What is your understanding of the importance of ensuring that referral arrangements to meet the ethical standards in the Code of Ethics?

Running an ethical and compliant financial advice practice extends far beyond an individual adviser’s desk; it requires meticulous management of the entire professional ecosystem, including colleagues, peers and third-party referral partners.

While the Financial Planners and Advisers Code of Ethics 2019 (Code of Ethics) primarily places responsibility on the individual, the practical reality of modern practice means that an adviser’s compliance and reputation are inextricably linked to the actions of those around them. Every referral, internal file review or shared office conversation acts as a touchpoint that can either uphold or compromise the principles set out in the Code of Ethics.

Effective management of this ecosystem is, therefore, a foundational requirement for satisfying the Code of Ethics. This involves establishing and enforcing clear governance structures and due diligence processes. When engaging with external partners, such as mortgage brokers, paraplanners or accountants, an advice practice must ensure these relationships do not create a conflict of interest and are always in each client’s best interests.

Internally, a culture of peer accountability and compliance monitoring is essential to ensure consistency in client service and adherence to the standards that comprise the Code of Ethics. A failure to manage a colleague who takes shortcuts, or a referral partner who pressures clients, is effectively a failure to uphold the ethical duties of the practice itself.

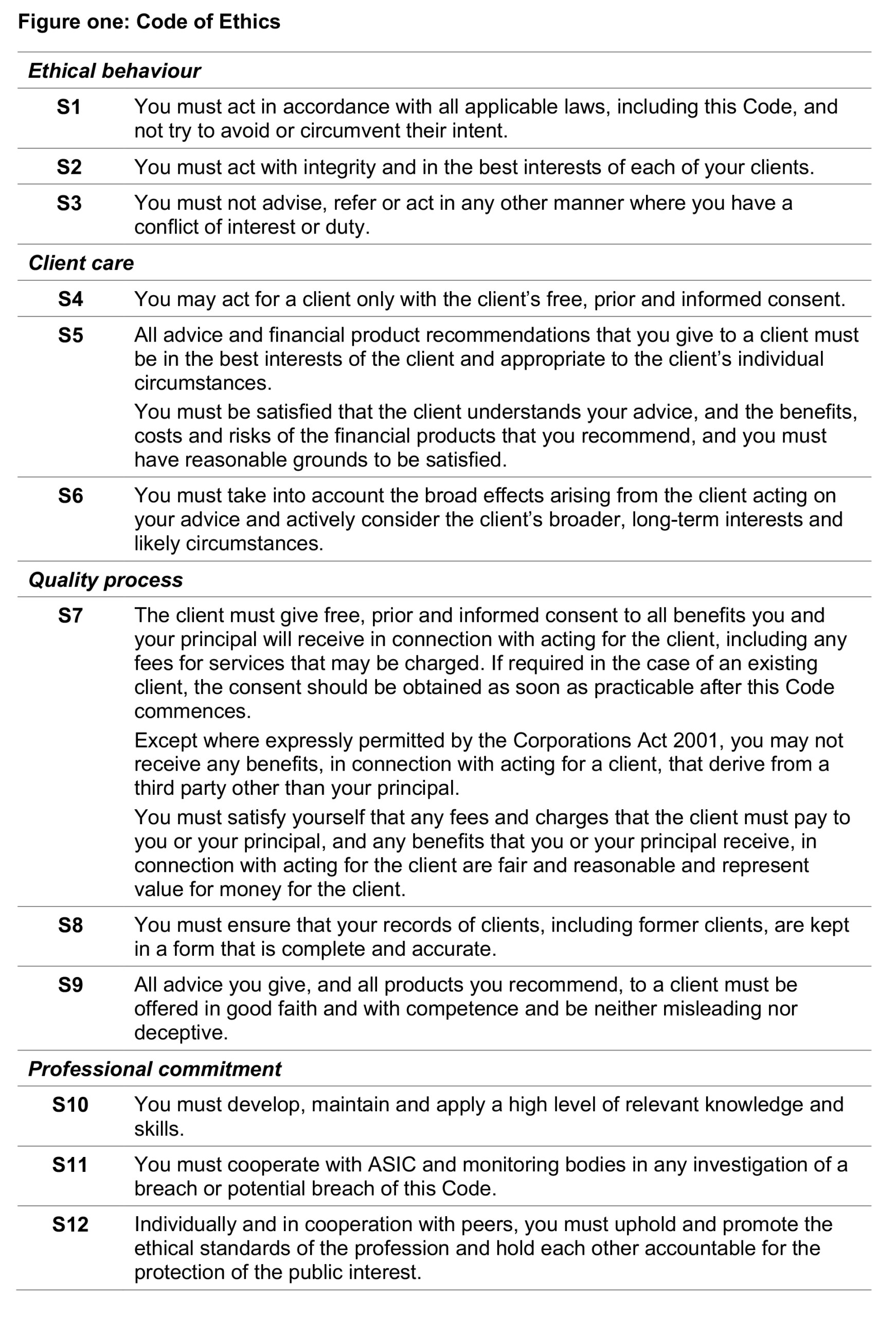

Ultimately, the commitment to the Code of Ethics must be a shared commitment, enforced from the top down and monitored across all external and internal relationships. It is important to implement strategies to vet, monitor and manage peers and referral parties, transforming the often-unregulated fringes of the practice into a robust line of defence that safeguards both the client’s best interests and the professional integrity mandated by the Code of Ethics (figure one).

Ethics, colleagues and peers

While building a strong ethics and compliance culture is essential for promoting positive decision-making, even well-intentioned companies can inadvertently set the stage for ethical problems. This often happens when the environment compels individuals to make choices they know, or suspect, are not right. Examples might include recommending an in-house product when it clearly isn’t in a client’s best interest, utilising a high-fee platform to reduce an adviser’s administrative workload for a client with few assets, or rigidly adhering to a licensee’s “cookie-cutter” advice model that ignores a client’s specific needs.

Such environments can also foster ‘motivational blindness’, defined as the tendency to overlook the unethical actions of others when noticing them would conflict with one’s own self-interest. This is particularly relevant for support staff who may have reservations about an approach or decision but are unlikely to speak out if the advice business does not genuinely welcome or protect internal questioning. When staff are discouraged from raising concerns, ethical issues can remain hidden and persist, undermining the entire firm’s commitment to compliance and client best interests.

There are five ways companies might unintentionally trigger good people to make unethical choices[1]. Each of these is examined through the lens of the financial adviser Code of Ethics (Code) (figure one) and illustrates how a weak business and ethics culture can lead your peers to actively or passively make decisions that potentially breach, or support a breach, of the Code.

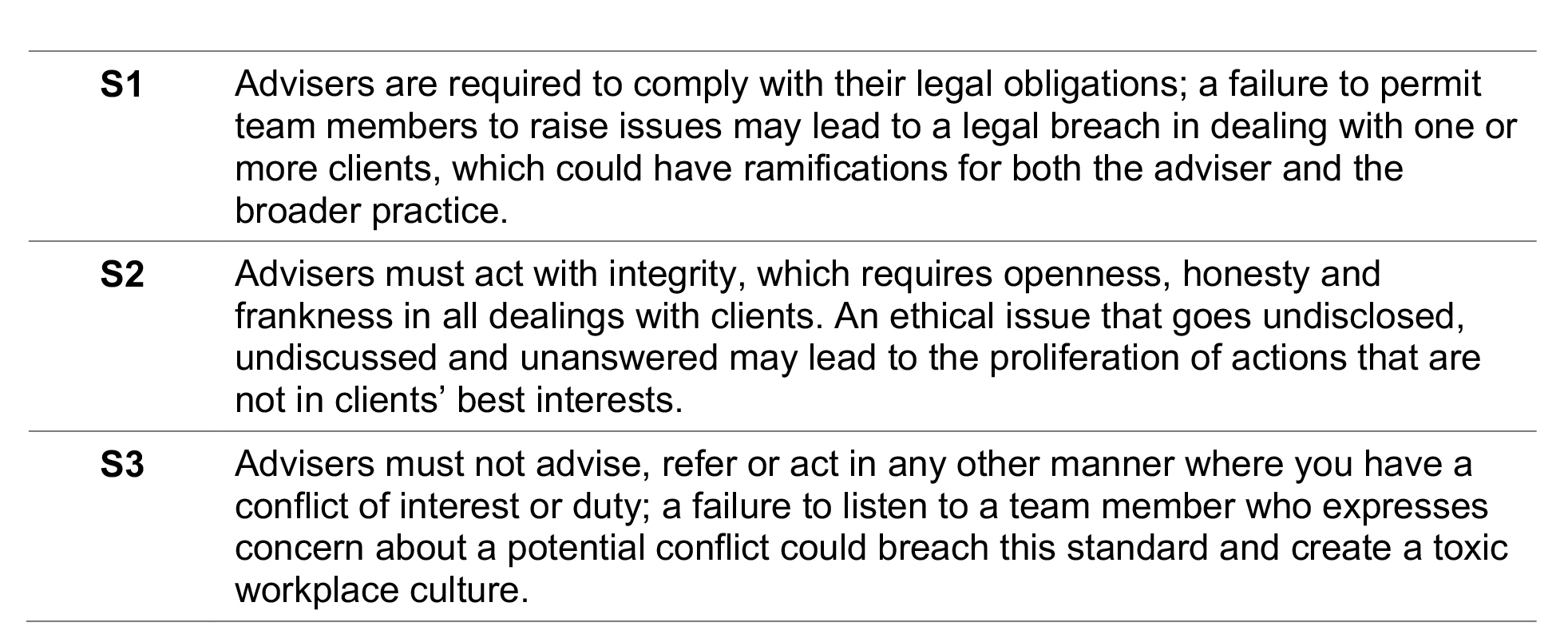

1. Create an environment where it’s psychologically unsafe to speak up

Managers and team leaders need more than an open-door policy; they need to encourage their staff to raise and discuss ethical concerns. Creating a culture where your team can speak freely is essential if you’re to avoid misconduct in your practice. Equally important is that those team members are listened to.

Appropriate mechanisms for your team to communicate are crucial, as is an environment in which each team member is comfortable to speak up. Importantly, any issues raised must be addressed; a feeling of futility or a negative reaction to an issue that’s raised does not create a supportive environment and is likely to stultify future discussions.

Failing to provide a safe environment for your team to discuss ethical issues or dilemmas can ultimately have a negative impact on clients and could potentially result in the breach of several standards of the Code of Ethics, including:

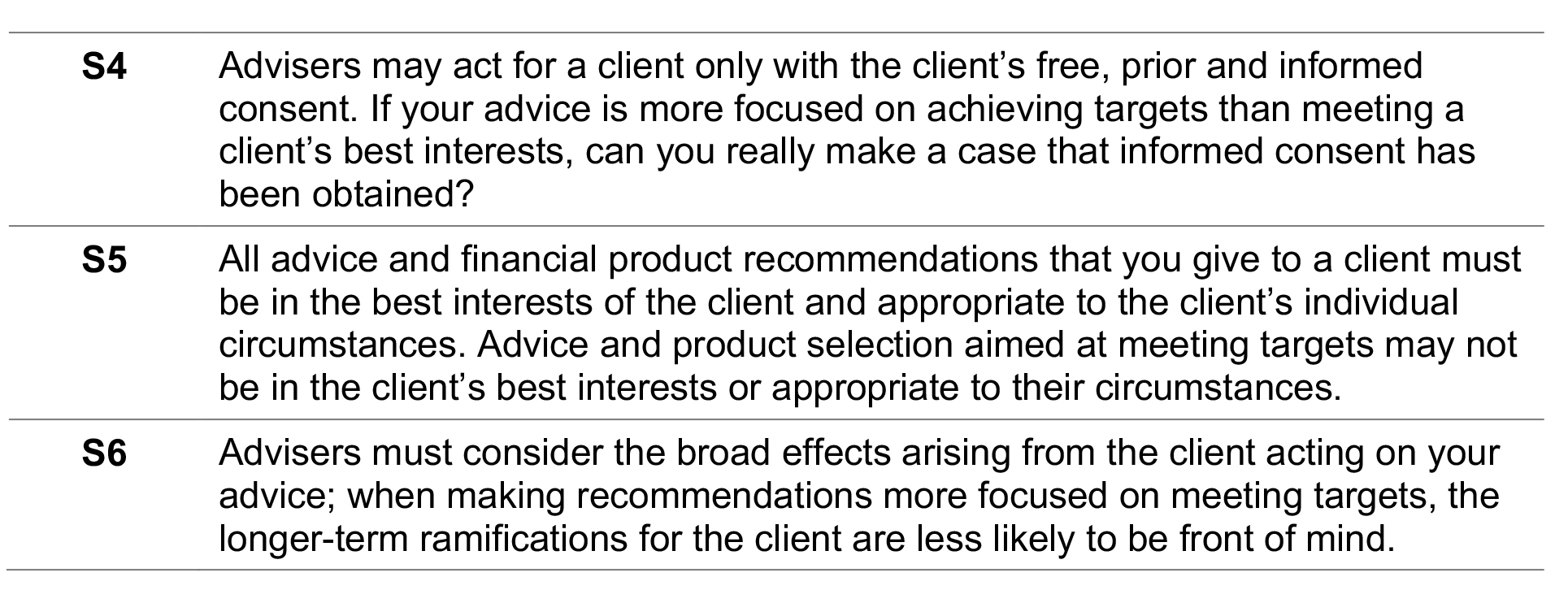

2. Avoid pressure to reach unrealistic performance targets

Performance targets can be financial targets such as profitability or assets under management or focus on client acquisition or retention. Research from Harvard Business School suggests “unfettered goal setting can encourage people to make compromising choices in order to reach targets2”.

The standards that comprise the Code of Ethics focus on doing the right thing by clients – obey the law, act in client best interests and act professionally. The 2018 Hayne Royal Commission heard several cases in which performance targets may well have influenced actions, such as those to ‘churn’ clients or move them into in-house products or platforms.

While it is common business practice to have a range of performance targets, it’s important that they are both realistic and achievable without having to compromise the advice provided to clients. Targets that are client and service centric can lead to ethical outcomes for those clients.

While striving to reach performance targets can result in breaching several standards of the Code, it’s the ‘Client Care’ standards where it is most likely to cause a breach.

3. Discussing ethics once there’s been a transgression

Too many leaders assume that talking about ethics is something you do once there’s been a client complaint, an obvious transgression or an AFCA investigation. Previous articles in this series have discussed the importance of ethics, business culture and ongoing ethics training in your financial practice. It is not solely a matter of how you behave, but how you and each of your team members conduct business. That’s why it’s important to educate and reaffirm, on a regular basis, the importance of ethical practices in your business.

This is particularly important for considering issues that don’t fall neatly into right and wrong. While the ‘grey zone’ – that area that exists on a continuum between right and wrong – can provide challenges for your business, it can also provide benefits. Being aware of the grey zone and using examples and case studies that aren’t black and white provide an excellent opportunity for training and discussion. List the situations that your team may encounter in their day-to-day work that might not be black and white. Once such situation is identified, you can take a proactive approach with training.

This grey zone reinforces the importance of all employees of a financial planning business being aligned with its values and practices. If you are transparent about how to deal with ethical issues, if you discuss them regularly and not just when there’s an issue, there’s a lower chance of breaching the Code of Ethics and, therefore, less likelihood of facing enforcement action.

This will help maintain professional commitment and uphold standard 12.

4. A positive example isn’t being set

Positive leadership is crucial and all leaders in your business must accept their responsibility in setting that positive example. They must be vigilant about their intentions and be mindful of how their peers and subordinates might interpret their behaviour.

Leaders must take care with how they react to external and internal factors, as these demonstrate acceptable responses. These factors might include:

- a client complaint or negative review on social media

- lower than expected revenue or poor financial performance

- losing a valued staff member to a rival practice

- a change of licensee

- a systems issue or breakdown

- regulatory change or challenge.

Leaders need to model ethical behaviour. In an advice practice, this includes compliance with the standards that comprise the Code of Ethics. Failure to do this not only sets a poor example, but it could also set the business on a problematic path.

In a letter to investors in 2019, veteran investor Warren Buffet made the following comment:

“Over the years, Charlie and I have seen all sorts of bad corporate behaviour, both accounting and operational, induced by the desire of management to meet Wall Street expectations. What starts as an “innocent” fudge in order to not disappoint “the Street” can become the first step toward full-fledged fraud…And if it’s okay for the boss to cheat a little, it’s easy for subordinates to rationalise similar behaviour.”

All leaders need to set a positive example for their team, particularly where an ethical dilemma that arises is not clearly defined.

5. Avoid cultural numbness[2]

Cultural numbness creates a situation that, irrespective of how principled you are, over time, the bearings of your moral compass will shift toward the culture of your organisation. Situations where an ethical leadership is lacking are often those where good people can make poor decisions. Cultural numbness is described as a state where the ‘warning bells have stopped ringing’, where a culture of ethics does not exist, and positive examples are not set by business leaders.

In an advice practice, it could be the difference between acting in your or the practice’s best interests rather than the client’s. It could be skirting legal boundaries (breaching standard one), failing to manage conflicts of interest (breaching standard three) or simply recommending products without taking into account the long-term ramifications of the client acting on your advice (breaching standard six).

The standards that comprise the Code of Ethics are not prescriptive, are not intended to provide definitive guidance. Individual circumstances will differ in practice and there is allowance for differences of professional opinion on how the ethical rules of the profession should apply in a particular case.

This is where positive leadership and an ethics centric business culture will stand an advisory practice in good stead, particularly in those circumstances where you encounter ethical decision making that is not black and white. Doing what is right will depend on the circumstances and will require you to exercise your professional judgement in the best interests of each of your clients.

There are several cultural practices to that could be implemented to encourage all staff to speak up in circumstances they believe to be working against client best interests or verging on unethical behaviour.

- Establish a practice-wide code of conduct

This code of conduct should encapsulate your business values and the Code of Ethics. Your code of conduct should set clear expectations about your employees’ behaviour when carrying out their duties, including how to deal with difficult issues where a decision could result in a breach of one or more ethical standards. You need to ensure all staff understand each of the twelve standards in the Code of Ethics and how each standard may specifically intersect their role. - Foster a safe environment

Leadership must actively demonstrate that questioning an approach is valued, not penalised. If a support staff member raises a concern that turns out to be minor or unfounded, they should be thanked for their diligence, not reprimanded for wasting time. This removes the fear of negative consequences that fuels motivational blindness. - Decouple rewards from questionable outcomes

The Corporations Act 2001 prohibits conflicted remuneration, designed to protect consumers by ensuring financial advice is in their best interest, rather than being swayed by financial incentives. It is important therefore to ensure that employee compensation, bonuses and promotions are based on ethical behaviour and process adherence, not solely on revenue generation. - Leadership by example

Advisers and principals must visibly and consistently adhere to the highest ethical standards. If leaders are seen cutting corners, staff will quickly learn that ethical practice is optional. Ethical humility, where leaders admit mistakes and seek input, is crucial. - Workplace training and discussions about ethical dilemmas

This is a positive way to ensure all staff understand both the practice’s values and the obligations of the Code of Ethics. The use of case studies to discuss ethical dilemmas can reinforce the practice’s standards of conduct and clarify behaviours and practices that do and don’t work within your code of conduct.

Importantly, ethics training should not be a once off and does not solve a problem. Ideally, training should teach team members to make good decisions that are compliant with the law and consistent with your practice’s values.

This training could be incorporated as part of regular team meeting; as suggested above, by using a variety of case studies which could address common ethical dilemmas across the financial planning industry. The AFCA website[3] is a good source of cases and decisions made by AFCA to form the basis of discussion.

Ethics and referral partners

Financial advice practices often need to refer clients to other specialists – both inside and outside the firm – to address the full range of client needs that exceed the adviser’s own competency or specialisation. Such specialties might include risk advice, tax services, SMSF administration or paraplanning. These referral arrangements are frequently established at the licensee level, meaning the adviser may be directed to specific third-party providers.

The way these partners interact with your client has a direct impact on your practice. A negative experience with a referral partner not only reflects poorly on them but can damage your relationship with your client. Critically, poor conduct by a partner can lead to a breach of an ethical standard, resulting in consequences for you if you fail to act on the issue.

This makes standard three of the Code of Ethics particularly important. It mandates that you must not advise, refer, or act in any other manner where you have a conflict of interest or duty. While the debate around standard three has been long running, it remains enforceable. In its current form, the standard addresses actual conflicts between the duties owed to your client and any personal interest or duty owed to another individual or organisation.

According to guidance[4], you will breach standard three if “a disinterested person, in possession of all the facts, might reasonably conclude that the form of variable income (e.g. brokerage fees, asset-based fees or commissions) could induce an adviser to act in a manner inconsistent with the best interests of the client or the other provisions of the Code.”

However, the guidance also clarifies that you would not breach standard three merely by being a duly remunerated employee of an entity that provides retail financial advice and services and referring to a specialist within that practice, even if profit-sharing is involved. Regardless of the referral structure, you are still required to ensure that the advice and services provided are always in the best interests of your client and comply with all other provisions of the Code.

Accountants

It’s one of the most common referral arrangements in the industry. Many a business has taken advantage of the natural synergies between accounting and financial advice to build a business where an accounting practice acquires and embeds financial advice businesses – or vice versa.

As well as being synergistic, there are also areas of overlap. For years, accountants have advised clients about investment strategies to manage and mitigate tax and have been advocates of self-managed super funds (SMSFs). While in many cases an SMSF may be an appropriate strategy for a client, there may be times where you question its validity as an appropriate approach for your mutual client. Irrespective of the relationship with the referral partner, your client and their best interests must always come first.

If there’s a scenario where a client’s accountant makes a recommendation about an investment or a strategy, even if it’s tax related, you have the right to question it, particularly if you don’t believe it to be in the client’s best interest. While there’s a case for making enquiries of a strategy even if the accountant isn’t a referral partner, if it is a formal referral relationship it’s even more important.

You may query a recommendation because you have a better understanding of an asset class or financial product, or because of your in-depth knowledge about the client’s financial objectives and their risk profile. An accountant’s product or strategy recommendation may be too risky for that client or inappropriate when you consider their total portfolio.

In such cases it is important to call it out and discuss the holistic view with the referral partner; that way, you can agree on what’s best for the client, what will help them achieve their financial objectives (including tax management) and what works within the agreed risk parameters.

Risk advice

Risk advice is a specialist area. Some financial planning practices may have an in-house risk expert, others refer to a specialist business. It would be expected that in-house risk advisers would adhere to your practices’ approach to managing ethics in a way that’s consistent with your firm’s code, as well as the Code of Ethics. That, however, needs to be stipulated and not assumed; a failure to act accordingly can have negative repercussions not only for your client, but for the broader practice and its staff.

Where you refer to a specialist risk practice, it is important to have an agreement with respect to the service provided. You need to ensure that it’s appropriate for each client and will meet their needs over time.

Mortgage brokers

Mortgage brokers have a particular skill set and there may be times you need to refer a client for loan assistance. Renumeration for mortgage brokers typically comes from the financial institution where they place the business and, in most cases, they are paid an upfront commission and a trail or ongoing commission for the business. These commissions are paid out once the loan settles and are based on a percentage of the loan amount. It is important your client understands this, and you both need to be confident that the loan has been placed with the most appropriate institution for the client, not that which offers the most handsome remuneration.

In January 2020, at the same time as the Code of Ethics became law, the Federal Government passed legislation to create a duty for mortgage brokers to act in the best interests of consumers. The legislation created a duty for mortgage brokers to act in the best interests of consumers and requires mortgage brokers to prioritise consumers’ interests when providing credit assistance (known as the conflict priority rule)[5].

Managing referral arrangements

When engaging with specialists for client referrals, you should formalise the relationship with a Service Level Agreement (SLA) that clearly outlines your expectations regarding their conduct and service standards. If a formal SLA isn’t in place, or if it doesn’t cover the requirements stipulated in the Code of Ethics, establishing or amending it is a priority. Never assume your clients will be treated in the manner or receive the quality of advice you expect.

It is crucial to review the advice provided by any third party to whom you have referred a client. If you have any doubts or queries about the appropriateness of the advice, you must address them immediately with the referral partner. This may be a difficult conversation, as the partner might perceive it as a challenge to their professionalism. However, if you genuinely believe a recommendation is not in the client’s best interest, you have an ethical duty to act.

To make this conversation effective and less confrontational, frame your concern around the client’s best interests. Explain your query by referencing the client’s specific financial objectives, risk profile, estate plan, or existing portfolio, whichever is most relevant. By making the client and their outcomes central to the discussion, the conversation becomes less personal and remains focused on achieving positive results for your mutual client.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC or AFCA and for each, potential breaches of the Code of Ethics are identified. These case studies represent examples of those that would be of value for the business to discuss as part of its workplace training.

Case study one: A focus on gearing strategies

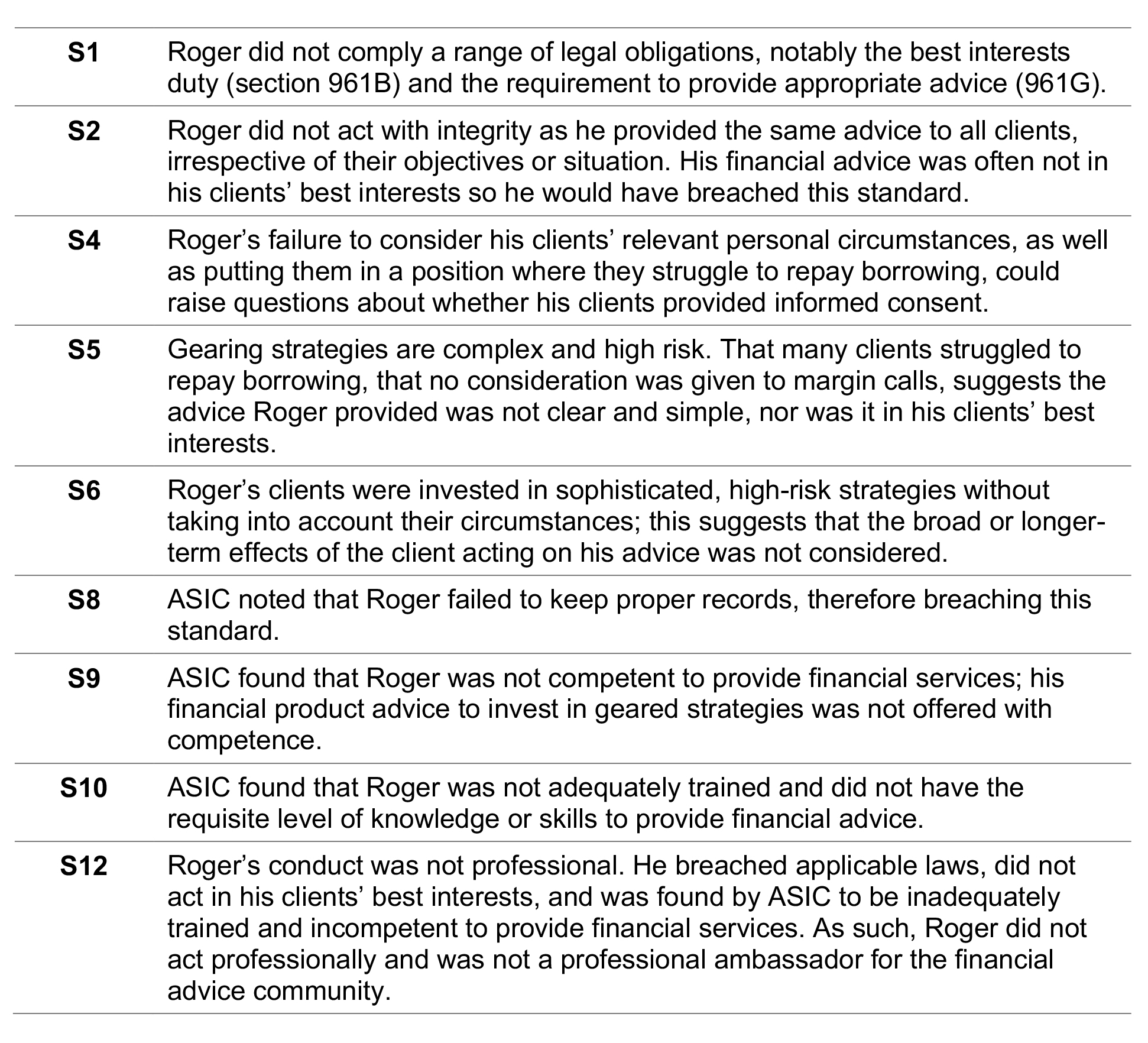

Roger was an authorised representative of ACME Advice on Queensland’s Gold Coast. An ASIC review found that Roger failed to act in the best interests of his clients. ACME Advice actively encouraged its authorised representatives to recommend gearing strategies to clients to invest in the sharemarket. ASIC noted that Roger provided advice that was inappropriate when his clients’ relevant personal circumstances were reviewed. When queried by ASIC, Roger commented he was following the strategy provided by his licensee and adopted by other authorised representatives of ACME Advice.

In providing advice to his clients, ASIC found that Roger failed to consider their relevant personal circumstances, their cash flow or their ability to cover margin calls. He also failed to consider an exit strategy from the gearing arrangements for his clients and did not recommend or implement appropriate personal insurance cover.

Additionally, ASIC found that Roger failed to keep proper records and that he was not adequately trained or competent to provide the financial product advice that formed the basis of his recommendations. His lack of understanding about relevant legal and professional obligations as a financial adviser created additional risks to his current and future clients.

Roger received a five-year ban from ASIC with respect to providing financial services, carrying on a financial services business or controlling an entity that carries on a financial services business. The licensee was also penalised.

Roger’s approach to working with clients would have seen him potentially breach the following standards of the Code:

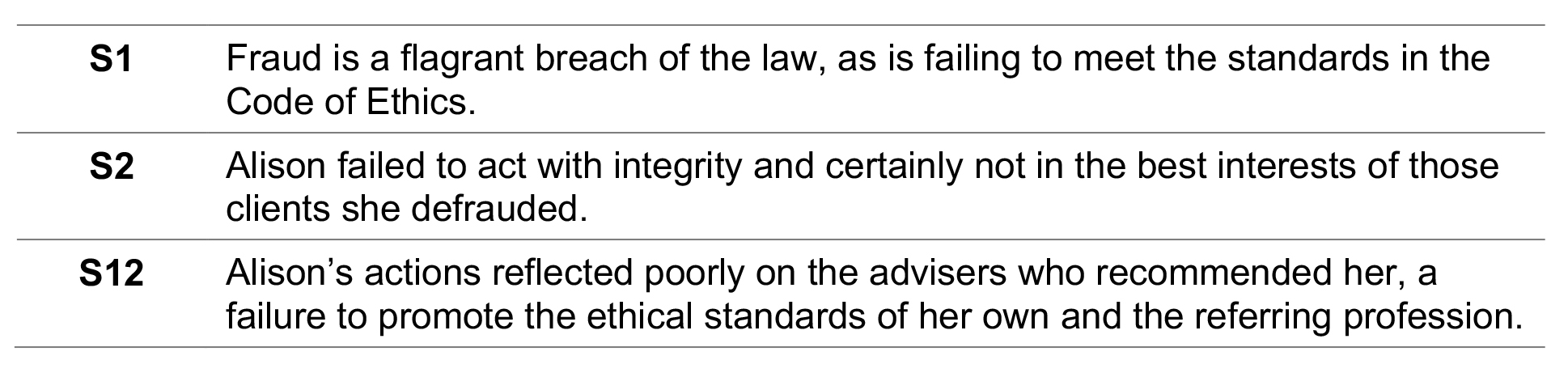

Alison was a mortgage broker with ACME Mortgage Brokers. She provided mortgage broking services to a number of financial advice practices in Sydney’s northern beaches 2015 to 2024. Between 2017 and 2022, Alison dishonestly obtained funds from her employee and clients.

She was convicted of 15 counts of dishonestly obtaining a financial advantage by deception, five counts of dealing with identity information to commit an indictable offence, and one count of dishonestly obtaining property by deception. She was sentenced to four years’ imprisonment.

Under the Corporations Act and the National Consumer Credit Protection Act, ASIC may permanently ban a person from the financial services and credit industries if they are convicted of fraud. Consequently, based on her convictions, Alison has been banned permanently, which means she cannot:

- provide any financial services or engage in any credit activities,

- control an entity that carries on a financial services business or engages in credit activities

- perform any function for an entity carrying on a financial services business or engaging in credit activities, including as an officer, manager, employee or contractor.

Shelley and Louise from ACME Financial Advice referred several clients to Alison over a four-year period; five were among those she defrauded. While Shelley and Louise had conducted due diligence before forming a referral relationship with Alison and they had a formal SLA in place, her actions reflected badly on them. It adversely affected their client relationships and they believed their association with Alison sullied their reputation.

By defrauding her clients, Alison would have potentially breached the following standards in the Code of Ethics had it applied to her as a mortgage broker. She did fail to meet the mortgage brokers best interests duty:

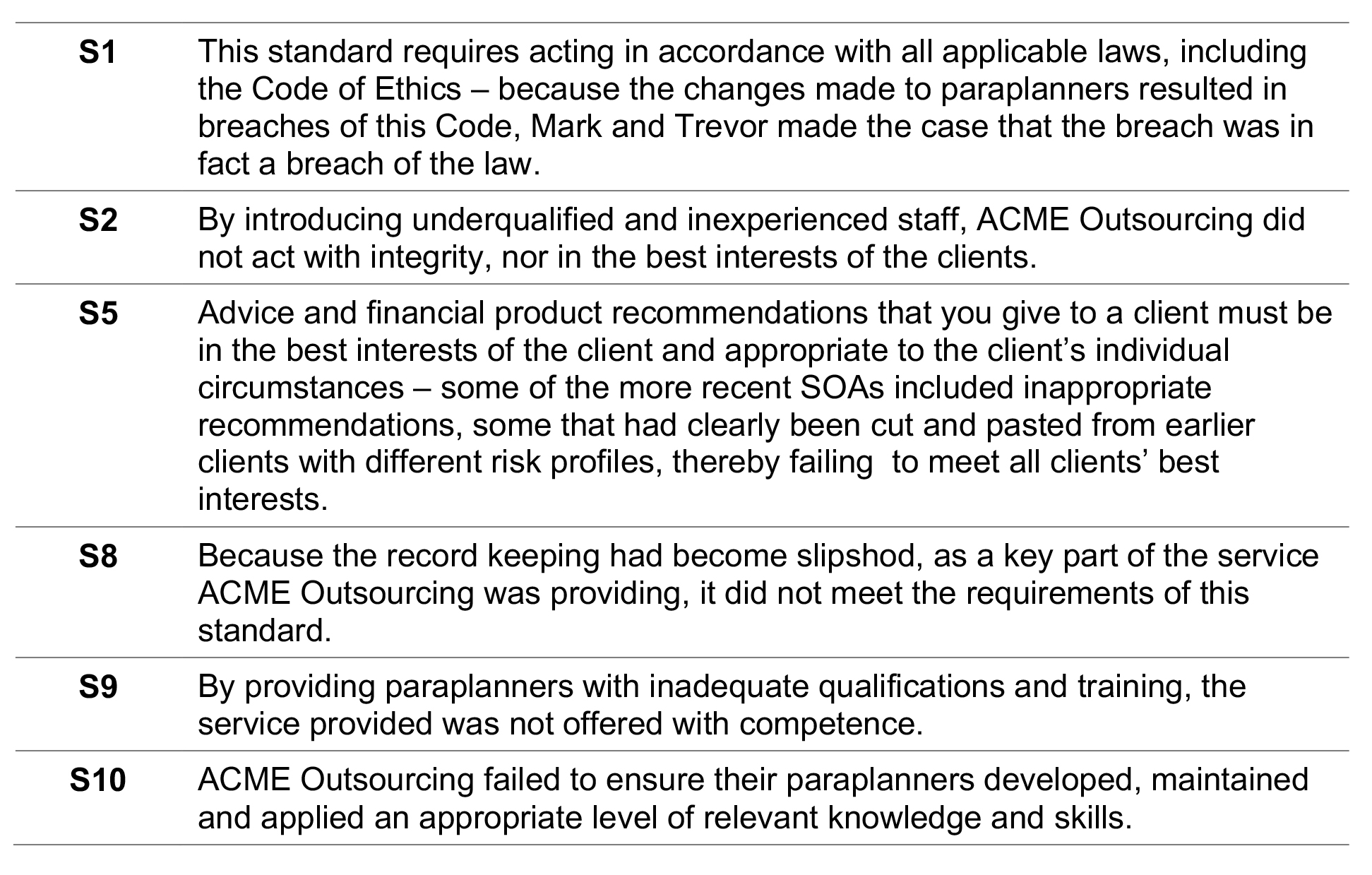

ACME Financial Advice was located in a growth corridor in Melbourne’s northern suburbs, in an area that had experienced gentrification and an influx of professional couples. The practice was growing quickly and the business principals, Mark and Trevor, decided to outsource some of their business processes so they could scale their business more quickly, without having to add too many more staff.

Mark was charged with finding some potential outsource providers and they held a ‘beauty parade’ to see what each had to offer. They settled for ACME Outsourcing, with staff based offshore, as they could get a significant amount of their business processes dealt with at a very reasonable cost. One of the processes they outsourced was paraplanning.

As part of the due diligence process, Mark and Trevor made sure that the paraplanners provided by ACME Outsourcing had appropriate Australian-equivalent accreditation and qualifications, were RG146 compliant and there were processes in place to ensure ongoing professional development.

Once satisfied this was the case, as ACME Outsourcing met the other criteria the practice leaders required, the company was appointed to provide services to ACME Financial Advice.

At the six-month review, Mark and Trevor expressed their satisfaction with ACME Outsourcing. It had met the KPIs set and in the case of paraplanning, provided quality and timely service. However, not long after, they noticed a sudden decline in the quality of Statements of Advice and reporting. They were undertaking client reviews and the information coming into the practice was incomplete and/or inaccurate.

After making several enquiries, they discovered the initial high quality paraplanners had been replaced by inexperienced and less qualified staff. Mark and Trevor also noted that the record keeping by these new team members was not meeting their service level agreement. It was evident the new staff members were being paid less by ACME Outsourcing.

Because they had used the Code of Ethics to frame the KPIs agreed with ACME Outsourcing, they were able to refer to them when detailing the issues arising from the change in paraplanning staff. In particular:

Trust is the foundation of every successful financial advisory relationship. An adviser’s credibility is hard-earned and must be fiercely protected. When a colleague or referral partner breaches this trust, it doesn’t just damage their reputation; it directly undermines the adviser-client relationship, potentially causing irreparable harm.

Advisers must be vigilant. It’s important to choose referral partners who share a deep commitment to integrity, transparency and, crucially, an ethical framework that aligns with the Code of Ethics’ twelve standards. Colleagues must be measured by the same standards. By carefully selecting and regularly reassessing these partnerships, advisers safeguard the trust they’ve cultivated, ensuring the bedrock of their practice remains unwavering.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

———

Notes:

[1] https://hbr.org/2016/12/why-ethical-people-make-unethical-choices

[2] https://hbr.org/2019/04/the-psychology-behind-unethical-behavior

[3] https://my.afca.org.au/searchpublisheddecisions/?_gl=1*qdtfpa*_gcl_au*MTE1NDQ0NzYzMi4xNzU5OTY4NzU5

[4] Financial Planners & Advisers Code of Ethics 2019 Guide, October 2020

[5] ASIC Regulatory Guide 273, Mortgage brokers: Best interests duty

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

———