Jeffrey Schulze

As investors digest implications of a higher US consumer price index reading and a historic summit between US President Donald Trump and Chinese President Xi Jinping, ClearBridge Investments says investors needn’t shy away from new highs, particularly when earnings expectations are holding up.

“We are staying disciplined, using volatility as an opportunity to deploy capital, while modestly favouring the stronger earnings revisions and more reasonable valuations available in non-U.S. equities,” Jeff Schulze, head of economic and market strategy at ClearBridge Investments, says.

“The rebound in US equities from late-March lows has been swift and broad-based, with equities rising 13.6 per cent since their trough. April alone accounted for 10.4 per cent of the gain, making it the best monthly performance since 2020 and the 12th best monthly return in more than 75 years.

“A key reason we continue to believe US markets can climb higher is the green overall signal emanating from the ClearBridge US Recession Dashboard,” Schulze says.

The dashboard, which tracks a range of economic indicators, has now returned a fully green reading after Housing Permits, previously delayed by government shutdown data disruptions, stabilised and flipped from yellow to green.

The bullish signal comes against a complex macro backdrop. Wednesday’s CPI print showed US inflation running at 3.2 per cent annually, above consensus forecasts, reinforcing expectations that the Federal Reserve will keep rates on hold through mid-year. Separately, the first face-to-face meeting between President Trump and President Xi since 2023 has raised hopes of a de-escalation in trade tensions, though markets remain cautious.

Schulze says, “The US labor market has alternated between positive and negative prints for the past 11 months, with net job creation modestly positive on balance. More broadly, the labor market has cooled over the past few years primarily due to drags from changes in immigration policy and the aging population demographics. It still does not appear that artificial intelligence (AI) is driving widespread layoffs, although there are pockets of softer hiring.

“We are encouraged by initial jobless claims – our economic canary in the coalmine – notching its lowest total since 1969 last week alongside other recent signs of labor market stabilization. Looking ahead, we remain on watch for AI-driven job losses, but we are also eyeing AI job creation as previously unimaginable jobs emerge on the back of this technological advancement.”

The geopolitical risk has not disappeared.

“The equity rally does appear to be vulnerable to a re-escalation of the conflict in the Middle East, particularly if disruption to trade in the Strait of Hormuz lasts longer than is currently expected (reopening around mid-year). Given that the bulk of the April rally occurred in conjunction with the de-escalation of tensions in the Middle East, we believe the risk of a prolonged supply bottleneck is real.

“We continue to believe that the economic impacts should remain manageable and not result in a meaningful economic slowdown: further pullbacks would likely represent buying opportunities, in our view. At the same time, we do not believe investors should be scared off by the markets being back at all-time highs.

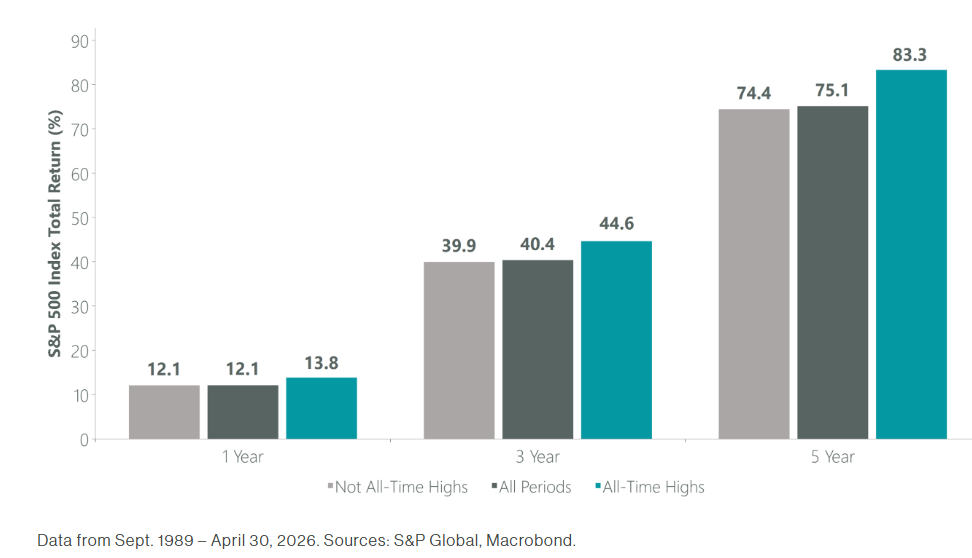

“Our work (counterintuitively) shows that investing at new highs has historically outperformed deploying capital when the benchmark is below peak.

The S&P 500 is trading back above 20 times on a forward price-to-earnings basis, a level some investors treat as a ceiling.

“But the benchmark has traded above that multiple 63 per cent of the time since first crossing the threshold in April 2020, without acting as a headwind to returns. Over the past six years the index has risen 147.5 per cent, roughly double the long-run average, underpinned by cumulative next-12-month earnings growth of 137 per cent.”

“First-quarter results, now past the two-thirds mark by market capitalisation, have delivered strong upside surprises, with information technology, energy and materials sectors showing notable strength. Consensus expectations for mid-teens earnings growth have continued to rise rather than follow the typical seasonal pattern of downward revision.”

“We continue to believe non-U.S. equities present an attractive opportunity relative to domestic US stocks. Emerging markets (EM) look particularly compelling despite their recent strength, with robust revisions to earnings expectations powering their returns and supporting a continued constructive fundamental outlook.

“Valuations also remain less challenging than in the U.S., and although some EM economies are significant oil importers, the adage that the stock market is not the economy rings even more true in the case of many EM countries.

“Developed non-U.S. equities should also benefit from positive earnings revisions and attractive valuations, although to a lesser degree.”