Advisers can gain a clearer understanding of lifetime annuities and how they can be effectively integrated into client portfolios.

For many financial advisers, lifetime annuities have long sat in the “too hard” basket.

They’re often thought of as outdated products: with rigid structures, poor value for money and require uncomfortable client conversations about loss of control. In practice, many advisers learned to work around them – building retirement strategies almost entirely from account-based pensions, supplemented by the Age Pension where available.

It is estimated that over five million Australians planning to retire within two decades, joining more than four million already over the Age pension eligibility age of 67.[1] Yet, we have seen that take-up of lifetime income products generally remains extremely low; nearly 90% of Australians over 50 are not using – or haven’t heard of – lifetime annuities, and only 3% of retirees have secured an income stream guaranteed for life.[2]

That scepticism wasn’t irrational. The lifetime annuities of old earned their reputation.

As noted in a Firstlinks article, “Enthusiasm for annuities, coming from people who are not yet retired, overlooks these limitations… annuities offer no access to capital for unexpected expenses such as health crises or age care.

They offer no residual value to support a grieving young family, and they are not transferable between spouses. In addition, annuities offer low returns because they are usually backed by bonds to generate guaranteed income for an indefinite period. Because an annuity is a promise to pay a regular income for life, there is also the counter-party risk that the provider may not be able honour that promise over the long term.”[3]

For financial advisers focused on flexibility, control and personalised outcomes, avoidance made sense. But the retirement income landscape has changed – and so have lifetime annuities.

Understanding why advisers historically stayed clear is the first step to reassessing their role today.

A new category has emerged

Regulatory change supported the emergence of a new category of lifetime annuity, with providers such as Generation Life, AMP North, Challenger and Allianz Retire+ each bringing their own iteration to market. These solutions are most commonly referred to as market-linked or investment-linked lifetime annuities.

Unlike traditional lifetime annuities, where annual income payments were generally fixed at a set level or increased each year with CPI, investment-linked structures tie annual income to the performance of underlying investments, providing exposure to a broader range of asset classes, including growth assets. Rather than delivering on a static income profile, payments move over time in line with investment outcomes, offering a potential pathway for income growth throughout retirement.

Importantly, these solutions are not designed to replace account-based pensions. Instead, they are increasingly positioned to sit alongside them – forming part of a more diversified and resilient retirement income strategy.

The result is a different use case. Lifetime annuities are not an all-or-nothing decision, but a tool that can be incorporated within a holistic and layered retirement income strategy. Given that no two retirees are the same, the flexibility to tailor income sources across different time horizons, can help advisers design strategies that better align with individual spending needs, risk tolerances and retirement objectives.

Seven common reasons advisers have avoided annuities – revisited

Reason 1: “My client will lose their capital if they die early”

This has historically been one of the strongest objections from both advisers and clients.

All lifetime annuities offer a death benefit. Gone are the days when clients lose a significant proportion of their savings if they pass away soon after commencing an annuity.

Investment-linked lifetime annuities offer a lump sum death benefit payable to nominated beneficiaries if the policyholder passes away during an eligible Death Benefit Period. Most death benefits aim to return the difference between what was invested into the annuity and what has already been paid out as cumulative income.

Reason 2: “What if the provider can’t honour the annuity for life?”

Counterparty risk has always been front of mind for financial advisers recommending lifetime income.

An annuity is, by definition, a long-term promise. Financial advisers have rightly questioned whether any provider could safely support income payments over decades, particularly through market shocks, demographic shifts and regulatory changes.

In Australia, lifetime annuity providers are regulated by APRA and subject to stringent capital and prudential requirements designed to withstand extreme market events. In Generation Life’s investment-linked annuity structure, each investment option is separate and distinct from other investment options and from the provider’s own assets, such as the management accounts and assets of Generation Life. This means each investment option is appropriately structured for protection from potential adverse outcomes affecting either the provider or other investment options.

While no financial structure is risk-free, today’s regulatory framework and capital governance and oversight requirements are materially stronger than when many advisers first formed their views on annuities.

Reason 3: “Annuities don’t offer value for money”

Value has often been assessed narrowly, using internal rates of return or break-even periods.

Viewed through that lens, traditional annuities struggled to compete with account-based pensions in rising markets. Advisers may be worried about recommending solutions that might appear sub-optimal in hindsight if markets performed strongly or clients passed away earlier than expected.

However, value in retirement is not just about maximising returns; it is about managing risks that markets alone cannot solve — particularly longevity and sequencing risks.

Investment-linked lifetime annuities are designed to return capital as cumulative income over time, often providing higher starting income than traditional annuities. Features such as Generation Life LifeIncome’s LifeBooster [4]and LifeIncome Flex,[5] give financial advisers and their clients the optionality and flexibility to increase starting income tailored to their objectives thus, enabling clients to potentially receive their initial investment back sooner.

Importantly, these solutions can also deliver on behavioural values by improving confidence to spend and reducing the temptation to spend too little. For many clients, this form of “value” may not be fully visible in projections, but it is felt in their lived retirement experiences.

Reason 4: “Annuities are fixed income instruments”

This reason has been well founded historically. Until 2021, lifetime annuities were fixed income instruments.

Traditional lifetime annuities, where annual income is either fixed or linked to CPI changes have limited exposure to growth assets. As a result, financial advisers may often be understandably cautious about recommending products that lock clients into rigid income streams in case of constrained real growth potential.

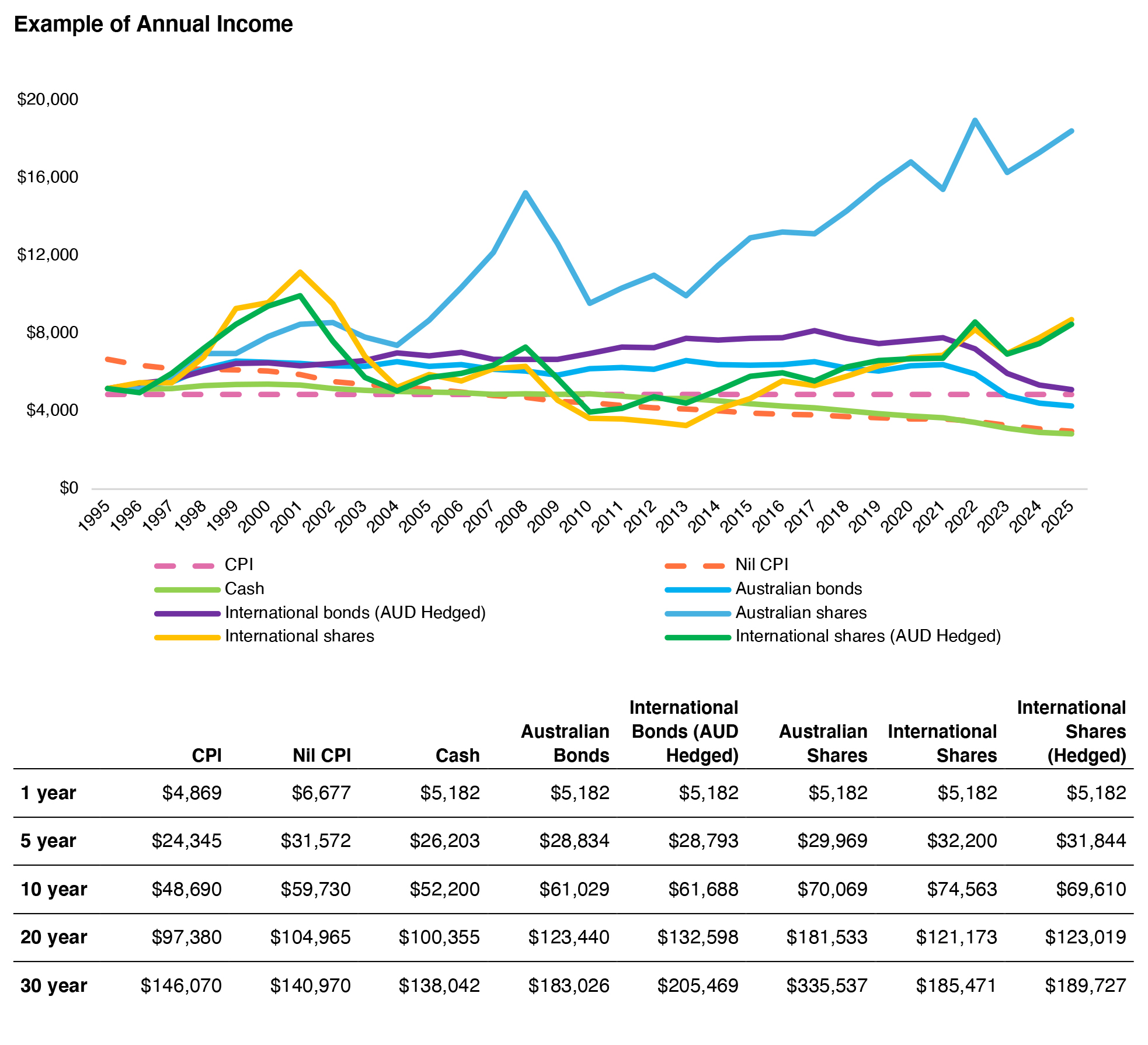

Over long-term periods of 30 to 50 years, asset classes such as Australian and international bonds, and equities have historically outpaced CPI. While past performance is not a guarantee of future returns, this highlights the importance of having exposure to growth assets as it may deliver higher cumulative income over time.

Source: Generation Life. Starting income is based on a 65-year-old female commencing an investment-linked lifetime annuity with $100,000 and an income redistribution rate of 2.5%. The graph shows the historical performance of various portfolios of an investment-linked lifetime annuity policy. Estimated fees, expenses and costs of investment-linked lifetime annuity are 1.01% p.a. No fees have been taken into account on the CPI-linked or fixed rate annuity. Past performance is no indication of future performance. This illustrates until age 95 only, however an investment-linked lifetime annuity will pay your client an income for life. The starting incomes of the CPI and Nil CPI traditional annuities are based on the rates as at 06/01/2025 commencing with $100,000. Performance of the CPI Linked Annuity is based on historical CPI of the respective period. The level of annual income from the Nil-CPI annuity does not change. However, all income is discounted by CPI of the respective period.

Investment-linked lifetime annuities address this structural limitation by linking changes in annual income to underlying investment performance, rather than fixed or CPI-indexed rates. This allows financial advisers and their clients to access diversified portfolios, including growth assets such as equities, infrastructure and private markets.

Based on the above example, an investment-linked structure may generally deliver higher cumulative income over the medium to longer term compared to traditional fixed annuities, and in many cases may return an investor’s original capital through cumulative income sooner.

Income may rise or fall year to year, but over longer periods, the above is an example of how an investment-linked annuity can provide a pathway for income growth that better supports retirements that may span 30 years or more.

Case study: Comparing a traditional lifetime annuity with an investment-linked lifetime annuity

Meet Karlee and Adam. They are both 65 and entering retirement.

Karlee and Adam would like a reasonable income stream that is sustainable and positioned to grow in line with their living costs. They currently have a combined superannuation balance of $1,100,000 and $10,000 in personal assets.

They would like to spend $100,000 per annum to retire comfortably, with their income increasing over time to keep pace with their living costs.

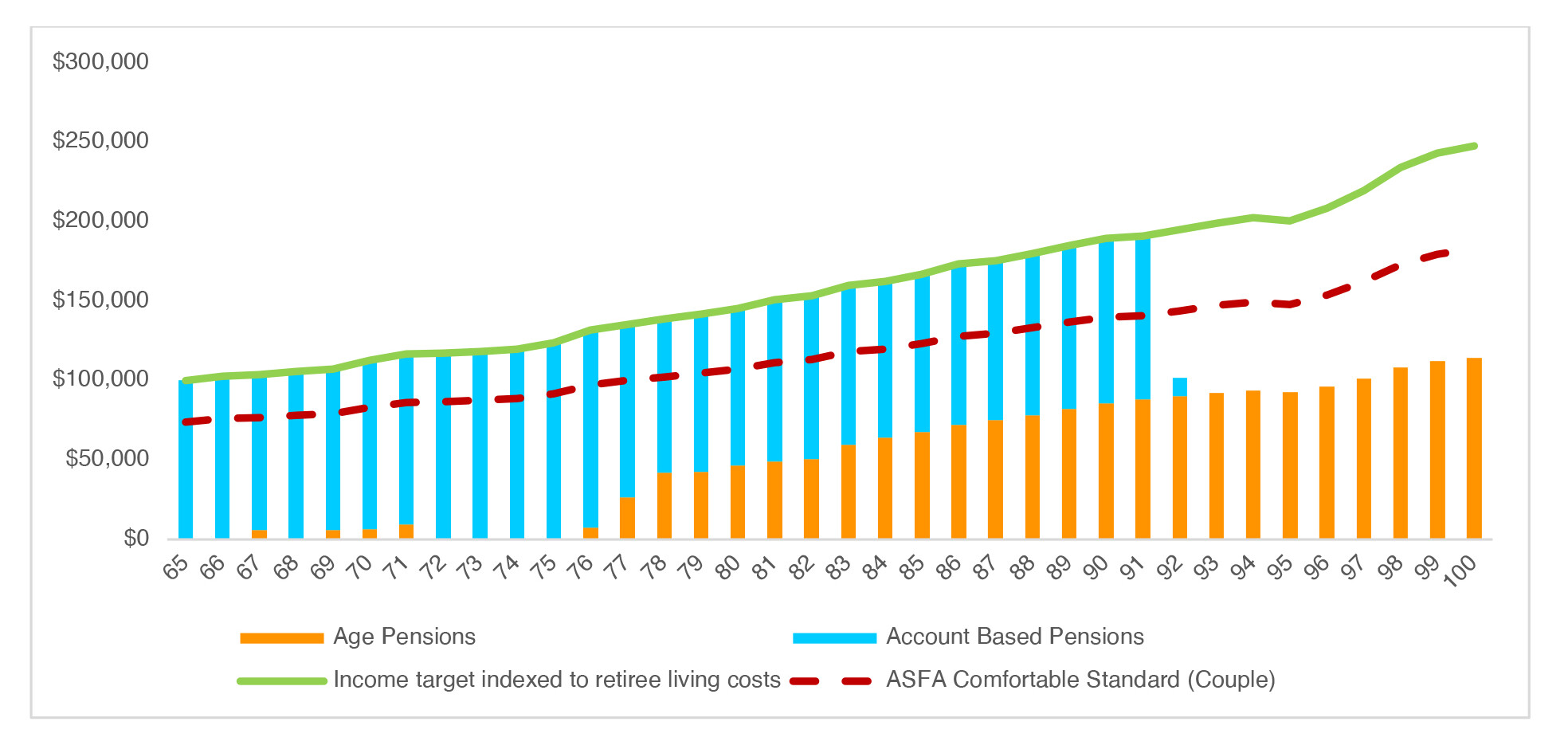

If solely relying on account-based pensions

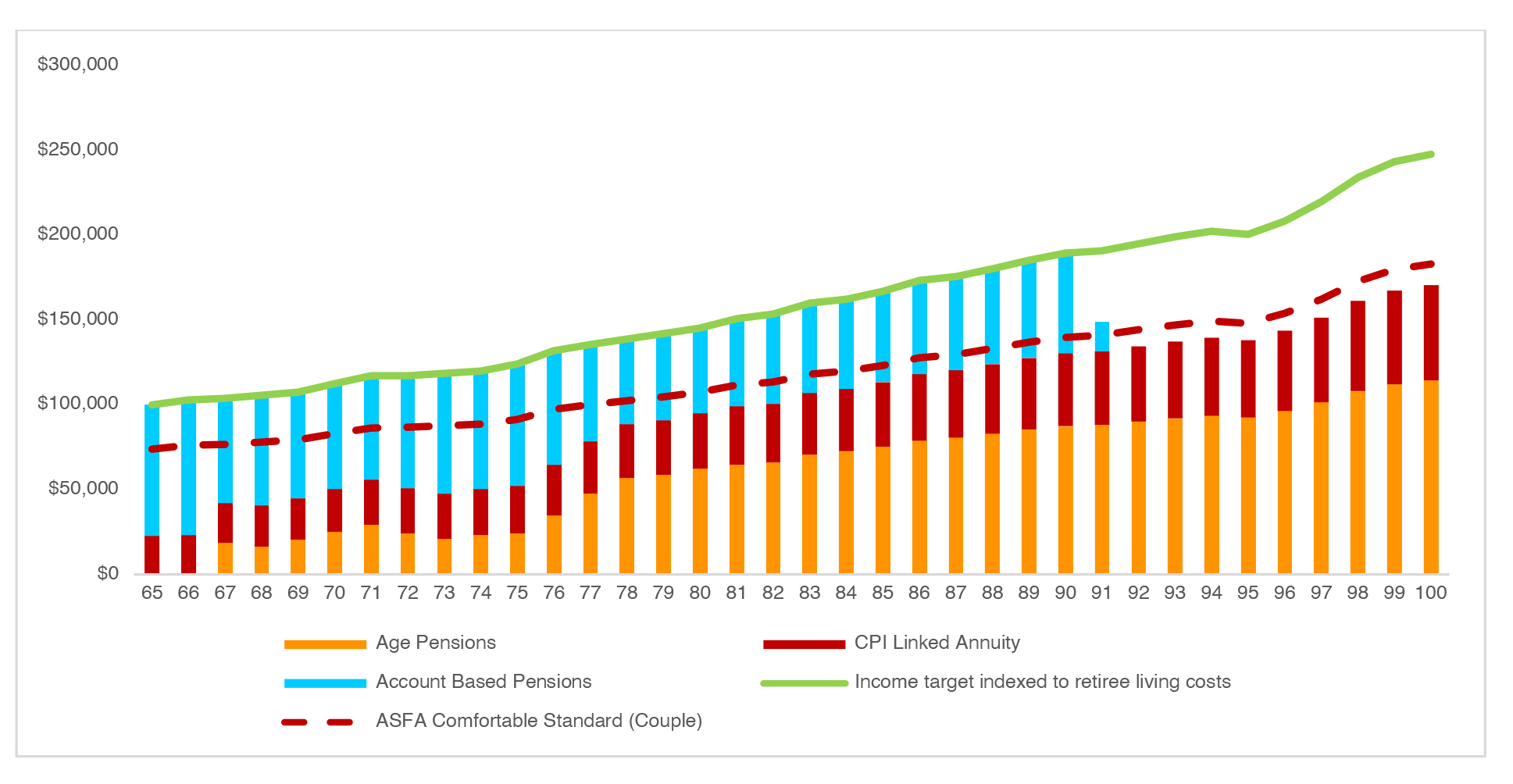

Income layering by combining a traditional lifetime annuity and account-based pensions

A traditional lifetime annuity provides a regular income guaranteed for life that is indexed to CPI (in this example). To meet their annual income target, additional drawdown, above the minimum level, from your account-based pension is required. Due to the concessional social security treatment of the annuity, ?they may receive immediate access to the Age Pension if eligible.

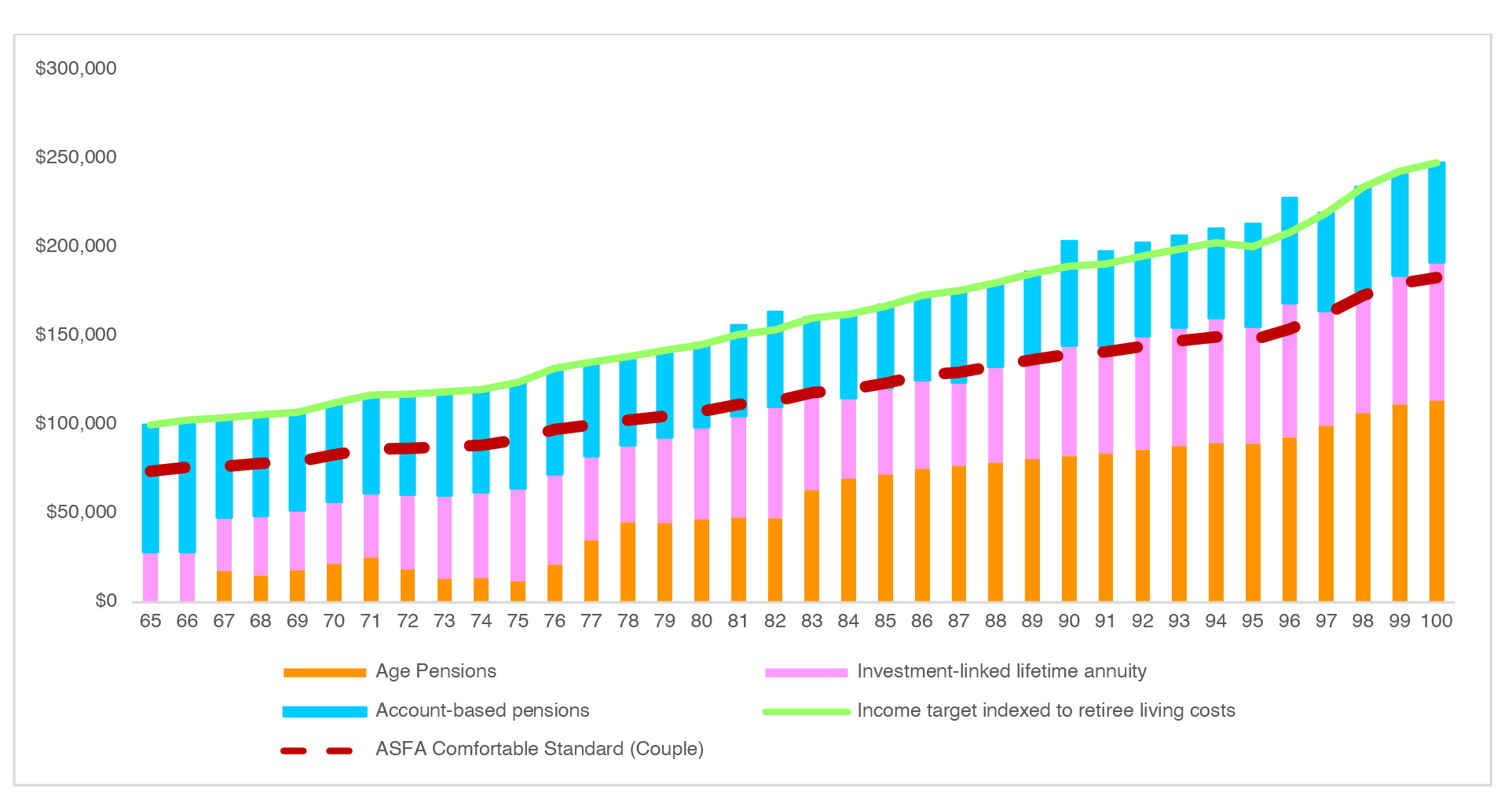

Income layering by combining an investment-linked lifetime annuity and an account-based pensions

An investment-linked lifetime annuity provides them access to assets that can help grow their annual income over time. This means they can potentially drawdown less from your account-based pension to meet their annual income target. Due to the concessional social security treatment similar to a traditional lifetime annuity, they may receive immediate access to the Age Pension if eligible.

Source: Generation Life. Based on a 65 year old couple with a starting superannuation balance of $1,100,000, $10,000 in personal assets and own their own home. Target annual income and the ASFA Retirement Standard are indexed based on historical changes in the CPI from 1991 to 1998, and the Retiree Living Cost Index from 1998 to 2025, as published by the Australian Bureau of Statistics (ABS). The ASFA Retirement Standard used is ‘comfortable lifestyle’ for a couple as at September 2025. Allocating 40% of the superannuation balance to a CPI-linked annuity based on rates available in January 2026 and an investment-linked lifetime annuity selecting an income redistribution rate of 5%. Account-based pension drawdown amount is to meet the target income, minimum drawdowns do apply. Annual income illustrations are shown in nominal dollars. Age Pension rates and thresholds are effective 01/01/2026. The illustration uses historical investment returns commencing 1st July 1991. Investment-linked lifetime annuity portfolio using back-tested returns of a portfolio consisting of 34.7% Australian shares, 38.39% international shares, 24.72% global fixed interest assets, 1.47% cash and 0.72% other assets. Allocating 60% of the superannuation balance into an account-based pension invested into a 70/30 diversified index portfolio which consists of a 30% allocation to ASX All Ordinaries, 40% to MSCI World Ex Australia Index, 20% to Bloomberg Global Aggregate Bond Index (AUD Hedged) and 10% to Bloomberg Ausbond Composite Index. Estimated administration costs of 0.30% p.a. for the account-based pension and 0.92% p.a. for the investment-linked lifetime annuity (there are no fees on income from the investment-linked lifetime annuity in the first financial year). Past performance is not a reliable indicator of future performance.

In this example, by allocating 40% of their superannuation balance to an investment-linked lifetime annuity, Karlee and Adam are projected to retain an account-based pension balance of $206,455 at age 100 — providing them with the flexibility to either increase spending in retirement or leave a legacy.

Compared to investing in a traditional lifetime annuity where annual income is indexed to CPI, this strategy is also projected to deliver an additional $199,826 in Age Pension benefits and $1,211,355 in cumulative income (without drawdowns?) by age 100.

Reason 5: “They’re too complex for clients to understand”

Lifetime annuities have often been perceived as complex, opaque and difficult to explain, especially when compared to the relative simplicity of account-based pensions.

In reality, much of the complexity sits in product design and pricing, not in client experience. Once established, the core proposition is straightforward: exchange a lump sum for income payable for life, with income movements linked to investment outcomes.

For advisers, the key shift has often been positioning annuities as part of a broader strategy, rather than a standalone decision. When framed as one income layer within a retirement portfolio alongside account-based pensions and the Age Pension, client understanding and acceptance tends to improve significantly.

Reason 6: “Tax makes them unattractive”

Tax uncertainty has also contributed to adviser hesitation.

In practice, lifetime annuities receive concessional tax treatment. Earnings whilst within the structure are generally tax free and can benefit from franking credits.

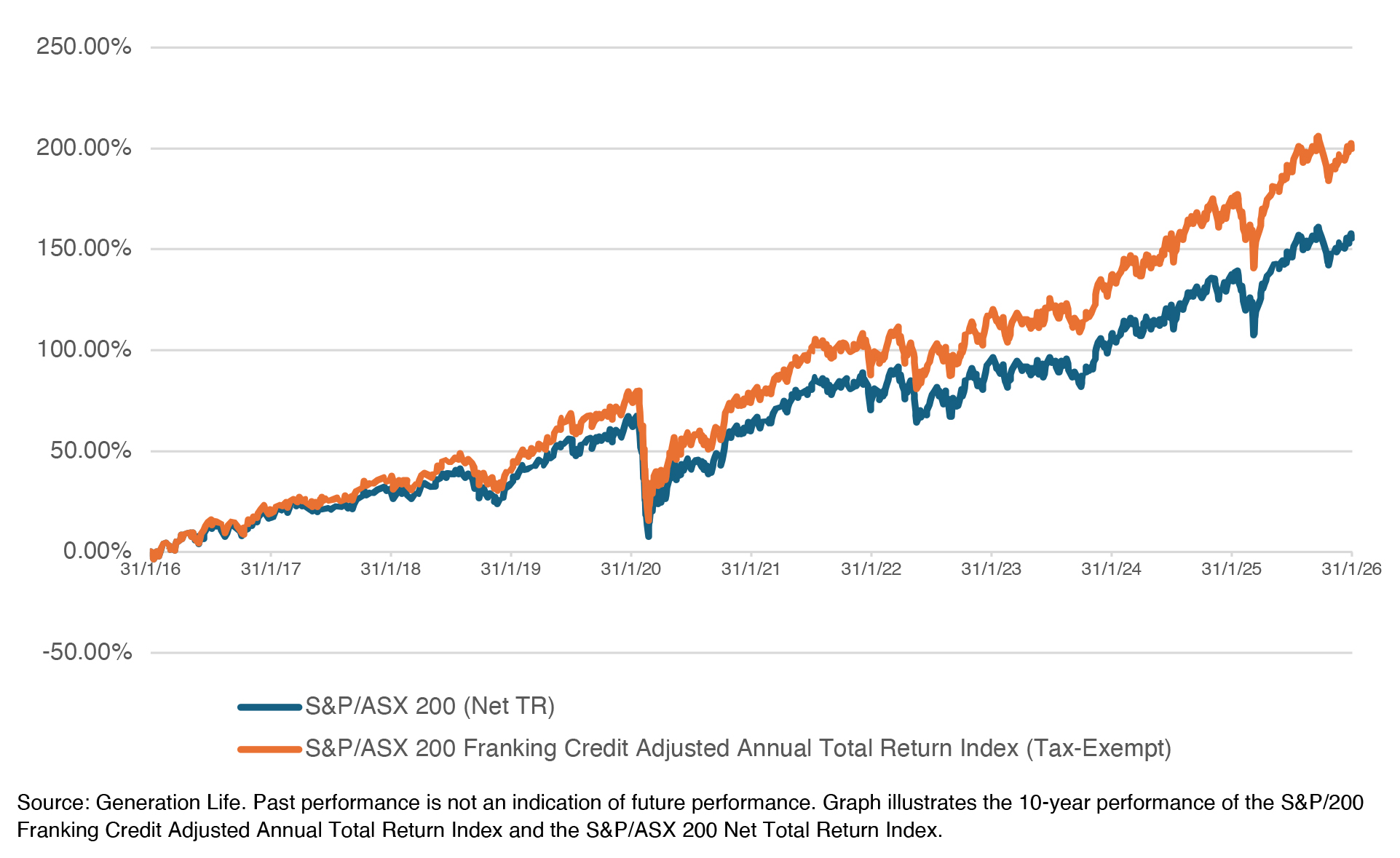

Example: The power of a tax-exempt environment

The annualised return of the S&P/ASX 200 Total Net Return Index was 9.12% over the past decade.

When you add the Franking Credit Adjustment, which applies to the tax-exempt environment, the annualised return is 10.99%. This represents an uplift of 1.87% in annualised return.

Source: Generation Life. Past performance is not an indication of future performance. Graph illustrates the 10-year performance of the S&P/200 Franking Credit Adjusted Annual Total Return Index and the S&P/ASX 200 Net Total Return Index.

There are tax benefits on the income payments too. Income payments are tax-free if using superannuation and are at least 60 years old. In all other cases, there are tax concessions on the regular payments.

In addition, lifetime annuities can interact favourably with social security means testing, potentially improving Age Pension outcomes or access to benefits such as the Commonwealth Seniors Health Card.

While tax outcomes are always client-specific, this area is often misunderstood rather than unfavourable.

Reason 7: “Annuities are inflexible and set-and-forget”

Perhaps the most persistent myth is that annuities lock clients into rigid, irreversible decisions.

While this was once largely true, modern lifetime annuities offer far greater flexibility than their predecessors. Many now allow investment switching, different income profiles, reversionary beneficiaries, varying payment frequencies, and integration with both superannuation and non-superannuation assets.

Providers such as Generation Life, demonstrate how these features can be combined to support more nuanced client scenarios including couples, phased retirement and changing income needs over time.

Importantly, there is no one-size-fits-all approach. Retirees are different, and individual circumstances vary from person to person. Circumstances also change throughout retirement. It is not a single decision made at one point in time, but a series of small, interconnected choices that shape a member’s confidence, readiness, and lifestyle outcomes.

Investment-linked lifetime retirement solutions also create meaningful financial adviser touchpoints, prompting timely client conversations and equipping financial advisers with the right information at the right moment, strengthening relationships and reinforcing the adviser’s ongoing value.

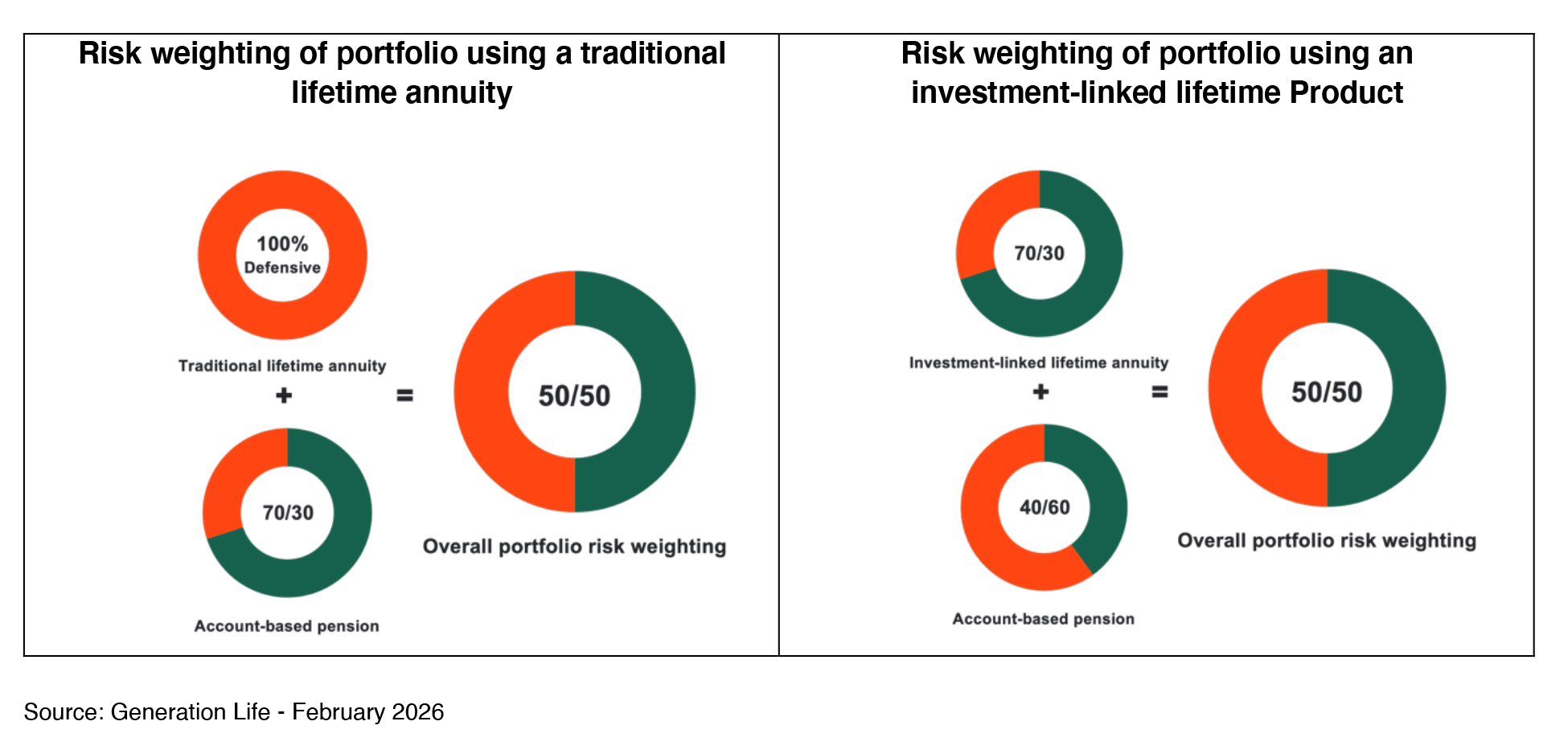

Example: Complementing risk profiles across retirement income streams

By combining an investment-linked lifetime annuity with an account-based pension, advisers can structure retirement income streams with different risk profiles while maintaining a consistent overall portfolio risk. Rather than viewing risk at the product level, this approach reframes risk at the portfolio level.

For example, consider a retiree allocating $300,000 to a lifetime annuity and $700,000 to an account-based pension.

When a traditional lifetime annuity is used, the annuity allocation is typically backed by defensive assets, requiring the account-based pension to carry a higher proportion of growth assets to meet income objectives. While the combined portfolio may still appear balanced, the growth is concentrated in the account-based pension.

By contrast, an investment-linked lifetime annuity allows growth assets to sit within the guaranteed income layer itself. This can improve income sustainability without increasing the total portfolio’s overall growth/defensive weighting.

There may also be social security advantages in using growth assets within an investment-linked lifetime annuity. This is because the assets test assessment is locked in on the starting balance, regardless of subsequent growth. In contrast, any growth in an account-based pension balance is assessed, which may lead to reductions in Age Pension payments.

The structural advantage is not about taking more risk, but about distributing risk more efficiently across income sources. Growth exposure within the lifetime annuity can support higher and more sustainable income, while the account-based pension can be positioned more conservatively, reducing sequencing and behavioural risk.

For advisers, this highlights the value of investment-linked lifetime annuities as a portfolio construction tool, enabling more flexible income layering and more resilient retirement outcomes

From products to purpose

What is even more powerful than the product changes, is the adviser problem being solved.

Advisers are increasingly dealing with retirees who underspend, de-risk too early and carry persistent anxiety about running out of money. In this context, income guaranteed for life can play a behavioural role as much as a financial one.

Used appropriately, lifetime annuities can help secure essential spending, reduce pressure on high-risk growth assets and give clients greater confidence to use their savings earlier in retirement.

They are no longer about replacing flexibility – but enabling it elsewhere in the portfolio.

A reframed question for financial advisers

The question is no longer “Why would I recommend an annuity?” It is “Which risks does this client need help managing and over what timeframe?”

For some retirees, the answer will still be “none”. For others, a measured allocation to lifetime income may meaningfully improve confidence, sustainability and outcomes. According to Accurium Confidence for Life: A retirement advice framework report,[6] it is estimated that solutions like Generation Life LifeIncome can provide up to a 41% boost in confidence that retirement spending would last for life[7] — giving retirees more peace of mind.

Lifetime annuities haven’t suddenly become a default solution. But in a more complex, longer retirement, they have become relevant again as part of a broader, adviser-led strategy.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Retirement (0.5 hrs)

please log in to start this quiz

——–

Notes:

[1] Deloitte (2024). ‘To close the financial advice gap, we must first appreciate how it can help us’. https://www.deloitte.com/au/en/Industries/financial-services/blogs/close-financial-advice-gap-how-it-can-help-us.html

[2] Based on results from the surveys referred to on page 8 and /or at Source 3 of the Generation Life Reimagining Legacy Guide 2023.

[3] Firstlinks. (2025). ‘Retirement is a risky business for most people. ‘ https://www.firstlinks.com.au/article/retirement-is-a-risky-business-for-most-people

[4] https://genlife.com.au/investor-strategies/building-wealth/more-income-in-the-early-years-when-you-need-it-most

[5] https://genlife.com.au/investor-strategies/building-wealth/lifeincome-flex-created-with-australian-retirees-spending-needs-in-mind

[6] https://www.accurium.com.au/confidence-for-life/

[7] Increase compared to that achieved in a strategy with an account-based pension alone. According to Accurium Confidence for Life: A retirement advice framework report

Generation Life Limited (Generation Life) AFSL 225408 ABN 68 092 843 902 is the product issuer. This communication is general in nature and does not consider the investment objectives, financial situation or needs of any person and is not intended to constitute personal financial advice. Any superannuation general financial product advice provided is by Generation Development Services Pty Limited ABN 14 093 660 523 as Corporate Authorised Representative No. 001317211 of Evidentia Financial Services Pty Ltd AFSL 546217. The product’s Product Disclosure Statement (PDS) and Target Market Determination (TMD) are available at www.genlife.com.au and should be considered before making an investment decision. Superannuation products’ PDSs, offer documents and TMDs are available via the websites of their product issuers. Professional financial advice is recommended. Generation Life, GDS and Evidentia do not make any guarantee or representation as to any particular level of investment returns. Generation Life does not accept any responsibility or liability for superannuation general financial product advice provided by GDS. Generation Life, Evidentia and GDS believe that the information provided is accurate and reliable, but no warranties of accuracy, reliability or completeness are given (except insofar as liability under any statute cannot be excluded), and exclude to the maximum extent permitted by law, any liability (including for negligence) that might arise from the information or any reliance on it. Statements that are non-factual in nature, including projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions, all of which are subject to change. Investments carry risk. Past performance is not an indication of future performance.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Retirement (0.5 hrs)

please log in to start this quiz——–