How do advisers work with vulnerable clients, particularly those affected by ageing and cognitive decline?

This article, proudly sponsored by GSFM, examines how advisers work with vulnerable clients, particularly those affected by ageing and cognitive decline. Part two focuses specifically on the rising incidence of elder abuse and the practical application of the Code of Ethics.

As highlighted in part one of this CPD series, vulnerability is a growing issue for Australians. Our nation’s demographic trajectory makes an increase in vulnerable clients unavoidable and, statistically, an increase in clients at risk of financial abuse inevitable.

Financial abuse is unfortunately common and accounted for 30 percent of allegations reported to the NSW Ageing and Disability Commission between 1 July 2019 and 31 March 2025[1]. The seriousness of this issue has resulted in the Financial Elder Abuse Project, an initiative of the Australian Human Rights Commission, which aims to strengthen the financial safety of older Australians. Running from 2024-2026, the project brings together representatives from the banking, financial, legal and community sectors to improve the prevention of, and response to, financial elder abuse[2].

Defined as ‘the misuse or theft of an older person’s money or assets’, financial elder abuse can cover a broad spectrum of behaviours, sometimes described as existing in the grey area between thoughtless practice and outright theft. It’s important to note that while all vulnerable clients may be at risk of financial abuse, it is most prevalent among the elderly.

The Financial Elder Abuse Project is being championed by Age Discrimination Commissioner Robert Fitzgerald AM who believes the risk factors contributing to financial elder abuse are likely to increase in the next 20-30 years, including the issue of inheritance impatience.

The risk factors noted by the Age Discrimination Commissioner include:

- the growing ageing population, with people living longer and healthier lives

- the largest intergenerational wealth transfer in history

- growing economic pressures, such as the rising cost of living, lack of affordable housing and low wage growth.

As an adviser, you are in the box seat to serve as frontline defenders to bridge the gap between financial management and safeguarding the personal autonomy of your clients. As will be explored in greater detail in this article, your role includes the proactive identification of risks by monitoring for red flags as identified by the Australian Financial Complaints Authority (AFCA).

Beyond technical oversight, you are uniquely positioned to engage in meaningful conversations with older clients and their families and facilitate transparent family meetings that clarify the client’s wishes. By acting as an objective third party, you have an opportunity to normalise the discussion of protective measures such as Enduring Powers of Attorney (EPOA) protocols to ensure that family involvement remains supportive rather than exploitative.

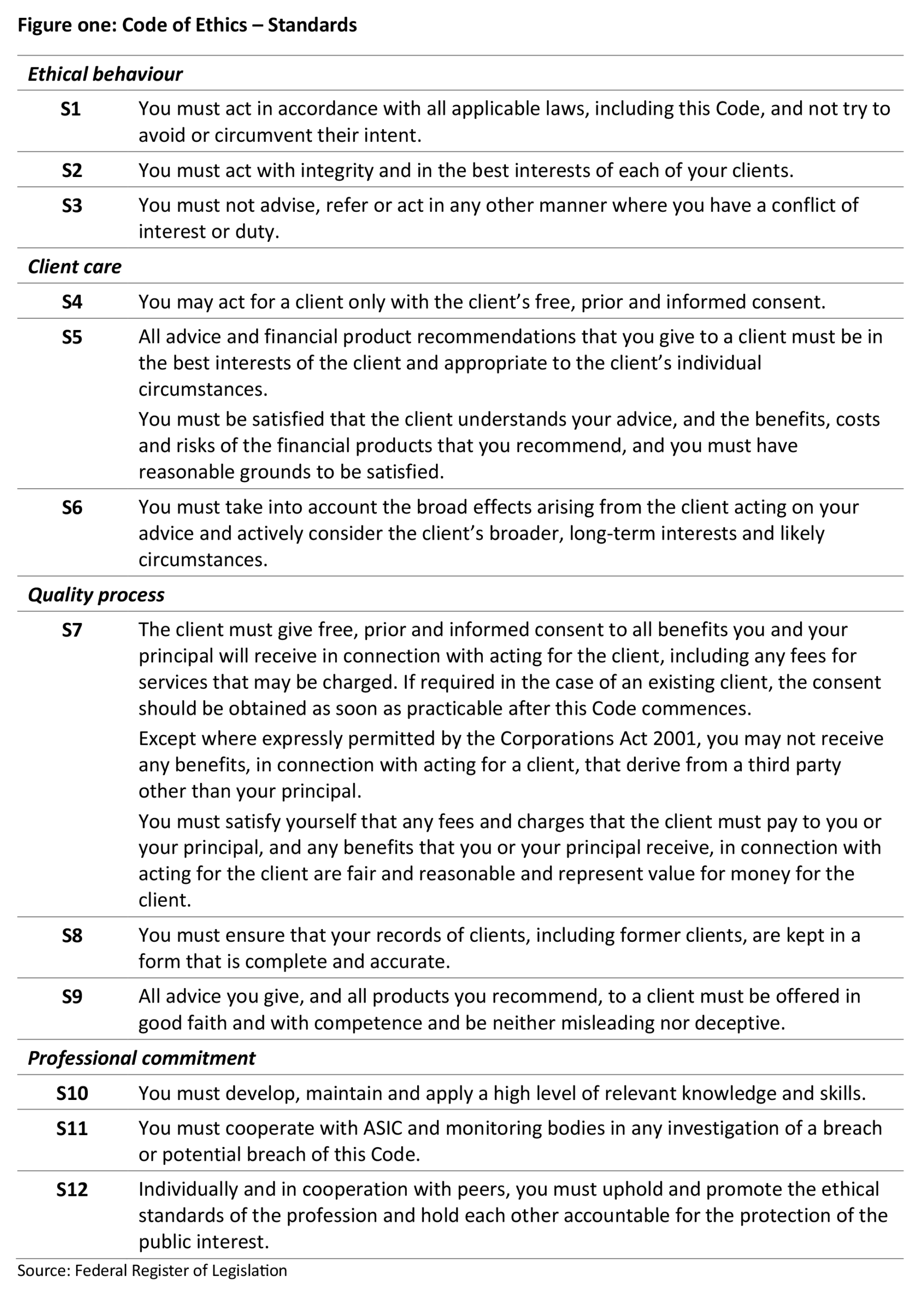

To ensure ongoing compliance with the Financial Planners and Advisers Code of Ethics 2019 (Code of Ethics) and its twelve standards (figure one), it is important that advice practices have strategies to define, identify and manage potential cases of elder financial abuse.

Financial elder abuse: definition, prevalence and forms of abuse

Definition

Elder abuse, as a broad concept, is defined by the World Health Organization (WHO) as:

“A single or repeated act, or lack of appropriate action, occurring within any relationship where there is an expectation of trust which causes harm or distress to an older person.”

Elder abuse typically takes several forms, and some individuals may be subject to one or more of these:

- Psychological abuse

- Physical abuse

- Financial abuse

- Social abuse

- Sexual abuse

- Neglect

Elder abuse can have serious physical and mental health, financial and social consequences. These can include physical injuries, premature mortality, depression, cognitive decline, financial devastation and placement in aged care facilities.

The Financial Services Council (FSC) defines elder financial abuse as:

‘Any activity by an individual that seeks to use fraudulent, illegal, deceptive or otherwise improper acts or processes to advantage from the financial resources of an older or elderly individual.’

In this definition, advantage can include:

- personal profit or gain

- enabling profit or gain for a relative, friend, spouse or business associate

- deprivation of the right of an older or elderly individual to benefits, resources, belongings or assets for any reason.

Prevalence

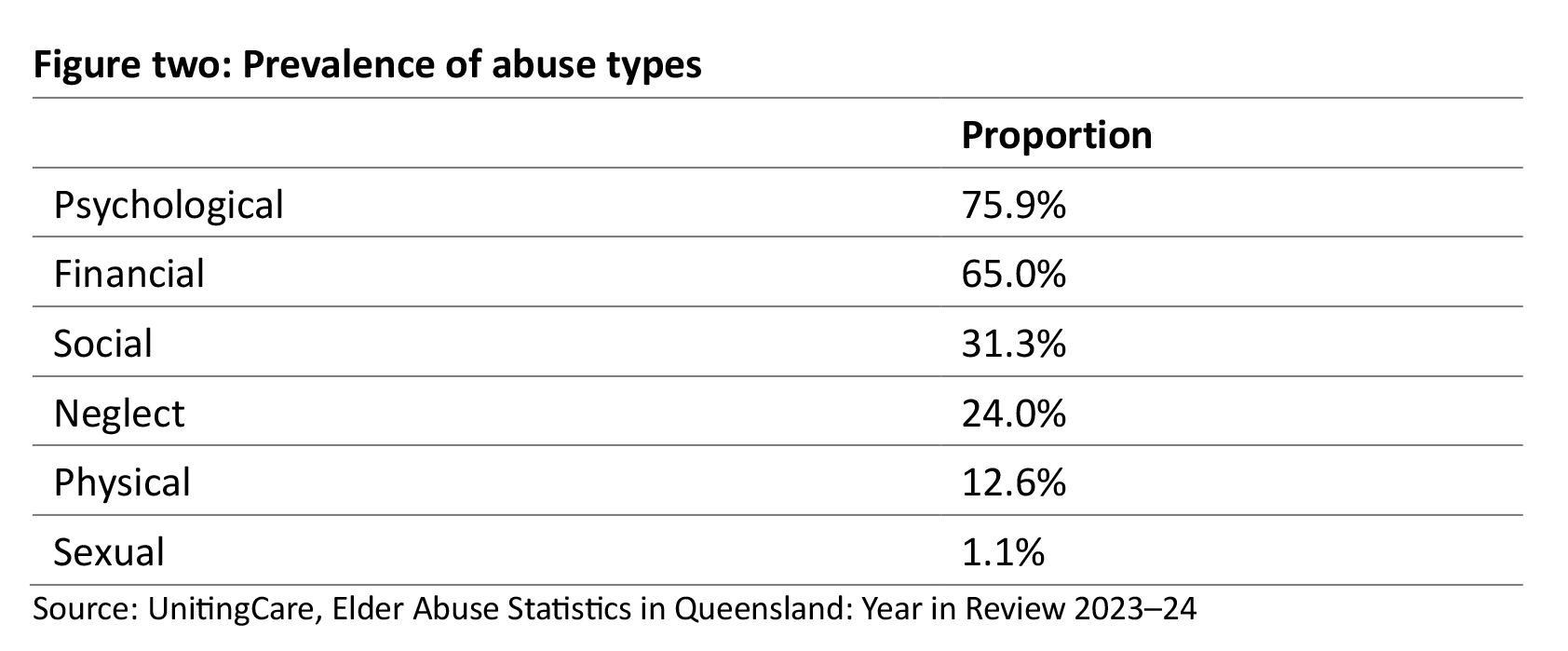

While several reports are currently in train, the most recently published show financial abuse to be the second most common form of elder abuse; disturbingly, 69.5 percent of victims experienced more than one type of abuse.

however, as highlighted by the Age Discrimination Commissioner earlier in this article, circumstances suggest that instances of financial elder abuse are expected to increase.

AFCA notes[3] the following risk factors may increase the likelihood of elder abuse:

- limited digital literacy

- language barriers

- geographical or social isolation

- cognitive impairment

- reduced mobility, vision, or hearing

- physical dependence on another person for care or help with tasks.

Forms of financial abuse

Elder financial abuse can take many forms. Your experience as a financial adviser is likely to vary from experiences across other financial services such as banks or insurers.

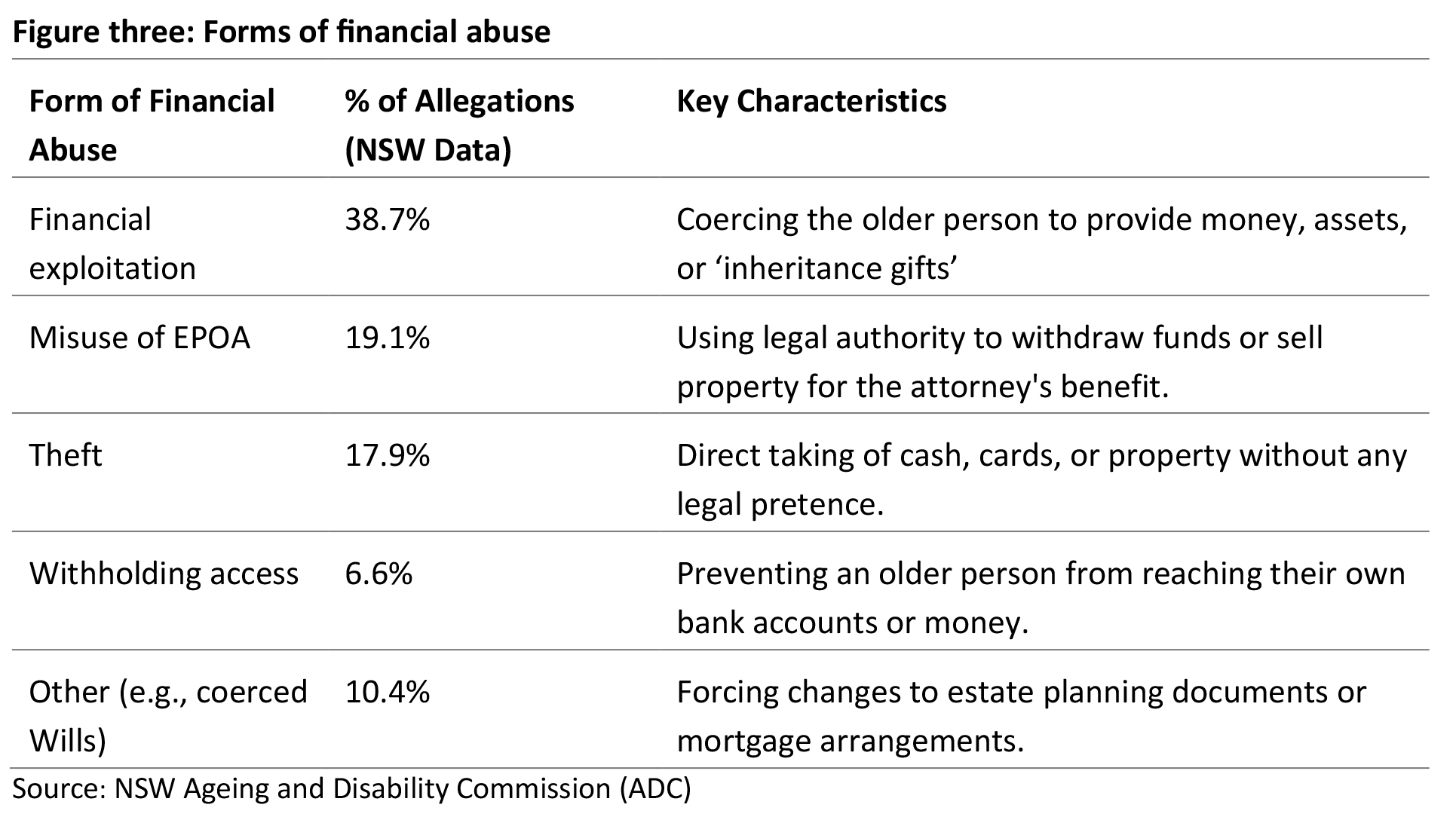

The NSW Ageing and Disability Commission (ADC) recently released a granular breakdown of financial abuse allegations, revealing that exploitation and the misuse of legal authority are the most dominant types of abuse.

Recent research has identified three specific ‘modern’ methods of financial abuse:

- Coerced ‘Granny Flat’ arrangements[4] – whereby a family pressures an older relative to sell their home and fund the construction of a granny flat on the child’s property, often without a legal contract. If the relationship breaks down, the older person is left homeless and without their original capital.

- Technology-facilitated abuse – the perpetrator exploits the older person’s digital illiteracy and gains access to banking apps, passwords and MyGov accounts. A 2025 study found that men are statistically more likely to experience this form of tech-based financial control than women[5].

- Tax and business exploitation – this involves unwitting tax fraud, where family members list an older person as a director of a shell company or use their Tax File Number to claim fraudulent refunds or shift business debts[6].

Ethics and financial elder abuse

Elder abuse can be an ethical minefield. You may have older clients at risk of financial abuse and you need to be alert to red flags. It’s hard to meet the basic ethical requirement – to always act in the client’s best interests – if you don’t act to protect your clients from potential (or actual) financial abuse.

Ethical considerations include:

- Avoid conflicts of interest, particularly in situations where two generations of a family are clients

- Avoid contributing to the perpetration of unlawful acts

- Ensure all clients are well informed; as clients age, ensure they understand what constitutes elder abuse

- Ensure your client understands the advice, and has capacity to act

- Be respectful – after all, just because a client is old does not mean they’re not able to make valid financial decisions

- Your client’s best interests come first.

In its updated approach to financial abuse of older people, AFCA expects that where a financial firm sees warning signs that an older person might be experiencing financial abuse, it will take steps to ensure the person is making an independent and informed decision. It further notes the importance of distinguishing signs of potential financial abuse of an older person from a decision freely made by an older person who has capacity to do so.

Warning signs of elder abuse

AFCA has observed the following warning signs in complaints involving financial abuse of older people, but notes that it is a non-exhaustive list.

An older person may:

- Engage in financial activity that is unusual or inconsistent with their long-standing patterns of financial activity

- Be accompanied by someone who appears to pressure them into making financial decisions

- Have a third party speak on their behalf, including in situations involving language barriers

- Ask for communications to be sent to a third party, especially when that person is not formally authorised

- Appear fearful (particularly of the person accompanying them) or withdrawn

- Not understand or be aware of recent financial decisions (e.g. they are confused about why they are being asked to consent or sign a document)

- Sign a guarantee of a company’s loan when they were not encouraged to obtain independent financial or legal advice about the guarantee

- Be unable to explain, or appear confused about, their financial products or decisions

- Register for online services despite having no prior history of online interactions

- Express concerns about missing funds or financial documents.

Where these or other signs arise, AFCA states that financial firms should make further inquiries and proceed with caution. This may include delaying the processing of a customer’s request or taking other preventative steps.

In a situation where a financial firm has reasonable cause to suspect financial abuse, they should not require evidence before escalating the matter or considering what safeguards may need to be put in place.

When considering the appropriateness of a financial firm’s response, AFCA will consider whether it took timely preventative, supportive and restorative action without first placing a burden on the customer to provide further information. Any additional safeguards introduced should be proportionate and sensitive to the older person’s circumstances – for example, it would not be appropriate to ask someone with limited digital literacy to use online portals.

AFCA general principles for dealing with financial abuse

AFCA’s approach aims to align with community expectations and good industry practice, including meeting industry codes of practice, such as the Code of Ethics, in relation to elder financial abuse. This approach includes the following general principles:

- Consider the context – understand older people experiencing financial abuse are likely to be experiencing considerable stress and may need additional care. Financial firms should take a flexible approach and tailor support options to each customer’s unique circumstances and needs.In complaints, AFCA considers whether financial firms should have been aware of the potential warning signs of financial abuse.

- Engage with care – engage with the older person with sensitivity, dignity, respect and compassion. This may include referring them to services with specialist training and experience.In complaints, AFCA considers whether the financial firm exercised its role with reasonable care and skill, identifying and responding to warning signs of abuse that emerge from engagement with its customer.

- Prioritise safety and agency – the safety and wellbeing of the older person must be a priority in the firm’s communication, documentation and financial and account arrangements. This includes accepting an older person’s disclosure of financial abuse at face value and working with the older person to provide information in an accessible and flexible way.In complaints, we consider whether the financial firm should have taken precautions or other preventative action when warning signs of abuse were present.

Assessing client vulnerability

Today’s landscape of shifting family dynamics and complex wealth transfers highlights the importance of establishing a thoughtful process to identify and support vulnerable clients. This isn’t simply about meeting regulatory requirements; it is about honouring the trust your client has placed in you to safeguard their hard-earned legacy and independence.

One way to do this is to develop a simple checklist to be used when meeting with older and/or vulnerable clients. As well as being the right thing to do for potentially vulnerable clients, it can help you meet your ethical requirements. Such a checklist could include sections on:

- Identifying vulnerabilities – type of vulnerability, signs of reduced understanding or inconsistent instructions or the recent life events that may have occurred.

- Clients’ comprehension and ability to provide informed consent – for example, the client being able to demonstrate understanding, and adequate time was allowed for reflection and follow-up questions.

- Your communication approach – did you adapt language and pace to the client’s capacity, your use of plain English, repetition or visual aids where needed.

- Presence of family members, carers or other third parties – were the client’s views clearly distinguished from the input of others, did you assess the risk of undue influence and in the case of EPOA involvement, was it aligned with client’s welfare and wishes?

- Appropriateness of advice – measured in relation to the client’s capacity as well as goals, would you be comfortable defending that advice under ethical scrutiny?

- Ethical red flags – did you experience discomfort or unease about proceeding and if so, did you consider the risk of financial elder abuse and evaluate any potential harm to your client’s dignity, independence or security?

- Documentation and escalation – where appropriate, did you document ethical reasoning or discuss concerns with peers or licensee? Should you pause, decline or escalate advice and related issues?

By weaving empathy-led vulnerability checks into your advice process will better help you identify subtle changes in a client’s wellbeing before a crisis unfolds. A proactive, compassionate approach can build on your trust relationship and ensure vulnerable clients have a professional ally.

It’s important to ensure that, practice wide, advice reflects the spirit and intent of the Code of Ethics. That is, client wellbeing is always prioritised over technical or commercial outcomes and any action taken would withstand public and professional scrutiny.

Case studies

The following case studies are loosely based on those published by ASIC and AFCA. Names of people and places have been changed.

Case study one: Due diligence

Martin sought compensation for a series of withdrawals totalling $737,000 that he had made from his account-based pension. He had made the withdrawal requests himself. Martin told his adviser, Mark from ACME Advice, that the funds were being used for personal matters, to support family members and to cover his living expenses.

After the funds had been withdrawn, Martin’s daughter advised Mark and ACME Advice that her father had been the victim of a sophisticated scam. She argued that Mark (and ACME Advice) should have recognised the signs of financial abuse and intervened. She made a formal complaint to AFCA.

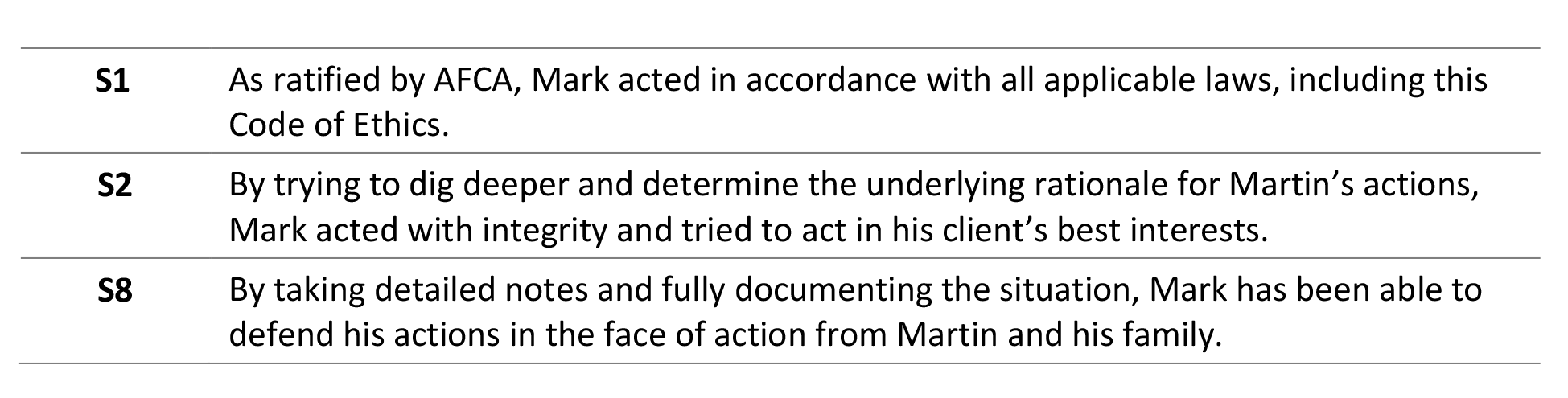

AFCA found that Mark went above and beyond his duties in attempting to assist Martin. His contact notes and contemporaneous records demonstrated that the adviser had:

- made repeated enquiries about the purpose of the withdrawals

- expressed concern for Martin’s wellbeing

- encouraged him to seek legal advice

- offered to provide personal financial advice.

Martin declined each of these offers. Consequently, AFCA found that Mark and ACME Advice had met their obligations under the law, including the Code of Ethics. The transactions were authorised, conducted on an ‘execution only’ basis, and deposited into the complainant’s own account. AFCA determined that Mark and ACME Advice were not responsible for Martin’s loss.

Mark’s actions saw him make best endeavours to determine whether there was an issue and comply with his ethical obligations. Importantly, he upheld the following standards.

Case study two: Coercion into a granny flat

Audrey had been widowed for 15 years. She and her husband had invested well over time and her financial adviser, Lisa from ACME Financial Advice, had looked after her financial interests for more than a decade.

At their semi-annual review meeting a year prior, Audrey told Lisa she planned to sell her home and contribute the proceeds toward her daughter’s intended purchase of a new home. She was to have her own granny flat on the property and would live there permanently. That way she would be closer to her daughter and if she needed assistance or care, it would be readily available.

Lisa was surprised. Audrey’s daughter lived in the country; at least two hours from Audrey’s current home and in an area not well serviced by transport. Lisa knew Audrey had remained active in her community. She loved her regular bridge session, was on a bowls team and volunteered at a local charity shop.

Despite Lisa expressing her misgivings, Audrey proceeded with her plans. As well as contributing the proceeds of her property sale to her daughter’s new home, Lisa later redeemed some investments to pay for the fit out of her granny flat.

Less than one year after Audrey moved to her new residence, Lisa received a tearful call. Audrey and her daughter had fallen out; she had missed her community and had not found her place or her people in the new location. She wanted to return to her community but, when she requested the money to do so, was told she had no right. Despite the money from the sale of her property and investments, she was not listed on the title deed, nor was her financial contribution recorded elsewhere.

Although she had some investments, it was not enough for her to set up home, leaving Audrey in a vulnerable position. It’s not an uncommon scenario – as identified by the Australian Human Rights Commission in its current Financial Elder Abuse Project, granny flat arrangements are an increasingly common form of financial abuse.

Although Lisa recognised the situation as unusual and unexpected, she failed her elderly client. She did not recognise coercion, and she failed to recommend that Audrey seek legal advice before selling her home and investments. Legal advice would likely have led to contractual arrangements that provided Audrey with some protections. Ultimately, Lisa’s inaction resulted in her client being in a financially vulnerable position. Lisa potentially breached the following standards in the Code of Ethics:

Case study three: Misuse of an EPOA

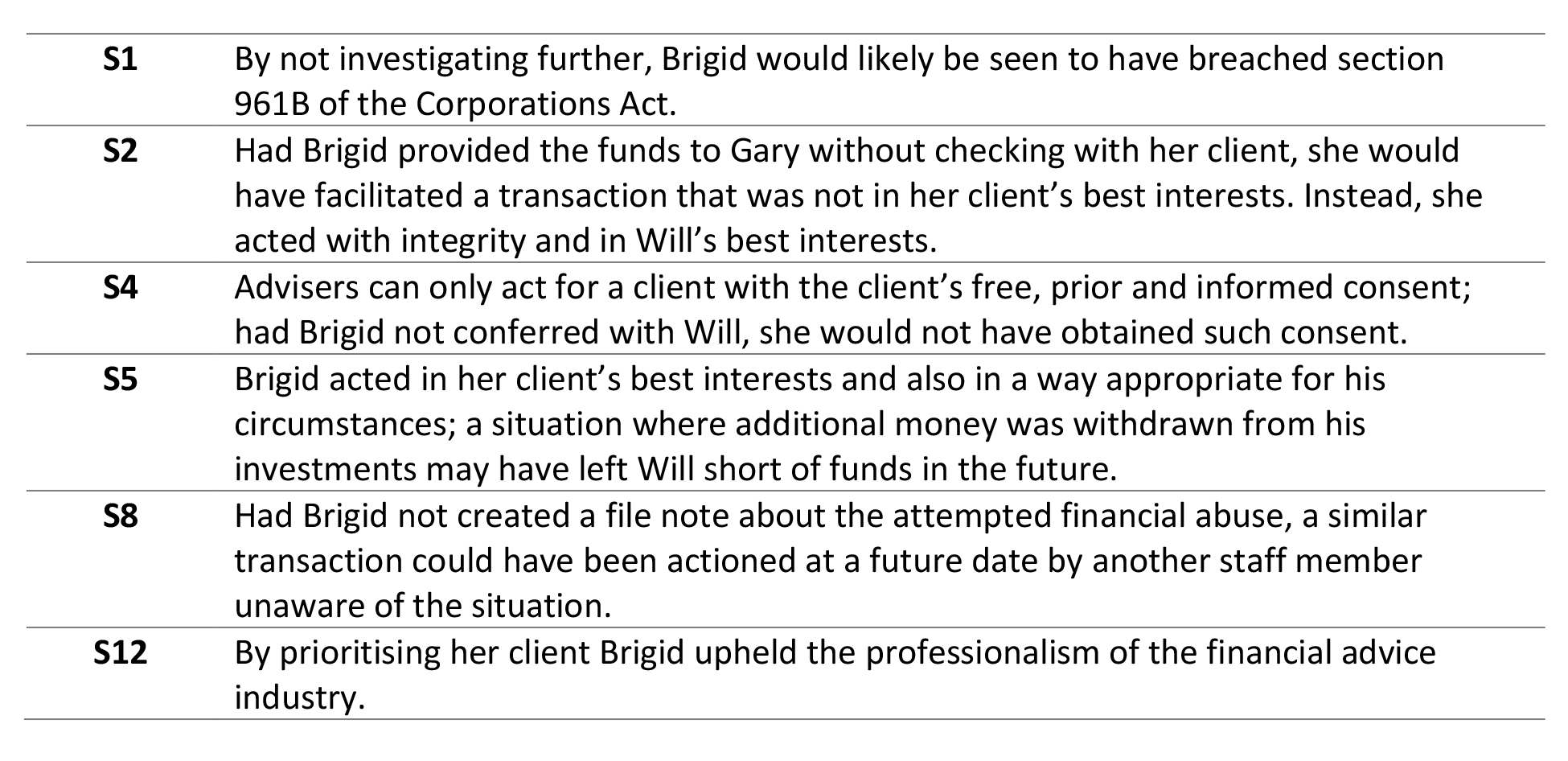

Will is in his early 80s and had been a client of ACME Advisors for over a decade. A few years ago, Will’s two sons established a joint EPOA should their father require assistance and stewardship in his later years. Will’s financial adviser Brigid knows of the EPOA and has met with both sons on several occasions.

Despite a recent stroke, Will’s mental acuity had remained strong. However, he’s no longer able to drive and found it challenging to live at home on his own. As a result, Will moved in with his son Gary and daughter in law Cynthia. Although he’s able to be reasonably independent in their home, Cynthia sees herself as Will’s default carer.

Gary contacted Brigid and asked her to redeem a managed fund investment valued at $88,000. He explained that it would be used to make some modifications to his and Cynthia’s home to make it safer and more comfortable for Will to live there. He talked about a ramp in the event Will needed to use a wheelchair, railings in the ensuite bathroom used by Will and some garden landscaping to make it easier for Will to safely enjoy their outdoor space.

Brigid called Will at a time she knew Gary would be at work. She wanted to ensure that Will was aware of this request, its purpose and quantum. Will was aware of the building works and had seen the quotes. He was aware that the modifications had been quoted at $46,000. Gary had intended to keep the remaining $42,000 as ‘payment’ for Will living in his house and his wife’s services as a ‘carer’. He had not intended to inform his father about this, let alone seek his approval. Brigid did not action the transaction and made a file note of this issue in case the situation arose again at a time she wasn’t present at the firm.

Although AFCA acknowledges that employees of financial firms are “not expected to be detectives”, it does state that it is an adviser’s duty to exercise reasonable care and skill. This includes an obligation to question a client’s authorisation of a transaction, especially in circumstances where financial abuse is possible, or the use of funds is not consistent with the customer’s wishes or is not for their benefit.

Through her actions, Brigid acted in Will’s best interests and did not breach the Code of Ethics. However, had she simply actioned Gary’s request, she would have potentially breached the following standards:

Read Part 1:

CPD: Ethical financial advice for vulnerable clients – part one

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Professionalism and Ethics (0.5 hrs)

ASIC Knowledge Requirements: Ethics (0.5 hrs)

please log in to start this quiz

———

Notes:

[1] NSW Government Ministerial Release, World Elder Abuse Awareness Day, 15 June 2025

[2] https://humanrights.gov.au/resource-hub/by-resource-type/reports/older-peoples-rights/financial-elder-abuse-project

[3] The AFCA approach to financial abuse of older people, November 2025

[4] Australian Human Rights Commission (AHRC), Financial Elder Abuse Project (Launched Nov 2024; Progress Report October 2025)

[5] AIHW (2025), “Technology-facilitated abuse” subsection, citing Powell et al. and the ANROWS Technology-Facilitated Abuse National Survey

[6] Professor Ann Kayis-Kumar and Professor Jan Breckenridge (UNSW), Exploitation of Financial Systems in Domestic and Elder Abuse, 2026

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Professionalism and Ethics (0.5 hrs)

ASIC Knowledge Requirements: Ethics (0.5 hrs)

please log in to start this quiz

———