Strong business culture is essential to maintaining an ethical advice practice.

A strong business culture has been identified as a critical attribute of an ethical business. This article, proudly sponsored by GSFM, investigates the interrelationship between a strong business culture and ethics in financial advice.

The relationship between ethics and business culture is deeply connected. Business culture is a defining force that shapes an organisation’s identity and guides its conduct, whatever the industry it operates in. The values, norms and behaviours embedded in a company’s culture are what hold the organisation and its people together.

In today’s hyperconnected, highly regulated and closely scrutinised environment, the focus on ethical conduct is greater than ever. Your colleagues, stakeholders, regulators and clients expect accountability, transparency and an unwavering commitment to doing what’s right. In this context, business culture acts as both the driving force and the testing ground for how values are applied in practice.

Organisational culture provides the foundation upon which ethical standards are built and sustained. This is especially true in financial advice, where clients place immense trust in professionals to safeguard their financial wellbeing, deliver on their objectives and ultimately help them to meet their future goals. In recent years, increasing attention on the ethical dimensions of advice has highlighted just how strongly business culture influences client outcomes and the broader reputation of the industry.

A global perspective of business culture and ethics

Several reports on ethics in the workplace have been published in 2024-2025. Two key reports were published by the Institute of Business Ethics, which was established in 1986 to champion the highest standards of ethical behaviour in business. Its Ethics at Work 2024 report[1] is based on a survey of over 12,000 working adults in 16 countries. From it and other similar reports published over the past two years, several common themes and issues emerged. These include:

- A growing concern around AI, automation and emerging technologies: Many employees worry about misuse of AI, potential bias, replacement of human roles, and insufficient organisational readiness. This is especially pertinent in advice practices, in which ‘fintech’ has already disrupted many traditional roles through automation.

- Cultural disconnects: Senior leadership often claim high ethical behaviour, but this doesn’t always filter down; consequently, research finds that middle managers are less likely to behave accordingly. This can result in poor modelling for all staff and an adverse impact on business culture.

- Measurement & accountability gaps: Many firms that were surveyed lack robust ways to measure ethical culture, supply chain or third-party risk, real-time analytics and benchmarking.

- Employee well-being: The wellbeing and psychological safety of employees was noted as becoming more central as ethics issues. Stress, overwork, the growing concern around automation have been found to tie directly into misconduct risk and reputational risk.

- Regulatory change: Globally, there has been ongoing regulatory change and scrutiny, particularly in the financial services sector. Respondents noted an increase in oversight and greater prominence given to ethics culture in supervisory work.

Although these results arise from a myriad of businesses across industries and geographies, there are parallels with Australian financial advice businesses and the importance of business culture. Here’s how those global ethics and culture findings translate into clear parallels and lessons for Australian financial advice businesses.

1. AI and technology

There has been increased discussion about the use of AI across varied aspects of advice businesses such as reporting, client service and in some cases, investment selection and portfolio construction. As well as concern for job losses, thought must be given to the ethics of emerging technologies – are they to benefit the business or the client?

The uncertainty created by emerging technologies can adversely impact business culture, which in turn can affect the ethical frameworks that underpin the business. The same risks seen globally – potential for bias, loss of human judgement and lack of transparency – apply here.

Advice businesses must ensure technology enhances, not replaces, human ethical judgment. It is important to maintain rigorous oversight, explain algorithms in plain language to clients, and ensure data privacy and fairness are built into every system. ASIC and the Financial Planners and Advisers Code of Ethics (Code of Ethics) both demand informed consent, transparency and fairness – principles that should extend to digital tools.

2. Cultural disconnects: culture is more than compliance

The financial advice sector is not immune to toxic workplace behaviours that undermine ethical decision-making. A culture tolerant of bullying, cutting corners or discrimination corrodes professionalism and client trust.

Strong governance around how staff behave and not just what financial advice they give is critical. It is important to embed respect, inclusion and psychological safety in training, policies, and critically, for leadership to set the right example.

While principals and licensees often articulate ethical values, the message can weaken at the operational level where client-facing staff experience conflicting pressures. Middle management must be empowered and accountable for living the firm’s ethical values. Performance reviews should be linked to cultural and conduct outcomes, not just business targets. Ethical leadership should cascade consistently from the top through every adviser and support role.

3. Measurement and accountability: turn ethics into metrics

Many advice firms rely on anecdotal or compliance-driven views of culture. Few track ethics performance in a systematic way. Consider the adoption of measurable indicators to monitor culture. These could include staff engagement, complaint resolution rates, compliance audit outcomes and client trust scores. Regular surveys and benchmarking can make ethics tangible and manageable.

4. Employee wellbeing: ethics starts with the individual

Burnout, excessive compliance pressure and the fear of making mistakes can create an environment where ethical lapses and poor decision-making thrive. A business culture that promotes good mental health, balanced workloads and open communication creates a healthy work environment.

It’s important to encourage staff to raise ethical concerns without fear. A healthy, supported team – from advisers through to support staff – make better ethical decisions and build stronger, trust-centred client relationships.

5. Regulatory change – it’s inevitable!

Just as global regulators have the spotlight firmly centred on culture and non-financial misconduct, ASIC and Treasury continue to emphasise ethical standards in the advice profession through the Code of Ethics and Quality of Advice Review outcomes.

So, regulatory change can be expected to reach further than in the past. Assume greater scrutiny of culture and governance, as well as personal and business conduct beyond compliance checklists. Firms that proactively demonstrate a strong business culture maturity – through transparent leadership, client-centric outcomes and staff engagement –will be better positioned in the evolving regulatory landscape.

For Australian advice businesses, these parallels highlight that business culture and ethics is not peripheral. It is strategic infrastructure. Embedding ethics into leadership, systems and daily behaviours isn’t simply about avoiding regulatory breaches. It is about building resilient, trusted businesses that can thrive amid technological change, regulatory evolution and shifting societal expectations.

Ethics and financial advice

Financial advisers play a vital role in helping Australians achieve their financial goals. However, trust in the profession has been undermined over time by a small number of individuals engaging in unethical behaviour.

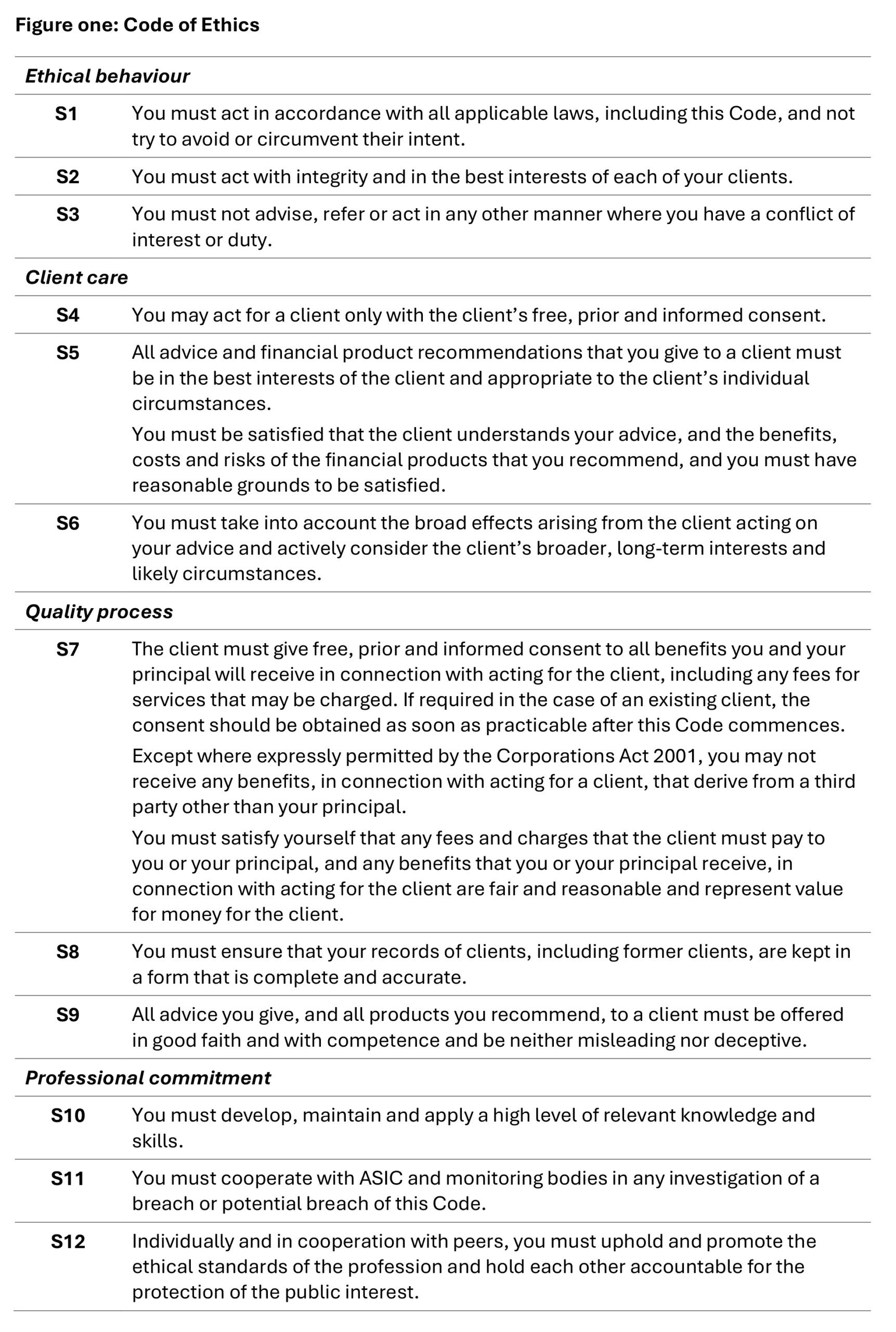

The Code of Ethics (figure one) is closely aligned with the legislation that governs the provision of financial advice. ASIC expects Australian Financial Services (AFS) licensees to take reasonable steps to ensure their authorised representatives comply with both the law and the standards set out in the Code.

To meet these expectations, licensees should:

- Ensure authorised representatives understand their ongoing obligation to comply with the Code.

- Provide training and guidance on the types of conduct consistent with the Code’s principles.

- Support advisers in raising concerns about how the licensee’s systems or controls may affect their ability to comply—and act on those concerns where appropriate.

- Monitor adviser conduct regularly to assess compliance with the Code.

- Update systems and processes as needed to maintain compliance with both the Code and the Corporations Act 2001.

Building a positive business culture in an advice business

The results from global surveys discussed earlier in this article have drawn clear parallels between a positive business culture and a business that acts ethically. Creating a positive business culture is fundamental to the success of any organisation, regardless of industry.

A strong culture creates an environment where employees feel valued, respected and motivated to perform at their best. This in turn drives productivity, strengthens retention and improves overall business outcomes. In sectors where ethical integrity is critical, a positive culture provides the foundation on which ethical behaviour and decision-making thrive.

Several key elements underpin a positive business culture: a clear sense of purpose and values, effective communication, recognition and reward, and opportunities for growth and development.

At the heart of any positive culture is a well-defined purpose and set of values. Organisations must clearly articulate their mission and core principles, communicate them widely and embed them into daily operations. When employees understand and identify with their company’s purpose, they feel more connected to their work, more motivated to contribute to its success and more inclined to act ethically.

Open, transparent communication is another essential pillar. This means fostering dialogue between employees and leadership, as well as among peers. When communication is clear and consistent, employees are more informed, engaged and comfortable sharing ideas or raising concerns. This openness is especially vital in ethical matters, allowing staff to seek guidance or question decisions without fear of reprisal.

The ethics centric advice practice

It’s important that an ethics-centred approach to financial advice should extend beyond the adviser. It should encompass everyone within the practice; from the receptionist who greets clients, to the administrator managing documentation, to the adviser developing financial plans and the paraplanner implementing investment strategies.

Every team member must understand how the Code of Ethics relates to their responsibilities and how they can uphold the Code in their daily work. By doing so, they not only support advisers and licensees to meet their obligations but also help safeguard the integrity of the entire practice. Ultimately, it is the licensee and adviser who bear accountability, and the consequences, if the Code of Ethics is breached.

So, how can advisers optimise their business culture and embed ethics at its heart? Listed below are twelve strategies that can be implemented to create an ethics-centric practice that can help support your business culture and mitigate the risk of breaching the Code of Ethics.

1. Define and communicate your company’s mission and values

This should be a clear and concise statement that outlines the purpose of your business and the values that guide it. It is important to state a purpose that goes beyond profit, such as “helping Australians achieve financial wellbeing with integrity.”

This is an opportunity to ensure ethical practice forms a key part of your mission and values. Values could include ‘Always put the client’s best interests first’ or ‘We help our clients attain their financial and life objectives by situating their interests front and centre.’ Clients and staff should hear and see these values consistently in your marketing, client and staff onboarding and internal messaging.

2. Code of conduct

A practice-wide code of conduct, one which encapsulates your business’s values as well as the Code of Ethics, should provide your team with a clear understanding of their role and set clear expectations about employee behaviour when performing that role. It should also detail how each of the Code’s twelve standards may specifically intersect their role.

3. Checklist

Create a checklist to be used to safeguard compliance with the Code of Ethics. The questions in the checklist should be tailored to each role within your practice and include those relevant to dealing with prospective, new and existing clients.

4. Client communication

It’s particularly important be transparent in your communications to foster openness and trust. Establish ongoing channels of communication and explain how you will communicate with them; it’s also important to detail the method and frequency.

Remember to not make promises you know you cannot (or may not be able to) keep. As well as potentially being a breach of the Code of Ethics, it will reflect badly on your practice.

5. Foster open and transparent intra-practice communication

This can be achieved through regular team meetings, one-on-one check-ins with employees, and other communication tools. Encourage team members to discuss issues that could potentially breach the ethical standards in the Code of Ethics.

6. Set key performance indicators (KPI)

Reinforcing your company’s values, adhering to your practice’s code of conduct and behaving in a way that makes ethical behaviour central to their work you and your team will create an ethical practice. Although a values-driven KPI may sometimes be more challenging to quantify than one with specific and measurable outcomes, it will highlight the importance of your company’s values and ethical practice to your business.

7. Workplace training

It is essential to make sure all staff understand both your values and the obligations of the Code of Ethics. You can use workshops to promote ethics in your workplace, which will reinforce the practice’s standards of conduct and clarify behaviours and practices that do and don’t work within your own code of conduct – and within the Code.

Importantly, ethics training should not be a once off and, as far as possible, should be practical. Training should teach team members to make good decisions that are compliant with the law (including the Code) and consistent with your practice’s values.

Ethics training could be incorporated as part of a regular team meeting; for example, by using case studies that address common ethical dilemmas across the financial planning industry. Cases could be drawn from the AFCA data base and discussed – how would your practice have dealt with situation that arise? You can also encourage team members to discuss issues arising with their clients, or something within your organisation’s processes or technology that might lead to a breach of the Code.

8. Feedback loop

Feedback is important. By encouraging staff to provide honest feedback about processes, conversations and client interactions, you are better placed to make sure you’re aware of issues that may arise that could potentially compromise your business. A feedback loop can help you identify gaps in relation to processes and procedures, and where a checklist or workplace training may ensure your business is not exposed.

9. Lead from the top

As highlighted in the findings from global ethics surveys, it’s important to set a good example for staff, irrespective of your position in a practice. Culture reflects leadership. If principals or senior advisers cut corners, staff and clients will notice.

For those who are senior in the practice, it’s even more important to demonstrate acceptable behaviour. Senior advisers and personnel will set the tone for ethics in the practice; as such, they need to demonstrate the Code of Ethics in their words and actions.

Mentoring and coaching is important here; you can pair junior advisers with leaders who emphasise integrity. Coaching should include ethics and emotional-intelligence modules, not just technical CPD.

10. Hire the right people

When hiring new employees, it is important to consider whether they share the same values as your business. Consider including some ethics-based questions into your interview; this could include client scenarios to see what actions your prospective employee would take.

Having the right people in your business will help support the business culture and ensure that all team members are working towards the same goals, that there is a strong sense of cohesion within the team and that your clients are prioritised.

11. Regular audit

These or similar strategies may have already been implemented in your practice. If so, it’s important to review the effectiveness of each. What’s working well and what’s not? If you can identify gaps in processes that may lead to a breach of the Code of Ethics, it’s better to identify them ahead of time, rather than when ASIC comes knocking on your door.

12. Encourage a good work-life balance

Employees who feel that they have a good work-life balance are more likely to be happy and productive in their work. A happy team member is more likely to be aligned with your values, support your business culture and work hard to support your business and its most important asset – your clients.

For financial advisers, an ethical business culture is a living system. It has a shared purpose, transparent leadership, rigorous governance, client-first practice, supportive workplace, engaged community, responsible technology and measurable progress. Implementing these elements not only satisfies regulatory standards but also creates lasting trust, a competitive advantage in a sector where reputation is everything.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from the Australian Financial Complaints Authority (AFCA) or ASIC. For each, potential breaches of the Code of Ethics are identified.

These case studies are representative of those that could be used as part of workplace training. An example of what the adviser did or did not do, why the client complained (or ASIC investigated) and the outcome. How would your team members have dealt with the situation? What would they do if they saw a colleague conducting themselves in a similar way? What are your business’s processes and procedures in such an event?

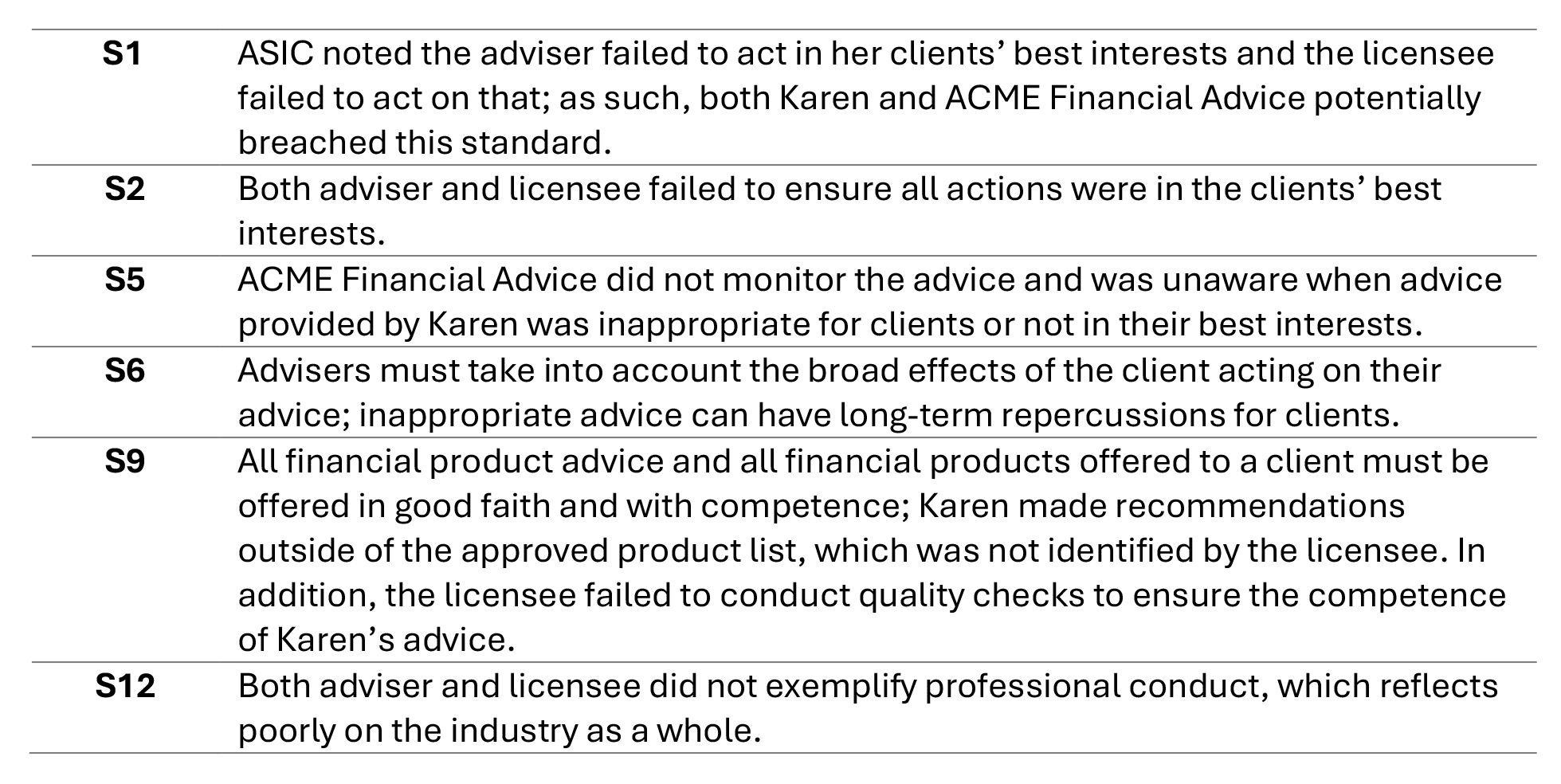

Case study one: Weak business culture and licensee failure

ASIC received numerous complaints about adviser Karen and instigated an investigation. The investigation found Karen had had frequently breached her best interests obligations by providing her clients with inappropriate advice and failing to put her clients’ interests first. At the time, Karen was an authorised representative of ACME Financial Advice.

When Karen’s case went to the Federal Court, it was found that ACME Financial Advice had received numerous complaints from clients, however they had failed to take appropriate action. In ASIC’s words, ACME Financial Advice failed to take reasonable steps to ensure that Karen had provided appropriate advice to clients, acted in her clients’ best interests and put her clients’ interests ahead of her own.

After hearing the case, the Court’s findings included that ACME Financial Advice did not have a strong business culture. Processes to monitor the advice given by advisers were inadequate, and the group failed to identify when their authorised representatives were avoiding advice quality checks or recommending non-approved financial products. There were also no steps taken by the licensee to monitor their authorised representative’s compliance with the Code of Ethics.

Commenting on the case, ASIC Deputy Chair Sarah Court said, ‘Financial advice licensees need to understand that they can be liable if their advisers do not act in the best interests of their clients and do not prioritise their clients’ interests over their own.’

Both ACME Financial Advice and Karen were subject to penalties arising from the case.

In this case, the licensee ACME Financial Advice and adviser Karen potentially breached the following standards:

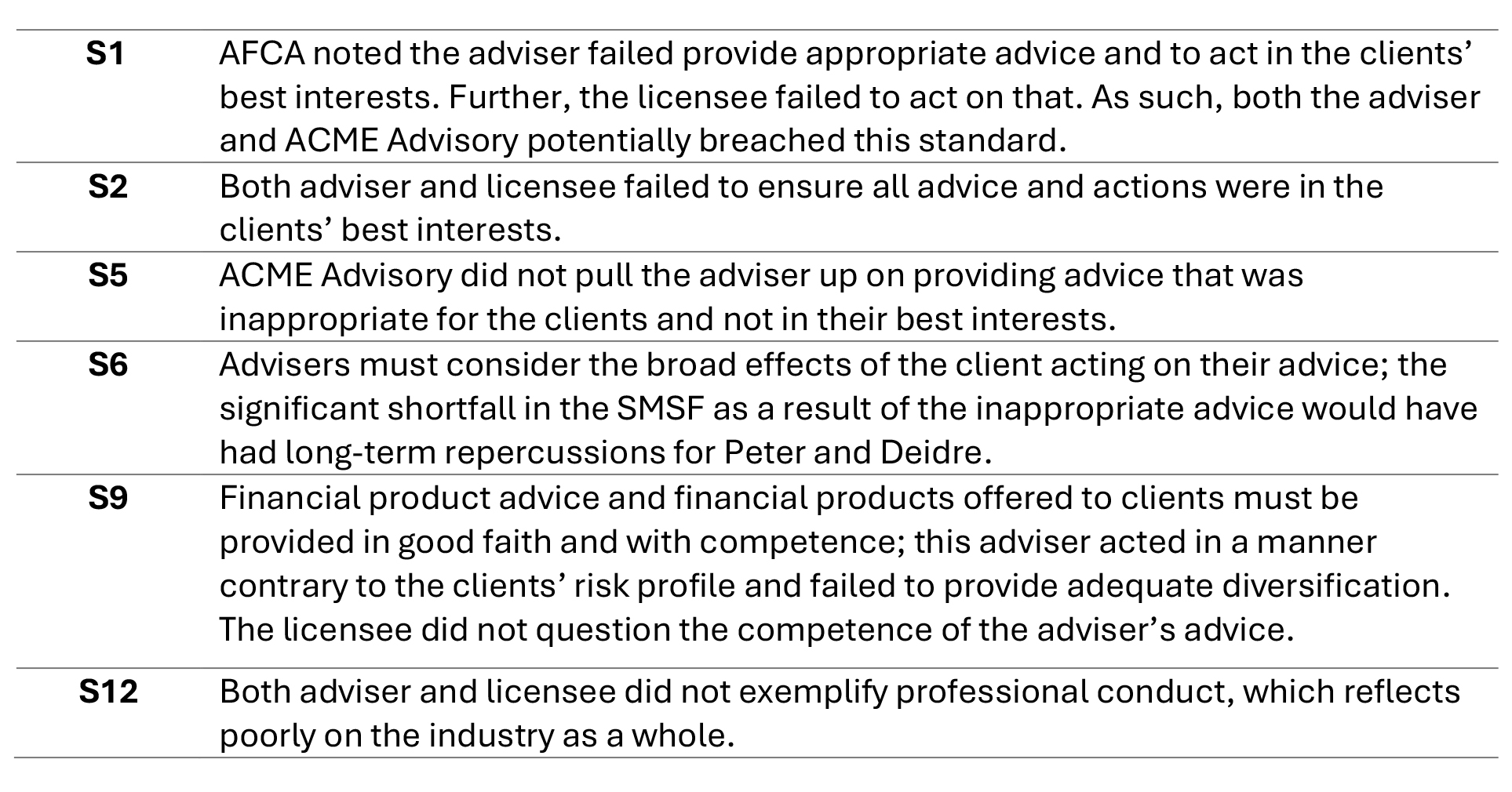

Case study two: Poor business culture results in poor client outcomes

AFCA has a large number of determinations relating to a single licensee. In this case study we’ll refer to it as ACME Advisory and examine a single determination. This particular licensee is a good example of a poor business culture, one in which clients’ interests were not prioritised and advisers not encouraged to necessarily act in clients’ best interests. The financial firm entered voluntary administration on in January 2022 and did not provide a response to the complaint.

Peter and Deidre lodged a complaint as trustees of their self-managed superannuation fund (SMSF). The complainants were clients of ACME Advisory from November 2009 to October 2021 during which time the financial firm provided them with investment advice for the SMSF portfolio.

The complainants say the financial firm’s advice was inappropriate during this period because it failed to diversify the portfolio according to the SMSF’s risk profile and was highly concentrated in a related party product.

AFCA’s finding was that ACME Advisory did not provide appropriate advice. As a result of its recommendations the complainants were exposed to a level of risk that was too aggressive for their risk profile and the SMSF portfolio lacked diversity. AFCA also noted that it shared the complainants’ concern about whether ACME Advisory adequately disclosed the risks associated with its related products and prioritised their SMSF’s interests ahead of its own.

AFCA found in favour of Peter and Deidre and note: “But for” the financial firm’s failure to provide appropriate advice, the SMSF would have been $1,016,175.80 better off.”

ACME Advisory was informed that it had to pay $1,016,175.80 to the SMSF or a superannuation fund nominated by the complainants plus interest on the above compensation amount equal to the change in the consumer price index from 1 July 2022 to the date of payment.

In this case, the licensee ACME Advisory and its adviser potentially breached the following standards:

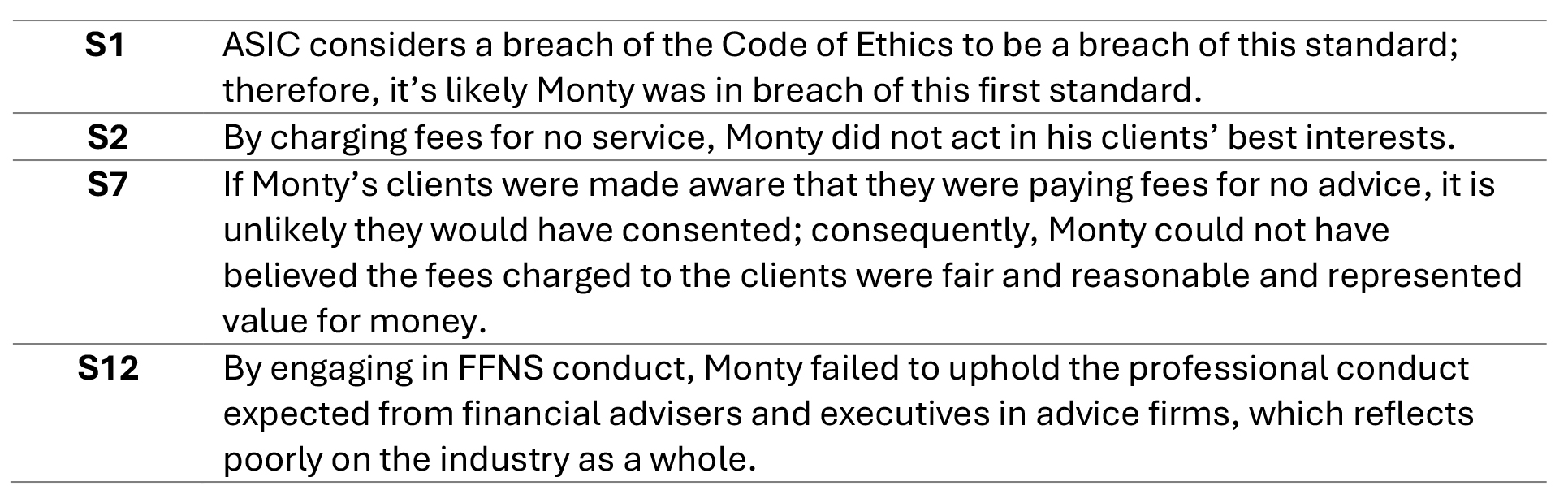

Fees for no service (FFNS) conduct was a key focus of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry that was held between 2017 and 2019. That business still engage in FFNS conduct suggests a poor business culture that prevails within the firm.

ASIC has banned Monty, financial adviser and director of ACME Advice in Brisbane.

ASIC found that ACME Advice engaged in FFNS conduct in relation to a number of clients between January 2022 and October 2023. During this period, Monty held executive roles in the firm, as well as being both a shareholder and financial adviser of ACME Advisers. ASIC noted that he became aware of the FFNS conduct but failed to adequately investigate the FFNS conduct, or to implement adequate systems to prevent it from reoccurring.

Further, ASIC also found that it had reason to believe that Monty was not a fit and proper person to participate in the financial services industry. A key reason for this was because as one of ACME Advice’’ shareholders, Monty “enriched himself at the expense of affected clients by failing to refund an estimated $81,652 in fees plus interest.”

Because of his actions, Monty has been banned for 10 years from:

- Providing any financial services

- Performing any function involved in the carrying on of a financial services business (including as an officer, manager, employee or contractor)

- Controlling an entity that carries on a financial services business.

In this case, adviser Monty potentially breached the following standards:

Case study four: Dishonest conduct

ASIC issued a permanent ban for financial adviser Finn. The regulator found that for a one-month period in 2023, Finn had made 37 unauthorised transactions on the trading accounts of his clients using an online trading platform.

During the same period, Finn also lodged seven hard copy investment instruction documents with the same trading platform. These documents contained forged signatures and purported to relay instructions to deal with financial securities on behalf of his clients.

The permanent banning follows Finn’s conviction earlier this year for engaging in dishonest conduct and providing financial services without appropriate authorisation. While he was sentenced to a total of 18 months’ imprisonment, he was released after entering a recognisance release order of $5,000. This required him to be of good behaviour for 18 months. He was also fined a total of $15,000.

As a consequence of his actions, Finn is permanently prevented from:

- Providing any financial services or engaging in any credit activities

- Controlling an entity that carries on a financial services business or another person who engages in credit activities

- Performing any function involved in the carrying on of a financial services business or in the engaging in of credit activities.

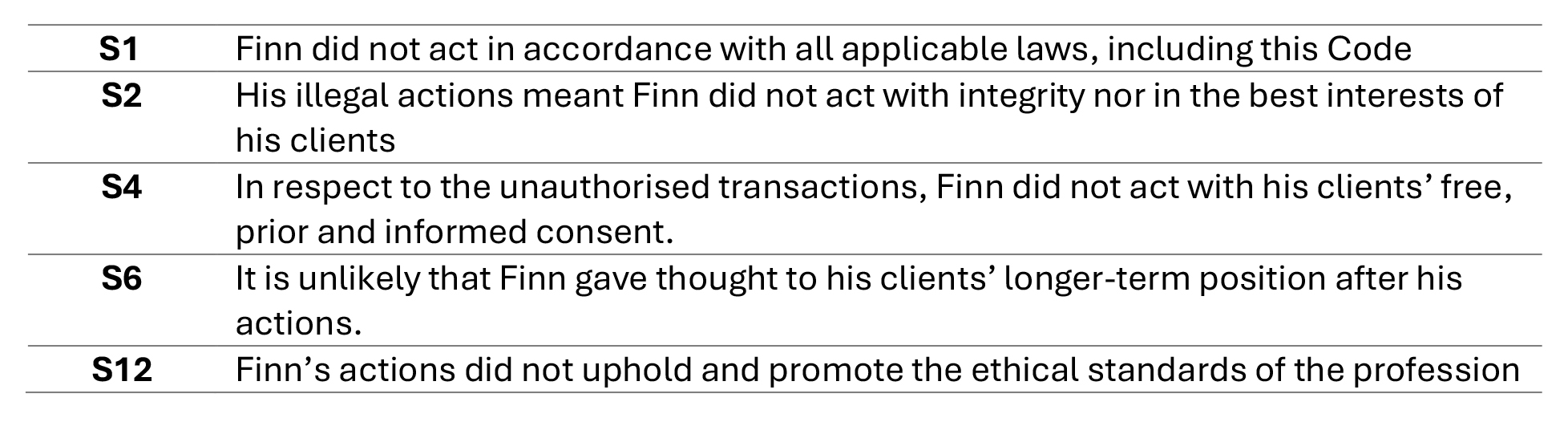

The action taken by Finn were illegal, unprofessional and potentially breached the following standards of the Code of Ethics:

The lessons from global ethics research are clear: culture is the backbone of ethical, sustainable performance. For Australian financial advice firms, this means that integrity cannot be treated as an afterthought or a compliance exercise. It must be woven into leadership, systems, technology and daily client interactions.

As AI, automation and regulatory complexity reshape the profession, advice businesses that prioritise ethical culture – supported by psychological safety, transparent leadership and measurable accountability – will be better equipped to navigate uncertainty and build enduring trust. Non-financial conduct, diversity, wellbeing and ESG are not distractions from core business goals; they are now essential components of long-term credibility and client confidence.

A strong business culture can serve as a compass. It can steer staff through the complexities of ethical dilemmas and ensure that they consistently act in the best interests of clients. This alignment of values fosters a sense of accountability and responsibility. By investing in the development of a strong business culture, financial advice firms not only fulfill their moral obligations to clients but also lay the groundwork for sustainable success in an industry where trust is the most valuable currency of all.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

———

Notes:

[1] https://www.ibe.org.uk/ethicsatwork2024.html

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

———