Investment Bonds can offer financial advisers a versatile, tax-efficient investment structure capable of complementing or substituting traditional vehicles such as superannuation and trusts

Introduction

Beyond Super: Why investment bonds are shaping the next era of wealth planning

For more than three decades, Australia’s superannuation system has been in near-constant motion. What began in 1992 with the introduction of the Superannuation Guarantee has since been reshaped by a rolling series of reforms, each altering the rules that govern how Australians save for retirement. From Simplified Super in 2007 to the Transfer Balance Cap in 2017, the pattern has been one of regular intervention.

The major superannuation tax policy changes recently announced by Treasurer, Jim Chalmers is only the latest example. While the measure appears to only target a narrow group upon application, it has reignited wider debate about the stability of Australia’s retirement-savings system and the need for broader, more flexible wealth strategies.

As a result, financial advisers are exploring tax smart strategies as tax and regulatory reforms may increasingly constrain wealth structures. With clients seeking alternative solutions for wealth accumulation and intergenerational transfers, investment bonds continue to gain strong momentum as one of the most flexible and tax-effective options.

Investment bonds present a compelling, tax-effective alternate or complement to superannuation and other investment vehicles. Governed by both Life Insurance and tax legislation, investment bonds combine highly tax-effective investment solutions with strategic flexibility, estate planning advantages, and diversity in investment choice.

Core uses of investment bonds:

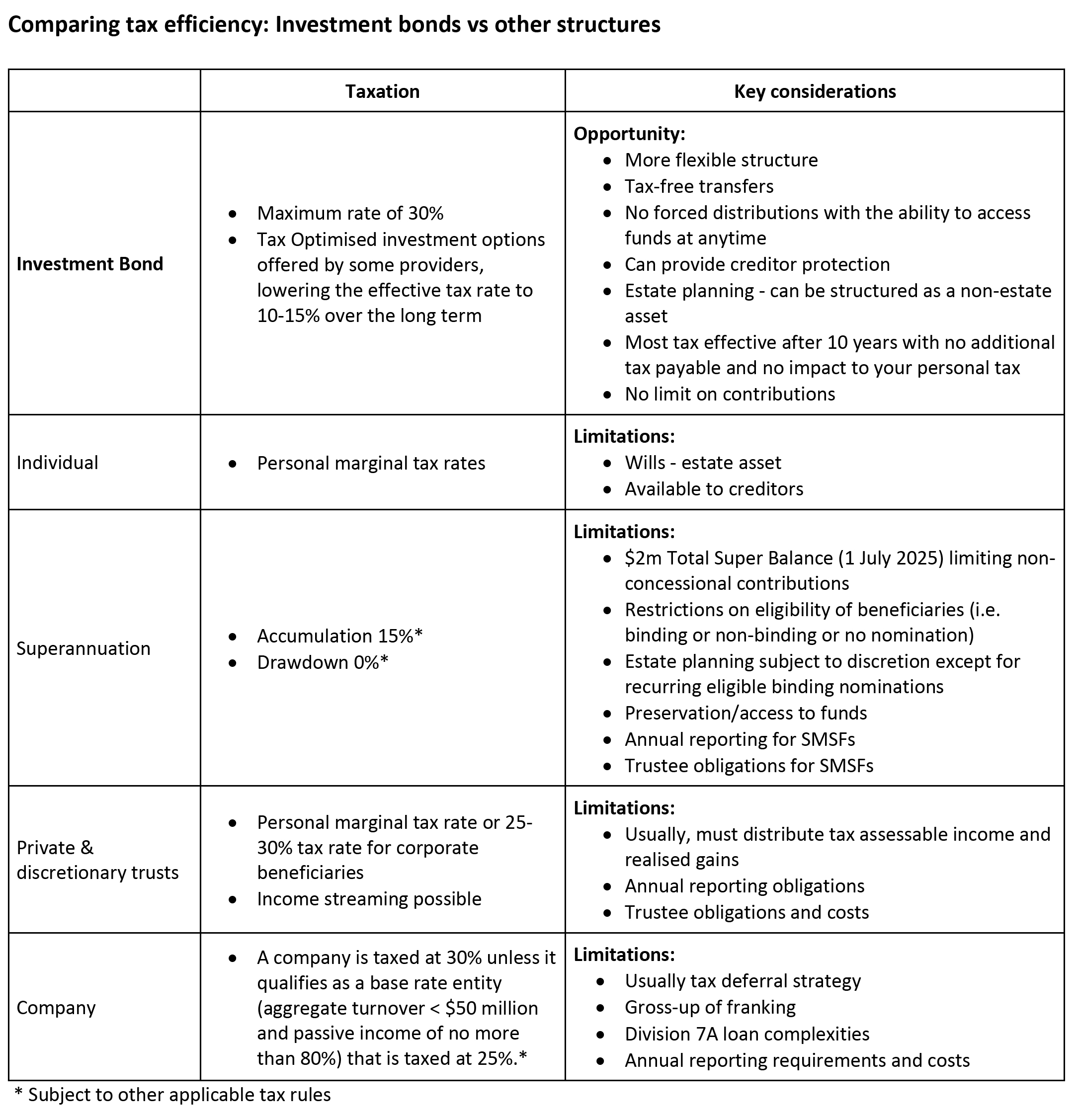

- Investing tax-effectively: All earnings are taxed at a maximum rate of 30%. The effective long-term tax rate can be significantly lower depending on the investment options you choose.

- Providing estate and succession planning flexibility and certainty: Transfer wealth to future generations tax-free and with certainty and peace of mind.

- Looking for an alternative to superannuation: There are no limits on how much and when you can contribute to an investment bond. Funds can be accessed at any time, you don’t have to wait until preservation age.

- Managing income levels in private trusts: Earnings generated by an investment bond are retained within the investment bond and need not be declared and distributed.

- Creating an income stream: You can create a regular income stream and there are no restrictions on when you can start the income stream – particularly useful if you are intending to retire early and access to superannuation is not available.

- Qualify for or improve social security benefits: To help manage or improve Government benefit entitlements in particular circumstances.

Legislative & structural overview

Investment bonds: defined

An investment bond is a tax-paid investment vehicle sometimes referred to as an insurance bond providing flexibility, control and access at any time. Investment bonds are offered by a life company structure, meaning they are subject to the Life Insurance Act and relevant tax provisions under the Income Tax Assessment Acts.

Investment earnings are taxed at a maximum rate of 30% within the investment bond. The actual effective tax rate may be lower as a result of the effective tax management practices implemented by the product issuers. No tax is paid by the investor on the investment earnings while they remain invested. Investors also have the flexibility to alter their investment options at any time usually without any switching fees or personal tax implications.

Investment bonds can provide access to a range of investment options to accommodate individual preferences and risk tolerances. Income and growth generated by an investment bond is usually not distributed to investors and held within the investment bond. This can help with managing personal tax assessable income levels and personal tax liability.

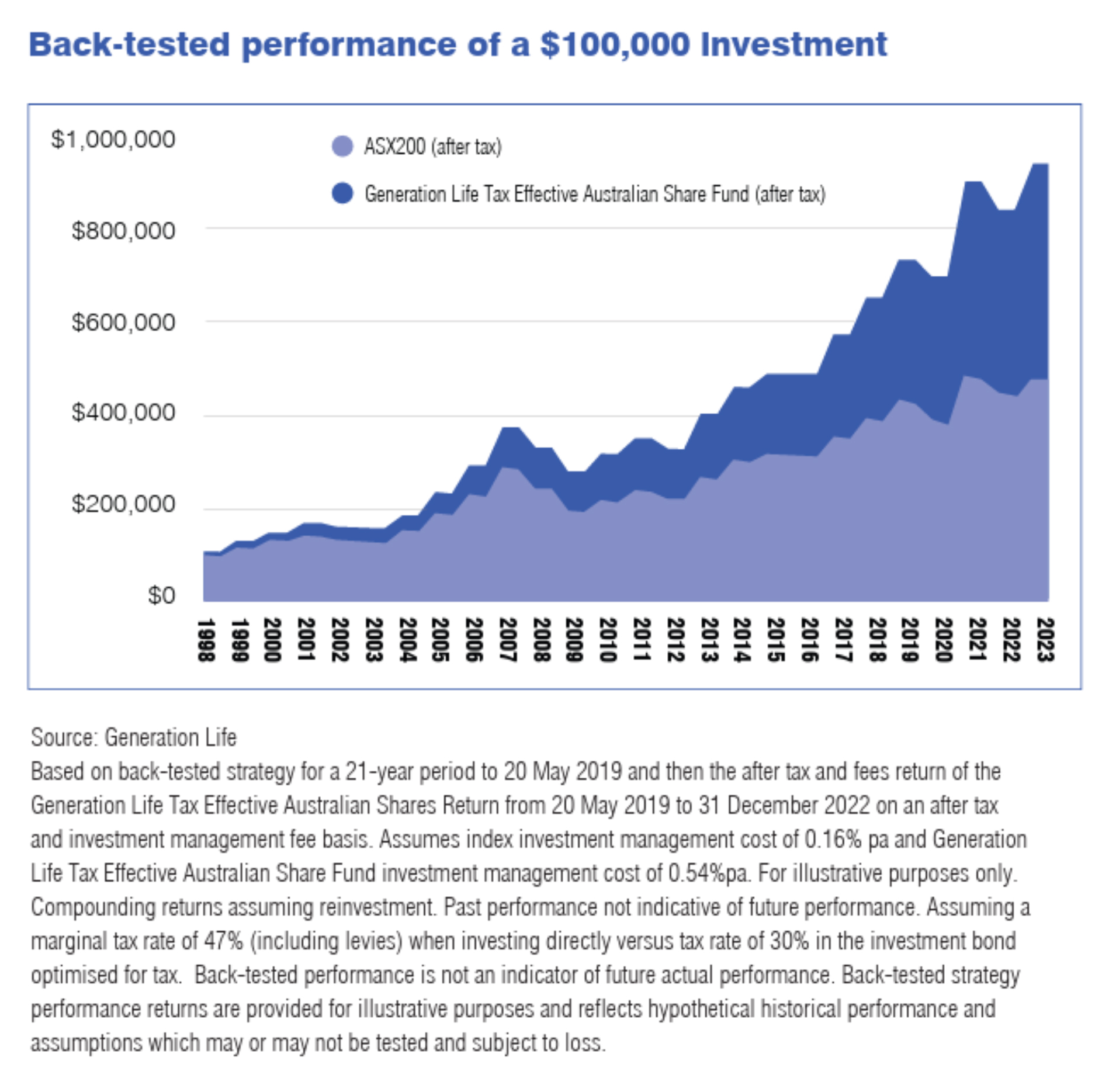

It’s for these reasons that investment bonds can offer a powerful, long-term tax-effective way to accumulate wealth for investors.

Consistent legislative stability

Investment bonds have enjoyed stability in their tax legislative framework having largely remained

unchanged since the tax rate was aligned to the company tax rate of 30% in 2001. This contrasts with superannuation, which has had over 30 major changes to its legislation and related government policies since the introduction of compulsory superannuation in 1992.

Superannuation remains a highly tax-effective way for most Australians to save for retirement, offering concessional tax treatment of contributions and favourable tax rates on earnings. But today, in light of potential superannuation reforms such as Division 296, Australians are reminded that complexities and constant changes often bring uncertainty – and that trusted advisers are essential in navigating both.

As legislation shows little signs of stabilising, it’s more important than ever to diversify financial and wealth accumulation strategies. Investment bonds, for example, offer tax advantages, flexibility, and estate and succession planning benefits, along with the track record of legislative certainty, making them a compelling option for those who may be impacted by the possible changing legislative landscape, both now and in the future.

Tax can be one of the biggest costs associated with any investment

Australian investment managers generally report on investment portfolios with a headline (pre-tax return) which does not necessarily reflect consumable returns in the hands of investors.

Investment returns and investment costs are two key factors that investors tend to focus on. But another critical factor is often overlooked – the impact of tax.

Tax is often the biggest cost for investors, and investors can feel very limited by the strategies available to reduce that cost. However, the impact of tax isn’t tomorrow’s problem.

How tax can erode returns:

An investor on the top marginal tax rate can lose up to 47% of portfolio returns to tax and Medicare.

As a guide, an investor who earns a pre-tax return of 5.0%p.a. on a managed Australian share fund may have their after-tax return whittled down to 3.1%p.a., even after allowing for dividend imputation credits.

In effect, 1.9% of the original before-tax 5% return – almost 40% – is lost to tax [1]

The compounding effect of this can be significant over time. Not being aware of the effects of tax can have a significant impact on your clients’ after-tax investment returns.

A tax aware approach to investing connects the dots and can reduce the impact of tax by pro-actively managing to reduce tax using a range of implementation strategies.

The reward for investors can be higher after-tax returns without taking on additional investment risk. As less tax means more to invest, the tax savings may compound over time, helping investors reach their financial goals sooner.

Investment bonds can provide a tax-effective solution to grow wealth, with tax on earnings capped at a maximum of 30%. Effectively, they can deliver improved after-tax returns with no additional investment risk.

Latest innovations in investment bonds

Investment bonds continue to deliver a tax-effective solution for building wealth through a range of investment options tailored to suit the investor’s objectives. But the opportunities go much further. Today’s investment bonds are using exciting new strategies to reduce the effective long term tax rate for many growth-oriented investments. In such a case, investors can enjoy the best of the five benefits below:

- A diverse portfolio spread across a variety of asset classes

- Enhanced after tax returns, deepening the benefits of compounding

- The ability to invest to achieve a variety of personal goals

- Access to their funds when needed.

Key tax benefits of investment bonds

1. Maximum tax rate of 30%

Unlike most direct investments — where assessable earnings for personal investors are taxed at their marginal tax rate plus Medicare levy — assessable earnings within an Investment Bond are taxed internally at a maximum of 30%. For clients in the 39% or 47% tax brackets, this represents an immediate tax arbitrage.

2. Effective tax rate reduction – tax optimised investment options

Through active tax optimisation of Investment Bonds, the effective long-term tax rate within some Bonds can be between 10% and 15% p.a. depending on the investment option(s) selected by the investor.

3. A tool against “bracket creep”

Earnings are taxed within the Investment Bond and held as otherwise distributable income that can accumulate.

Investment bonds can help shield clients from being pushed into higher brackets, by not distributing assessable income year-on-year. For clients worried about rising personal tax rates, this can help manage and improve after-tax outcomes.

4. After-tax investment outcomes and compounding returns

The returns from and performance of Investment Bonds are provided on an after-tax basis, unlike many other investments – such as managed funds, shares and term deposits – where the returns are often quoted before tax and are then taxable at your client’s marginal tax rate plus Medicare levy each year.

Over the long-term, the compounding benefit of a lower effective tax rate on earnings generated and retained within an investment bond can be significant when compared to direct investment options where the impact of the tax is generally incurred at a personal level annually, with less remaining to re-invest.

Analysis by one investment bond provider shows that an individual on a 47% marginal tax rate (includes Medicare Levy) can grow an Australian share portfolio by an extra 56% over a 20-year period when the long term average tax rate of investment returns can be lowered to 10%.

5. The 10-year advantage

If the investment bond is held for at least 10 years, withdrawals — including all earnings — are free from any additional personal taxes.

- The 10-year period starts from the investment’s commencement date

- Additional contributions of up to 125% of the previous year’s contributions can be made annually without resetting the 10-year period (the “125% rule”)

- Withdrawals before 10 years may result in an assessment of earnings, but these attract a 30% tax offset, to reduce any top-up tax liability.

6. Flexibility to switch at any time with no personal capital gains tax

Investment Bonds offer flexibility to switch between investment options at any time. Switching within an Investment Bond also does not trigger a personal CGT event. This is because the transactions occur within the investment bond’s tax structure, where the life company accounts for any realised capital gains.

7. Death benefits paid tax-free

Upon the death of the life insured (which is normally the owner, but can be another person), proceeds from the investment bond are paid tax-free to nominated beneficiaries — regardless of their dependancy status. This contrasts with superannuation, where non-dependants can face a death benefits tax of up to 17% (including Medicare levy) on the taxable component.

Additional benefits of investment bonds

- Simple tax reporting – There is no need to provide a tax file number, and no annual tax reporting is required while the investment is held. Furthermore, there is no tax reporting on a withdrawal provided you do not make the withdrawal within the first 10 years.

- Access to the investment at any time – unlike superannuation, an investment bond offers investors complete access at any time – you don’t have to meet any age or retirement requirements to access the investment.

- Protection from creditors – Similar to superannuation, if an investment bond is appropriately structured and owned by an individual and they or their spouse (including de facto spouse) are nominated as a life insured, the investment can be protected from creditors in the event of bankruptcy. This protection applies to the investment bond itself and can apply to proceeds from the investment bond received on or after the date of bankruptcy.

- Peace of mind for funeral expenses – A simple and tax-effective investment designed to help pay for future funeral costs, so to ease the financial burden on loved ones during their time of grief. Funeral bonds are also exempt from asset and income test (up to $15,750 as at 1 July 2025), which can help improve social security benefits.

Diversified strategies across multiple structures

The financial landscape is marked by constant change and growing uncertainty. Long-standing structures such as superannuation, family trusts, and other investment vehicles are increasingly subject to government review and reform.

Now more than ever, diversified strategies across multiple financial structures are critical. This approach not only helps mitigate the risks posed by potential legislative changes, but also provides much-needed flexibility, resilience, and control. As part of a broader diversified strategy, investment bonds are emerging as a powerful, tax-effective vehicle—particularly relevant in today’s financial landscape.

Managing distributable income in trusts

A private, discretionary or family trust can decide to reduce its distributable income if invested in an investment bond. Unlike other investments such as shares, managed funds and term deposits, an investment bond does not distribute taxable income to investors unless a withdrawal is made before meeting the 10-year rule requirement.

There are also no trust or personal capital gains tax consequences when modifying the trust’s investment strategy via an investment bond. While the trust remains invested in an investment bond, there is no annual taxable income in the hands of the trust that it must distribute.

The ‘125% opportunity’

Unlike superannuation where personal contribution amounts are capped and subject to penalty tax rates if exceeded, investment bonds provide much greater flexibility on how much can be contributed to the investment. There are no restrictions with an investment bond on the maximum amount that can be invested, unlike superannuation where the non-concessional contributions cap and the total balance cap limit investors’ abilities to make additional non-concessional contributions.

With an investment bond, there are no limits on the maximum amount that can be invested in the first investment year, which starts on the day the investment bond is set up. Each subsequent investment year starts on the anniversary date of the investment bond’s initial start date.

Each investment year, additional contributions of up to 125% of the previous year’s contributions can be made without re-setting the 10-year advantage period. This means that these additional contributions benefit from being treated (for tax purposes) as if they were invested at the same time as the initial contribution. They do not have to be invested for the full 10 years to be included as part of the 10-year advantage.

It is important to know that the 10-year advantage will restart if:

- no additional contribution is made in a particular investment year, and an additional contribution is made in any subsequent investment year.

Furthermore, if contributions in an investment year exceed 125% of the previous investment year’s contributions, then that is also possible, however, the 10-year advantage period will restart.

If a client wanted to make additional contributions but did not want to reset the 10-year advantage period on their investment, they could instead start a new investment bond. Alternatively, setting up an investment bond with a Regular Savings Plan and automatically increasing the regular savings amounts each year would provide a simple and effective way to automatically take advantage of the 125% opportunity.

Case Study: Comparing alternative tax structures[2]

John, 50, is a medical specialist, who given his profession, is subject to malpractice risk. He has surplus income of $50,000 per year after PAYG tax and his earnings put him on the highest marginal tax rate of 47% (including Medicare levy). He also has a super balance of over $3million and, if Div 296 is reintroduced and brought in, some super earnings would be subject to the additional 15% tax.

John recently received a $500,000 death benefit payment from his late mother’s super (after paying his share of death benefit tax). Due to John’s total super balance, he can no longer make non-concessional contributions into his super. He intends to continue working but would like the flexibility to access his funds before fully retiring. He also wants to reduce his working hours from after age 60.

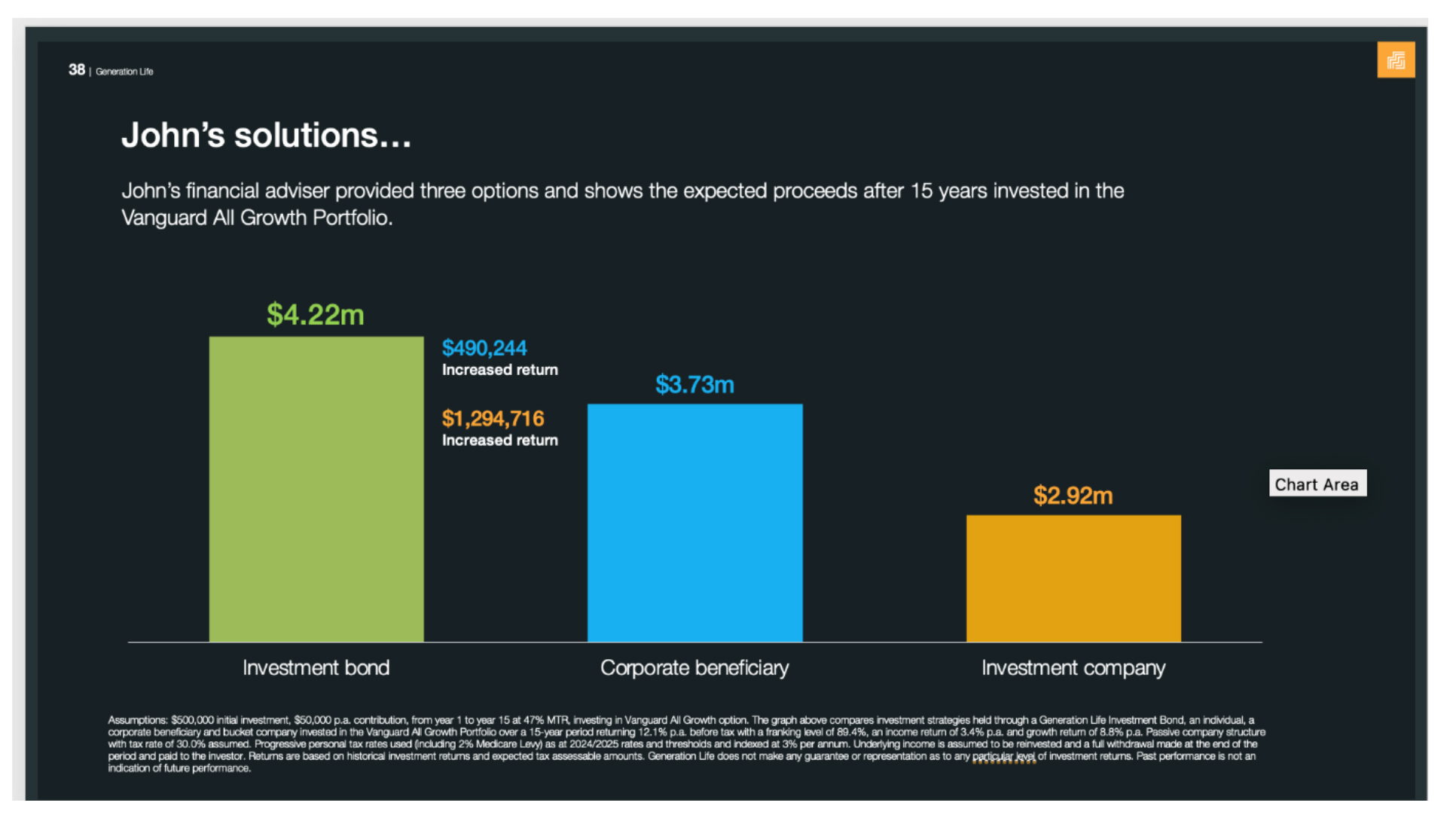

John’s financial adviser puts forward three options for John to invest his death benefit payment proceeds and surplus income in alternative structures. His adviser presents the options along with anticipated after tax proceeds after remaining invested for 15 years, about:

- Investment company = $3.02million

- Discretionary trust with a corporate beneficiary = $3.87 million

- Investment bond = $4.39 million

The numbers are compelling – the investment bond offers an increased return of $1.29 million when compared to the Investment Company and $490,000 more than investing through a private trust with a corporate beneficiary.

By investing in an investment bond, John has:

- The ability to access funds at any time for when he decides to reduce his work hours.

- A tax effective investment structure.

- Simple ongoing administration and monitoring with no set up costs.

- No potential Division 7A issues and requirements to manage that may otherwise arise when utilising corporate structures such as “bucket” companies.

- No deferred tax impact, often the case where corporate entities are used to hold investments.

- The benefit of the investment being protected from creditors in event of bankruptcy.

- The ability to set up the investment a non-estate asset, giving him flexibility in how and when to pass his wealth on.

The opportunity for John’s adviser is clear. Investment bonds provide a strategic and tax-effective solution that preserves flexibility and ensures access to funds at any time. While this case highlights the benefits of tax-effective investing, investment bonds can also deliver strong outcomes in other scenarios — such as intergenerational wealth transfers and estate planning.

Case study assumptions

Assumptions: $500,000 initial investment, $50,000 p.a. contribution, from year 1 to year 15 at John’s 47% MTR including Medicare levy). The graph above compares investment strategies held through a Generation Life Investment Bond, a family trust with a corporate beneficiary and John as the other trust beneficiary, an investment company invested an Australian and international share portfolio over a 15-year period. The returns assume a 12.1% p.a. total return on the portfolio( before tax) with a franking level of 89.4%, an income return of 3.4% p.a. and growth return of 8.8% p.a. Both the corporate beneficiary and investment company are taxed at a rate of 30.0% as a non-base rate entity for tax purposes. Progressive marginal tax rates for John are used (including 2% Medicare Levy) as at 2024/2025 rates and with other PAYG earnings indexed at 3% p.a. Underlying investment income is assumed to be reinvested and a full withdrawal made at the end of the 15-year period and paid to the investor. Returns are based on historical investment returns and expected tax components. Generation Life does not make any guarantee or representation as to any particular level of investment returns. Past performance is not an indication of future performance.

Conclusion

Investment Bonds can offer financial advisers a versatile, tax-efficient investment structure capable of complementing or substituting traditional vehicles such as superannuation and trusts. With capped tax rates, strategic withdrawal rules, and estate planning flexibility, they can provide prime and tangible after-tax benefits, particularly for high-income earners, retirees with large super balances, and families seeking certainty in wealth transfer.

As the debate about the stability of Australia’s retirement-savings system and the need for broader, more flexible wealth strategies continues, the role of investment bonds as an alternative is poised to expand — making it critical for financial advisers to master the technical details and strategic uses of these products.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Tax (Financial) Advice (0.5 hrs) and Technical Competence (0.25 hrs)

ASIC Knowledge Requirements: Taxation (0.5 hrs) and Estate Planning (0.25 hrs)

please log in to start this quiz

———

Notes:

[1] Case study source: Generation Life

[2] Stop your investment returns being consumed by tax, Generation Life 2020,

Disclaimer: Generation Life Limited (Generation Life) AFSL 225408 is the product issuer and provides general financial product advice and other services related to investment life insurance products and life risk insurance products. Any superannuation general financial product advice provided is by Generation Development Services Pty Limited ABN 14 093 660 523 (GDS) as Corporate Authorised Representative, No. 001317211 of Evidentia Financial Services Pty Ltd AFSL 546217 ABN 97 664 546 525 (Evidentia). The information provided is general in nature and does not consider the investment objectives, financial situation or needs of any person and is not intended to constitute personal financial advice. The product’s Product Disclosure Statement (PDS) and Target Market Determination (TMD) are available at www.genlife.com.au and should be considered in deciding whether to acquire, hold or dispose of the product. Superannuation products’ PDSs, offer documents and TMDs are available from the websites of their product issuers. Professional financial advice is recommended. Past performance is not a reliable indicator of future performance. Generation Life, GDS and Evidentia do not make any guarantee or representation as to any particular level of investment returns. Generation Life does not accept any responsibility or liability for superannuation general financial product advice provided by GDS. Generation Life’s investment bonds can provide certainty as they are governed by legislation that has changed infrequently and can be appropriately structured to bypass an estate and be protected in case of bankruptcy of the life insured. Investments carry risks.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Tax (Financial) Advice (0.5 hrs) and Technical Competence (0.25 hrs)

ASIC Knowledge Requirements: Taxation (0.5 hrs) and Estate Planning (0.25 hrs)

please log in to start this quiz———