Combining an asset ownership mindset with a systematic investment process has the potential to result in significant and sustained alpha generation and deliver positive outcomes for your clients.

Emerging markets (EM) are highly inefficient. Complicated governance structures, evolving macroeconomics and immature institutions result in elevated stock price volatility. This creates significant alpha generation opportunities, as well as challenges, for active investors in EM equity markets.

EM specialist Ashmore believes that companies with structural competitive advantages delivering growth are best placed to benefit from EM secular growth drivers, as well as being well placed to navigate economic and market drawdowns.

Furthermore, opportunities to generate alpha are amplified by the fact that EM companies are poorly researched, especially for their medium-term fundamentals. Consequently, businesses of enduring quality are often undervalued and trade at prices that fail to reflect their ability to sustain high returns over the long term.

The compounding power of quality and growth in EM

The three characteristics most important to selecting quality EM companies are:

- Sustained quality, companies with enduring competitive advantages

- Diversified growth, compounding through reinvestment

- Mispriced valuation, with mispriced medium-term fundamentals

The combination of these factors is best positioned to deliver a portfolio of EM equities that meets it investment objectives and investor expectations.

Sustained quality

Quality companies typically share four important characteristics.

- High and sustainable return on capital

-

- Superior returns can be eroded by competition over time. Only a small number of companies have structural competitive advantages that can sustain high returns on capital.

- High returns can arise for a short-term period during industry or macro upturns. However, only few companies sustain their strong returns through cycles; the path to successful investing lies in identifying them.

- Strong predictable cash flow generation

-

- This provides the foundation for a company to be able to make the correct investment decisions over a cycle.

- Reported earnings can be subject to accounting presentation while cash generation rarely lies and ultimately determines the value of a business.

- Robust balance sheet

-

- This enables companies to improve their competitive position during a macro downturn. For example, they can invest in their brands, technology, distribution and growth while others are retrenching.

- Excessive leverage can lead to large negative outcomes for equity investors and can destroy even the best business models.

- Skilful management and non-financial factors

-

- Capital allocation provides the link between business value and shareholder value. Long-term orientated companies that understand and address material non-financial exposures to the benefit of all stakeholders can sustain and expand their competitive advantage.

- A skilled management team can continue to reinvest cash at high rates of return and grow the underlying earnings power of a business.

Identifying structural quality attributes requires an understanding of how a company achieves its attractive economic characteristics to ensure they are sustainable. Companies with high historic returns on investment capital (ROIC) can be identified though quantitative screens. However, one of the key determinants for future returns is a qualitative assessment of whether competitive advantages can be sustained or even improved upon.

Competitive advantages are distinct characteristics that are difficult to replicate and therefore enable super normal returns to be sustained. Sources of structural advantages usually comprise one of the following:

- Intangible assets: including intellectual property, licenses and brands.

- Cost advantages: driven by a proprietary process, superior scale or niche positioning.

- Network effects: a system’s value increases as the number of users expands e.g. as a social network or marketplace.

- Switching costs: products with high benefit/cost ratios where the risk of changing provider is high.

If a company’s management team allocates capital correctly, the company’s competitive advantage can expand as the company grows which leads to the potential for strong returns. Stocks can defy market expectations for competitive advantages to erode and ROICs to reduce to industry average, thereby creating the opportunity for sustained outperformance.

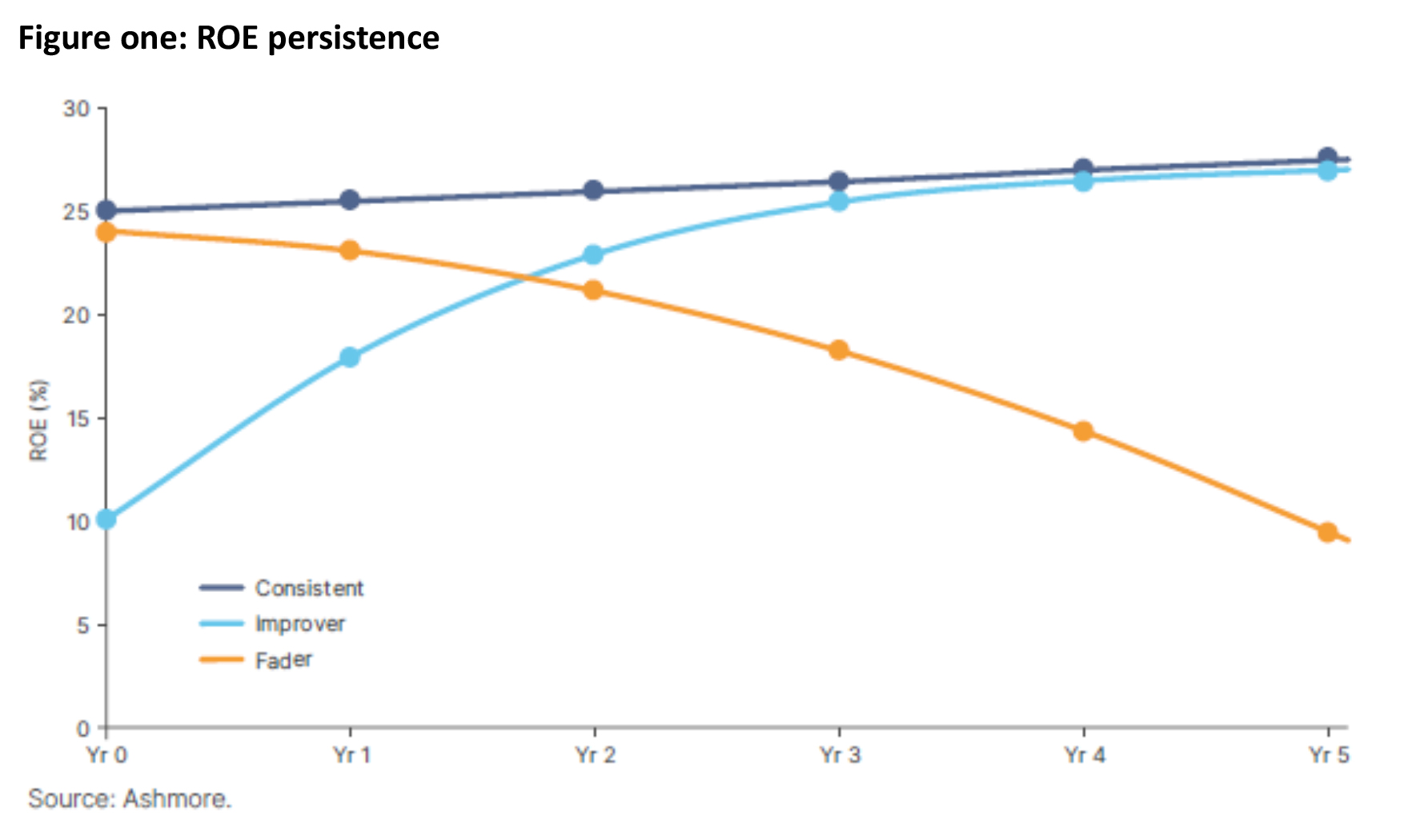

This positive effect is amplified for companies at an earlier stage of developing a competitive advantage. Consequently, focusing on companies with ‘consistent’, as well as ‘improver’, ROE profiles can often be well rewarded (see figure one).

Diversified growth

There are multiple factors to consider when targeting companies with durable growth characteristics. These include:

- Durable growth over high growth: many companies are predicted to generate high growth yet only a select few actually deliver. Consequently, identifying realistic and durable growth drivers is key, as is being selective.

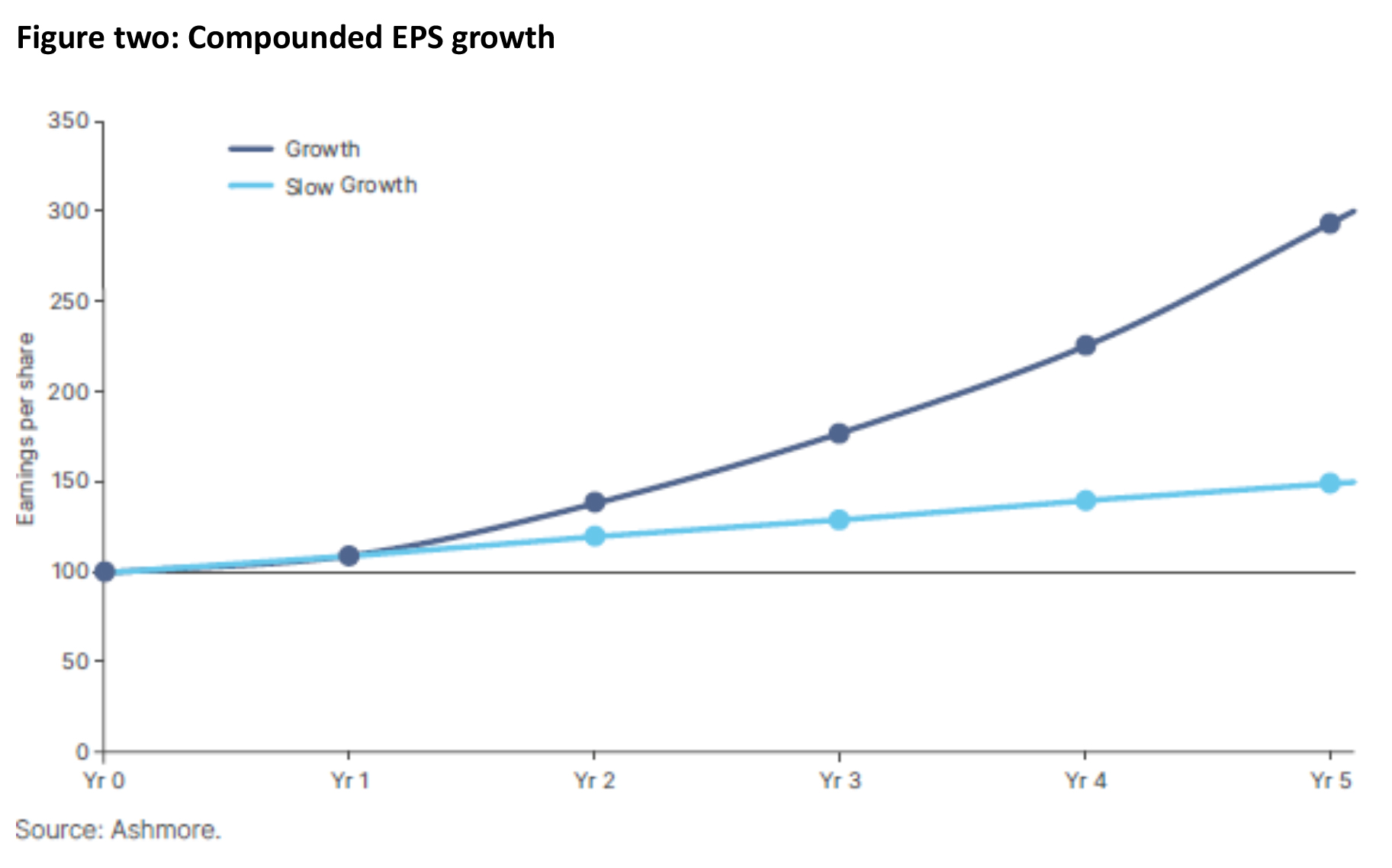

- Compounding growth through reinvestment: growth is most attractive when combined with quality as this enables a virtuous cycle whereby free cash flow can be re-invested at high rates of return. Taken in combination with a long runway for high return investment opportunities, this enables capital to be compounded over many years.

The power of compounding earnings is not perceptible in the short term. Instead, most shareholder returns are reflected via changes in earnings multiples. However, over the longer term, it is growth and compounding of cash flows and earnings that can lead to extraordinary returns.

- Preference for diversified growth drivers: Growth drivers can include price increases, entering new markets, new product development, cost reduction and operating leverage.

Cyclical growth that is driven predominantly by economic expansion and external factors cannot be relied upon. It is uncontrolled by management and can quickly disappear so requires additional analysis.

Growth driven by market share gains, product innovation and other initiatives is more durable as it is independent of the economic climate and is inherently more controllable.

- The perils of low growth: beyond a lack of compounding, limited growth opportunities can often be value destructive. It can lead management teams under pressure from shareholders to allocate outside their core competency.

- Timeframe and forecast error: while long term profitability attributes are targeted, our experience has been that the value of financial forecasting and its accuracy starts to diminish after a five-year time horizon, especially during periods of heightened technology disruption.

Mispriced valuation

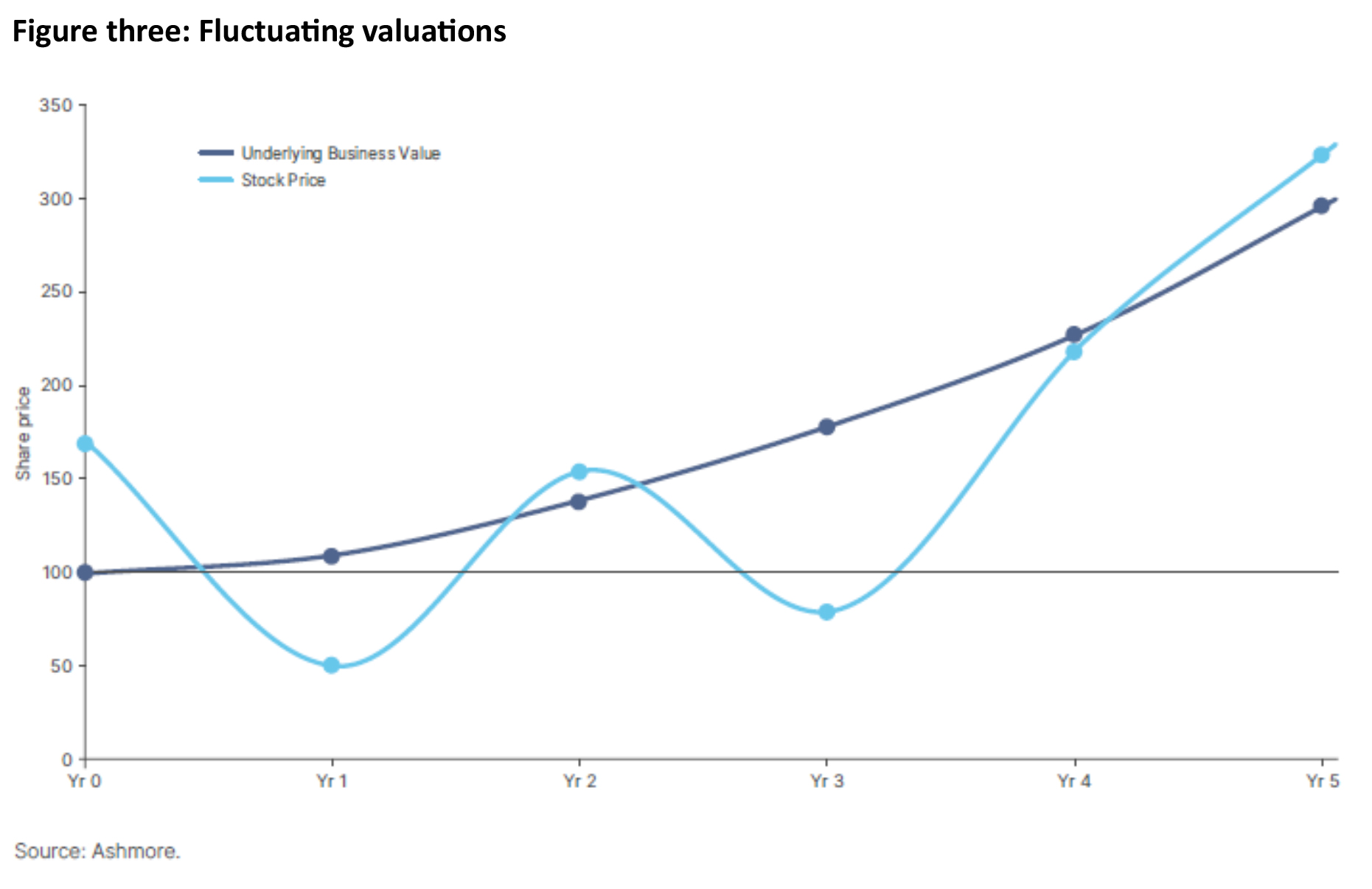

Valuation discipline is important, otherwise you could be paying for the next 3-5 years of shareholder returns upfront, which meaningfully limits the total returns you are likely to make.

We believe companies with high quality attributes over the near term often trade at a premium to the broader market. This reflects some expectation of short-term operational outperformance.

However, over the longer run, businesses that can sustain their quality attributes are able to exceed expectations by maintaining high levels of profitability. Stock prices typically discount high rates of return being competed away and thus systematically undervalue quality companies.

The strongest examples of quality businesses with durable growth prospects can be held over the long run, unless market expectations become excessive. However, the potential for forecast error means position sizes should always be adjusted to the upside available.

The importance of top down

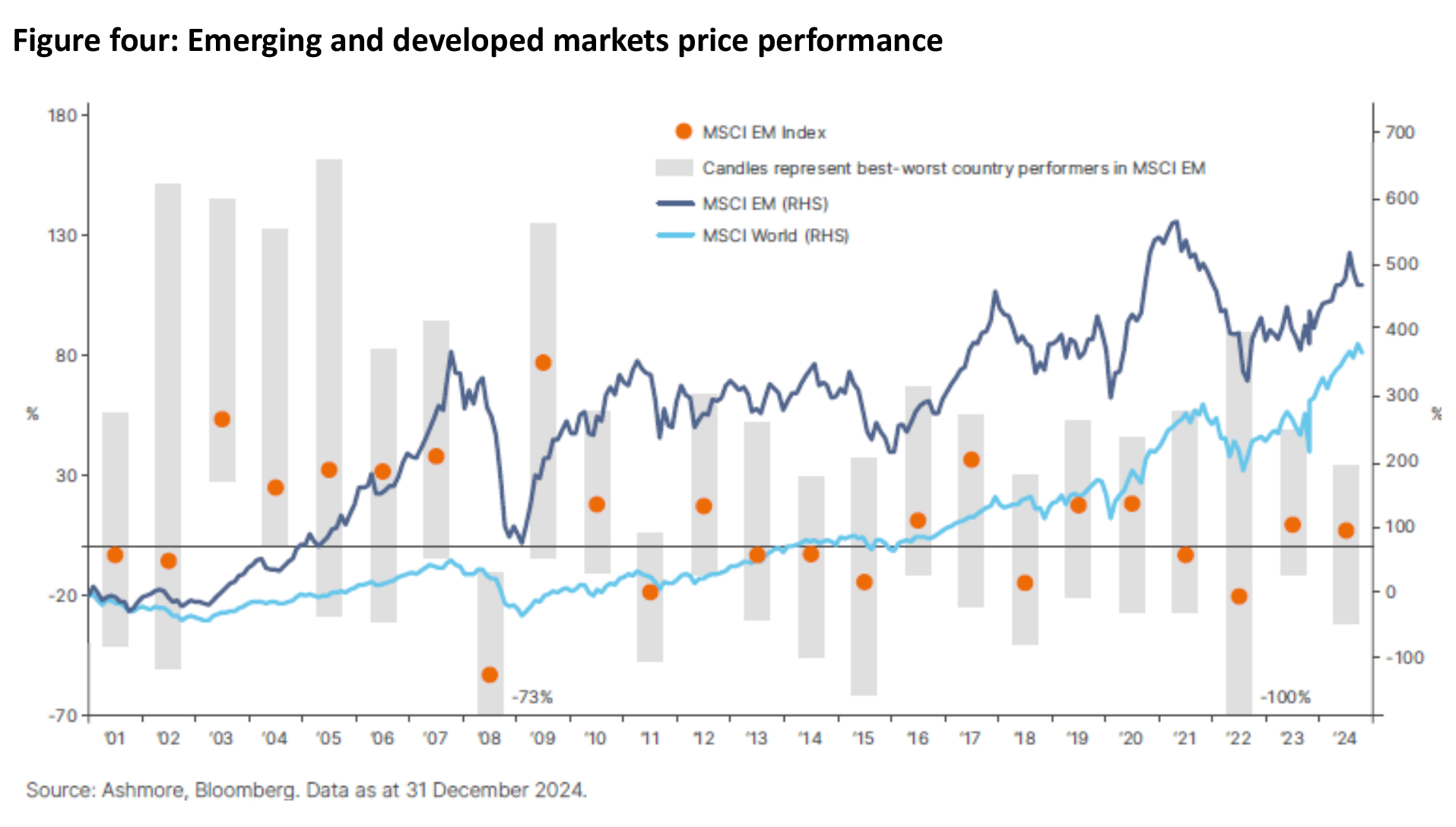

EM companies lead the world in a wide range of industries, yet they sit in economies with often immature institutions. The outcome is potentially higher stock returns but also the risk of macroeconomic volatility. This is highlighted by the significant dispersion in EM between best-to-worst country performance each calendar year (figure four).

Macroeconomic factors can, therefore, be the dominant driver of returns in the short term, often via currency impact and market multiples. Over the medium term, top down can impact a company’s operating environment and growth opportunity. Consequently, we believe an explicit assessment and integration of top down in our investment approach can help sustain alpha generation over the long run.

The use of top-down factors

By way of illustration, although Ashmore’s EM equity strategy is primarily driven by bottom-up fundamental conviction, top-down analysis plays three significant roles:

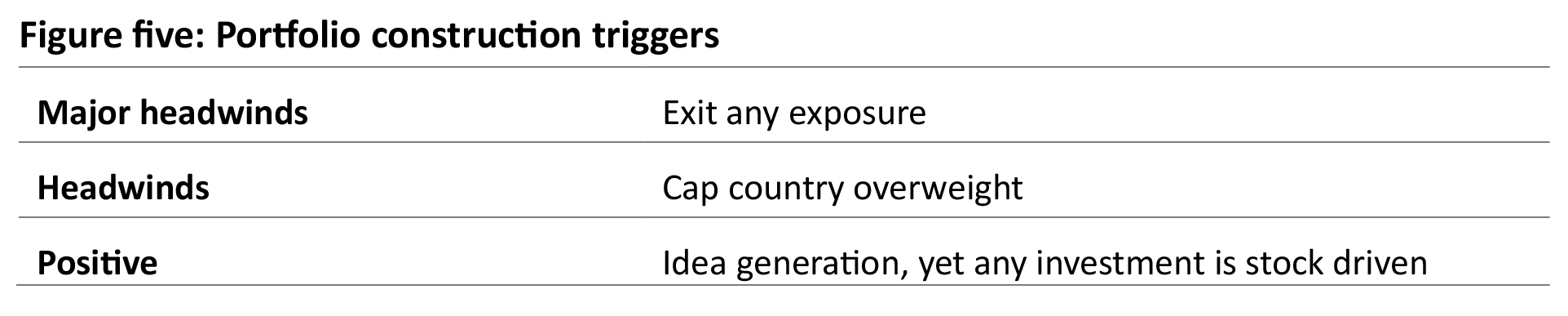

- A risk overlay which aims to mitigate major macro headwinds.

- To steer the portfolio away from economies facing headwinds.

- An idea generation tool attracting us to positive macro trajectories.

Further, Ashmore believes it is important to generate a proprietary team top-down view to ensure its alignment and full integration into the investment process. Each quarter the team scores countries formally, framed by a Country Scorecard. This assesses nearer team leading indicators, as well as longer term structural macroeconomic drivers, including institutions/politics.

Key top-down drivers that are assessed and scored include economic activity, the monetary cycle, fiscal accounts, external accounts, private debt and politics.

Drawing on Ashmore’s macro research, country analysis is undertaken by the member of the team responsible for stock research in that geography. This serves to frame the operating environment for their company research. Consistent macro scoring principles are applied to both short- and longer-term indicators to produce an overall rating, which impacts portfolio construction.

Case study: Country score examples

China: 2023-25

Score: Headwinds

This rating reflects a combination of poor corporate and consumer confidence weighing on activity. Together with an ineffective fiscal policy response, this is leading the economy to offset real estate pressure only modestly. Policy visibility has improved, and the private sector has seen support which has improved our conviction on select stock opportunities, but Ashmore continues to cap its China overweight until there is greater clarity over tariff risk and domestic policy.

Russia: 2022

Score: Neutral to Headwinds

In Q1 2022 Ashmore had a long-standing overweight to the market and a Neutral macro rating. It was then downgraded to ‘Headwinds’ due to rising tail risks of a war with Ukraine, which led to the overweight being meaningfully reduced ahead of the invasion. Ashmore did not go to a zero weight – i.e. ‘Major headwinds’ – as the team did not expect the invasion to materialise.

South Africa: 2022-24

Score: Major Headwinds to Neutral

In Q1 2022 Ashmore changed the rating from ‘Headwinds’ to ‘Major Headwinds’. The economy had many pre-existing challenges which ranged from poor infrastructure and weak institutions to emigration of the highly educated. Ashmore downgraded the rating given lack of political reform progress and crippling electricity blackouts.

The assessment has since improved following elections in May 2024 and the establishment of a coalition that includes the more reform orientated Democratic Alliance, as well as less pressure from electricity shortages. This led to a ‘Neutral’ view. The outlook remains uncertain, though, with limited compelling bottom-up opportunities.

Greece: 2023

Score: Headwinds to Neutral

In Q2 2023, Ashmore upgraded Greece from ‘Challenges’ to ‘Neutral’ on an improved economic growth trajectory, a reducing fiscal burden, deleveraging households and the re-election of an orthodox government with a pro-reform agenda.

——

At points of time in the cycle, top-down impacts can dominate and overwhelm stock returns, especially in US dollar terms. To successfully mitigate macro risks requires experience to understand policy scenarios, a wide breadth of vantage points to connect interrelated drivers, as well as a systematic framework to ensure consistency of assessment and an explicit impact on portfolio construction.

Differentiated outcomes

There’s a range of differentiators that EM investors can seek when making investment decisions. These include six differentiated outcomes prioritised by Ashmore:

Stock idiosyncratic

With a stock idiosyncratic approach, no single top-down, style factor nor stock should dominate portfolio outcomes. This ensures an EM equity portfolio is diversified across best stock ideas with capital allocation maximised by the prevailing rating discipline.

Importantly, a stock idiosyncratic approach should enable an EM equity strategy’s outperformance of the MSCI Emerging Markets index to be sustainable over the market cycle.

Portfolio active risk should evidence several stable portfolio attributes; namely a consistent, but not dominant, style underpinning of quality and growth attributes, and the disproportionate importance of stock idiosyncratic risk.

‘Sustained’ not ‘high’ quality

Companies with high historical returns on capital may appear attractive ex-post. However, those with sustained forward looking quality attributes have the potential to exceed market expectations by sustaining strong robust returns. Their resilience across economic cycles and varied business conditions makes their earnings power more dependable, which the market ultimately rewards.

The greater the predictability of a company’s earnings, cash flows, and management execution, the higher the valuation multiple investors are typically willing to assign. Moreover, companies that exhibit enduring quality often navigate market downturns more effectively, emerging stronger and gaining share from weaker competitors.

In short, a focus on enduring quality not only supports return potential but also enhances the portfolio’s overall risk-reward profile.

‘Diversified’ not ‘high’ growth

Investment in high-growth companies in EM is attractive given significant structural tailwinds, yet there are important further considerations.

A portfolio biased exclusively to high growth companies can make portfolio returns unstable and impede a manger’s ability to compound alpha. Style based momentum investing can also create market distortions.

Instead, investing in companies with a range of growth drivers enables the EM manager to take advantage of market dislocations and helps the portfolio navigate a range of market cycles. Growth categories include:

Rapid growers: firms experiencing strong, secular growth supported by long-term tailwinds.

Mid growers: businesses with dominant industry positions and high visibility of durable growth.

Cyclical growers: quality companies in cyclical sectors where near-term growth visibility is stronger, though longer-term visibility may be limited.

As an EM strategy moves through the business cycle, companies compete for capital. In the case of Ashmore, its disciplined rating framework causes exposure to each growth category to ebb and flow over time.

‘All Cap’

Ashmore believes that researching small- and mid-capitalisation (SMID) stocks can be particularly rewarding. When management teams allocate capital effectively, a company’s competitive advantage can strengthen as it scales, leading to the potential for exceptional long-term returns. This effect is often amplified in businesses that are still in the early stages of developing and enhancing their competitive edge.

An ‘all-cap’ approach to EM investing has proven accretive to alpha over time, with SMID companies frequently ranking among top contributors to performance.

Maximising capital allocation

There is greater potential for mispricing in emerging markets and hence valuation discipline has outsized importance. Ashmore systematically implements valuation discipline through its stock ratings which trigger the resizing of positions.

The most frequent driver of changes in position size is related to valuation, followed by a change in the growth profile of a company, and lastly by a quality reassessment. This reflects the inherent high volatility that is exhibited in emerging markets, even for high quality companies.

Performance over a cycle

By targeting investment in companies with sustained quality and diversified growth attributes which can be resilient to, and benefit from, the transformative economies that they operate in, an EM manager is better positioned to deliver positive investor outcomes.

The characteristics Ashmore targets are designed to enable EM equity strategies to mitigate permanent loss of capital risk but not at the expense of participating in strong market backdrops.

The manager does not seek to be structurally ‘defensive’, nor does it target the minimalisation of volatility as a strategy outcome. Indeed, it avoids low growth companies, such as telecommunications and utilities, despite them displaying low volatility characteristics. This approach reflects the risks of misallocation of capital as they attempt to grow, and since they forgo the attractive growth opportunity inherent in emerging markets investing.

Ashmore’s approach seeks to exploit episodes of market volatility systematically. Changing market expectations for company growth profiles, as well as market discount rates, can lead to sharp fluctuations in EM company stock prices. However, this has no bearing on the quality of the company, and Ashmore’s investment process systematically seeks to exploit such volatility underpinned by its rating discipline.

The importance of a valuation discipline means the firm is careful not to “overpay” for attractive growth. Finding such valuation opportunities can often coincide with market uncertainty around a particular company which can then be exploited. Typically, once the company fundamentals become clearer to the market, the volatility of the stock subsides, and investors are rewarded.

An EM equity approach that focuses on maximising investment returns over a cycle means that investment decisions, as well as primary evaluations, are made over this time frame.

One of the key determinants for future returns is whether a company’s competitive advantages can be sustained or improved upon. This enduring quality attribute is rewarded by the market over the medium to long term, although, over shorter periods, it may be overshadowed by economic or sectoral cycles, especially given greater macro volatility in emerging markets.

Advisers looking to include an EM equity strategy into client portfolios should look for experienced managers that focus on the importance of compounding earnings, the nature of which is evident over the medium term, yet less so over shorter-term periods.

By combining an asset ownership mindset with a systematic investment process, a quality EM manager is able to exploit mispricings in quality growth fundamentals dispassionately. This has the potential to result in significant and sustained alpha generation and deliver positive outcomes for your clients.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Managed Investments (0.25 hrs) and Securities (0.25 hrs)

please log in to start this quiz

———–

Important information: The information included in this article is provided for informational purposes only. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Ashmore Investment Management, PAN-Tribal Asset Management Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Managed Investments (0.25 hrs) and Securities (0.25 hrs)

please log in to start this quiz