What is the role of investment bonds and their role in the investment landscape?

Introduction

Tax-smart investing is one of the central pillars of quality, effective, financial advice. The capacity for tax to drag on investment returns, stifle compounding, and eat away at gains is substantial – especially in a highly taxed country like Australia – and applying the right strategies and structures can significantly amplify the growth of an individual’s wealth.

In Australia, superannuation has long been regarded as the pre-eminent tax-effective investment structure, allowing tax deductible contributions and concessional rates on earnings and withdrawals in retirement. But, as a vehicle for retirement savings, access restrictions mean advisers must also have other tax-smart strategies in their toolkit, for non-retirement wealth goals – such as education savings, or intergenerational wealth transfers. Additionally, the re-election of a Federal Labor government has ensured the introduction of Div 296 superannuation tax changes, which effectively double the tax paid on investment earnings for super balances over $ 3 million.

This growing need for tax-effective investment strategies outside of superannuation has seen advisers increasingly turn to investment bonds, spurring significant growth in the sector. But tax-smart investing isn’t just about lowering tax on earnings, it’s about considering the tax impact more broadly, in areas such as switches and transfers, estate planning and death benefits, policy risk, timing, and reporting and administration. In these areas too, advisers are finding reasons to embrace investment bonds as a powerful tax-smart structure.

In this article, we will take an under-the-hood look at investment bonds, and their role in the investment landscape – through a lens of tax-effectiveness. We will examine their features, use cases, and the ways they can meet a broad range of tax challenges faced by investors in Australia today.

Tax-smart investing as a core advice value-add

To the extent that tax can have a much greater impact on wealth outcomes than either management expenses or investment performance, it should be unsurprising that the selection of tax-effective strategies and structures is central to the financial advice value proposition.

Indeed, studies by both Russell[1] and Vanguard[2] concluded that tax-smart investing and planning was one of the most valuable benefits advisers delivered to their clients. Indeed, in quantifying the annual ‘alpha’ tax-smart advice at 1.3%, Russell’s 2024 ‘Value of an Adviser’ research concluded that optimising the tax treatment of investments added more value each year than asset allocation (1.1% p.a.).

In Australia, the tax-smart element of advice takes on extra importance due to the complexities of our tax system, and our relatively high personal tax rates, which sees personal tax account for a much bigger proportion of total taxation receipts than many other countries. In 2022 for example, personal tax revenue accounted for 40% of all tax revenue collected in Australia[3] – well above the OECD average of 24%. Furthermore, the spectre of bracket creep looms large, with some estimates suggesting one million Australians could face the top marginal tax rate by 2030[4] (triple the number of 10 years ago).

Defining tax-smart investing and core strategies

Tax-smart investing refers to selecting and structuring investments to minimise or defer tax liabilities while aligning with the client’s objectives, time horizon, and risk profile.

The core levers advisers can use within tax-smart strategies include:

- Minimising tax on investment earnings

- Selecting vehicles with capped or concessional tax rates.

- Minimising tax on withdrawals

- Using structures with tax-free redemption conditions (e.g., 10-year rule in investment bonds, retirement phase in super).

- Minimising tax on switches and transfers

- Avoiding CGT on internal rebalancing or ownership transfers.

- Minimising tax on death

- Using vehicles that pay tax-free death benefits to non-dependents.

- Reducing reporting/admin burden

- Selecting structures that remove annual personal reporting requirements.

- Optimise timing of taxable events

- Deferring of tax burdens until lower tax rates apply

- Minimising ‘policy risk’

- Diversifying the strategies used, to mitigate the impact of any government policy or legislative changes, as is seen frequently with superannuation.

While both super and investment bonds can be suitable to meet many of these challenges, the last challenge listed – to minimise exposure to legislative changes – has taken on increased importance recently with the proposed Division 296 changes to superannuation tax. It is within this context that adviser interest in – and usage of – investment bonds is experiencing rapid growth[5].

Investment bonds – tax benefits at a glance

The underlying legal structure of an investment bond is a life insurance policy with an investment component, issued by a life company or friendly society, and for this reason investment bonds are sometimes referred to as insurance bonds. But today’s offerings are certainly ‘not your father’s insurance bond’!

The key tax-smart features of an investment bond include:

- Earnings within the investment bond are taxed at a maximum rate of 30% (the company tax rate), but the effective tax rate can be lower through the use of franking credits and other strategies used by the issuer.

- They are tax paid investments, with no personal tax assessable income while the client remains wholly invested, and no annual tax reporting burden for individuals.

- No personal income tax is payable on withdrawals made after 10 years if the 125% rule is adhered to (see below for more details).

- Withdrawals can also be made within 10 years, on a tax-free basis for certain defined events (such as the death of the nominated life insured), or on a reduced tax basis between years 8 and 10.

- No personal capital gains tax when switching between investment options or making a withdrawal.

- They can be used to invest for the benefit of a child without minor tax rates applying.

- No tax on death benefits, even when paid to non-dependents.

- Flexible succession and estate planning features to control the transfer of ownership or future benefit payments without creating a taxable event.

Investment bonds – a closer look at the tax treatment

Because of the way investment bonds are taxed internally, they are often described as combining features of both insurance policies and managed funds. Through a combination of legislated tax concessions, and savvy portfolio management by the investment bond issuer, tax drag can be minimised at many points, amplifying the power of investment bonds as a tax-smart wealth building vehicle.

Tax-capped earnings

A maximum internal tax rate of 30% provides obvious relief for clients on marginal rates of up to 47%. Effective tax rates can be significantly lower – as low as 10-15% due to portfolio-level tax strategies such as franking credits and the tax-aware acquisition and disposal of underlying assets.

Tax-free withdrawals after 10 years

If held for 10+ years and the 125% contribution rules observed, withdrawals are completely tax-free to the investor, with no CGT, and no assessable income.

Uncapped access to tax-advantaged investing

Unlike superannuation, there are no caps on the amount that can be initially invested into an insurance bond. Investing millions or even tens of millions is allowable under current legislation. For each year after inception, you can then add up to 125% of the amount added the year before, without resetting the 10-year period.

Tax reduced withdrawals between years 8 and 10

On withdrawals made between 8 and 9 years after the investment bond inception date, only two thirds of the investment growth need be included in the holder’s assessable income. Between years 9 and 10 that drops to one third.

Tax offset of 30% and low-income earners

Any growth component received from an investment bond that is included in a person’s assessable income receives a 30% tax offset, reflecting the tax paid by the investment bond issuer. This can be particularly valuable for low income clients, as any remaining tax offset after accounting for the investment bond earnings can be used to reduce tax payable on other income.

Tax-deferred compounding

Because earnings are retained pre-personal-tax, the compounding effect occurs on a larger base, enhancing long-term after-tax returns.

CGT-free switching and transfers

Internal switches between investment options incur no personal CGT. Ownership transfers (including to minors or testamentary trusts) where no consideration are also free of income tax and CGT implications for the parties involved, and do not reset the 10-year clock.

Wealth transfer and estate planning

Minimising the tax burden left to others in the event of wealth transfers, including in the event of death, is a critical part of financial planning. Investment bonds can help avoid creating unintentional tax events and therefore work to ensure as much wealth as possible is transferred to the intended beneficiary. Unlike super death benefits, which are taxable when paid to non-dependents, or the winding up of estates or distribution of discretionary trusts – where the tax status of beneficiaries comes into play – investment bonds allow tax-free death benefits to any nominated beneficiary, as well as the ability to facilitate tax-free transfers.

Tax paid investments: why the big deal?

The ‘tax paid natures’ of investment bonds offer several valuable benefits to investors, some obvious, and some not so. The table below provides a useful summary of the strengths and considerations applying of tax paid and non-tax paid structures.

Use cases and case studies for investment bonds

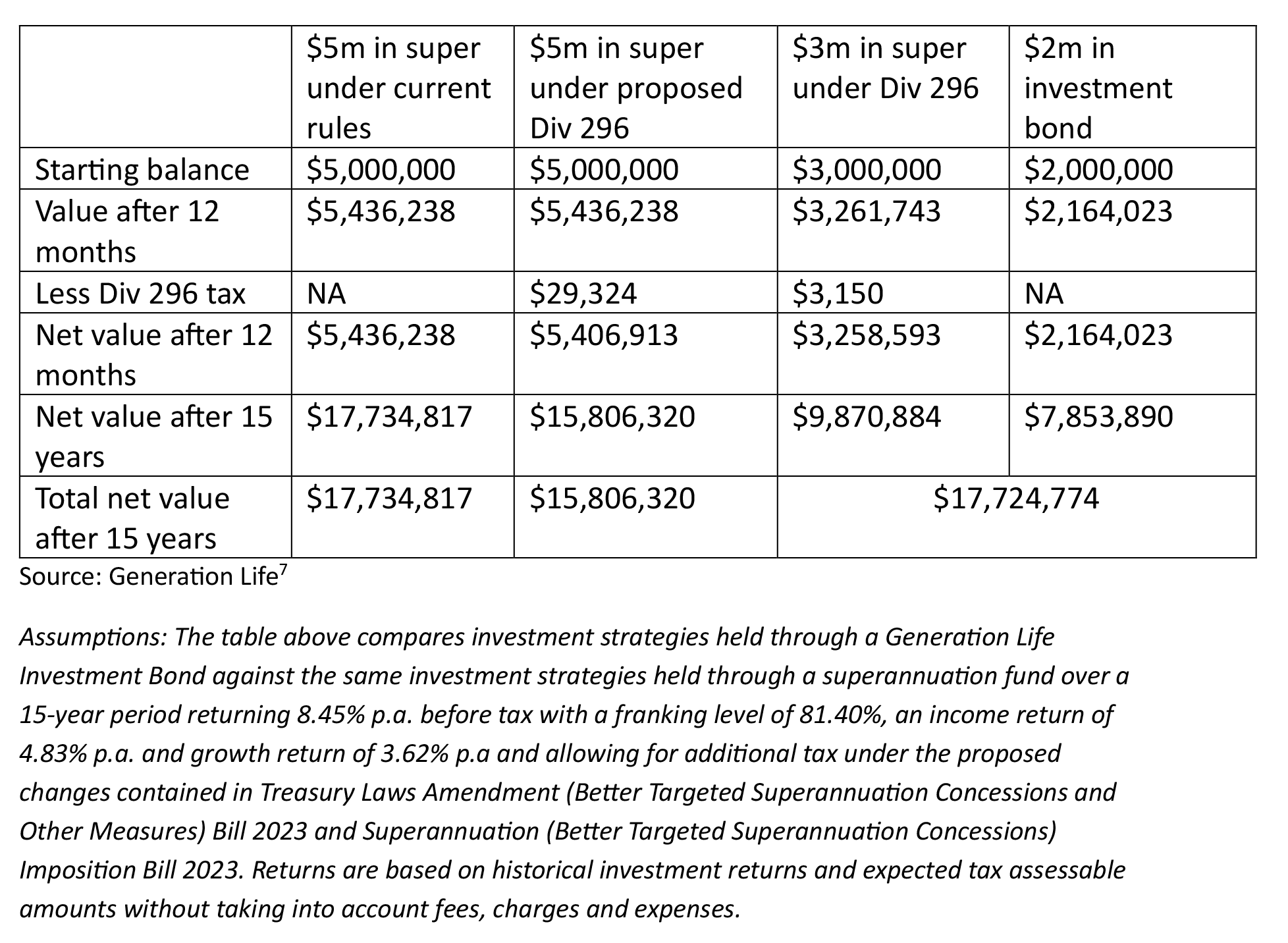

Use case 1 – avoiding the proposed Div 296 superannuation tax

Alex is a 64-year-old surgeon with $5m in her SMSF.

Under the proposed Div 296 changes, superannuation balances over $3m attract an additional tax on earnings of 15%, levied on the individual, and levied on capital gains even if they remain unrealised. Alex acts on the recommendation of her adviser to move $2 million into an investment bond.

Although the maximum tax payable on earnings within the investment bond is 30%, Alex chooses a provider and investment option with a historical rate closer to 10%, representing a significant saving on the 30% potentially payable under superannuation (15% + 15% Div 296 additional earnings tax).

An illustrative example of the outcomes can be seen in the table below:

Use case 2 – high-income earners reduce tax drag

A taxpayer on a marginal tax rate above 30% may achieve an overall higher investment value by using an investment bond and maintaining it for at least 10 years.

Max, a widower, is 81 years of age, a conservative investor and is ineligible to make non-concessional contributions to superannuation. He generates $140,000 investment income each year, including from a lifetime annuity which is indexed to inflation. The current level of income is above Max’s requirements. His financial adviser recommends investing a portion of his savings in an investment bond which will reduce his assessable income as investment bond earnings, while capped at 30%, can be closer to 10-15%, substantially lower than Max’s marginal tax rate (up to 39% including Medicare).

Use case 3 – low-income earners[8]

An investment bond that is cashed in earlier than the 8th year has the full amount of the growth assessable with a 30% tax offset available.

If a person (for example, a non-working spouse) has a marginal tax rate below 30%, any remaining tax offset after accounting for the investment bond earnings can be used to reduce tax payable on other income.

Investors close to retirement can use investment bonds as a means of deferring assessable income to a time after retirement, when their marginal tax rate may reduce.

Conclusion

At a time when legislative shifts can quickly erode once-reliable tax advantages, investment bonds stand out as a flexible and resilient pillar within a diversified, tax-smart investment strategy. Their capped internal tax rate, potential for effective rates well below the maximum of 30%, and the ability to deliver tax-free withdrawals after 10 years provide tangible, long-term benefits for a wide range of client circumstances.

Unlike superannuation, investment bonds impose no contribution caps and allow unrestricted access to funds, making them adaptable to evolving needs and market conditions. Their estate planning advantages – including tax-free death benefits to non-dependants and the ability to bypass probate – add another dimension of strategic value, particularly for intergenerational wealth transfer.

For advisers, the growing popularity of investment bonds underscores the importance of looking beyond traditional structures to protect and grow client wealth in a tax-effective way. By integrating investment bonds alongside superannuation, trusts, and direct investments, advisers can create more robust, policy-resilient portfolios that deliver stronger after-tax outcomes, reduce legislative risk, and support a broader range of client goals.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Tax (Financial) Advice (0.5 hrs)

ASIC Knowledge Requirements: Managed Investments (0.5 hrs)

please log in to start this quiz

———–

References:

[1] https://priority1.net.au/wp-content/uploads/2024/09/04fe234d-e856-4726-a8e4-8983bb8db6b6_AP0391_-_Value_of_an_Adviser_AUS_V1F_WEB_2408.pdf

[2] https://www.ch.vanguard/content/dam/intl/europe/documents/en/putting-a-value-on-your-value-quantifying-vanguard-adviser-alpha-eu-en-pro.pdf

[3] oecd.org/tax/revenue-statistics-australia.pdf

[4] https://www.afr.com/politics/one-million-australians-face-top-tax-rate-by-2030-20221005-p5bnao

[5] https://www.afr.com/wealth/superannuation/the-little-known-asset-class-set-to-soar-thanks-to-labor-s-super-tax-20250507-p5lx7b

[6] https://generationlife-endpoint.azureedge.net/live/attachments/cm3cwp71e1kw00qdx4orxgorz-generation-life-booklet-series-tax-aware-investing.pdf

[7] Ibid.

[8] https://www.mlc.com.au/content/dam/mlcsecure/adviser/technical/pdf/insurance-bonds-a-super-alternative.pdf

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Tax (Financial) Advice (0.5 hrs)

ASIC Knowledge Requirements: Managed Investments (0.5 hrs)

please log in to start this quiz