Paul Meierdierck

The impact of the Iran conflict and higher oil prices on economic growth, inflation and the path of interest rates are ultimately uncertain and pressuring near-term sentiment for markets. But despite these near-term headwinds, LaSalle Investment Management portfolio manager, Paul Meierdierck said the long-term outlook for REIT investors remains compelling.

“While we acknowledge market dynamics can change quickly and geopolitical events are fluid, we typically view geopolitical events such as these as part of the “wall of worry” markets typically climb over time, with pullbacks presenting potential longer-term investment opportunities.

“The global listed real estate market entered 2026 in a more supportive phase due to improving macroeconomic conditions, moderating supply and attractive valuations, creating a compelling long-term outlook for REIT investors,” said Meierdierck.

Listed real estate is currently trading at attractive levels relative to both broader equities and private property markets.

“REITs are trading at more than a 20 per cent discount to broader equity market and valuations look quite compelling today,” Meierdierck said.

“Real estate has materially repriced and public REITs are now offering what appears to be a margin of safety relative to broader equities, while also trading at discounts to private real estate.”

Meierdierck said the sector is beginning to benefit from a broader rotation in equity markets, with value assets such as REITs, gaining renewed attention after several years where growth stocks dominated performance.

“For much of the past decade, growth significantly outperformed value and REITs were caught up in that trend,” he said. “What we are seeing now is the early stages of a rotation where value sectors are starting to regain investor interest, and that’s beginning to show up in the listed property market.”

Meierdierck said macroeconomic conditions are also becoming more supportive for real estate investors.

“Until the Iran conflict, interest rates had largely stabilised after a period of significant increases, and continue to remain within recent ranges, while credit spreads remain tight, and inflation expectations are well anchored. Together, those factors create a much more constructive environment for real estate than we have seen over the past few years,” he added.

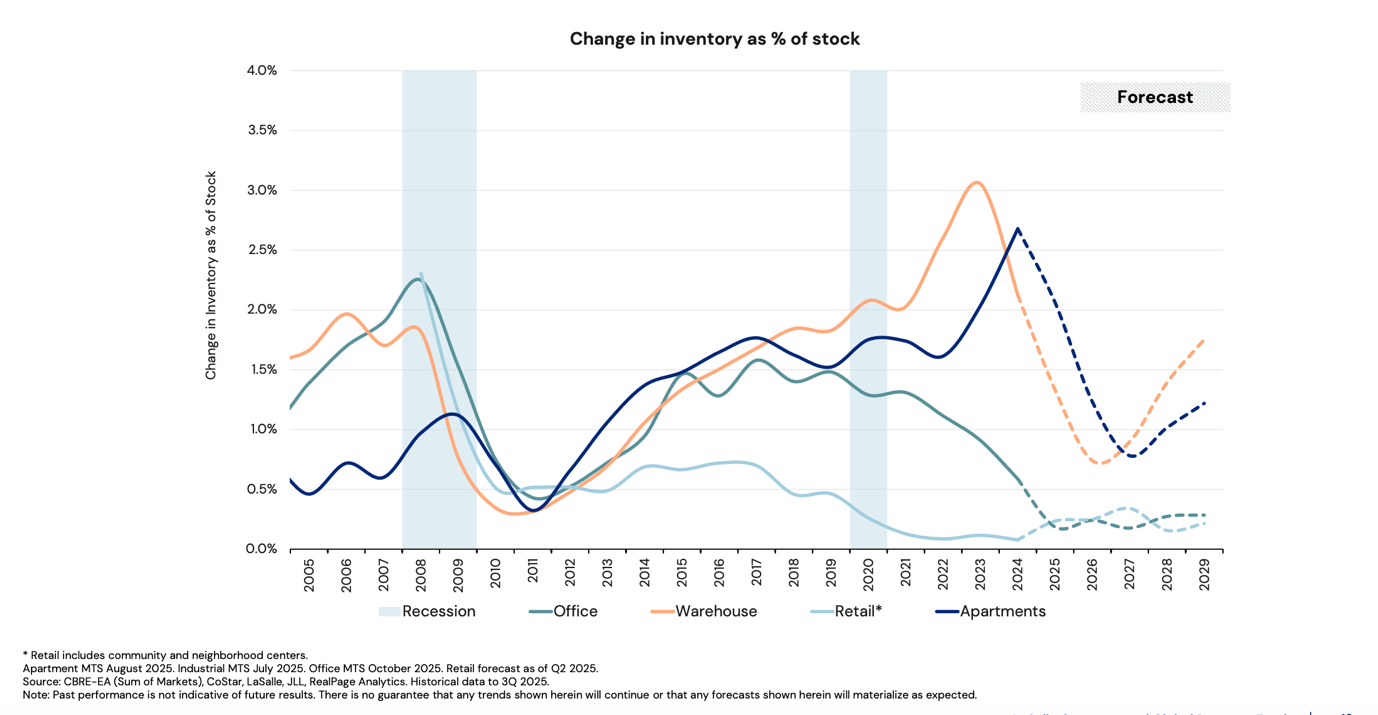

Declining supply supports fundamentals

At the same time, underlying property fundamentals remain strong, supported by declining new supply.

“Real estate supply continues to moderate while demand is stabilising. We’re reaching the point where new construction deliveries are slowing materially, which should support rent growth and occupancy across a number of sectors.”

He flagged warehouse and residential property markets as examples of this dynamic.

“Industrial supply increased rapidly during the low-interest rate period after the COVID-19 pandemic, but that excess supply is now being absorbed and deliveries are expected to bottom out this year.

“Markets tend to be forward looking, and we’re already seeing industrial property begin to outperform in anticipation of that tightening supply environment.”

Opportunities emerging in discounted sectors

While data centres and healthcare remain long-term growth sectors, Meierdierck said that the most compelling opportunities today are often emerging in areas where valuations have been heavily discounted.

“Healthcare has delivered very strong growth, but valuations already reflect much of that optimism. In contrast, sectors like offices, apartments, and self-storage are beginning to show improving fundamentals while still trading at significant discounts.”

He added that office markets in key global cities are stabilising as companies complete the process of adjusting to hybrid work models.

“Corporates have largely completed the process of rightsizing their office footprints. In prime locations like Manhattan and London’s West End, we’re seeing a more broad-based recovery in demand, which is creating selective investment opportunities.”

Meierdierck also highlighted digital infrastructure as a long-term opportunity, particularly data centre platforms that control key network connectivity locations.

“As digital connectivity and AI adoption continue to accelerate, companies that own highly connected data centre locations are in a very strong position. These sites form the backbone of digital infrastructure and provide a highly defensible competitive advantage.”

Recovery still in early stages

Overall, Meierdierck said the combination of improving fundamentals and discounted valuations provides a favourable outlook for the asset class.

“Listed real estate has already experienced a significant repricing, but the recovery is still in its early stages.

“With REITs still trading at a substantial discount to broader equities, we believe there is meaningful room for further upside as the cycle continues to normalise,” said Meierdierck.