What are the varied tax regimens as they apply to clients’ superannuation savings, in both the accumulation and decumulation phases?

Superannuation is regarded as the most tax-effective way to save for retirement. However, tax effective is not tax free. This article, proudly sponsored by Allianz Retire+, explores the super tax facts.

Australia’s total superannuation assets were $4.2 trillion at the end of 2024[1] which makes our nation the fifth largest pension market in the world[2]. The Australian superannuation sector has experienced phenomenal growth; the size of our asset pool has increased by nearly 500 percent over the last 20 years and, should this growth trajectory be maintained, Australia could become the second largest pension market globally by 2030[3].

With money comes interest – from those keen to make it, those keen to manage it – and those keen to regulate it. The growing size of Australia’s superannuation assets have superannuation firmly in the sights of government agencies (including the ATO) and regulatory bodies. Although this scrutiny plays a vital role in safeguarding the nation’s retirement savings, it can also result in some ‘tinkering’ with the system.

While a well-known quote suggests that death and taxes are the only certainties in life, change is just as inevitable. Advisers are all too familiar with this reality, especially when it comes to superannuation and taxation. The rules governing super contributions, earnings, and withdrawals—along with their tax implications—are continually reviewed and adjusted.

Staying informed about the taxation system and its impact on superannuation is essential, as is the ability to clearly explain these complexities to your clients. By staying up to date with evolving tax and super laws, you not only showcase your dedication but also ensure your clients receive comprehensive, tailored financial solutions and are well positioned for positive retirement outcomes.

Super and tax

Super may be taxed at three points throughout its life cycle – on contributions, investment earnings and withdrawal. Super is generally taxed at a lower rate than regular income and withdrawals are tax-free if a client is 60 years or older. However, as with all taxable funds, it’s not straightforward. There are different types of contributions, some of which attract tax. The approach to taxation of earnings differs between the accumulation and pension phases. Super withdrawals can involve a wide range of complexities and variations. Finally, the tax treatment of defined benefit pensions differs from those drawn from an account-based pension.

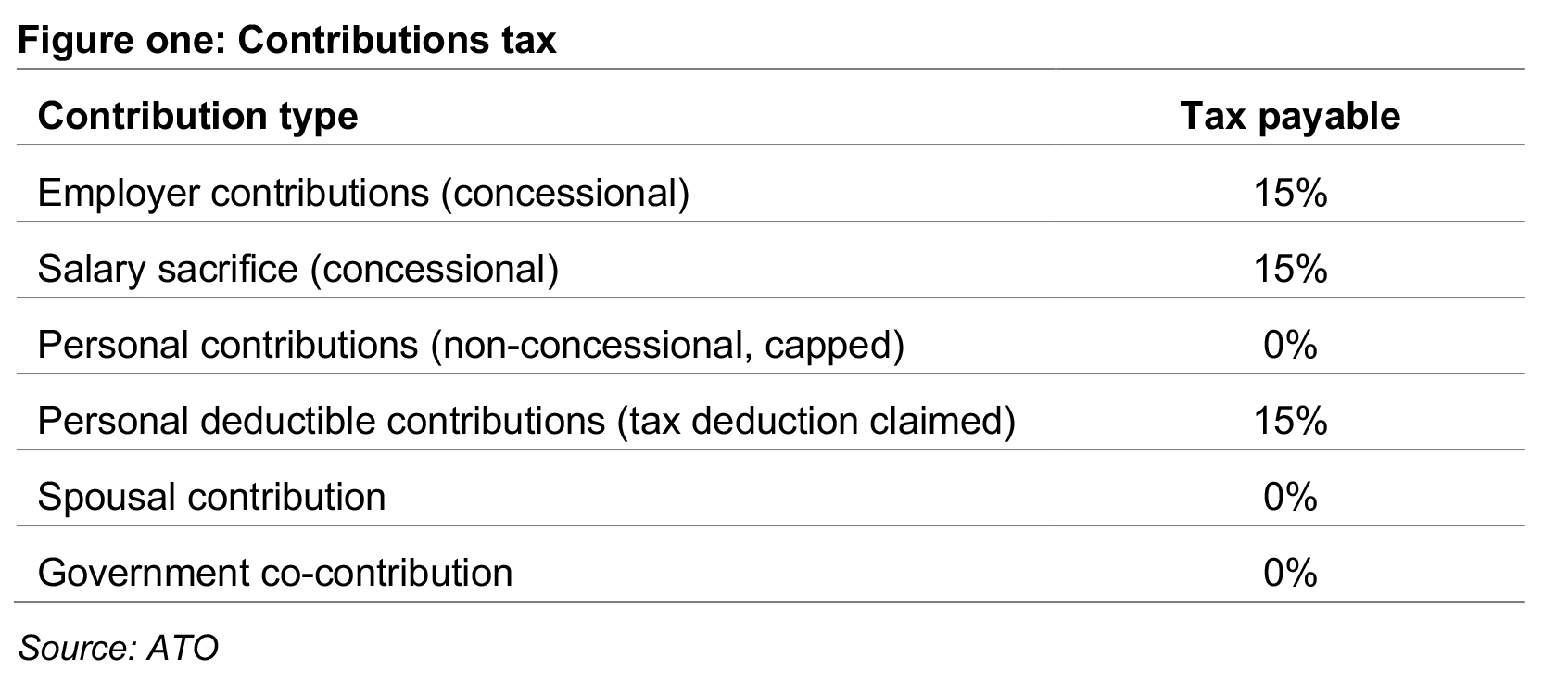

Contributions

Limits apply to both concessional and non-concessional contributions; these limits apply to the amount your clients can contribute to superannuation each year before incurring additional tax. This applies to money contributed to both superannuation funds and self-managed superannuation funds (SMSFs).

Concessional contributions or ‘before tax’ contributions include employer super guarantee (SG) contributions, other amounts paid by your clients’ employer as part of an agreement with you as well as other amounts paid by your clients’ employer from their before-tax income to their super fund, such as administration fees and insurance premiums. Other concessional contributions can include salary sacrifice contributions up to the contributions cap.

Non-concessional contributions are after tax contributions made by your client or their employer. Clients over the age of 75 may not make voluntary contributions to their super but may receive Superannuation Guarantee contributions from an employer. If a client has $1.9 million or more in the super system on 30 June in the previous financial year, they’re not able to make any non-concessional contributions.

Before-tax contributions are generally taxed at 15%, unless your client:

- has not provided their Tax File Number to their super fund

- earns more than $250,000 per annum

- exceeds the concessional contributions cap.

For the 2024-2025 financial year, the contributions caps are:

- concessional contributions – $30,000

- non-concessional contributions – $120,000.

Any excess concessional contributions will count towards the non-concessional contributions cap.

Where a client exceeds their contributions cap, additional tax becomes payable. Only the amount above the relevant limit is subject to additional tax; for example, if your client contributed $20,000 over the limit, extra tax is charged only on that $20,000. Concessional contributions that exceed the cap are taxed at the client’s marginal tax rate (including Medicare Levy).

Withdrawals

Each client must satisfy a condition of release to withdraw money from super. There are four main conditions of release, which include:

1. your client turns 65, even if they haven’t retired

2. your client reaches preservation age (figure two) and

3. your client commences a transition to retirement income stream (TRIS) while continuing to work part or full time. A TRIS strategy enables your client to top up the income received from their employment with a regular income stream from their super once they have reached their preservation age.

This income stream enables your client to either reduce their working hours without reducing their income or continue working and increase salary sacrifice contributions to boost the value of their super.

There are restrictions on the amount a client can withdraw via a TRIS in any one financial year. A client under 65 years old must receive a minimum of four percent and a maximum of 10 percent of the balance of their super funds each financial year.

The exception to this is if and when your client meets a ‘nil cashing restriction’. This includes the scenario where your client:

- reaches preservation age and retire

- turns 65

- becomes permanently incapacitated

- us diagnosed with a terminal medical condition.

Satisfying a condition of release with a nil cashing restriction (as detailed above) means that the account-based pension is no longer subject to the restrictions that generally characterise a TRIS.

When implementing a TRIS strategy, you and your client need to decide from which payer to claim the tax-free threshold on the client’s tax file number declaration. If the client claims the tax-free threshold with both an employer and the super fund, they may face a tax liability at the end of the financial year.

A TRIS automatically rolls into the retirement phase as soon as your client reaches 65 years old. For the other conditions of release listed above, the client needs to notify their super fund to instigate the move from TRIS to the retirement phase.

4. The client satisfies an early access requirement, such as they:

- can claim on medical, compassionate, hardship or incapacity grounds

- can claim to withdraw voluntary contributions under the First Home Super Saver scheme

- are a temporary resident who is permanently leaving Australia.

Tax-free and taxable components of withdrawals

Some super is tax-free and some taxable upon withdrawal, depending on the type of contributions made and whether tax was paid on it.

Tax-free withdrawals are generally from your client’s non-concessional (after-tax) contributions, including personal contributions made from after-tax income, unless your client was allowed a tax deduction for them.

Taxable withdrawals are generally from concessional (before-tax) contributions – those made from income before tax was paid on it. This includes:

- super contributions made by your client’s employer

- contributions your client made by salary sacrifice

- super contributions your client claimed a tax deduction for.

The amount of tax paid on withdrawal of taxable super prior to age 65 depends on:

- contributions and related investment earnings on which your client’s super fund has paid tax (at the rate of 15%) forms the ‘taxed element’ of your taxable super

- any amount included in your client’s taxable super that the fund has not paid tax on forms the ‘untaxed element’ of their taxable super.

Generally, a client’s super benefit will include both a tax-free and a taxable component. When a withdrawal is made, the super fund calculates the components of the withdrawal based on the proportion of components that make up the total value of your client’s super account.

Investment earnings

Superannuation is regarded as a good retirement savings vehicle because of the low tax paid on investment earnings. During the accumulation phase, earnings are taxed at 15 percent and are deducted from those earnings by the fund. Once a client opens a retirement income stream, investment earnings are tax-free.

Where a client takes a lump sum and invests it outside of superannuation, investment earnings may be subject to tax.

Tax offsets

Those clients who are retired or over 60 may be eligible for tax offsets; this is dependent on their income and assets, where their income is derived and whether they retired, fully or partly.

The relevant offsets are:

- The seniors and pensioners tax offset (available only to those who qualify for the Age Pension)

- Lump sum tax offset

- Super income stream tax offset

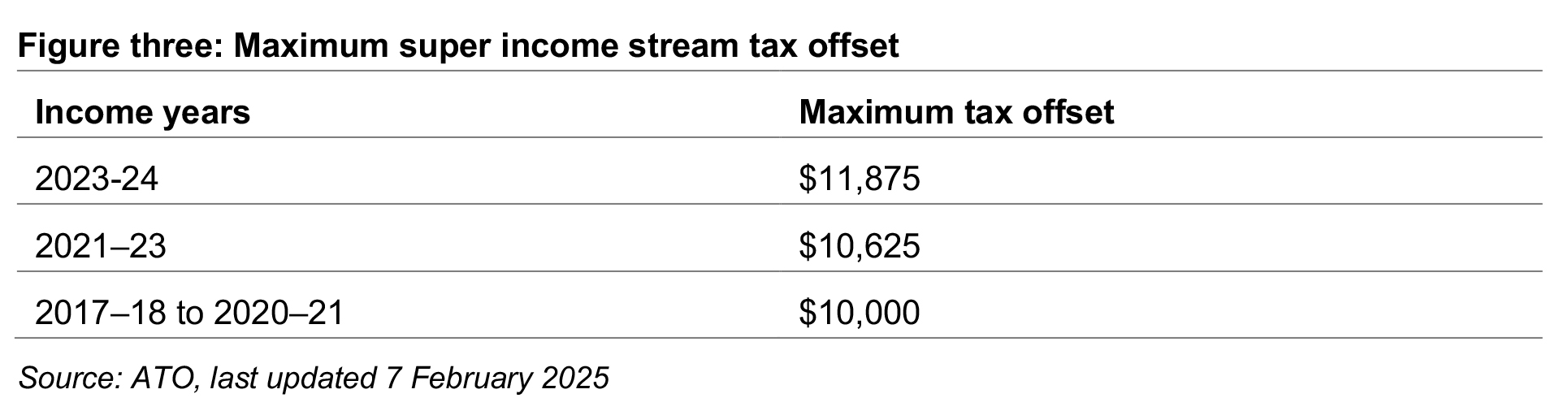

Most super accounts are comprised of taxed and untaxed elements. A client receiving income from a super income stream may be eligible for a tax offset equal to:

- 15% of the taxed element

- 10% of the untaxed element

The tax offset amount available to your client on the taxed element will be shown on the PAYG payment summary received from their super fund at the end of each financial year.

The tax offset amount the client can claim on the untaxed element will not be shown on this payment summary and is subject to a cap (figure three).

Tax offsets cannot be claimed for the taxed element of any super income stream your client receives before they reach their preservation age, except where the super income stream is a disability super benefit or death benefit income stream.

Lump sum withdrawals

Lump sum withdrawals may be subject to tax (figure four), especially if the client has not reached preservation age; for those under, 60 lump sum payments may be accessible only if special circumstances are met.

The low rate cap amount is the limit set on the amount of taxable components (taxed and untaxed elements) of a super lump sum that can receive a lower (or nil) tax rate. It applies to clients who have reached their preservation age but are below 60 years. It’s a lifetime cap that’s reduced by any amount previously withdrawn and applied to the low rate threshold.

Once a lump sum is withdrawn from a super account, it’s no longer considered to be super. If your client invests the money, earnings on those investments are not taxed as super and generally need to be declared in the client’s tax return.

Defined benefit pensions

Income received from a defined benefit pension is generally comprised of three components:

- a tax-free component

- a taxable component that is already taxed

- an untaxed taxable component.

The untaxed component is included in your client’s assessable income and tax is paid at their marginal tax, rate less a 10 percent tax offset. However, if the client is over 60, the tax-free and taxable component are generally received tax free and are not assessable.

This changes when the client’s total annual pension payments are above the defined benefit income cap, which is $118,750 for the 2024-25 financial year. In this scenario, the client will lose the 10 percent offset above this amount. In addition, 50 percent of the tax free and taxable components above this amount become taxable.

Division 296 tax

This new proposed tax has proved divisive and has yet to get legislative support. It was rescheduled for debate on 13 February 2025, as the last bill on the last day of the current parliamentary sitting period. It was not passed and is unlikely to be put to the Senate before the next federal election.

The proposed new tax would be introduced under Division 296 of the Income Tax Assessment Act 1997 and will apply at a rate of 15% to the portion of ‘earnings’ exceeding $3 million at the end of the financial year, calculated using the following formula:

Tax Liability = 15% × Earnings × Proportion of Earnings

This 15% tax will be imposed in addition to the tax already paid by the superannuation fund on assessable income.

The proportion of earnings above $3m at the end of the financial year subject to the new 15% tax will be calculated under the following formula:

Proportion of Earnings = Total Super Balance Current Financial Year − $3 million

The ‘earnings’ component will be calculated as the movement in the total superannuation balance of the member for the year, adjusted for most contributions and withdrawals through the year, using the following formula:

Earnings = Total Super Balance Current Financial Year − Total Super Balance Previous Financial Year + Withdrawals – Net Contributions

The Australian Taxation Office (ATO) will assess the tax at the individual level, following the same approach used for Division 293 tax. Individuals will have the option to pay the tax personally or authorise their superannuation fund to make the payment on their behalf.

In summary, it is crucial for financial advisers to have a thorough understanding of the tax regime as it applies to the superannuation system. As you guide your clients through the complexities of the financial landscape, the interplay between tax and super highlights your essential role in maximising your clients’ retirement outcomes.

In an ever-changing economic environment, where legislative updates are frequent and market fluctuations can cause client uncertainty, advisers with in-depth knowledge of taxation within the superannuation framework are best equipped to provide timely and relevant guidance.