Investment bonds can be integrated into modern estate planning to achieve tax efficiency, control, and asset protection in wealth transfers.

Introduction

Contrary what we are regularly told, the ‘great intergenerational wealth transfer’ is not coming. It’s already well underway.

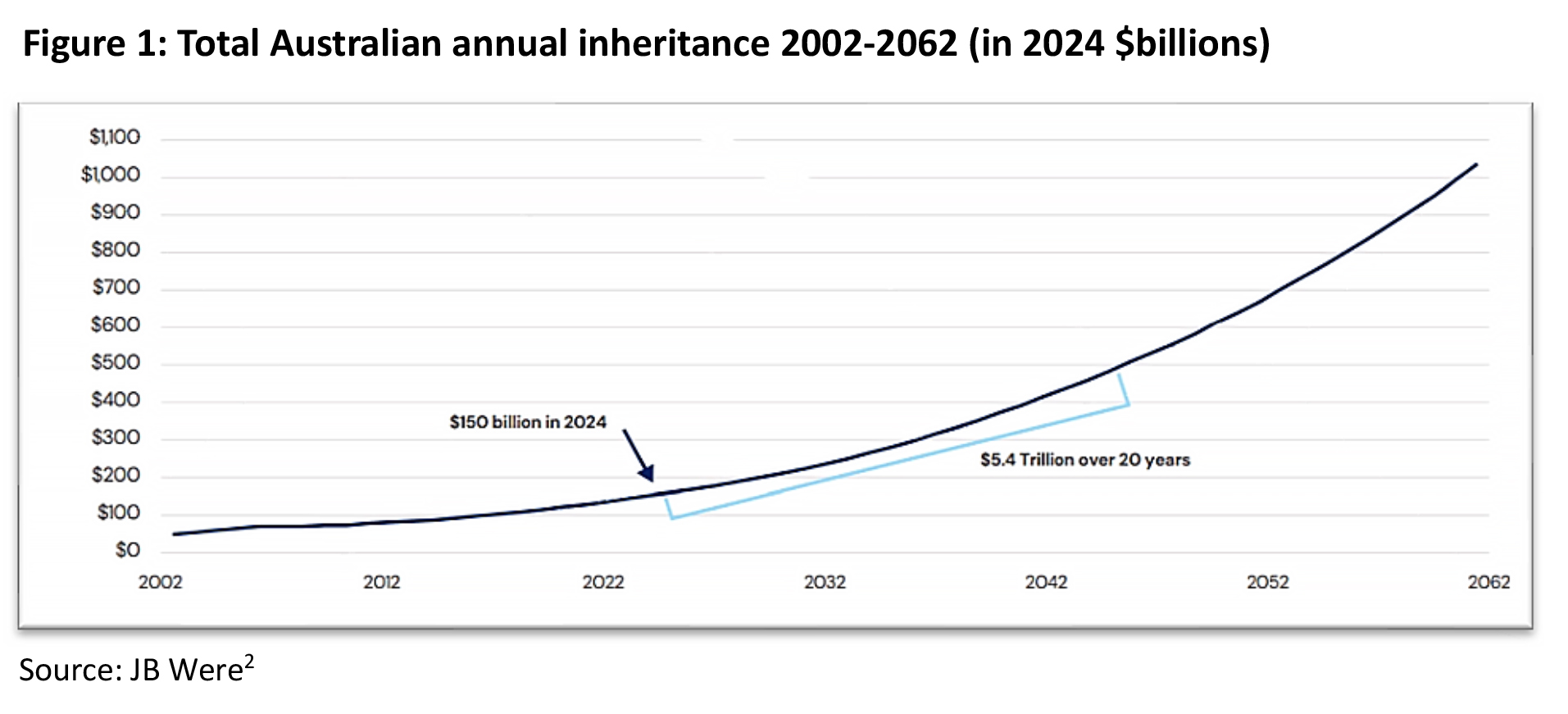

The enormity of this ‘handing down of wealth’ from older to younger generations was initially put in the spotlight by a Productivity Commission report, published in 2021. That report[1] estimated around $1.5 trillion had already been transferred by Australians over the previous 20 years, and that over the coming 30 years – to 2050 – that figure was expected to top $3.5 trillion.

Since 2021, asset values, especially house prices, have continued to surge, so much so that estimates by stockbroker JB Were suggest the eventual amount transferred by that date will be closer to $5.4 trillion[2], a truly astonishing amount.

In an ideal world, such transfers would occur efficiently, tax effectively, and in line with the transferrer’s wishes. Sadly however, without expert advice – financial and legal – wealth transfers are becoming increasingly complex and contested, subject to expensive legal disputes from family members who are often embittered and disenfranchised, and falling into tax traps that significantly erode the end value of the amounts inherited or gifted.

Indeed, research by ANZ Private Bank over a 25-year period found about 70 per cent of transfers of intergenerational wealth fail because of dissipating wealth, family conflicts, misaligned family values, delays and bungled execution[3].

Fortunately, advisers can augment traditional estate planning strategies, which rely on superannuation, wills, and trusts, with innovative solutions which are tax-smart, and far more resistant to any legal contest, giving clients far more peace of mind and certainty that their transferred wealth will end up with the right person, and in the right amount.

Increasingly, advisers are turning to investment bonds as a core pillar of wealth transfer strategies, and in this article, we will explore their structure and operation in more detail. We will also look at how the evolving estate planning landscape is proving the catalyst for their growing popularity.

Estate planning – an increasingly fraught landscape

Readers can be forgiven for interpreting the term ‘estate planning’ in a narrow sense, pigeonholing it as an area that is mainly about wills and other legal instruments, and largely about the transfer of wealth upon death. But estate planning is actually a much broader field, underpinned by a variety of strategies and instruments to transfer wealth and responsibilities between generations, both on and before death.

As such, it is a field that is becoming increasingly complex, and fraught by challenges and conflicts. There are several factors shaping this rapidly changing landscape:

- family structures are evolving, with blended, single parent, and same sex parents becoming more common

- while life expectancies are increasing, so too is the rate of dementia, the need for expensive medical care, and the demand for aged care support

- unaffordable housing, soaring school fees, and general cost of living pressures are seeing increasing instances of family members agitate for early inheritances

- the frequently changing tax rules around superannuation and retirement incomes, for example the proposed Div 296, which require deep technical expertise to successfully navigate.

One big happy family. Not.

According to a UNSW 2024 study, around 30% of children live in families outside the traditional “nuclear” family model. That includes about 12 per cent of children who live in step or blended families[4].

As families dissolve (due to separation, divorce or death of a partner) and new families are formed, it is not uncommon for wealth transfers to favour the children in the newer family, which in turn sees many aggrieved parties, including children from earlier marriages, and former spouses and de-facto partners.

Lawyers estimate disputes about wills and estates have grown 80% over the last decade[5]. And, according to one expert, disputes involving blended families now account for about eight in 10 legal actions[6], which is why strategies to avoid expensive and divisive legal battles need to be recalibrated to reflect changing and complex family relationships.

As court decisions continue to remind us, mechanisms previously thought to be robust and beyond dispute, such as wills, and even binding death benefit nominations in superannuation, are not immune to legal challenge.

And, depending on the state, and the amount being disputed, the success rate of such challenges can be alarmingly high.

In Queensland for example, it is estimated that 77% of challenges to wills are successful[7]. The Solomon Hollett Lawyers report[8], which focused on Western Australia, found that challenges pertaining to estates worth less than $600,000 have about a 60 per cent chance of success, climbing to 100 percent for estates over $3 million.

How traditional structures fall short

Traditional estate structures, such as superannuation, family trusts and direct asset holdings, each offer advantages, but they can also create unintended tax, timing and control issues at the point of wealth transfer.

Superannuation, for example, remains one of the most tax-effective vehicles for retirement accumulation, but less so for intergenerational transfer. When benefits are paid to non-tax dependants (such as adult children), the taxable component of the fund can attract up to 17% in death benefits tax, equating to tens, or even hundreds of thousands of dollars of eroded value in larger balances.

Moreover, superannuation death benefits form part of the estate unless a valid binding nomination exists, exposing them to potential challenge or delay. Even binding nominations themselves are still open to challenge on the grounds of capacity, improper execution, ambiguous terms, or failure to comply with fund rules or procedural steps, leading to delays even if a challenge is unsuccessful.

Generation Life’s Not Tomorrow’s Problem research[9] revealed that outside of super, advised clients are primarily using family trusts as the structure to transfer wealth. While trusts assist in effectively managing access to and the distribution of wealth, there will be times where the structure may not be as tax efficient as some alternatives.

At some point, the use of a discretionary or family trust may not be effective where the trust’s beneficiaries’ personal, taxable income levels are at higher marginal tax rates. The use of child beneficiaries (like grandchildren) may also not be effective, as minors may face penalty tax rates on unearned income.

Where a testamentary trust has been established under a will for estate planning, the practicalities of managing the trust on an ongoing basis may also prove expensive or burdensome for appointed trustees.

Property and direct investments, meanwhile, trigger capital gains tax (CGT) on disposal and will be subject to the granting of probate, which can often delay execution of a will for 6-12 months.

These limitations highlight the value of complementary strategies that enable wealth to be transferred outside the estate while preserving governance and tax efficiency.

Investment bonds can provide such a structure: assets can pass directly to nominated beneficiaries, tax-paid within the bond, and free from probate, CGT, or death benefits tax.

Investment bonds at a glance: the tax-smart wealth vehicle

In simple terms, investment bonds are a form of life insurance policy with an investment component, designed to provide long-term, tax-effective wealth accumulation and transfer.

All investment earnings within the bond are taxed at a maximum rate of 30%, although franking credits, capital gains discounts and underlying fund tax offsets often reduce this effective rate to around 10–15% per annum over time. Some bond issuers, using innovative tax optimisation strategies, can bring this rate down even further.

Once a bond has been held for 10 years, the proceeds, including investment earnings, can be withdrawn on a ‘tax-paid’ basis, meaning no further personal tax is payable by the investor or beneficiaries. After commencement, investors can make additional contributions of up to 125% of the previous year’s amount without resetting the ‘10-year rule’.

Death benefits are tax free at any time, in stark contrast to the tax on superannuation death benefits, which can be as high as 17% if paid to non-dependents.

Bypass and control: why investment bonds are a powerful estate planning tool

Because investment bonds are issued under life insurance law, bond holders can nominate beneficiaries who receive the proceeds directly upon death, bypassing the will/estate entirely. This means the payment is not subject to probate, contest, or public disclosure, and can be made confidentially.

Some providers (for example, Generation Life) also offer a transfer of ownership feature (without triggering any tax burden or resetting the 10-year period), allowing control over when and how beneficiaries can access the investment – for example, releasing funds at a set age or limiting annual withdrawals. These features give clients the ability to protect beneficiaries from poor financial decisions while ensuring their wishes are honoured.

Investment bonds are therefore a cost-effective, tax-efficient, and convenient way to pass on wealth to dependants or other beneficiaries, with minimal administrative complexity. Because they sit outside the estate, investment bonds can distribute proceeds quickly and privately on death, providing certainty and reducing the risk of disputes or delays associated with probate.

For advisers, these options make investment bonds a powerful addition to the estate planning toolkit. They can help address the complexities of blended families, manage gifts to charities or non-family beneficiaries, or balance the needs of multiple generations.

Investment bonds can also offer protection in bankruptcies

As a life insurance policy, investment bonds are generally beyond the reach of creditors (provided they weren’t contributed to while insolvent or set up for the purpose of creditor avoidance). This status offers an additional layer of protection and certainty in wealth transfer scenarios impacted by bankruptcy.

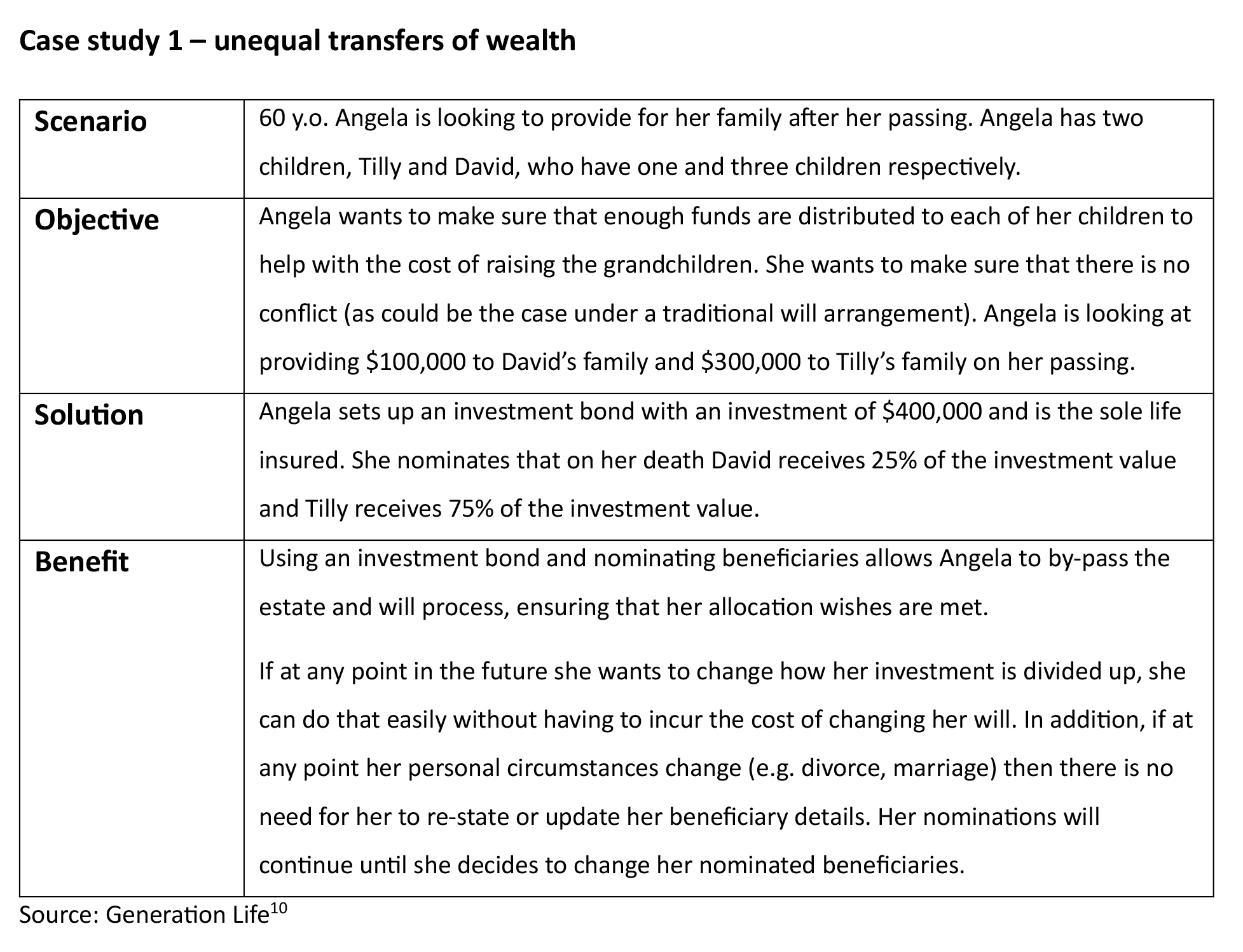

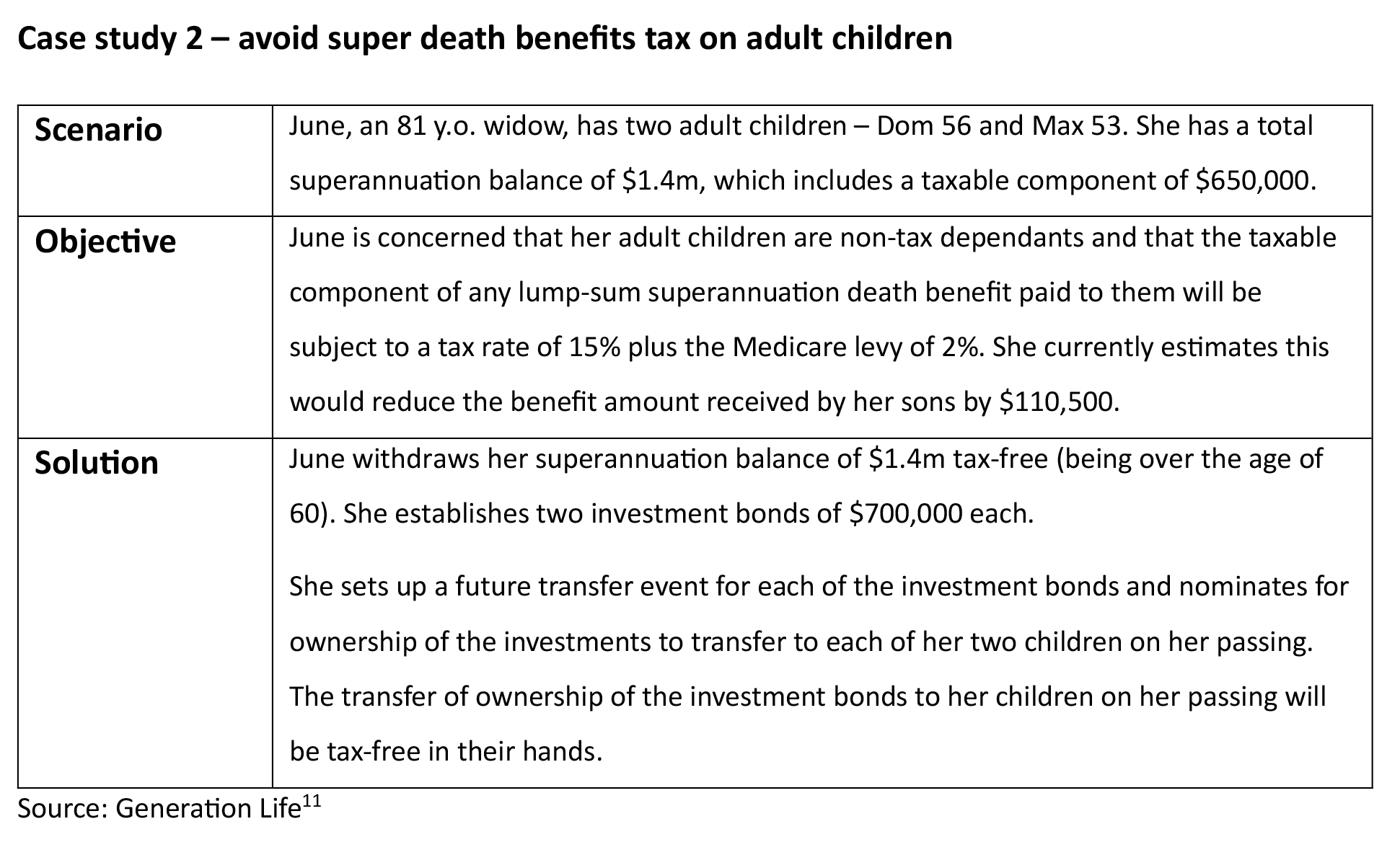

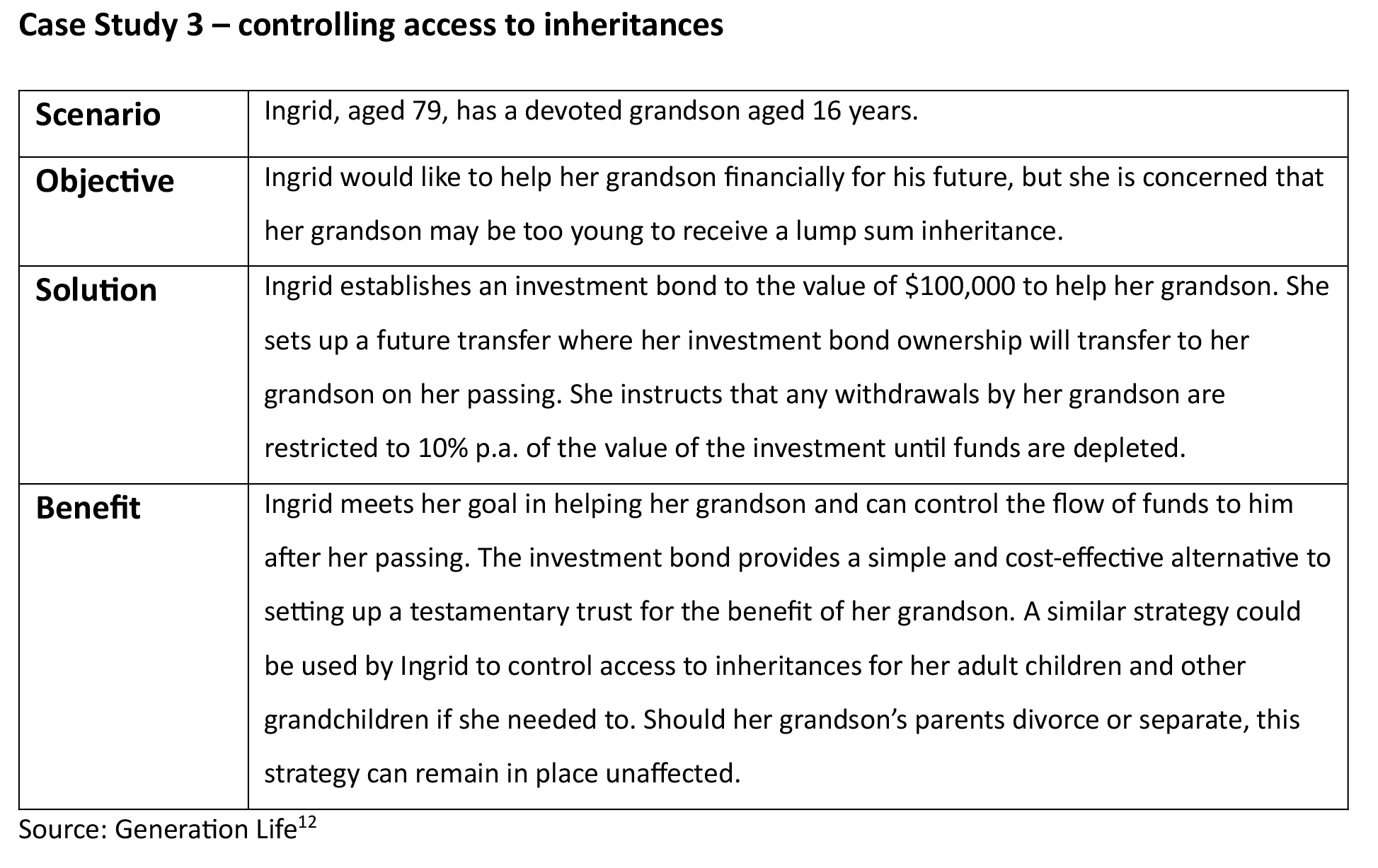

Strategy in action: Wealth transfer case studies

The following case studies demonstrate the flexibility and effectiveness of investment bonds in a variety of wealth transfer scenarios.

Summary

As Australia moves deeper into its largest intergenerational wealth transfer on record, advisers are being called upon to guide families through an increasingly complex and emotionally charged estate planning landscape. Traditional tools such as superannuation, wills and trusts continue to play a central role, but their limitations, including tax inefficiencies and exposure to legal challenge and probate delays, becoming more apparent as family structures evolve. Against this backdrop, clients are looking for solutions that provide both simplicity and certainty.

Investment bonds are now in the spotlight as one of the most versatile structures to meet this demand. Their unique combination of tax efficiency, flexibility, and control allows advisers to design strategies that preserve family harmony, protect capital, and ensure assets pass quickly and privately to intended beneficiaries. Whether used to supplement traditional estate planning, to offset superannuation death benefit tax, or as an alternative to a testamentary trust, they offer a means of transferring wealth that is technically robust and resistant to challenge.

By integrating investment bonds into a broader estate planning and wealth transfer strategy, advisers can help clients navigate the complexity of modern family life, manage tax and legal risks, and create enduring legacies that reflect both financial goals and deeply personal intentions.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.25 hrs) and Tax (Financial) Advice (0.25 hrs)

ASIC Knowledge Requirements: Estate Planning (0.25 hrs) and Taxation (0.25 hrs)

please log in to start this quiz

———–

References:

[1] https://www.morningstar.com.au/personal-finance/why-54-trillion-wealth-transfer-is-generational-tragedy

[2] Ibid.

[3] https://www.afr.com/wealth/personal-finance/succession-warring-families-undermining-3-5-trillion-of-inheritances-20230526-p5dbjo

[4] https://www.uniting.org/content/dam/uniting/documents/families-report/uniting-families-report-2024.pdf

[5] https://www.afr.com/wealth/personal-finance/how-blood-trusts-can-keep-step-kids-out-of-your-inheritance-20240206-p5f2q8

[6] https://www.afr.com/wealth/personal-finance/big-increase-in-inheritance-feuds-among-blended-families-20191212-p53jbs

[7] https://ballantynelaw.com/insights/contested-wills-statistics/

[8] https://www.afr.com/wealth/personal-finance/the-reason-so-many-adult-children-are-challenging-wills-20250122-p5l6i2

[9] https://coredatainsights.com/client-insights/not-tomorrows-problem-generation-life/

[10] https://generationlife-endpoint.azureedge.net/live/attachments/cl7qyf0ki0dld0pnpib4q0can-generation-life-estate-planning-guide-july-2022.pdf

[11] Ibid.

[12] Ibid.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.25 hrs) and Tax (Financial) Advice (0.25 hrs)

ASIC Knowledge Requirements: Estate Planning (0.25 hrs) and Taxation (0.25 hrs)

please log in to start this quiz