue its easing cycle, but at a slower pace than markets previously anticipated. A milder and more protracted decline in interest rates means fixed income investments may not benefit much from capital appreciation in the near term. Against that backdrop, our fixed income positioning for next year is focused on four themes:

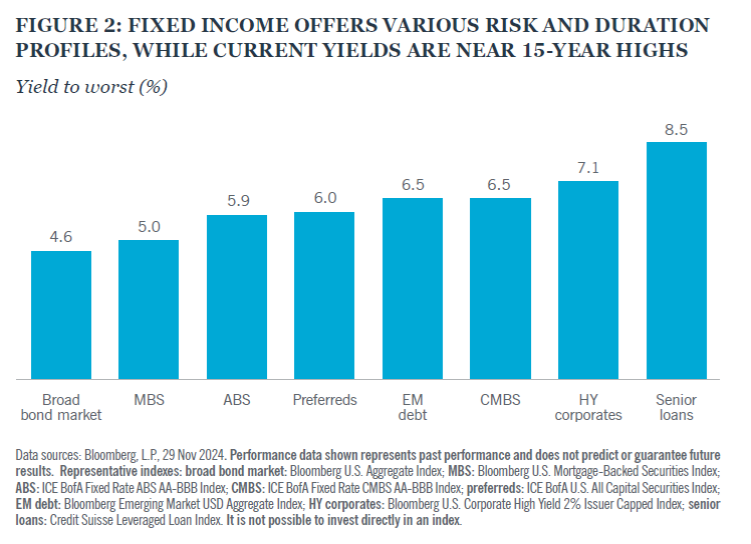

- Current yields are near their highest levels in more than 15 years. Higher base rates have significantly enhanced income potential, with yields of about 6% or more for investment grade plus sectors such as preferred securities and securitized assets, including asset-backed securities (ABS) and commercial mortgage-backed securities (CMBS) (Figure 2).

- Short- and long-term rates will be higher for longer. That makes exposure to shorter-duration, floating-rate instruments such as senior loans — currently yielding 8.5% — a compelling choice, especially given their sound credit fundamentals. Like senior loans, ABS are also relatively low duration, in addition to providing attractive yields. Also worthy of consideration are esoteric securities backed by nontraditional assets, offering a spread between 75 and 125 basis points in yield compared to short-maturity corporate bonds.

- Balance duration risk with credit risk. Within investment grade categories, we are less positive on corporates, where duration is much longer than in other fixed income sectors. In contrast, preferred securities — in particular, the $25 par segment — offer nearly 1.5% of yield per year of duration. Preferreds also look well-positioned for 2025, as potential deregulation and an expected pickup in M&A (mergers and acquisitions) activity could bode well for banks, the largest issuer of preferreds.

- Position for volatility. In the below-investment grade space, we favour an up-in-quality approach. Within senior loans, we find exposure to BB and B rated issues particularly attractive. BB rated loans, for example, have a healthy interest coverage ratio of 4.X, according to Bloomberg.

By Saira Malik, Head of Equities and Fixed Income, Chief Investment Officer