The primary challenge for investors is less about the direction of growth and more about its durability.

Positive growth but with rising fragility

Key takeaways

- Global growth remains positive, but increasingly fragile. A narrow set of drivers is supporting activity, increasing sensitivity to shocks and widening the range of potential outcomes.

- US growth is supported by AI investment, but durability is uncertain. Productivity gains have yet to translate meaningfully beyond corporate margins.

- Tariffs, energy and geopolitics add a layer of uncertainty. Outside of the US, cost pressures are more likely to lift inflation and weigh on growth, complicating policy trade-offs.

- Wider dispersion places a premium on portfolio resilience over forecasts. Elevated uncertainty argues against concentrated macro positions and in favour of flexibility as conditions evolve.

Summary: Bigger tails and a shrinking middle

At this spring’s Portfolio Strategy Group (PSG) forum, Capital Group’s fixed income investment experts examined the global macroeconomic landscape with a focus on mounting uncertainties and growing divergence. US economic growth over the past six months has been more resilient than anticipated at our last PSG. As we look ahead, data points to growth remaining positive but becoming increasingly fragile, with the conflict in Iran adding extra uncertainty.

US economic expansion is positive overall, but its composition is increasingly fragile, with AI investment representing a significant proportion of GDP. In the long term, AI has the potential to provide a huge productivity boost to the US economy, but the current influence of AI capex on GDP raises the risk that adverse shocks may quickly lead to weaker demand, heightened volatility, and greater dispersion, rather than a smooth cyclical adjustment.

Beyond the US, momentum has improved in parts of the global economy, especially the euro area, where growth is aided by fiscal stimulus and cyclical recovery. Nevertheless, this improvement remains at risk and is more vulnerable to policy constraints and external shocks such as higher energy prices and tariffs.

Trade policy changes and the Iran conflict are the two most recent examples of exogenous shocks that add uncertainty to the broader economic environment. Both have skewed risks toward more stagflationary outcomes. In this context, the primary challenge for investors is less about the direction of growth and more about its durability: what is the long-term impact from AI infrastructure? Composition: is growth being driven by AI investment or consumption? Distribution: what does the K-shaped economy mean for growth?

Portfolio positioning

Given the distribution of outcomes is wide with higher probability of tail events (AI productivity boost and stagflationary risk), we think it is prudent to avoid positioning portfolios for one macroeconomic outcome.

Guidance is therefore structured as a cautious balance between carry, diversification and downside risk management, with portfolios retaining the ability to add risk should valuations become more attractive due to volatility. More details will be provided at the end of this note but in summary, PSG guidance currently favours:

- Overweight duration in portfolios mainly through the US, while being underweight euro and UK.

- Maintain a steepening position.

- Remain very selective in credit markets, with a focus on securitised credit and opportunities in investment grade and high yield corporates.

1. AI driven growth is powerful but narrow

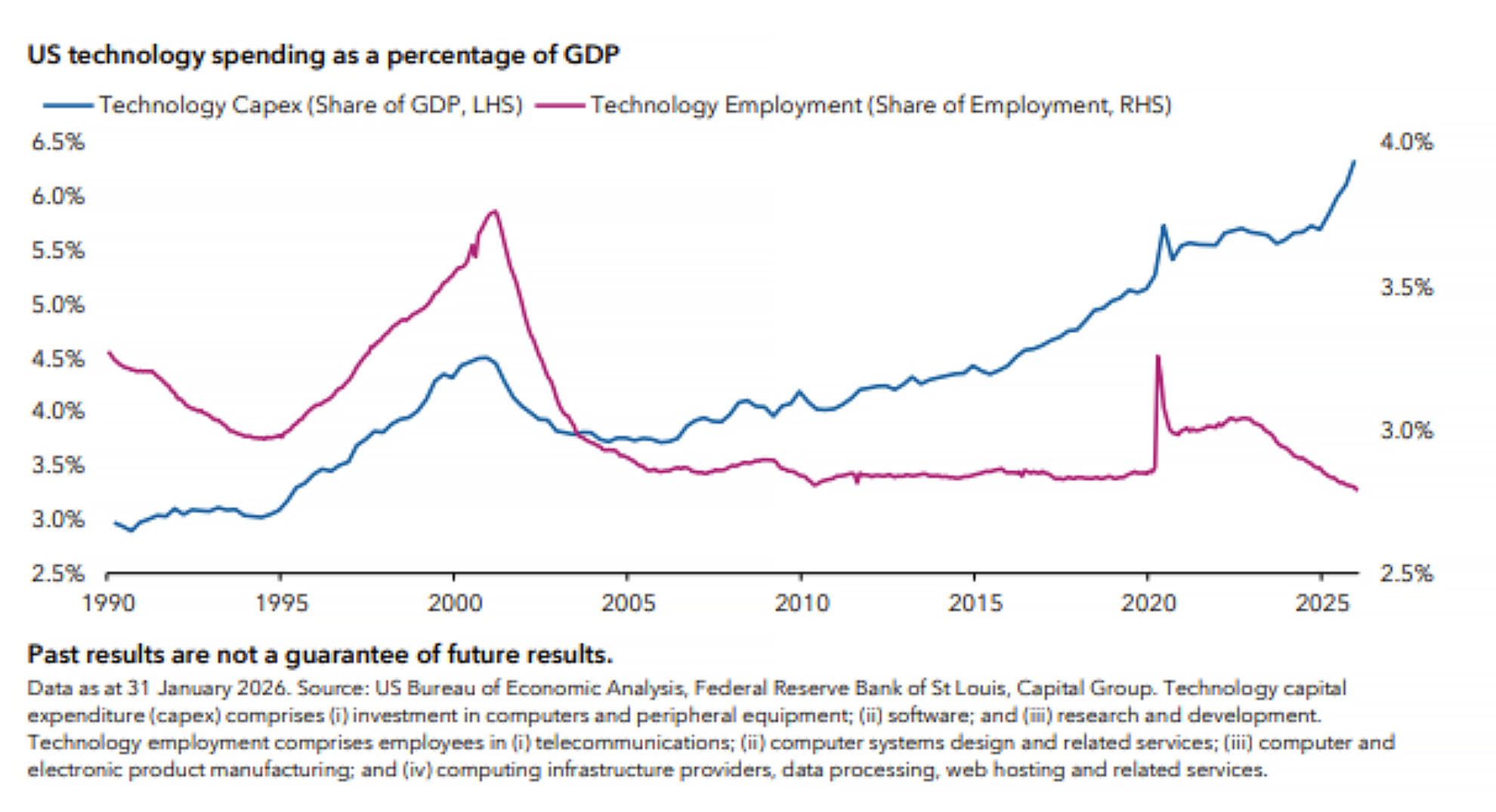

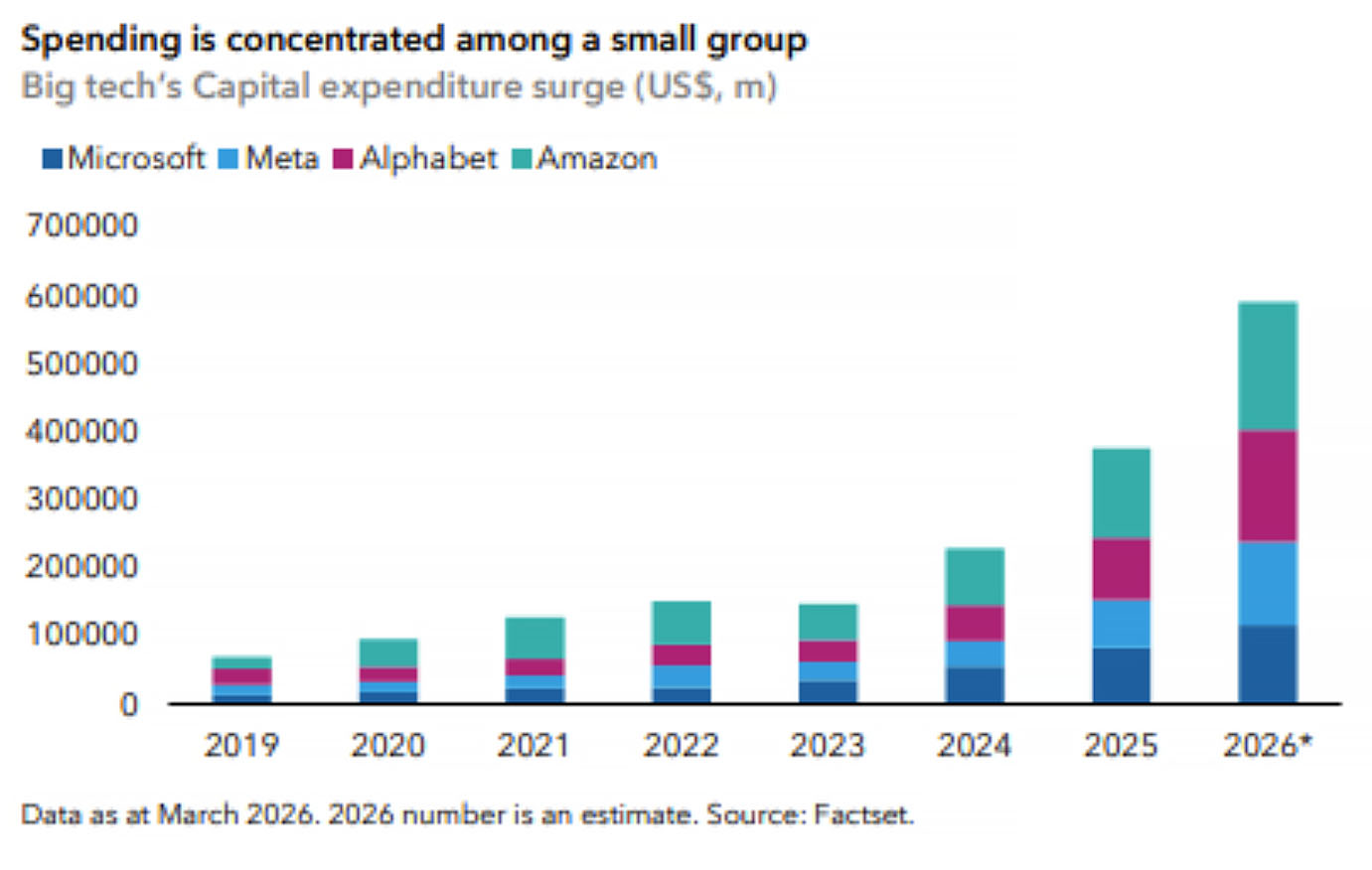

US growth remains positive, supported by large AI-related investments that continue to drive capital spending and productivity. The first chart on the following page puts current AI-related spending into some historical perspective. As a percentage of GDP, technology spending in the US is now well above the peak in the 1990s tech bubble, and as the second highlights, the majority of this is concentrated in a very small group of companies.

Although it is huge, companies view this spending as strategically essential from a corporate perspective because AI underwrites their platform relevance, control and future value chains, and the capacity to compete in the AI era. Put simply, the cost of not investing is deemed far greater than the near-term risk to return on investment.

This level of spending is significant because at this level, it represents around 1% of US GDP. From a cyclical perspective, this matters because it provides a meaningful offset to weaker momentum elsewhere in the economy. Growth can therefore remain resilient even if non‑AI sectors expand only modestly.

However, the composition of this spending limits its broader economic impact. Much of the investment is directed toward data centres and associated infrastructure, with a high import content and limited ongoing labour requirements once facilities are operational. As a result, the multiplier into employment and household income is relatively small.

While this spending currently supports US growth, it has also heightened the economy’s reliance on ongoing AI investment. And, importantly, with spending focused on a small number of companies, aggregate capex is clearly sensitive to changes in capital discipline at firm level. At the moment, this spending remains strategically important for the hyperscalers, with its durability shaped primarily by access to power, planning and grid connection constraints, and hardware availability. Any change that suggests companies ought to scale back spending would have a negative impact on overall economic growth.

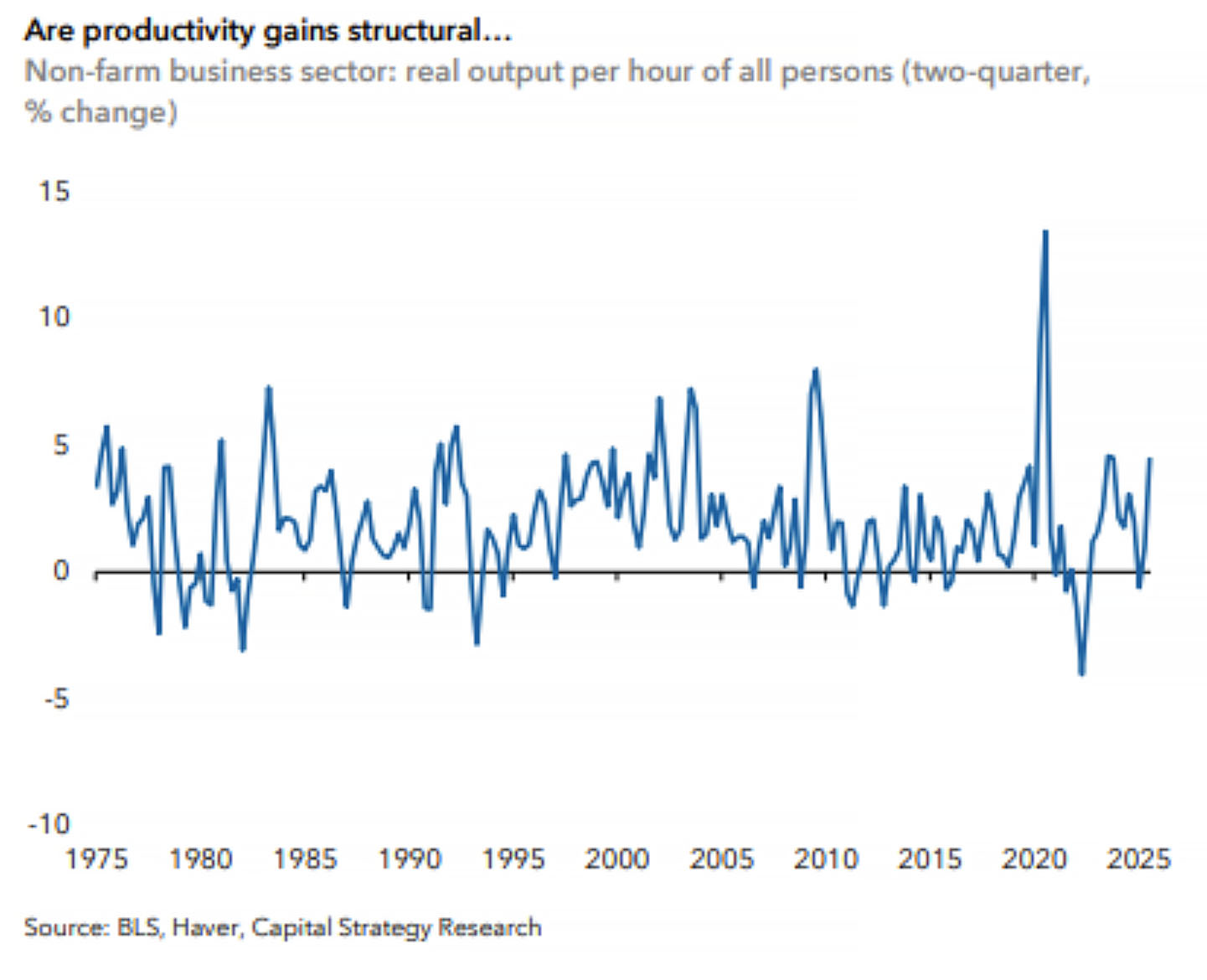

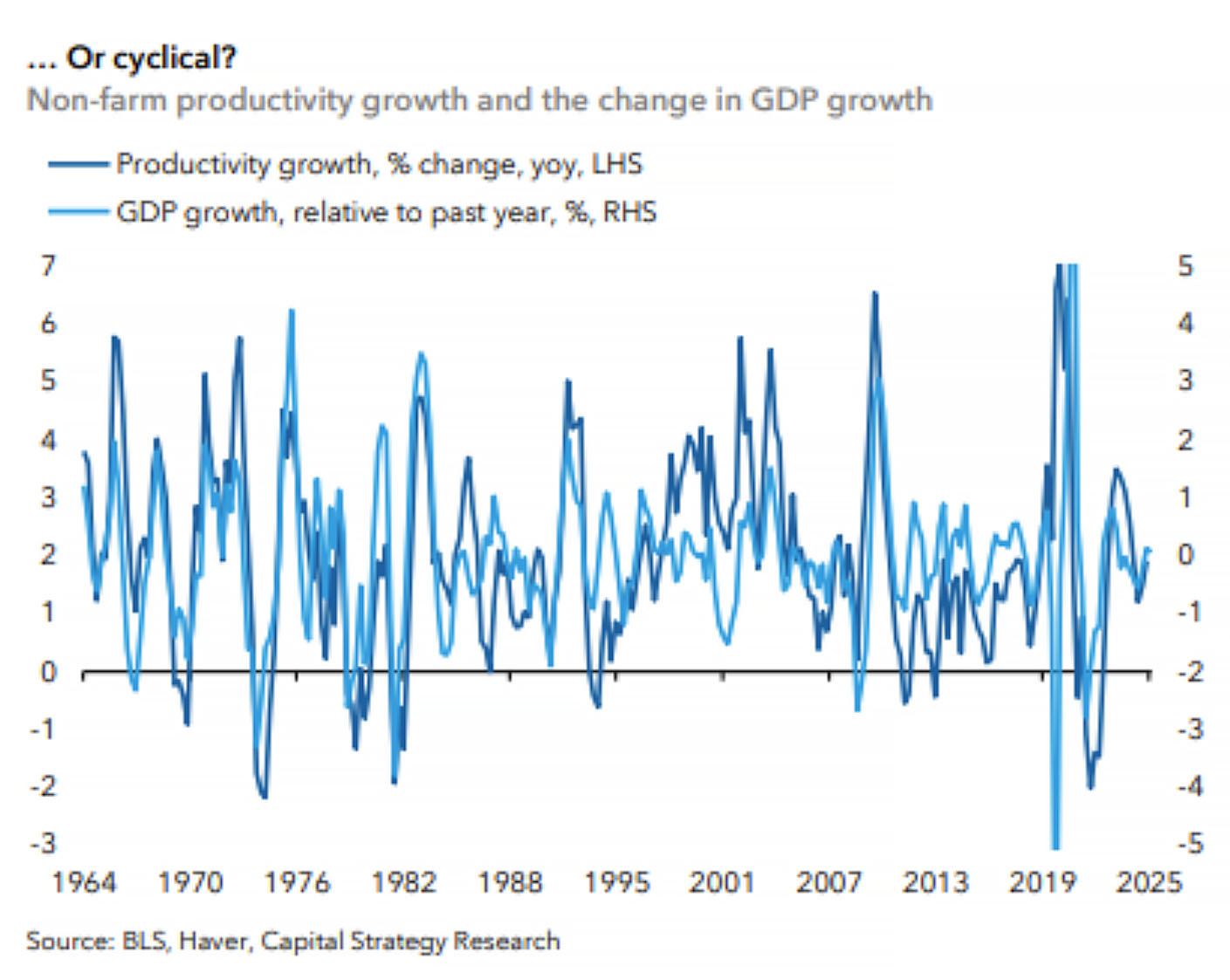

Are we already seeing AI productivity gains or just a cyclical bounce?

The broader significance of this capex cycle is its link to productivity, which surged in the US to an annualised pace of around 5% in the middle of last year. This unusual, though not unprecedented, pace of growth raises the question of whether the upturn was cyclical, reflecting an improving economy, or structural, marking the early stages of AI driven productivity gains.

The cyclical argument is that as growth accelerated, firms increased the utilisation of existing labour and capital rather than hiring, allowing productivity to act as a shock absorber. An alternative view is structural: that the upturn reflects the early impact of AI adoption, with efficiency gains initially concentrated and broader diffusion still to come.

This distinction is important for the overall outlook. If the 2025 surge was largely cyclical, productivity is likely to normalise as growth moderates; if structural, and therefore sustainable, it raises the prospect of higher potential growth. The key question then becomes how these productivity gains are transmitted through the economy. Do they accrue to workers or to firms? The macro implications differ materially, with growth likely more durable if productivity gains are passed to workers rather than retained primarily in corporate margins. At this stage, the data is not conclusive.

2. Labour market is softening in a ‘K shaped’ economy

The current surge in AI capex spending is helping to mask weakness across other parts of the economy. From a cyclical perspective, the labour market is emerging as a key fault line, sharpened by the debate about the durability of recent productivity gains. Although the overall unemployment rate remains low, there are signs of underlying softness.

First, US job growth has become increasingly concentrated in few areas such as the healthcare/education, leisure and government sectors. For example, January payroll growth was almost entirely driven by healthcare and social assistance, which together accounted for the vast majority of the 130,000 jobs created. Even after a strike-related pullback in February, healthcare remains the dominant contributor to employment growth in 2026. Outside of these sectors, job growth has been weak, underscoring the narrow and potentially fragile nature of US labour market resilience, although we acknowledge this trend has persisted since 2023 and growth has been fine.

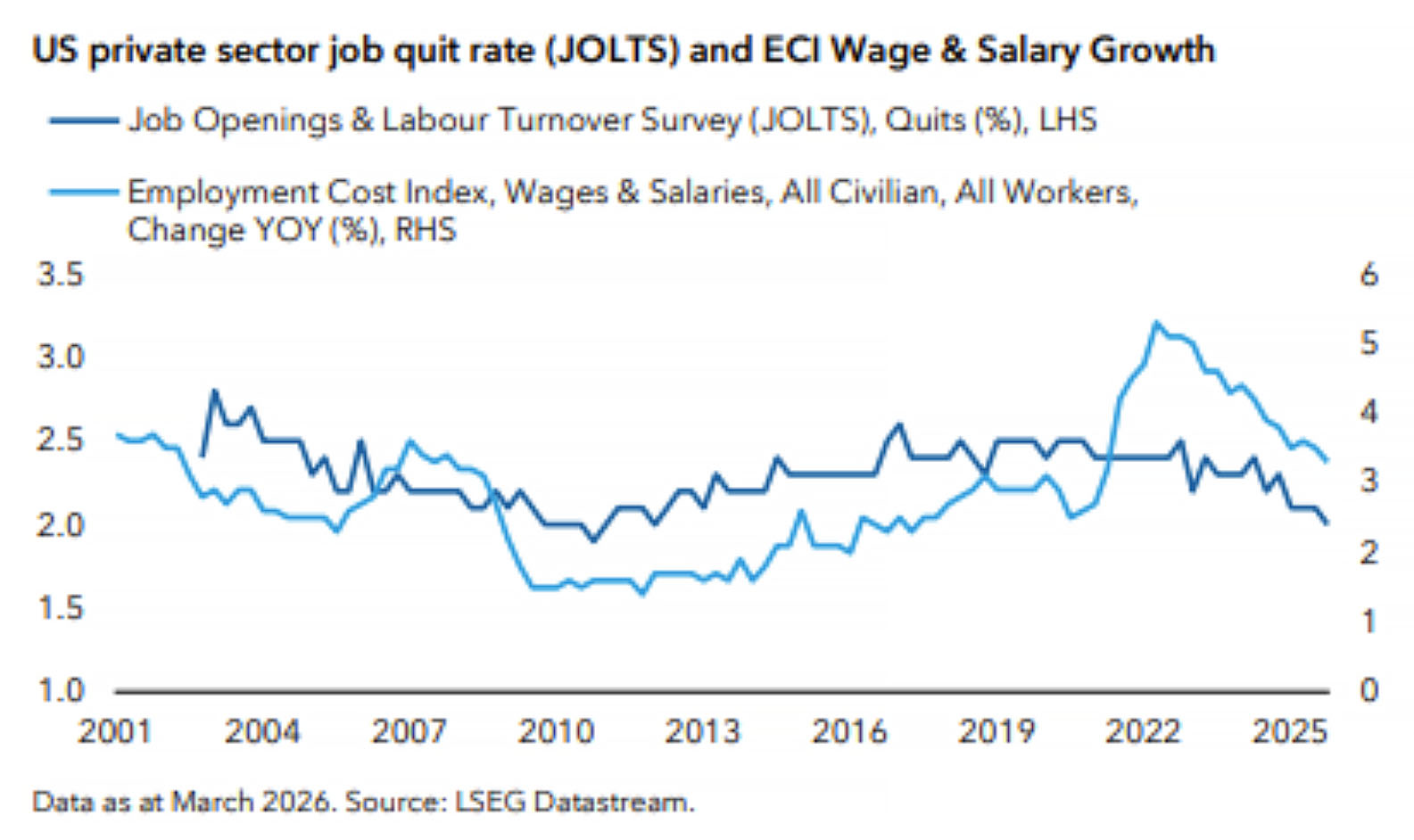

Second, in addition to this concentration risk, there are some broader signs of a softening in the US labour market. One place we can observe this is the JOLTS quit rate and wage data, which both continue to fall. This may reflect increasing worker caution as bargaining power weakens, potentially because recent productivity gains have accrued more to firms than to labour.

A degree of caution is also evident at corporate level, with companies retaining muscle memory of the difficulties in rehiring in the post-COVID era, preferring to implement hiring freezes rather than reducing headcount and creating a so called low-hire low-fire labour market. This data is more representative of lower income, less secure workers, who are more reliant on job switching and nominal wage growth, than higher-income cohorts.

Labour weakness in this cohort at the same time that overall unemployment remains low points toward the current ‘K shaped’ dynamic of the US economy. That is, the idea that low/middle income workers face more pressure on household budgets compared to their richer counterparts. This stress is also showing up in rising delinquencies among lower-income households.

The divergence matters because consumption accounts for roughly two-thirds of US GDP, according to the Bureau of Economic Analysis. At the same time, income is highly concentrated, with households in the top 20% receiving just over half of total US personal income. As a result, economic growth can remain resilient even as labour market stress intensifies for lower-income households, whose aggregate consumption is smaller.

The K-shaped economy dynamic is reinforced at firm level. Smaller companies that typically have less pricing power and greater exposure to tariffs face more pressure on margins than large counterparts. This, in turn, feeds through to wages and job security for workers in such enterprises.

For the economy as a whole, this means spending growth for these lower income households is lagging, with aggregate spending largely supported by high-income groups, which benefit from asset prices and stable employment. However, as the breadth of consumption narrows, US growth potentially becomes more fragile and exposed to the risk of a further weakening of the labour market.

This brings the sustainability of the recent productivity growth question into focus. In the near term, AI‑related investment continues to provide important cyclical support to growth, acting as stabiliser for the cycle and helping offset labour market softening and sustain aggregate activity even as hiring and wage momentum cool.

If the productivity upturn seen in 2025 was largely cyclical, then it could normalise as the labour market continues to soften, leaving the economy more exposed to further weakness in hiring and household income growth. However, the most important question is the transmission channel of productivity gains into the broad economy in the long term.

3. Productivity and fiscal policy are the main factors to shape medium-term outcomes…

The durability of the current growth mix ultimately depends on productivity, particularly in the US. If productivity gains prove more persistent, the key issue becomes transmission: whether those gains begin to show up more clearly through wages and lower inflation that supports real incomes over time or remain in corporate margins. If gains increasingly accrue to workers, we can anticipate this would contribute to higher levels of growth and a disinflationary environment alongside lower unit labour costs. But the jury is still out as there are many factors that contribute to this trend, including a potentially weaker USD in the long term, which can put more pressure on inflation.

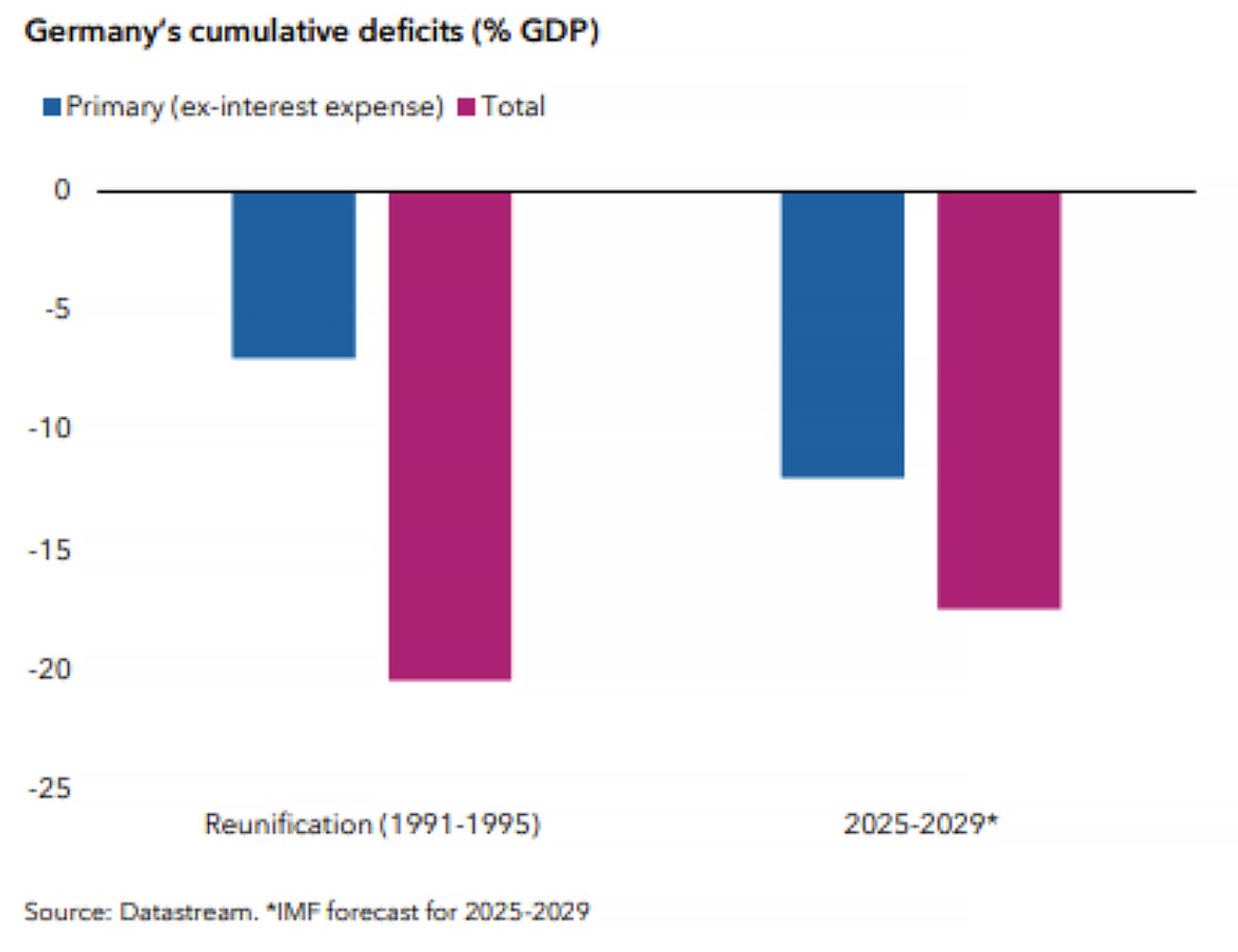

Elsewhere, medium-term economic outcomes increasingly hinge on whether policy can offset fragile growth dynamics, with fiscal developments playing a prominent role. Fiscal policy is providing support most clearly in Europe, where it is driven by the unusually large German fiscal impulse, which supports growth both cyclically and secularly despite recent shock-driven uncertainty. German government plans imply wider deficits by around 2-3% of GDP over the course of the parliamentary term relative to previous plans. It is worth reiterating just how significant this amount of stimulus is. On an IMF measure excluding interest payments, the planned spending amounts to a cumulative fiscal impulse of roughly 10% of German GDP over four years, larger than during reunification in the 1990s. There is some uncertainty around the timing and near-term transmission of this support, however, particularly given energy related headwinds.

That said, elements of the stimulus are beginning to appear in the data. The German economy exceeded expectations with annualised growth of 1.2% in the fourth quarter, while domestic manufacturing new orders have strengthened and survey indicators such as PMI (Purchasing Managers’ Index) have improved. However, companies are not yet reporting clear evidence of the stimulus feeding through to order books. Expectations are more cautious, with much of the impact anticipated later in the cycle.

Elsewhere, China could provide further incremental fiscal support. Credit data, which has historically been a strong leading indicator, continues to point to subdued growth and little sign of re‑acceleration. Our economists judge that, if this persists, it could prompt additional fiscal stimulus later in the year.

4. … But energy shocks and tariffs add a layer of uncertainty

Energy shocks and trade policies are amplifying regional dispersion in growth, inflation, and monetary policy, making the global macro environment more uncertain. The Iran conflict is the latest example of this. Even if the conflict proves relatively short lived, its impact on energy markets could linger through higher risk premia and capacity destruction during the conflict. That persistence matters for regions with higher energy sensitivity, where inflation pressures are more easily transmitted into domestic prices and real incomes.

Outside the US, rising energy prices challenge Europe’s growth recovery. Alongside the UK, parts of Asia and several emerging markets, the eurozone’s high energy dependence raises the risk that heightened energy prices lead to a less favourable trade off between growth and inflation.

Tariffs add a further layer of divergence and uncertainty to the macro picture. In Europe and Asia, their inflationary impact is less easily absorbed by margins than in the US and therefore more likely to feed through to consumer prices. At the same time, trade frictions weigh on external demand and corporate confidence, reinforcing any cyclical slowdown. The result is a macro environment in which inflation risks remain skewed to the upside even as activity softens due to continued supply shocks.

Whether higher headline inflation as a result of these factors leads to rate hikes depends on the persistence of the inflation shock, the extent of the damage to growth and if there is any fiscal support. Although the situation remains in flux, expectations for central banks around the world have shifted towards a higher probability of rate hikes, with the European Central Bank (ECB) and Bank of England (BoE) the most hawkish. However, it is important to remember this is very different environment from 2022 where the demand side was stronger and starting yields very low. Central banks will need to balance the risk of higher inflation against the impact on growth of aggressive tightening.

By contrast, the US Federal Reserve may still retain greater flexibility than its peers. The US economy is less sensitive to energy price shocks, and the Fed’s dual mandate allows it to place greater weight on labour market outcomes if downside risks emerge. As long as core inflation remains contained, a cooling labour market would give the Fed more scope to ease policy than central banks in regions where inflation pass-through is stronger.

Investment implications

Overall, the PSG view is that global economic growth remains positive and this continues to support selective exposure to credit, while acknowledging valuations remain relatively tight. However, the narrow and increasingly fragile nature of this growth argues against aggressive directional positioning. Therefore, rather than positioning for a single macro outcome, portfolio construction should emphasise balance across risk drivers, focus on bottom-up security selection, and preserve flexibility as uncertainty remains elevated.

In rates, the focus is on downside protection rather than expressing a high conviction growth view.

- US rates: US rates have moved higher without a meaningful change in outlook. The PSG believes that given its dual mandate, if core inflation stays stable, the Fed will likely focus on labour market weakness and favour lower rates, despite higher energy prices also given the lower energy sensitivity in the US.

- Global Rates ex-US: Improving growth trajectories, stickier inflation and increased deficit spending support an underweight position to Europe and UK rates.

- Curve: Curve steepeners through an overweight in the 2-5yrs part of the curve in the US and an underweight of the 10yr rates continue to offer the potential to provide protection against asymmetric outcomes where growth weakens but inflation risks remain present. In Europe, we position for a steepening of the curve as well although we have a more neutral view on the front end given the potential hawkish stance of the ECB and BoE.

In credit, elevated yields continue to support expected returns, but tight valuations and rising dispersion place a premium on issuer-level analysis.

- High yield: Long-term improvements in credit quality and shorter duration of the market continue to support a structural role for high yield, though positioning should be measured and focused on resilience.

- Investment grade (IG): Softening fundamentals, albeit from a healthy starting point, and higher issuance suggest a more cautious approach alongside still tight valuations. However, overall yields remain elevated for such a high-quality asset class, prompting us to keep a strategic allocation to IG corporates. Security selection rather than broad beta exposure is crucial also given the recent increase in dispersion

- Agency Mortgage-Backed Securities: While technicals remain supportive of agency MBS, valuations are tight relative to historical levels and interest rates volatility elevated arguing for caution toward the asset class at current valuations.

- Structured credit: Provides a high-quality, shorter-duration source of carry and remains attractive relative to other spread sectors. This is an area where we see more value although we continue to focus on senior part of the capital structure as capital structures remain still relatively compressed.

Emerging markets (EM): The Iran conflict is expected to increase dispersion across EM rather than threaten the asset class overall, with many emerging economies benefitting from stronger macroeconomic foundations than in previous geopolitical crisis. Opportunities are focused on local currency markets where yields are elevated, inflation is tempered and curves are steep.

Nonetheless, FX resilience remains uneven across EM, underscoring the importance of security selectivity. On the other hand, the hard currency part of EMD remains uninspiring as spreads do not fully reflect broad uncertainty, although idiosyncratic opportunities remain.

FX: Potential USD weakness and monetary policy divergence suggests an underweight to the dollar versus developed market and select emerging markets currencies. However, the level of convictions has been reduced as the continuation of the Iran conflict could be supportive of the USD in the short term.

———–

Iran conflict

At the time of writing, the duration and ultimate resolution of the conflict in Iran remains unclear. While both sides appear prepared militarily for an extended conflict, there is sharp divergence between their political tolerance for an extended war. Although the US has superior military capability, we think it has limited tolerance for a protracted war. The Iranian regime, by contrast, sees the conflict as existential, and so likely has a higher tolerance to maintain the war over the longer term. This divergence makes a swift ending to the war more challenging, with a risk that this becomes a battle of endurance. A long conflict is expected to increase dispersion across regions, sectors, and countries. Outcomes would increasingly depend on underlying fundamentals, policy credibility, external balances and fiscal resilience

———–

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.25 hrs) and General (0.25 hrs)

ASIC Knowledge Requirements: Economic Environment (0.25 hrs) and Fixed Interest (0.25 hrs)

please log in to start this quiz

———–

Disclaimer: Risk factors you should consider before investing:

– This material is not intended to provide investment advice or be considered a personal recommendation.

– The value of investments and income from them can go down as well as up and you may lose some or all of your initial investment.

– Past results are not a guarantee of future results.

– If the currency in which you invest strengthens against the currency in which the underlying investments of the fund are made, the value of your investment will decrease. Currency hedging seeks to limit this, but there is no guarantee that hedging will be totally successful.

– Depending on the strategy, risks may be associated with investing in fixed income, derivatives, emerging markets, sustainability-related investments and/or high-yield securities; emerging markets are volatile and may suffer from liquidity problems.

Statements attributed to an individual represent the opinions of that individual as of the date published and may not necessarily reflect the view of Capital Group or its affiliates. This communication is intended for the internal and confidential use of the recipient and not for onward transmission to any other third party. This communication is of a general nature, and not intended to provide investment, tax or other advice, or to be a solicitation to buy or sell any securities. All information is as at the date indicated and attributed to Capital Group unless otherwise stated. While Capital Group uses reasonable efforts to obtain information from third-party sources that it believes to be accurate, this cannot be guaranteed. In Australia, this communication is issued by Capital Group Investment Management Limited (ACN 164 174 501 AFSL No. 443 118), a member of Capital Group, located at Suite 4201, Level 42 Gateway, 1 Macquarie Place, Sydney, NSW 2000 Australia. All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company. All other company names mentioned are the property of their respective companies. © 2026 Capital Group. All rights reserved.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.25 hrs) and General (0.25 hrs)

ASIC Knowledge Requirements: Economic Environment (0.25 hrs) and Fixed Interest (0.25 hrs)

please log in to start this quiz