What is the practical guidance on due diligence, communication, and client protection when advising on private credit offerings?

Private credit is booming, and advisers are playing a big part in its growth.

A sector that was valued at around $133 billion[1] in size in 2021 had grown to $224 billion[2] in assets under management by 2025, an increase of almost 70 per cent in four years, catalysed by a lending pull back by banks, more generous credit underwriting, and investor appetite for income solutions with higher potential returns than traditional vehicles.

Investors can gain access to private credit exposure through various direct and indirect channels, with major investors including superannuation funds, and domestic and international asset managers. Some SMSFs and family offices have also accessed the sector directly.

Financial advisers are a major driver of this growth too, with around a third of advisers regularly allocating to the asset class, and a further 27 per cent having done so on an ‘opportunistic basis’[3].

But for all the buzz about private credit, black clouds loom on the horizon, with ASIC flagging major concerns about governance and disclosure failures it has observed among private credit providers. Their concern levels, articulated via two recently released reports – and underscored by a recent high-profile action against a provider of ‘term deposit style’ cash accounts – proved significant enough for them to announce private credit as one of their enforcement priorities[4] for 2026.

The sector is characterised by a wide variety of business models and structures, spanning credit contracts through to managed investment schemes. This in turn means the overarching compliance and disclosure framework can be a patchwork quilt of different acts and codes, making it harder for ASIC to regulate the sector and for participants to know what rules apply and when.

While private credit is far from an unregulated ‘wild west’, there is no doubt that a question mark hangs over the sector, with the failings of a few tainting the many. And whenever ASIC decides to take a look, extra vigilance on the part of advisers is advisable.

In this article, we will explore the world of private credit, examine the findings of ASICs surveillance of the sector, summarise the relevant obligations for advisers, and provide practical guidance for advisers to navigate the sector more confidently and compliantly.

What is private credit and how does it work?

Private credit refers to loans and debt investments made by non-bank institutions, often directly to businesses, property developers, or projects that fall outside traditional lending channels. These loans are typically originated and held by private credit managers. For borrowers they can allow access to funding that be hard to secure through banks. For investors they can offer access to yields that are usually higher than traditional fixed income products.

Unlike public bonds, private credit arrangements are often bespoke, involving direct negotiations between borrower and lender. Investment structures in the sector vary widely and can include:

- Pooled managed investment schemes (MIS)

- Listed or unlisted credit trusts

- Wholesale-only offerings available to sophisticated investors

- Retail credit funds, sometimes accessed through wealth platforms

Underlying loans might be secured or unsecured, and may relate to commercial real estate, small-to-medium enterprise (SME) lending, or asset-backed lending.

Many private credit offerings present themselves with features familiar to clients, for example ‘monthly income,’ ‘fixed term,’ or ‘secured’, but which can mask significant variations in liquidity, valuation practices, and credit risk.

For advisers, this means not all private credit products are created equal. Different offerings carry different fee structures, redemption mechanics, default handling procedures, and governance controls. Moreover, because the sector is not under a unified regulatory framework, disclosure obligations, trustee oversight, and reporting vary markedly across products.

The sector’s growing popularity, combined with patchy transparency and inconsistent disclosure, is precisely what has drawn the regulator’s focus. Advisers must therefore not only understand how private credit works but also ensure their clients do too, in language that makes the risks and trade-offs clear.

What ASIC ‘s observations of the private credit sector revealed

In the latter part of 2025, ASIC released two major reports into the growing private credit sector: a market review[5] (Report 814) and surveillance findings[6] (Report 820).

These investigations uncovered systemic issues in governance, transparency, and investor protection, highlighting that key segments of the market, especially those targeting retail and wholesale investors, present substantial enough regulatory concerns to warrant elevated scrutiny.

One core observation relates to conflicts of interest and misaligned remuneration.

In Rep 814, ASIC flagged widespread practices where managers retain borrower-paid fees (e.g. upfront, arrangement, or default fees) while also charging management fees to investors. In some instances, these borrower fees were not disclosed at all or were understated, raising concerns about true manager remuneration. These practices potentially create a conflict between investor’s best interests and manager incentives.

Valuation practices were another key area of concern. Many funds, especially those exposed to real estate construction and development, lacked independent quarterly valuations. Some used outdated valuations, or valuations generated internally or by related parties, undermining objectivity. Methodological inconsistencies were also uncovered:

“There is lack of clarity on whether LVR is based on cost, current value or forecast completion value. Some development sites purchased in 2021–22 are now lower in value due to building cost inflation of more than 20%. If funds are still using a 2021–22 valuation or original LVR, that value could be misleading.” ASIC Rep 814.

Across the two reports, ASIC also drew attention to portfolio opacity, finding some funds did not provide adequate disclosure about non-performing loans, credit concentration, or whether income distributions were being funded from borrower repayments, interest, or capital drawdowns. In some instances, distributions appeared unnaturally smooth given the underlying asset risk, suggestive of possible return engineering.

Terminology misuse further compounded investor misunderstanding. ASIC warned that this could give retail investors a false sense of safety, as demonstrated by the poorly understood distinction between a ‘term deposit’ and a ‘term account’. The similarity of labelling would lead many to conclude – reasonably – that they were the same, characterised by rock solid security and a government guarantee. But that is only true of term deposits. Many term accounts – including some popular with advisers – are far less secure and have underlying assets that are a mix of cash, residential mortgage-backed securities and asset-backed securities. As one analyst observed:

“[The conflation of the phrases is a deliberate marketing ploy.] The audience is not sufficiently literate to understand the risk-reward trade-off.” Ben Walsh, JP Morgan[7].

Just as ASIC has previously cautioned advisers about relying too heavily on research ratings, an emerging theme – also echoed in the Shield and First Guardian cases – is that advisers cannot rely on the ability to access an offering via a platform as indicative of suitability or endorsement.

Similarly, advisers shouldn’t rely on TMD documents as a substitute for their own due diligence. In a recent high-profile ASIC Stop Order, the provider’s description of the target market and investment timeframe was found to be problematic, as it did not reflect the risks associated with the underlying investment.

These findings underscore the need for financial advisers to exercise heightened vigilance when recommending private credit, especially to retail clients. Transparency, clear communication, and discussion about risks and trade-offs take on extra importance, as does doing their own thorough investigations about suitability.

Risks and regulatory considerations for advisers

The disparate regulatory landscape in private credit can be challenging to navigate. Sometimes the easiest approach is to go back to basics and revisit the foundational legal and ethical obligations applying to financial advisers, regardless of the product solution.

At the centre of course is the best interest duty, articulated in s961B of the Corporations Act, and requiring advisers to actively investigate and recommend only those products that are appropriate to the client’s needs, financial objectives, and risk tolerance. This includes considering product structure, liquidity, concentration risk, and valuation practices – areas where ASIC has found considerable variation among private credit funds.

Staying with the Corporations Act, and s961G, requires advice to be based on reasonable grounds, supported by due diligence that goes beyond high-level product summaries or ratings. ASIC has specifically cautioned advisers against over-reliance on external research houses, noting in REP 779:

“[Advisers] should be careful not to over-rely on advice licensee product approvals or external research ratings.” ASIC Report 779[8].

The assumption that platform-listed private credit products are vetted or low-risk has effectively been debunked by ASIC. When it comes to assessing product suitability, access and research ratings must not replace adviser due diligence and judgement.

Unfortunately, whereas many retail investment and risk offerings are homogeneous, allowing a degree of efficiency when advisers are comparing options, private credit offerings are characterised by much more variability in structure, complexity, and liquidity. Due diligence around such products is therefore likely to be a far more demanding task, where a wider range of disclosures and documents needs to be scrutinised.

The Adviser Code of Ethics[9] also reinforces these expectations. Several standards seem particularly relevant when it comes to private credit:

- Standard 2: requires advisers to act with integrity and in the best interests of each client – which demands a genuine understanding of the product, not just reliance on platform status or external ratings.

- Standard 5: compels advisers to ensure clients understand the advice and its consequences. Given ASIC’s concerns around investor confusion, especially with terms like ‘term investment’ or ‘secured’, this requires clear and proactive risk explanation.

- Standard 6: directs advisers to consider the client’s broader long-term interests and circumstances. Given the appeal of cash and income products to older, more risk intolerant investors, helping them understand how illiquid or opaque private credit exposures may affect liquidity, income reliability, and risk, seems especially critical.

- Standard 7: mandates that any remuneration or benefits received by the adviser or licensee must not compromise the client’s best interest. This is important given ASIC observations about opaque fee structures on private credit funds, which may act to incentivise product recommendations inconsistent with client objectives.

Ultimately, ASIC’s position is clear: regulatory attention is intensifying, and advisers who engage with private credit must not only understand these products in detail, but also explain them clearly, recommend them judiciously, and document their advice process thoroughly.

Wholesale v retail – the misclassification traps

Some private credit offerings are only available on a wholesale basis and herein lies another trap for advisers – the misclassification of investors as wholesale instead of retail. Classifying a client as wholesale just to access certain products, without assessing whether this aligns with their understanding, needs, and risk profile, may breach best interests’ duty. ASIC commentary in relation to the wholesale investor test, including their 2024 submission to treasury[10], reinforces the idea that meeting the test does not automatically mean the product or service is appropriate for that client and licensees must still ensure suitability and capacity.

Practical adviser guidance: due diligence client protection

As ASIC scrutiny intensifies around private credit, financial advisers must ensure robust due diligence and demonstrate alignment with client best interests. The diversity and complexity of these products mean that generic filters or assumptions such as platform access or model portfolio inclusion are not defensible demonstrations of professional analysis and judgement. Here is a simplified checklist of steps for advisers to navigate the complex landscape of private credit in a compliant, client focused way:

Product investigation and analysis

Before recommending a private credit fund, advisers should probe for specifics around:

- Asset types: Are loans secured? What sectors or geographies are being financed?

- Borrower screening: How are borrowers assessed for creditworthiness and covenant strength?

- Impairment policies: How are late payments or defaults reported and managed?

- Liquidity terms: Are redemptions gated, delayed, or subject to notice periods?

- Valuation processes: Are valuations independent, current, and transparent?

- Fees and expenses: Are there performance fees, withdrawal penalties, or hidden layers?

ASIC’s findings in REP 814 and REP 820 revealed provider performance in these areas to be variable and deserving of extra attention.

Assessing client fit

Private credit offerings can be complex and are often wrongly assumed to share the same risk and liquidity characteristics of traditional cash and income products. This means advisers must pay particular attention to assessing:

- Risk tolerance: Are clients prepared for potential delays, volatility, or capital loss?

- Time horizon: Does the investment suit clients who may need liquidity?

- Income expectations: Is the return steady, variable, or contingent on performance?

- Experience: Does the client understand credit products and how they differ from deposits?

Special caution is needed for SMSF holders and retirees, who may overestimate capital security based on familiar terminology like ‘term investment.’

Documentation and client communication

ASIC expects advisers to:

- Record analysis showing why the product suits the client’s profile and goals

- Evidence informed consent, including communication around risks, illiquidity, and volatility

- Avoid opaque language or excessive reliance on PDS extracts; use plain English and visual aids where appropriate

AFCA will not hesitate to examine whether the client truly understood the nature of the investment, even in wholesale contexts.

Ongoing monitoring

Beyond initial implementation, advisers should continue to monitor:

- Redemption delays, limits, or suspension (gate notices)

- Portfolio concentration drift

- Changes in fund governance or valuation methods

- Emerging liquidity or performance risks

- Client life events that may shift investment suitability

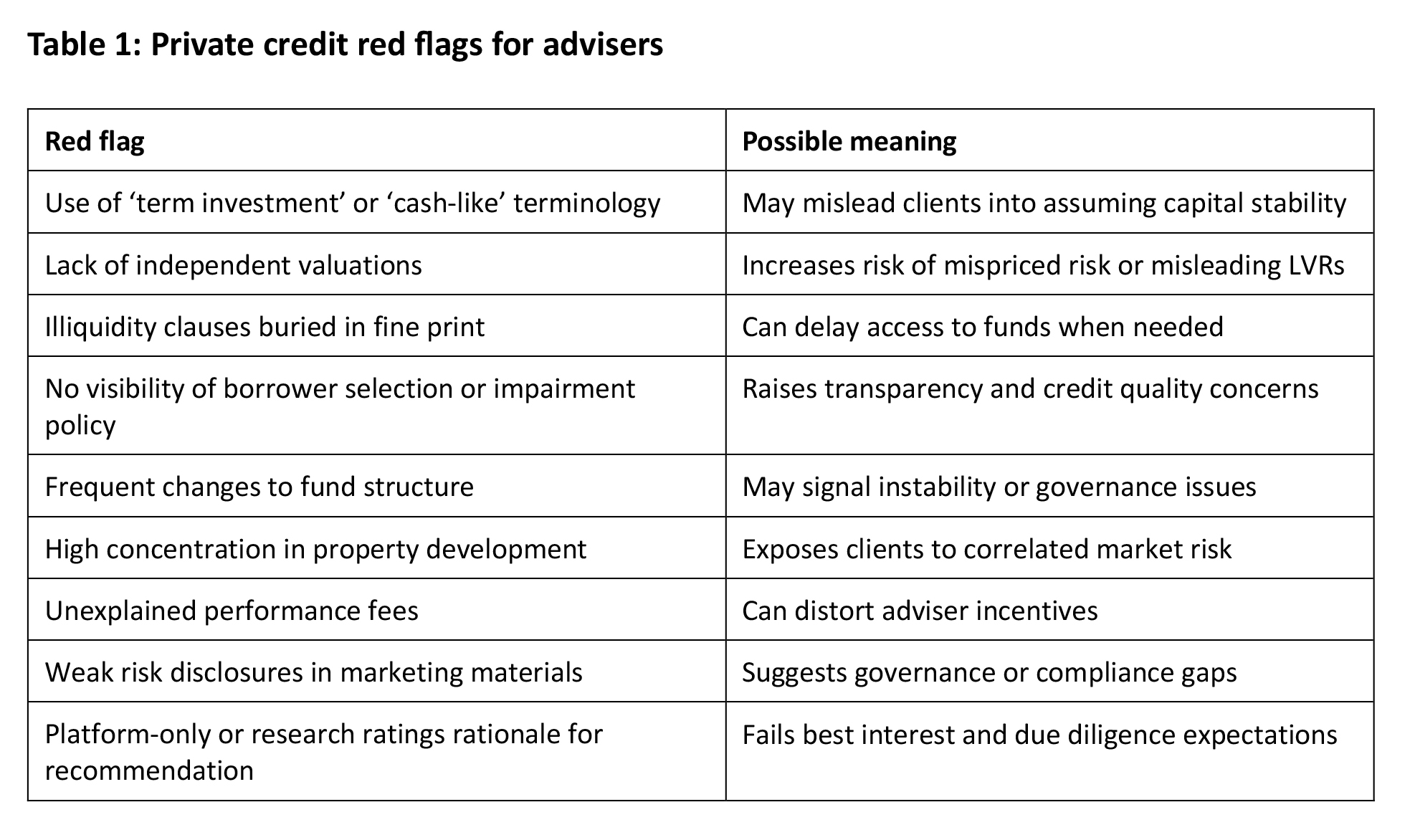

Red flags to watch out for

ASIC Reports 814, 820, along with their recent enforcement activities and media commentary, can also be distilled into a handy table of red flags and implications, giving advisers directional guidance around what to look out for when assessing private credit products:

Conclusion

Private credit is no longer a niche category, it has moved into the mainstream, with platforms, model portfolios, and advisory recommendations helping drive a multi-billion-dollar sector. But that growth has shone a light on the sector’s complexity and opacity, resulting in increased regulator concern. ASIC’s reports and enforcement actions make clear that advisers cannot assume product integrity based on platform access or research ratings alone. In an environment where fund structures, risk disclosures, and liquidity mechanisms vary widely, advisers must pay extra attention to their due diligence, communication, and documentation around private credit recommendations.

This is not to say the sector should be avoided: on the contrary there are many quality providers giving clients the opportunity to access income products that work harder than traditional vehicles (albeit with higher risk).

And for every risk highlighted in ASIC’s reviews, there is a practical adviser response, in terms of questions to ask, red flags to recognise, and conversations to have with clients.

With private credit now firmly on the regulator’s radar, this is a moment for advisers to assess their approach and arm themselves with the tools that can help reinforce their professionalism and expertise and deliver better outcomes for their clients.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Regulatory Compliance & Consumer Protection (0.5 hrs)

ASIC Knowledge Requirements: Regulatory Environment (0.5 hrs)

please log in to start this quiz

———–

References:

[1] https://axis.ausiex.com.au/articles/increased-interest-in-private-credit-as-inflation-takes-off/

[2] https://www.investordaily.com.au/markets/58101-private-credit-surges-past-224bn

[3] https://www.moneymanagement.com.au/news/funds-management/how-high-advisers-private-credit-usage-amid-asic-concerns

[4] https://www.moneymanagement.com.au/news/financial-planning/asic-flags-private-credit-misconduct-among-2026-enforcement-priorities

[5] https://www.asic.gov.au/regulatory-resources/find-a-document/reports/rep-814-private-credit-in-australia/

[6] https://www.asic.gov.au/regulatory-resources/find-a-document/reports/rep-820-private-credit-surveillance-report-retail-and-wholesale-surveillance/

[7] https://www.afr.com/wealth/investing/why-one-word-really-matters-when-it-comes-to-private-credit-20250922-p5mwx2

[8] https://download.asic.gov.au/media/dmifq31x/rep779-published-21-february-2024.pdf

[9] https://www.legislation.gov.au/F2019L00117/latest/text

[10] https://download.asic.gov.au/media/hxrizoei/202405-submission-no-62-wholesale-investor-and-wholesale-client-tests.pdf

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Regulatory Compliance & Consumer Protection (0.5 hrs)

ASIC Knowledge Requirements: Regulatory Environment (0.5 hrs)

please log in to start this quiz