Chad Padowitz

The recent surge in US equity markets, particularly the S&P 500’s 23 per cent increase in 2024, is largely due to valuation expansions. This has created significant risks for investors, as these expansions are arguably not justified and in turn exposes them to a greater risk of a paying too much for shares that may fall in value over time.

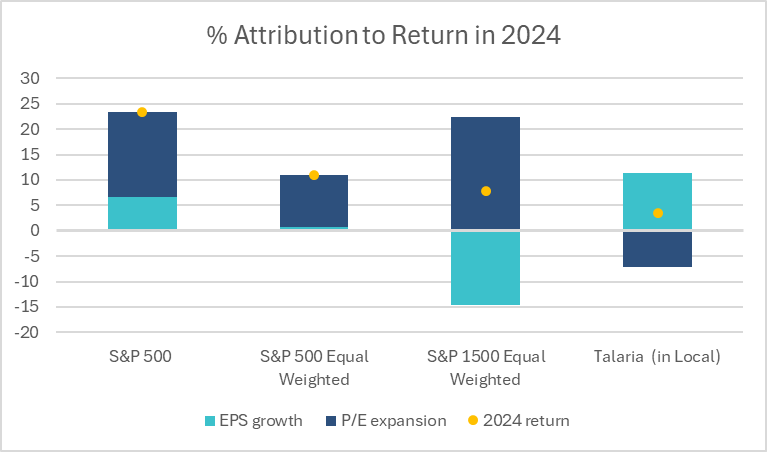

Early in 2025, the resultant risks are in plain sight. The chart below shows that while 7 per cent earnings per share (ESP) growth contributed to US share market gains last year, the much larger driver of rising share prices was an expansion in valuation multiples, as investors were willing to pay significantly more for each dollar of companies’ sales or earnings.

Source: Talaria, Bloomberg. Talaria return is only local performance of gross capital at risk of holdings as of 31 December 2024 for illustrative purposes.

While continued enthusiasm for mega tech may have made sense, what arguably went against logic was the degree of enthusiasm for a broader cohort of US stocks. The S&P 500 Equal Weighted index saw a 10 per cent rise last year driven almost entirely by valuation, despite only a 1 per cent increase in earnings per share (EPS).

Even more striking was the S&P 1500 Equal Weighted, which reflects a broader and more representative sample of US listed companies. EPS for these companies fell by 15 per cent, yet the index still delivered an 8 per cent return, driven by a dramatic multiple expansion.

Those high valuations have left little room for error for investors in the broader US stock market. The S&P 500’s forward price earnings ratio is significantly higher than its historical averages. For example, the latest forward price-earnings (P/E) ratio of 21.7x is 1.9 turns higher than the five-year average and 3.4 turns higher than the ten-year average.

This highlights that the rationale for paying more for many US shares is not solely related to recent and near-term fundamentals. Instead, it appears to rely on optimistic assumptions around further margin expansion, earnings and continued multiple expansions across the board, which may not be realised.

Lowering risks should be a key focus

While the risks associated with this trend are growing, calling an end to it is not our focus. Instead, we think investors would be wise to prioritise sectors with attractive valuations rather than chase the momentum. Practically, this means for every incremental dollar moving away from the current enthusiasm for mega technology companies to reduce investment risk

into those stocks with less balance sheet risk including companies with lower refinancing risk, and lower vulnerability to credit spreads. Portfolios with higher initial earnings yields may also be more attractive, even if their projected growth rate is slightly lower.

It will be important for investors to avoid overreacting to short-term market fluctuations and focus on long-term performance, especially with the potential for more share market volatility from rising bond yields and the second Donald Trump led US government.

A critical point for Australian investors

With valuations in mind, the coming year presents a critical moment for Australian investors. The temptation to follow market momentum will be strong, but long-term performance requires patience and rationality.

By Chad Padowitz