Advisers need to understand how DDO applies beyond product issuers, the importance of aligning advice with Target Market Determinations, how to identify and report significant dealings outside the target market, and why robust documentation and governance are essential to meeting ASIC’s expectations under the DDO regime.

For legislation pigeonholed by many observers as being ‘all about product manufacturers’, the Design and Distribution Obligations (DDO) laws certainly have a knack of worming their way into financial advisers’ lives.

Recent ASIC ‘Stop Orders’ placed on the term accounts offered by one very high-profile local institution[1] didn’t just fray the nerves of investors, it caused grief for unsuspecting advisers and lead many to rethink their whole appetite for private credit. (It also reinforced that term accounts and term deposits are not the same thing, and that the distinction matters).

Go back just a short time and it can be seen, ASIC have also placed similar orders on the income fund of a local manager[2], and the disability insurance product of a well-known life insurer[3], both scenarios in which advisers may not have been penalised but were certainly impacted. Advisers were also likely reminded that – as distributors – they too have strict behavioural, procedural, and reporting obligations under DDO, the lack of adherence to which can result in penalties.

Throw in ASIC’s late 2024 report into distributor compliance with the legislation (and subsequent guidance tweaks) and it is clear that much has been happening on the DDO front, making it timely to revisit DDO through an adviser lens.

This article will give readers an understanding of the origins and purpose of the legislation, the impacts for advisers, a timeline on key events and subsequent changes, and a practical adviser checklist to assume ongoing DDO compliance and awareness.

DDO: a consumer protection gamechanger

Although disclosure is generally regarded as one of the key pillars of financial consumer protection, there has for some time been a recognition that an over-reliance on disclosure can be harmful to consumers, who generally lack the knowledge and bandwidth to comprehend lengthy disclosure documents and then make complex choices. This recognition was one of the catalysts for the game-changing DDO regime, which requires firms to take a consumer-centric approach to designing and distributing financial products.

Coming into effect in October 2021, the origins of the design and distribution obligations regime can be traced all the way back to the 2014 Financial Systems Inquiry, which proposed a ‘principles-based product design and distribution obligation’[4].

By the time the DDO legislation was eventually passed in 2019 (with an extended ‘phasing in’ period’), its form had been strongly inspired by the UK’s MiFID ii laws[5], which were designed to ensure financial products were only manufactured and distributed when they were in the best interests of consumers.

In simple terms, DDO is a continuous feedback loop

The theory underpinning DDO is relatively simple:

- Product issuers ensure they only manufacture products for whom there is a clearly defined target market

- That target market is formally articulated via a Target Market Determination, (TMD) document

- Similarly, articulating who isn’t in the target market may be appropriate, although this is not mandatory

- Distributors (including AFSLs and their authorised representatives) provide data to issuers that help them assess whether the product design – or the definition of the target market – needs to change, and

- Issuers, in turn, provide data to ASIC, for them to assess the appropriateness of products and product categories.

Direct impacts on Financial Advisers

From a practical perspective, DDO impacted AFSLs and Authorised Representatives in several ways, mainly centred around the use of TMDs and reporting to product issuers.

TMD requirements

- Ensure a valid, current TMD exists for every retail product before recommending, issuing, or arranging it.

- Understand and apply each TMD’s parameters, including the product’s intended consumer, risk tolerance, and distribution conditions.

- Integrate TMD checks into advice and compliance processes (fact-finds, paraplanning, file reviews, and CRM workflows).

- Cease distribution immediately if:

- The product has no TMD, or

- The TMD is withdrawn or subject to an ASIC stop order

- Dealings outside target markets

- Record any cases where a product is recommended to a person outside the defined target audience

- Reporting to the issuer (generally within 10 days of a pre-defined date)

- ‘Significant’ dealings outside the target audience

- Product related complaints

- Other distribution data as required by the product issuer.

Reporting burden becomes a point of contention

AFSL reporting requirements associated with the DDO added to extensive list of ASIC reporting requirements, including breach data and Internal Dispute Resolution (complaints) data, and unsurprisingly have been the subject of much criticism.

Furthermore, the vague guidance associated with some aspects of these requirements – the threshold for ‘significant dealings’ for example – further compounded the stress and workload for advisers and licensees, many of whom naturally err on the side of overcompliance.

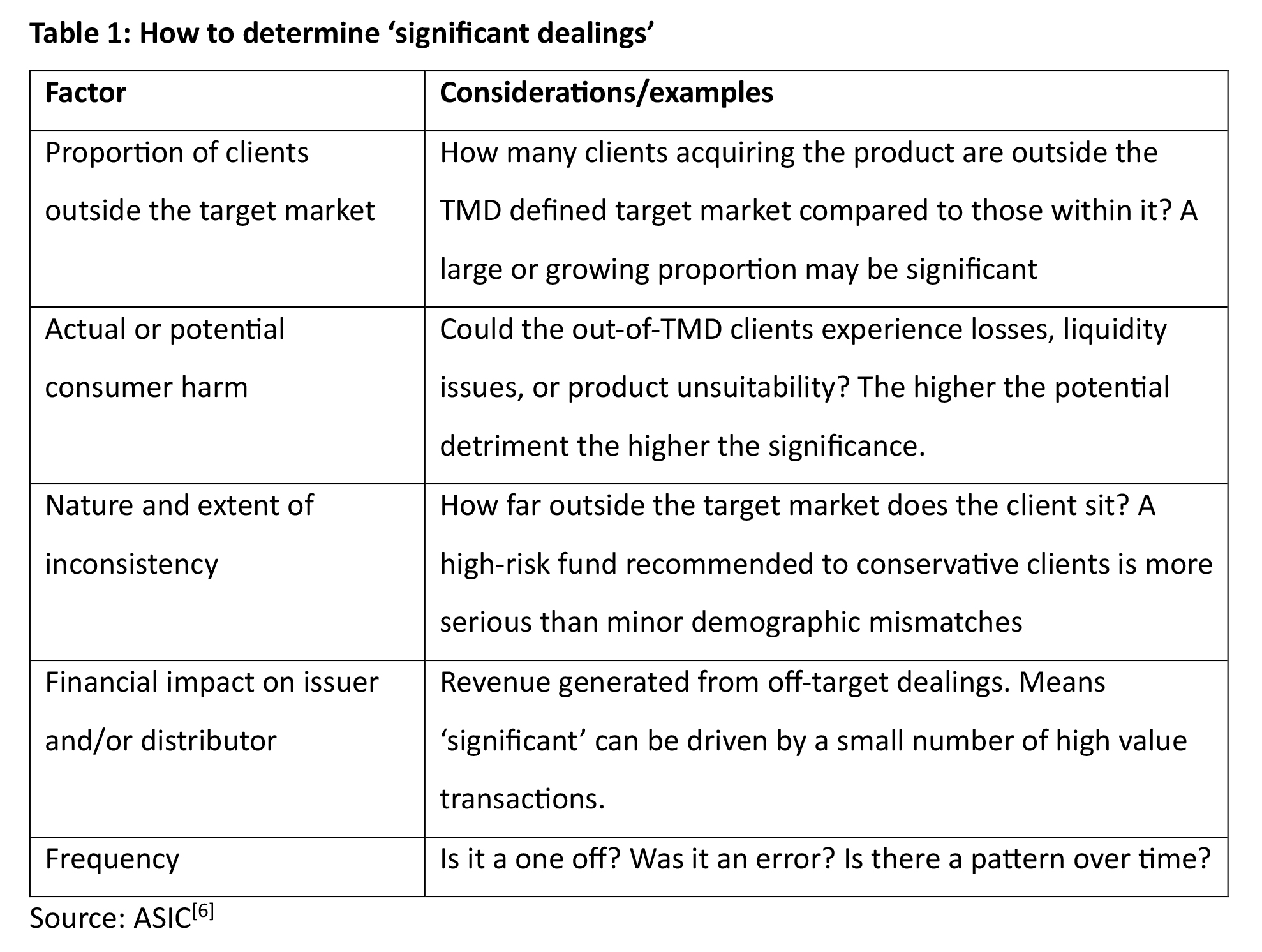

Significant dealings: when is significant really significant?

Neither the Corporations Act nor RG 274 define ‘significant’, with ASIC simply giving a list of considerations for advisers to weigh up in making this judgement themselves.

These considerations, from paras 160 and 161 of RG 274, are shown below:

Strong lobbying from the advice profession was successful in effecting change after the DDO legislation had been passed, when relief was granted (via ASIC instrument 2021/784) from the obligation for distributors to report to product issuers if they received nil complaints during a reporting period. ASIC consulted[7] on extending this relief in 2023, and at the time of writing it remained in place.

Michelle Levy also took aim at the requirements in her Quality of Advice Review recommendations[8], noting that product issuers, by specifying their own reporting needs, were effectively being allowed to impose legal obligations on distributors (including financial advisers) at will. Recommendation 12.2 proposed:

Amend the DDO reporting requirements in the Corporations Act to remove the requirement for relevant providers to:

- report significant dealings outside the target market to the product issuer

- comply with the additional reporting obligations specified by the product issuer in the target market determination, and

- report to the product issuer where there have been no complaints during the specified reporting period.

Unfortunately, this recommendation was not addressed in either Tranche 1 or 2 of the Delivering Better Financial Outcomes (DBFO) legislation (which dealt with most of her other recommendations) and so for the foreseeable future the reporting burden remains.

2023: ASIC releases its first report into DDO compliance

In May 2023, ASIC released Report 762, Design and Distribution Obligations: Investment Products, which found that there was “significant room for improvement” in DDO compliance[9].

At the time of publishing Rep 762, ASIC had already issued 26 interim stop orders, identifying several recurring themes in these actions. The most common included mismatched risk profiles, inappropriate investment timeframes or withdrawal conditions, overly broad target markets, and weak or absent distribution conditions. Some TMDs also suggested investors allocate excessively high portions of their portfolios to single products, raising suitability and diversification concerns.

To advisers, ASIC’s concerns were undoubtedly a red flag, a reminder about the need to conduct their own due diligence when assessing the underlying characteristics of a product, and its suitability for a client.

In other words, don’t solely rely on the TMD when matching clients to products.

2024: ASIC’s second report on DDO compliance

In September 2024, ASIC released its second comprehensive analysis of DDO compliance[10].

Report 795, Design and distribution obligations: Compliance with the reasonable steps obligation looked at 19 issuers of high-risk investment, insurance and credit products between October 2023 and August 2024.

A particular focus of this report was the distribution of products, including via advisers, with ASIC noting many issuers exhibited limited due-diligence and oversight of third-party distributors.

“Where personal advice was a selected distribution method, we observed that issuers took minimal steps to check customers actually received the advice before acquiring the product,” ASIC said in the report.[11]

“We acknowledge that in some circumstances an issuer will be unable to review the personal advice (e.g. if there are privacy concerns).”

This is despite issuers having clear guidance under Regulatory Guide 274 Product design and distribution obligations, ASIC added, that they can rely on a certification from the adviser that the client received current advice.

“However, we did not observe any issuers seeking such certification, although one issuer sought the adviser’s contact and AFS licensee details,” the regulator said.

The report recommended that issuers need to improve distribution practices, including in the selection and supervision of distributors (prompting concerns that issuers would hit advisers with further documentary requirements).

Overall, the report signalled that DDO oversight has moved from education to enforcement, with ASIC expecting demonstrable, data-driven assurance that distribution genuinely aligns with each product’s target market.

Following the release of Rep 795, ASIC also released minor updates to RG 274[12], including a strengthening of the ‘appropriateness’ requirement. ASIC revised this requirement to ensure product issuers had strong documented evidence showing they had applied an objective test when determining the appropriateness of the product to the target market. They further stipulated that this test could not be satisfied by simply including information in the TMD (as was previously allowed).

ASIC’s recent high-profile stop order puts distribution conditions in focus

Earlier in this article we mentioned how ASIC had placed a stop order on the high-profile issuer of a term account known to be very popular with advisers. Among the actions demanded by ASIC to lift the order were changes to the TMD, including:

- The addition of a distribution condition requiring investors to either receive personal financial advice, or to complete a questionnaire proving suitability, and

- The defining of a ‘negative target market’ (investors for whom the product was not suited.

Interestingly, and consistent with the concerns ASIC expressed in Report 795, it seems the issuer’s supervision of those distribution conditions was perhaps less rigorous than it could have been, as the AFR reported[13].

Does DDO ever come up in AFCA determinations against advisers?

AFCA determination 12-00-954693, handed down in August 2024, demonstrated that the complaints body does see the TMD as a critical reference point within the advice process[14].

The complaint arose after an adviser used their discretion under a managed discretionary account (MDA) to invest a retired couple’s SMSF in a small-cap growth fund that sat outside their agreed investment universe and risk profile. The fund’s TMD stated it was unsuitable for investors seeking income, and the clients’ SOA and objectives prioritised regular income and capital stability. When the clients later reviewed their portfolio and saw the fund’s volatility and limited income yield, they questioned how it aligned with their stated goals, leading to a formal complaint that the adviser had acted beyond their authority and outside the agreed parameters (the adviser claimed the investment was appropriate within the broader portfolio mix).

In finding in favour of the complainant, AFCA effectively drew a line between product governance and advice suitability:

- At the product (DDO/TMD) level:

- If the adviser had used the TMD as the basis for distribution, they would indeed have concluded the fund wasn’t suitable, since income-seeking clients fall outside the defined target market

- So, relying on the TMD would have led them not to invest in the fund (and doing so constituted an off-target dealing).

- At the personal advice level:

- AFCA accepted that, within the context of a diversified portfolio, a small exposure to a growth fund could still be consistent with the overall investment strategy and not cause financial harm

- However, there was still a procedural failure in that the adviser still acted outside the documented investment parameters and without updated client consent.

So, while AFCA found that within the context of the clients’ overall portfolio, the fund in question was reasonable – mitigating the amount of harm – this didn’t excuse the breach of authority by the adviser, and compensation was still ordered.

The takeout for advisers from this case include:

- The TMD governs product-level suitability, not portfolio-level advice

- Advisers must first ask: “Is my client inside the defined target market for this product?” If not, it may trigger a significant dealing report

- Even if, in portfolio terms, an exposure seems reasonable, you can’t override the TMD conflict without explicit client consent and an advice record

Productivity roundtable: Treasury to consult on simplifying DDO

In September 2025, it was announced[15] that ASIC had written to the Treasurer, nominating the DDO as one of the areas worth exploring in terms of bolstering productivity and economic growth. The letter noted that, in addition to ongoing discussions with Treasury about changes to the reportable situations regime, “other law reform ideas that have been raised… include reforms to the design and distribution obligations, product disclosure requirements, and simplification of the liability regime in the Corporations Act.”

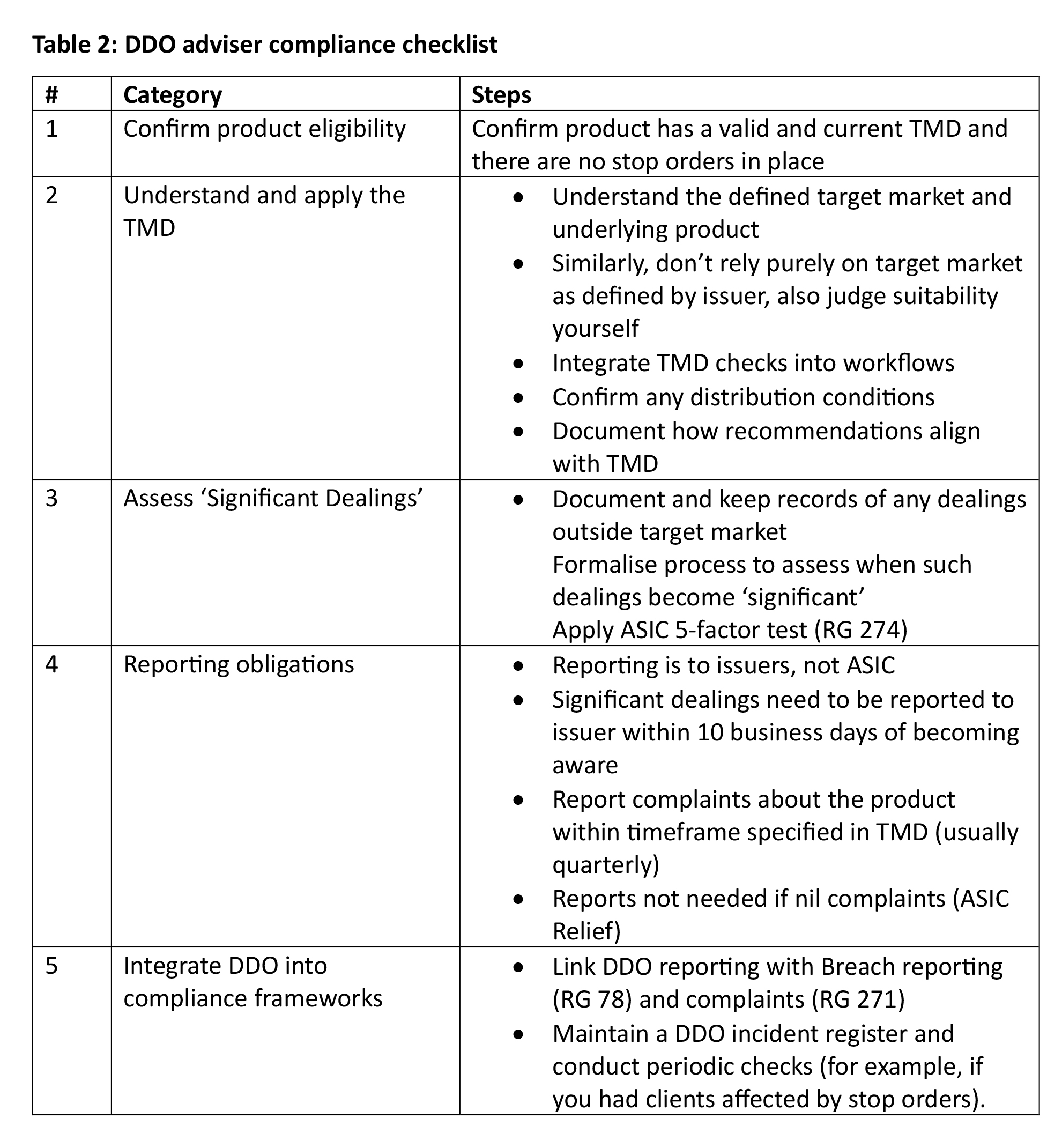

A practical checklist for adviser/licensee DDO compliance

Advisers are all too familiar with the glacial pace of legislative change, and so in the meantime must continue to comply with DDO laws as they currently stand. In this context, the checklist below may prove a handy reference point:

Summary

The article explores how the DDO regime, rather than purely targeting product manufacturers, is a critical area of compliance for financial advisers. It traces DDO’s origins from the 2014 Financial System Inquiry through to its 2021 commencement, explaining its goal of ensuring products are designed and sold to suitable consumers. ASIC’s two major reviews of DDO compliance (Reports 762 and 795) revealed weak governance, over-reliance on templates, and poor oversight of distributors, prompting them to sharpen their focus. This heightened scrutiny was brought to a head in September 2025, with the issuing of a stop order on a high-profile term account, popular with advisers.

For advisers, the takeaway is that TMDs should not be relied upon as the sole method for determining product suitability. ASIC expects advisers to apply their own due diligence, document client suitability beyond the issuer’s target market, and report significant dealings to product issuers. With ASIC now firmly in ‘enforcement phase’ with regards to DDO, advisers should take extra care to embed TMD checks, distribution reporting, and record-keeping into their compliance frameworks while awaiting any longer-term simplification through ASIC’s proposed DDO review.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Regulatory Compliance & Consumer Protection (0.5 hrs)

ASIC Knowledge Requirements: Regulatory Environment (0.5 hrs)

please log in to start this quiz

———–

References:

[1] https://www.news.com.au/finance/business/banking/regulator-freezes-115bn-in-funds-at-la-trobe-financial-leaving-aussies-in-dark/news-story/144f3ac0a8c9ffa71b1ea1ef85ea3f24

[2] https://www.moneymanagement.com.au/news/funds-management/asic-clamps-down-australian-unity

[3] https://www.investmentmagazine.com.au/2023/07/clearview-hit-with-ddo-stop-order/

[4] https://treasury.gov.au/publication/c2014-fsi-final-report

[5] https://www.moneymanagement.com.au/features/expert-analysis/design-and-distribution-obligations-putting-consumer-first

[6] https://download.asic.gov.au/media/etgm1amc/rg274-published-10-september-2024.pdf

[7] https://www.asic.gov.au/regulatory-resources/find-a-document/consultations/cs-1-extending-design-and-distribution-obligations-instrument/

[8] https://treasury.gov.au/sites/default/files/2023-01/p2023-358632.pdf

[9] https://www.asic.gov.au/about-asic/news-centre/find-a-media-release/2023-releases/23-115mr-asic-calls-on-investment-product-issuers-to-lift-their-game-on-design-and-distribution-obligations/

[10] https://www.asic.gov.au/regulatory-resources/find-a-document/reports/rep-795-design-and-distribution-obligations-compliance-with-the-reasonable-steps-obligation/

[11] https://www.ifa.com.au/news/34751-asic-flags-advice-checks-among-ddo-failures

[12] https://download.asic.gov.au/media/nv3oqcdb/attachment-to-rg274-published-10-september-2024.pdf

[13] https://www.afr.com/companies/financial-services/la-t robe-vs-asic-how-a-single-word-settled-the-stop-order-stoush-20250925-p5mxvs

[14] https://my.afca.org.au/searchpublisheddecisions/

[15] https://financialnewswire.com.au/financial-planning/ddo-regime-up-for-simplification/

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Regulatory Compliance & Consumer Protection (0.5 hrs)

ASIC Knowledge Requirements: Regulatory Environment (0.5 hrs)

please log in to start this quiz