Kirby Rappell

In a year of extraordinary global events, Australians can find comfort in their retirement balances continuing to grow. The first half of the year brought back some much-needed stability to fund returns; however, the second half saw extreme ups and downs as global events threw markets into turmoil. The final result, a double digit return for the median Balanced option, fails to capture the ups and downs experienced over the 12 months to 30 June 2025 but reinforces the benefit of taking a long-term approach to retirement savings.

In what feels like a replay of the past two years, international technology and Australian financial shares drove the majority of returns with options designed to track a benchmark outperforming more active investing strategies thanks to exceptional multiyear growth in a small number of companies.

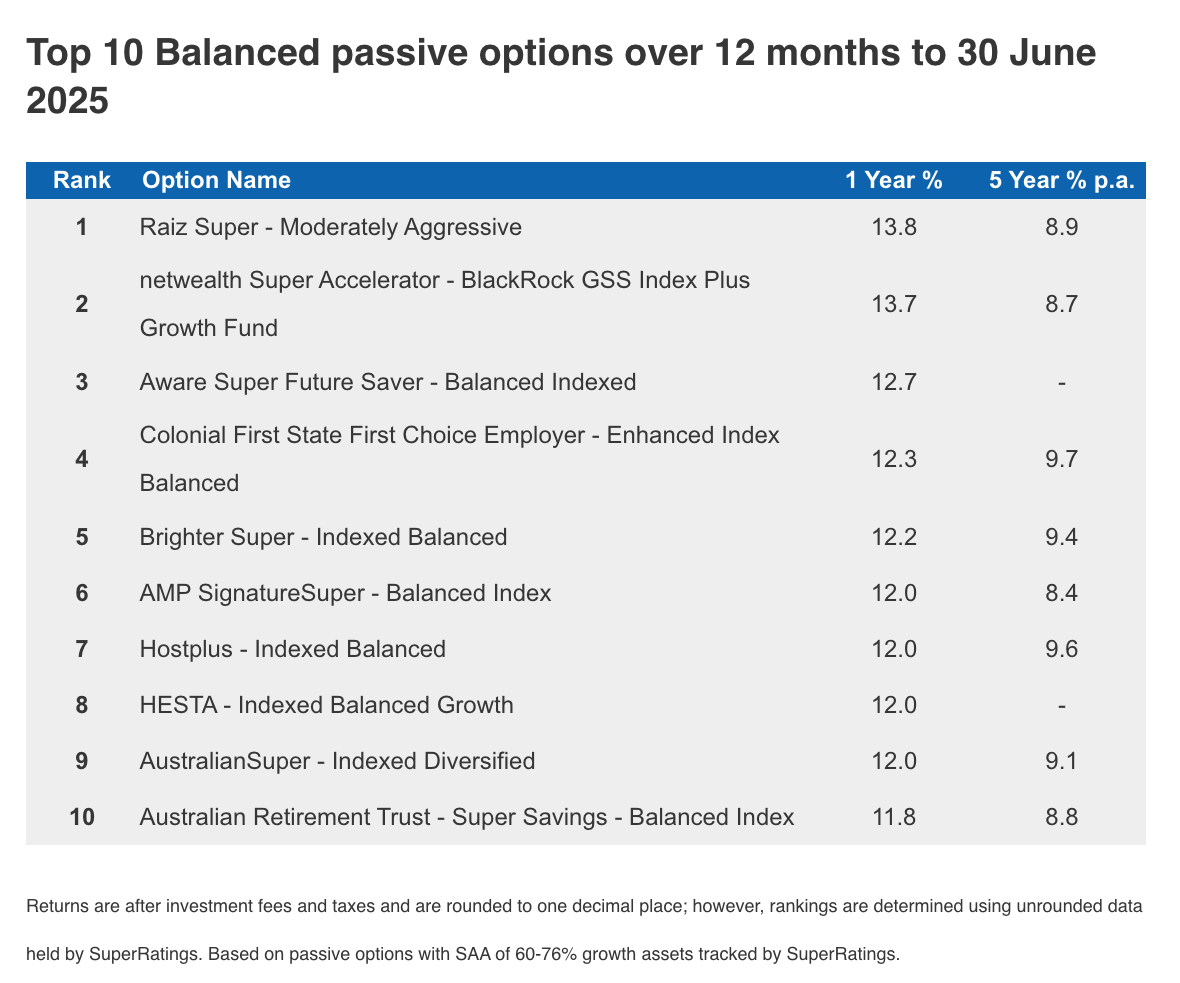

All Balanced funds, those with a strategic allocation of between 60% to 76% of their portfolio invested in growth assets, are again expected to deliver positive returns to members, while over half are expected to reach double digits for the year. Raiz Super’s Moderately Aggressive option took out the top spot in the SR50 Balanced (60-76) Index for the year ending June 2025 with a return of 13.8%, while legalsuper’s MySuper Balanced option return of 12.6% came in second. Hostplus’ Indexed Balanced option ranked third with a 12.0% return, closely followed by Colonial First State’s Enhanced Index Balanced option which also returned 12.0%.

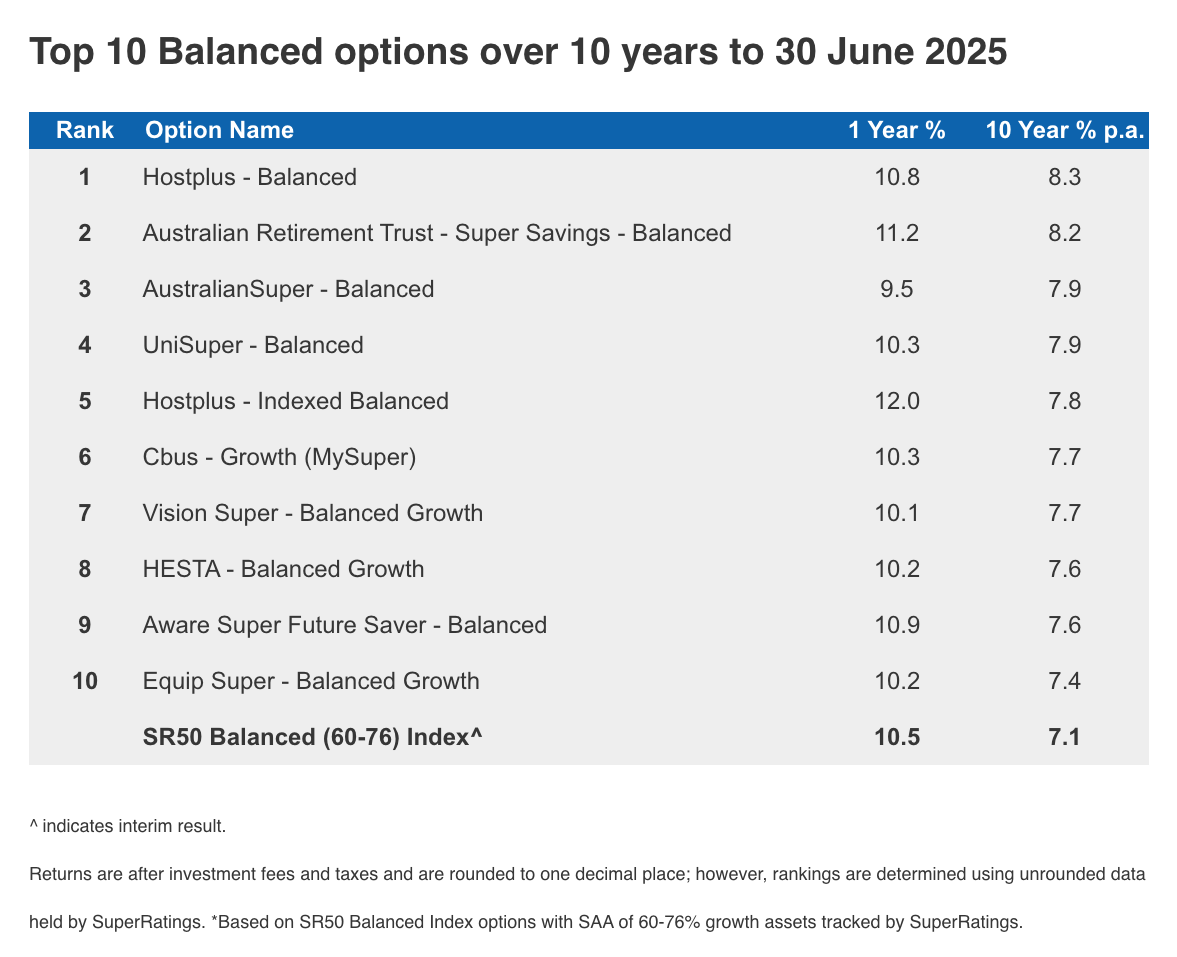

The table above displays the performance of the top performing Balanced funds for the year to 30 June 2025, as well as showing 10-year returns for those options with 10-year performance history, an important consideration given the long-term nature of superannuation investments.

“It’s pleasing to see a range of funds in this year’s top performers with some smaller funds showing their ability to deliver strong returns to their members through uncertain times” said Kirby Rappell, Director of SuperRatings.

Passively invested options, those tracking a benchmark at low cost, had another stellar year led by the strong returns of the magnificent seven in the US and CBA in Australia. The median passive investment option returned 11.8% for the year and 8.8% per annum over the past five years.

The top performing passive fund was Raiz Super’s Moderately Aggressive option with a return of 13.8% for the year to 30 June 2025, followed by netwealth Super Accelerator’s BlackRock GSS Index Plus Growth Fund and Aware Super’s Future Saver – Balanced Indexed option at 13.7% and 12.7% respectively.

Younger members with increased exposure to growth assets benefited from being invested in default lifecycle options over the year. For members aged 45 invested in lifecycle options the median return was 12.0% for the year. “While higher exposure to growth assets has benefited members over the past few years, it also comes with increased ups and downs, and we encourage members to learn how their fund’s investment strategy works so they are comfortable with annual and long-term performance outcomes.”

“With so many global events over the year there has been an increased level of uncertainty around fund returns this year” commented Mr Rappell. “However, superannuation is designed to build and maintain wealth for retirement and since most of us will have plenty of time until we retire and begin accessing our superannuation it is important to block out as much of the noise as possible and focus on how we are doing over the long term”.

Hostplus’ Balanced option remained the highest performing balanced option over 10 years returning of 8.3% p.a. followed by Australian Retirement Trust’s Balanced option and AustralianSuper’s Balanced option with 8.2% and 7.9% respectively.

“This year has been a strong result, well above the long-term annual return of 7.2% since compulsory superannuation began in 1992. Converted into dollars, $1 invested in the median balanced super fund in 1992 would now be worth approximately $2.84” continued Mr Rappell.

More ups and downs expected ahead over FY26

The increased ups and downs in the second half of FY25 were another reminder that superannuation settings need to be monitored to ensure they are suitable to current circumstances. Depending on when members need to begin drawing on their funds, they may have the option to ride out these kinds of ups and downs, however for members nearing, or in, retirement minimising these fluctuations can be a key factor in their retirement planning.

“Protecting members’ balances from sharp falls is a key function of superannuation investment teams and grows in importance as members near retirement or uncertainty rises,” said Mr Rappell. “While some funds that were more defensively positioned didn’t benefit as much from growth over the year, having strong diversification helps shelter members from market fluctuations and supports smoother returns over the long term”.

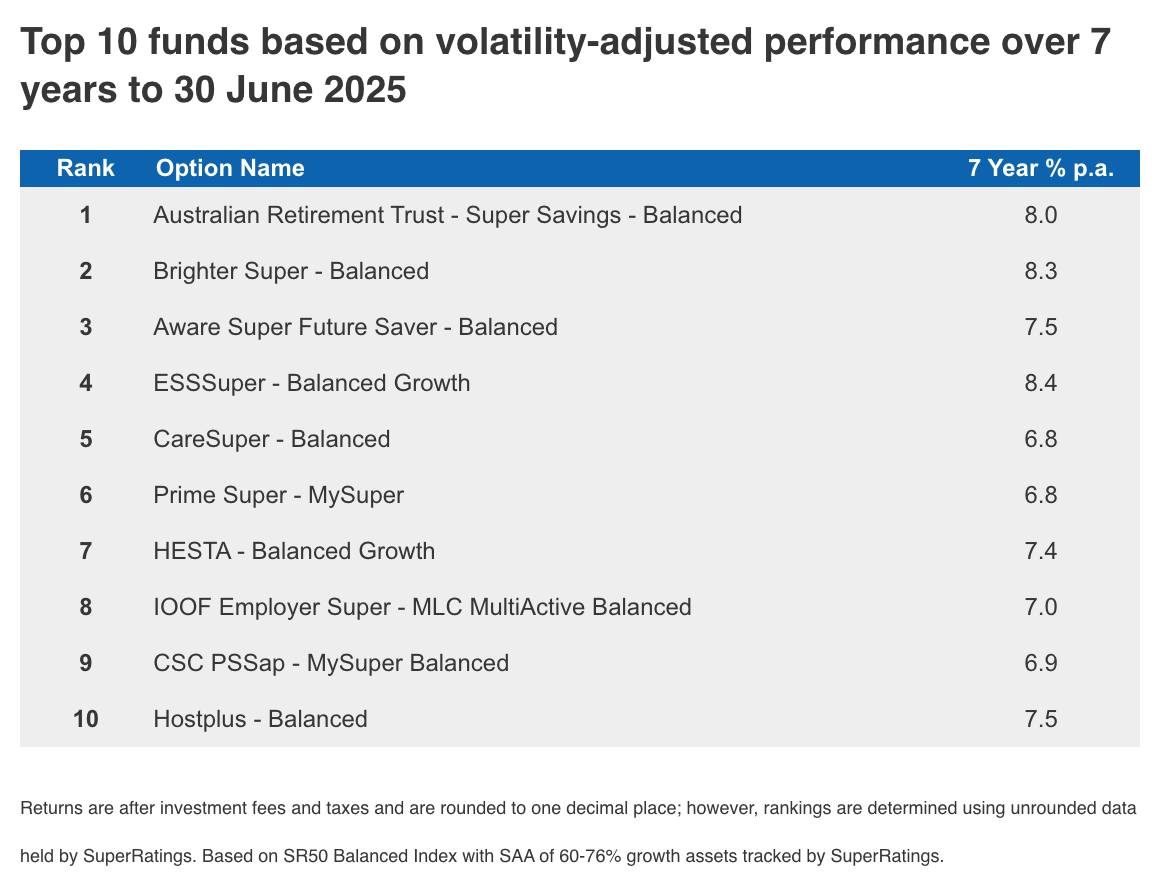

The table below shows the top 10 funds ranked according to their level of volatility, which measures how much members are being rewarded for taking on the ups and downs in their balances.

Members in the Australian Retirement Trust’s Super Savings product had the least ups and downs over the past seven years and returned of 8.0% p.a. over the past 7 years. This was followed by Brighter Super and Aware Super with returns of 8.3% and 7.5% p.a. respectively.

End of financial year is a great time to check not just how your fund has been performing but also that your superannuation settings are still right for you. Making changes that reflect your current situation will truly pay off when you see the difference it makes to your retirement balance. It is usually worth checking if the investment option you are invested in remains suitable for your current lifestyle and risk tolerance, any insurance cover is at an appropriate level and cost and to make sure all your personal details are up to date. If you are unsure about what your settings should be, most funds have a range of tools and calculators on their websites to help you. You also don’t have to wait for your annual statement to find your current details, with most funds offering a range of communication channels including phone, online portal, chat and mobile apps.

When making a choice it may also be worth seeking some help. SuperRatings provides over 200 product ratings on its website and funds often offer advice services to their members either directly or through associated advice networks. Advice comes in a range of detail and cost so make sure you understand what services are available and how much they will cost before going ahead with the service. Alternatively, you can always contact your own trusted financial adviser to discuss your superannuation settings. If you don’t have one yet the MoneySmart website contains information on how to choose a suitable adviser.