Fiduciary duty is more than a regulatory hurdle; it is the moral and professional backbone of a sustainable financial advice practice.

Today’s financial adviser stands as a true professional partner; a fiduciary whose primary purpose is to empower clients to achieve their life goals and financial objectives. This article, proudly sponsored by GSFM, examines the importance of fiduciary duty and ethics in the Australian financial advice practice.

Ethical financial advice is an essential aspect of ensuring the wellbeing and financial success of both individuals and businesses. Within this, fiduciary duty plays a crucial role in establishing trust, integrity and client-focused decision making.

As defined by the United Nations Principles of Responsible Investment (UN PRI), fiduciary duty exists to ensure that those who manage other people’s money act in the interests of beneficiaries, rather than serving their own interests. For financial professionals, fiduciary duty serves as a guiding principle that compels them to put their clients’ best interests first.

At its core, a fiduciary duty is a powerful commitment to partnership. It is the gold standard of professional relationships, ensuring that every recommendation, strategy and conversation is filtered through a single lens: the client’s best interest. This isn’t just about avoiding conflicts; it’s about the proactive pursuit of the best possible outcomes for those who entrust you with their futures.

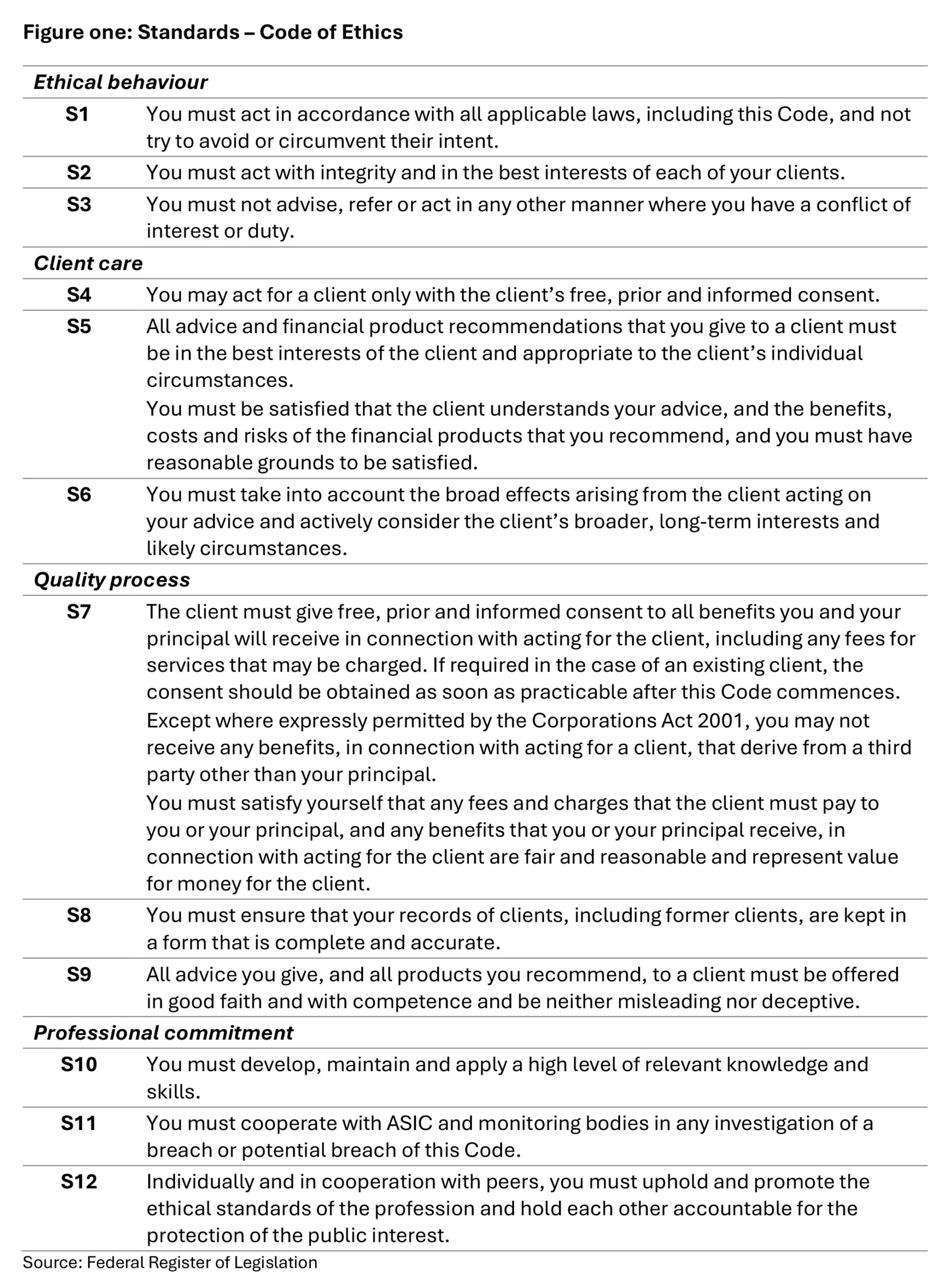

Fiduciary duty defined

A fiduciary duty is a fundamental legal and ethical responsibility that financial advisers, investment professionals and others in the financial services industry owe to their clients – it’s a promise to put their clients first. For financial advisers, this means moving beyond basic compliance to act with absolute loyalty and transparency. It is a legal and ethical mandate to prioritise clients’ financial well-being above their own personal gain or profits for the practice or licensee.

To honour this duty, an adviser must:

- Apply expert judgment and due diligence to ensure every recommendation aligns with each client’s specific objectives, goals and risk tolerance

- Disclose any potential conflicts of interest so the advice clients receive is unbiased and free from hidden incentives

- Exercise sound judgment, due diligence and integrity when managing assets on behalf of their clients.

Ultimately, this duty is the cornerstone of the adviser-client relationship. By aligning directly with the twelve standards (figure one) that comprise the Financial Planner and Adviser Code of Ethics (Code of Ethics), the fiduciary standard transforms financial advice from a simple transaction into a trusted, long-term partnership built on accountability.

ASIC describes the best interests duty and related obligations as:

“…designed to ensure that retail clients receive advice that meets their objectives, financial situation and needs, and that you act in the best interests of your clients when providing advice.”

As it relates to financial advisers, this can be articulated as always acting in the client’s best interests, acting with competence, honesty, integrity and fairness…words that appear in the value statements that underpin the Code of Ethics.

In July 2013, the introduction of FOFA included an amendment to the Corporations Act 2001 that enshrined the best interests duty into law and extended the existing fiduciary duty financial advisers owe to clients.

This duty encompasses the know your client requirement, the obligation to understand recommended products and the mandate to keep the client’s interests central to all advice. Alongside these amendments, strict penalties for non-compliance were introduced, including banning and disqualification orders.

Section 961B of the Corporations Act 2001 (as amended) lists the actions advisers must undertake to satisfy the best interests standard. In summary, these are[1]:

- To identify the client’s financial situation, objectives and needs; these should be provided to the adviser by the client.

- To identify the subject matter of the advice sought by the client (whether explicitly or implicitly).

- To identify the client’s relevant circumstances – the objectives, financial situation and needs that would reasonably be considered as relevant to the advice sought on the identified subject matter (i.e. the client’s relevant circumstances).

- To ensure this information is complete and correct, and to make reasonable enquiries if gaps or inconsistencies are apparent.

- To assess whether you have the expertise required to provide the client advice on the subject matter sought and, if not, decline to provide the advice.

- When considering the advice sought, whether it would be reasonable to consider recommending a financial product. If a financial product is deemed relevant, a recommendation should only be made after thoroughly investigating the most appropriate products relevant to the client’s circumstances.

- When advising the client, the financial adviser must base all judgements on the client’s relevant circumstances.

- Take any other step that, at the time the advice is provided, would reasonably be regarded as being in the best interests of the client, given the client’s relevant circumstances.

Number eight is a catch all statement that encapsulates the spirit of the legislation. Regardless of a client’s specific requests, all advice must be rooted in a deep understanding of their unique profile and circumstances. While the best interests duty is a formal requirement for retail clients, a comparable fiduciary standard governs professional conduct when dealing with wholesale clients.

A failure to act in a client’s best interests would not only breach section 961B of the Corporations Act 2001, but it would also breach several ethical standards, including:

ASIC notes that the best interests duty and related obligations are designed to ensure that retail clients receive advice that meets their objectives, financial situation and needs, and that you act in the best interests of your clients when providing advice.

ASIC’s Regulatory Guide 175 AFS licensing: Financial product advisers—Conduct and disclosure (November 2024) contains guidance about:

- How the best interests duty applies to personal advice (both comprehensive and scaled advice)

- Features of good quality advice

- The ‘safe harbour’ provisions, defining how to comply with the best interests duty

- The modified best interests duty and when it applies

- Use of processes to provide advice

- How to recognise a possible conflict of interest, and

- The conflicts priority rule and how it applies to products or services provided by a related party.

A practical fiduciary framework

There are several practical measures your advice practice can implement to ensure your team consistently meets its fiduciary duties and ethical responsibilities as outlined in the Code of Ethics. These include:

Transparency and disclosure

At its core, a fiduciary duty requires you to act with undivided loyalty to your clients. Transparency is the mechanism that makes this loyalty verifiable. By clearly communicating all costs, risks and associations, you eliminate any information asymmetry that may favour the professional over the layperson.

Ultimately, transparency and disclosure can transform your relationship from being simply transactional into a partnership built on informed consent, one that ensures your client’s best interests remain the primary driver of every decision.

There are several ways transparency and disclosure can support your fiduciary duty:

1. Transparency ensures clients have access to all relevant information about their investments, including potential risks, fees and conflicts of interest. By disclosing such information, your clients can make informed decisions and understand the implications of their investment choices. This transparency helps you fulfill your fiduciary duty by avoiding any misleading or incomplete information that could compromise any clients’ best interests.

Transparent disclosure of fees enables clients to understand the costs associated with your advice and their investments. This disclosure allows your clients to assess the value they receive from your services and make informed decisions about their financial goals.

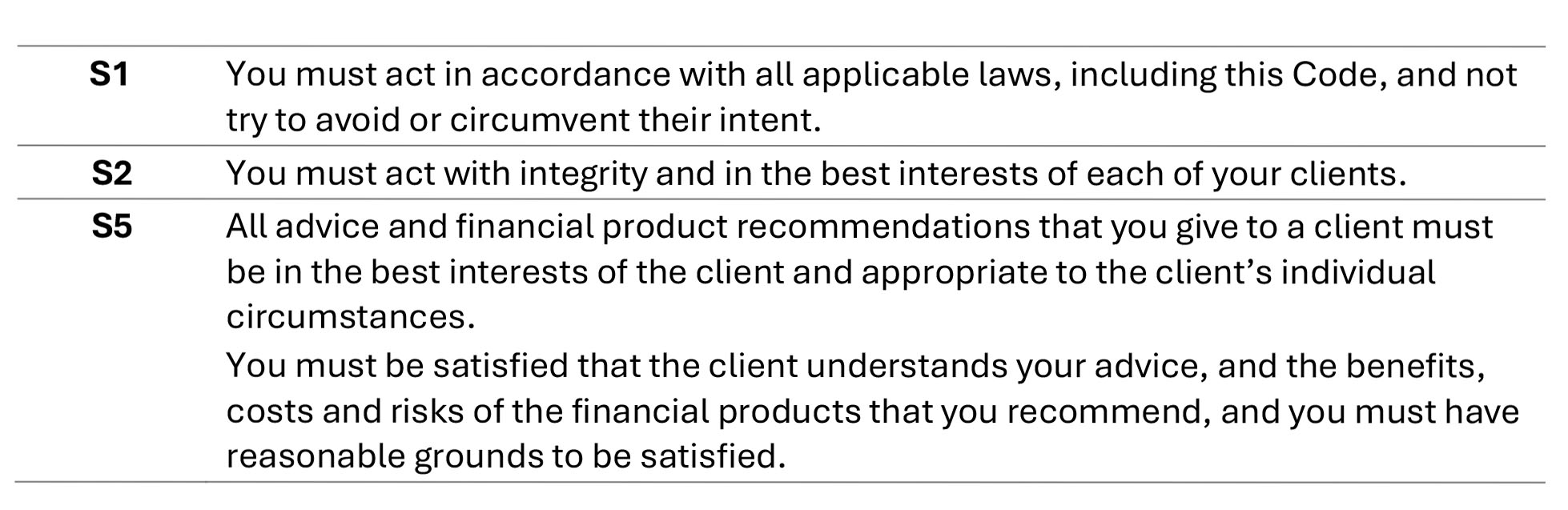

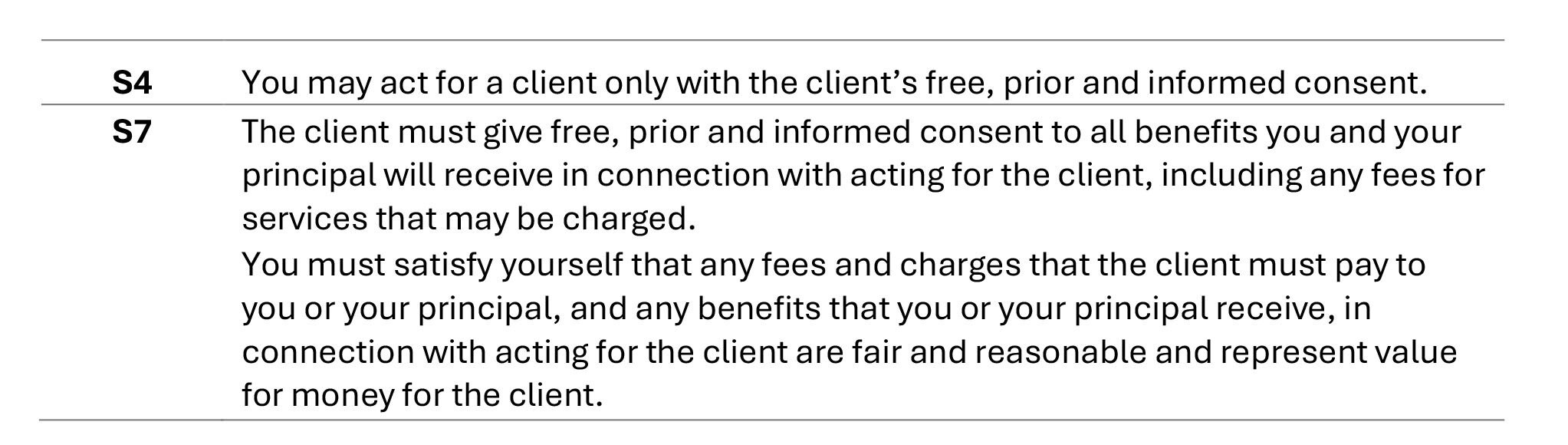

Transparency also ensures you meet standards four and seven of the Code of Ethics; without transparency, a client cannot provide informed consent. Being transparent about your advice, particularly about any benefits you receive – whether they flow to you or your licensee – are more likely to result in costs that are fair and reasonable and represent value for money for the client, as required by the standard.

2. It is an obligation for advice professionals to avoid or appropriately manage conflicts of interest. Transparency about any potential conflicts that could compromise clients’ interests provides clarity to your clients and ensures you take necessary steps to mitigate such conflicts. Full disclosure allows your clients to evaluate the advice they receive, helps you to maintain the clients’ trust and meet your fiduciary obligations.

Being transparent about any potential conflict of interest and how it is being managed can keep you on the right side of standard three.

3. Advisers must be transparent about investment advice provided to clients: the strategies, associated risks and any potential limitations or drawbacks. Clients need to have a clear understanding of how your recommendations align with their financial goals and risk tolerance.

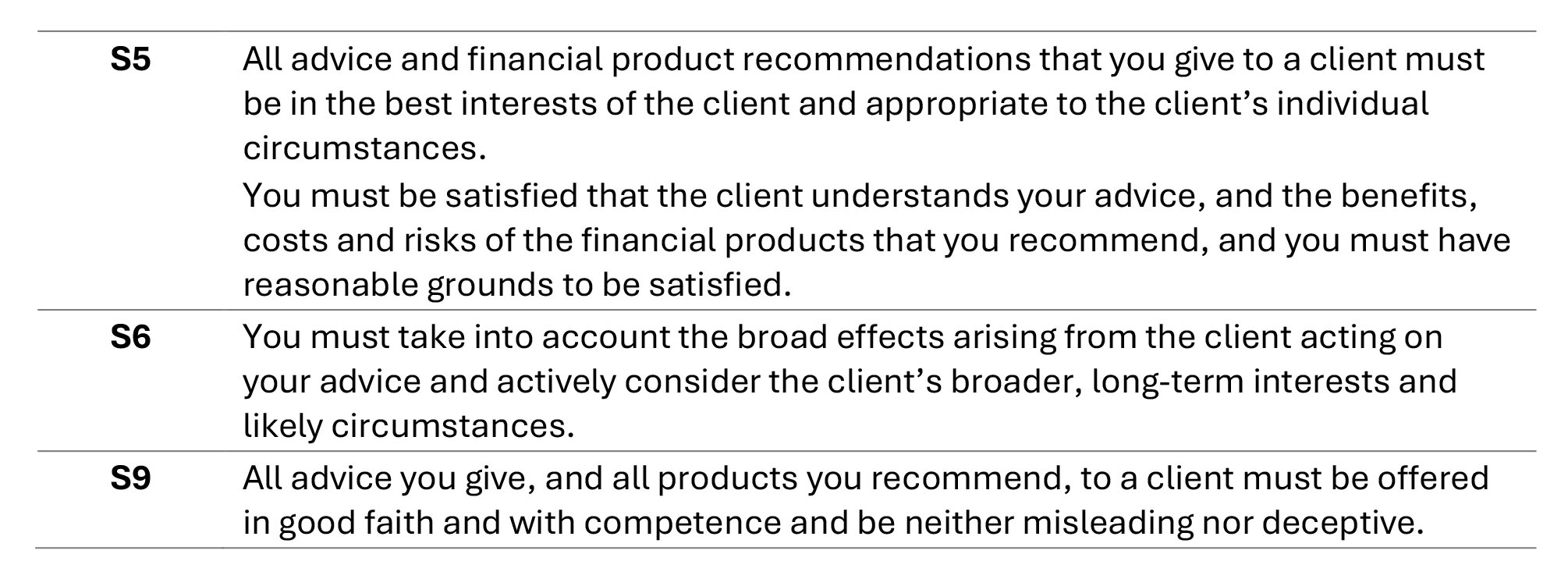

Transparent disclosure helps clients make informed decisions and helps you fulfill your fiduciary duty by providing suitable investment advice. Advice and product recommendations are covered by standards five, six and nine. Approaching advice with full transparency will help you meet those standards.

Ultimately, transparency enables clients to make informed decisions and trust that you have prioritised their best interests.

Client centric decision making

A commitment to client centric decision making provides the foundation for meeting your fiduciary duty. This approach means placing the client’s best interests at the forefront of each action and recommendation.

You have a legal and ethical obligation to act in all clients’ best interests, which requires prioritising factors such as their life goals, financial objectives, risk tolerance and financial security. By embracing a client centric mindset, you can tailor advice to align with each client’s unique circumstances, aspirations and long-term financial success.

A client-centric approach allows you to deliver personalised financial solutions that empower clients to achieve their objectives with confidence. This not only reinforces your fiduciary responsibility but also elevates the value and impact of the financial advice you provide.

Investing the time to understand your clients’ unique needs, preferences and concerns allows you to craft financial strategies that are both highly effective and personally resonant. This client-centric approach does more than just deliver results; it cultivates a foundation of trust and solidifies long-term loyalty, significantly boosting your professional credibility. Ultimately, a robust client-adviser relationship is the cornerstone of building and sustaining a thriving, reputable financial advisory practice.

A client first approach positions you to comply with key ethical and professional standards, including those outlined in the Code of Ethics, notably those in the ‘Client Care’ subsection (standards four-six). By prioritising your clients’ best interests at every stage of the advice process, you fulfill both your fiduciary duty and ethical obligations and, at the same time, enhance the overall quality and effectiveness of your advice.

Duty of care and skill

Fiduciary duty mandates a high standard of care and skill. Financial advisers are expected to possess and maintain the requisite expertise to provide truly competent advice. This requires a commitment to continuous professional development, staying ahead of shifting industry trends, evolving regulations and emerging best practices.

By upholding this standard of excellence, you ensure that every recommendation is underpinned by current data and optimised strategies. Fulfilling this duty not only demonstrates your professional integrity but also ensures direct alignment with the requirements of Standard ten.

Legal protection and accountability

Fiduciary duty also provides clients with legal protection and avenues for recourse in the event an adviser does the wrong thing for a client. Clients can seek redress through AFCA, and both ASIC and AFCA can hold financial professionals accountable for any misconduct or negligence that results in financial harm.

The legal framework that governs financial advice creates a strong incentive for advisers to act with integrity and maintain the trust of their clients. Legal protection and accountability are also enshrined in the Code of Ethics.

Case studies

The following case studies are based on real cases dealt with by ASIC or AFCA; however, the names of people and organisations have been changed and some details altered. For each case study, it will be shown where the adviser has potentially breached or upheld their fiduciary duty and how this did or did not comply with the twelve standards that comprise the Code of Ethics.

Case study one: A failure of fiduciary duty

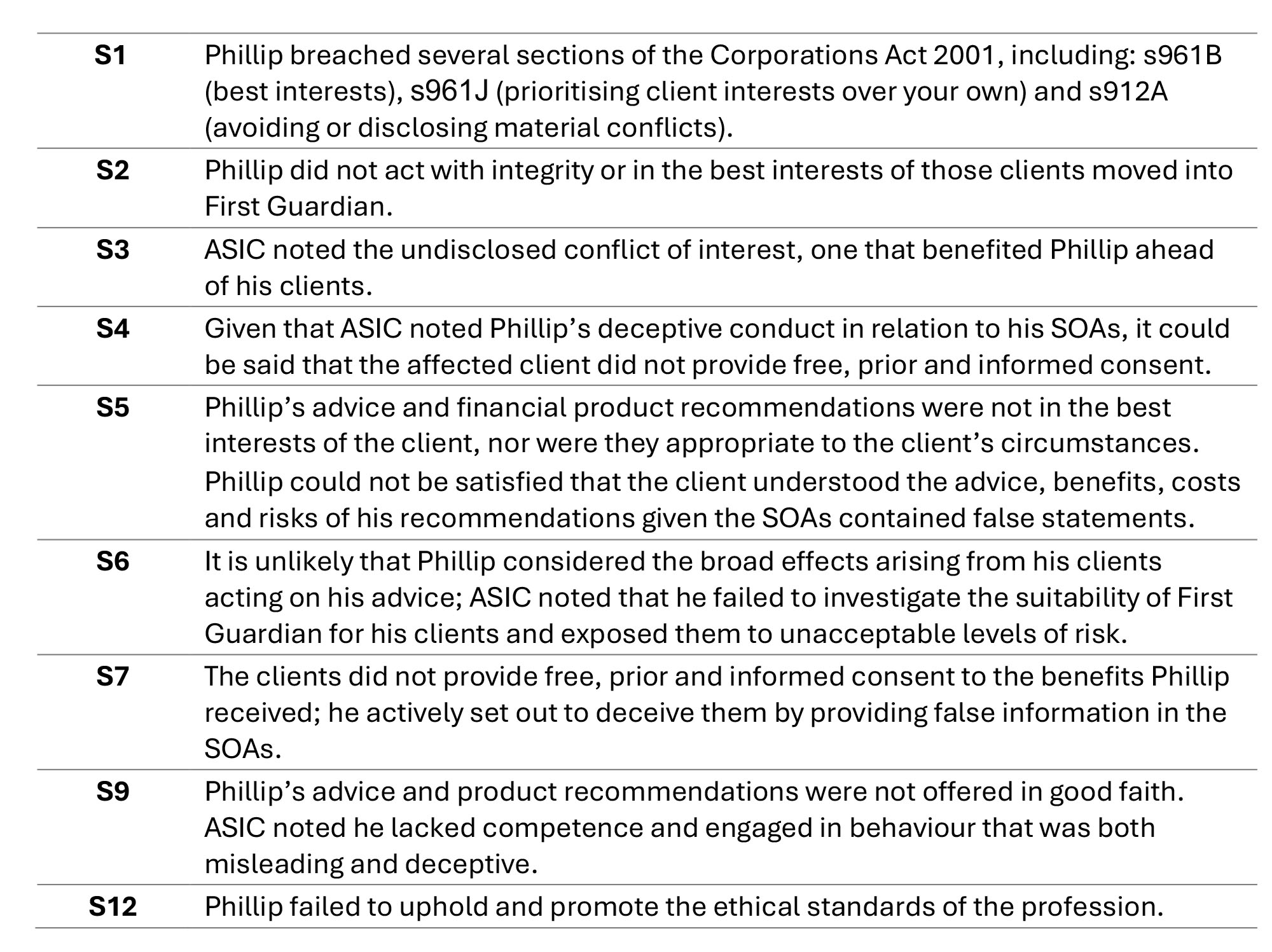

Readers will be aware that there have been a number of cases relating to investments in the First Guardian Master Fund (First Guardian), many of which are ongoing. This first case study is drawn from ASIC’s actions in relation to First Guardian. Names and details have been altered.

ASIC has issued a 10-year ban against former financial adviser Phillip following findings of serious professional misconduct. The regulator determined that Phillip breached his fundamental obligations by prioritising personal gain over client welfare, specifically regarding recommendations to invest in, and roll superannuation into, the First Guardian Master Fund.

Key findings of misconduct

The investigation revealed several critical failures in Phillip’s practice:

- Conflict of interest – he accepted $100,000 in payments classified as conflicted remuneration

- Deceptive conduct – he issued SOAs falsely claiming he received no benefits that could influence his recommendations

- Failure of care – he failed to investigate the suitability of First Guardian for his clients, exposing them to unacceptable risk levels.

- Lack of competence – ASIC concluded that Phillip was not a “fit and proper person” to provide financial services and posed a high risk of future legal contraventions.

The 10-year prohibition is comprehensive. Phillip is barred from:

- Providing any financial services.

- Controlling any entity within the financial services sector.

- Performing any function related to the operation of a financial services business.

ASIC stated that its enforcement action serves to protect consumers, maintain public confidence in the financial system and act as a deterrent against similar unethical behaviour within the industry.

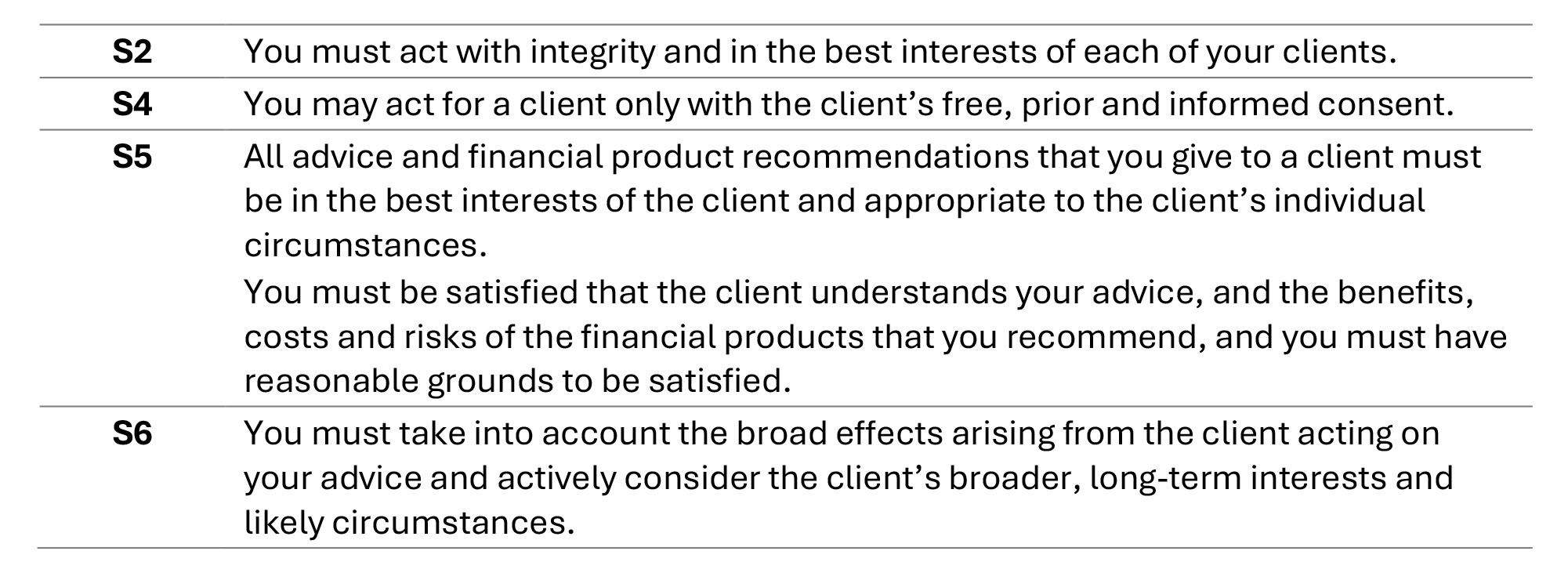

This case study highlights the interrelationship of fiduciary duty and ethics. As well as failing in his fiduciary duty to his clients, Phillip potentially breached nearly every standard in the Code of Ethics as follows:

Case study two: Inappropriate advice

Lydia sought compensation from her adviser, Charlie, and his firm, ACME Financial Advice, asserting that they had mismanaged her portfolio. Her primary contention was that the advice provided failed to meet her goal of maximising capital growth to facilitate retirement by age 60. She argued that the poor investment performance constituted a failure to act in her best interests.

ACME Financial Advice and Charlie denied any mismanagement, maintaining that the advice was appropriate for the client’s profile. They highlighted two key factors for the portfolio’s decline:

- To achieve the aggressive returns Lydia desired, she would have had to take on risk levels far exceeding her documented tolerance, which would have been inappropriate and contrary to her best interests.

- The firm noted that the significant reduction in Lydia’s portfolio balance was primarily driven by several large capital withdrawals she made over a three-year period.

The AFCA investigation of the matter saw the body rule in favour of the financial firm based on several key points:

Evidence versus recollection – while Lydia claimed her primary goal was early retirement, AFCA gave greater weight to contemporaneous documentation maintained by Charlie and ACME Financial Advice (Fact Finds, SOAs and file notes), which did not support her assertion.

Suitability of advice – AFCA concluded that advising Lydia to pursue the high-risk strategies required to attain her desired returns would have been negligent, given her recorded risk profile.

Responsibility for losses – AFCA found there to be no evidence of mismanagement; rather, the depletion of funds was attributed to market performance and Lydia’s own withdrawal history.

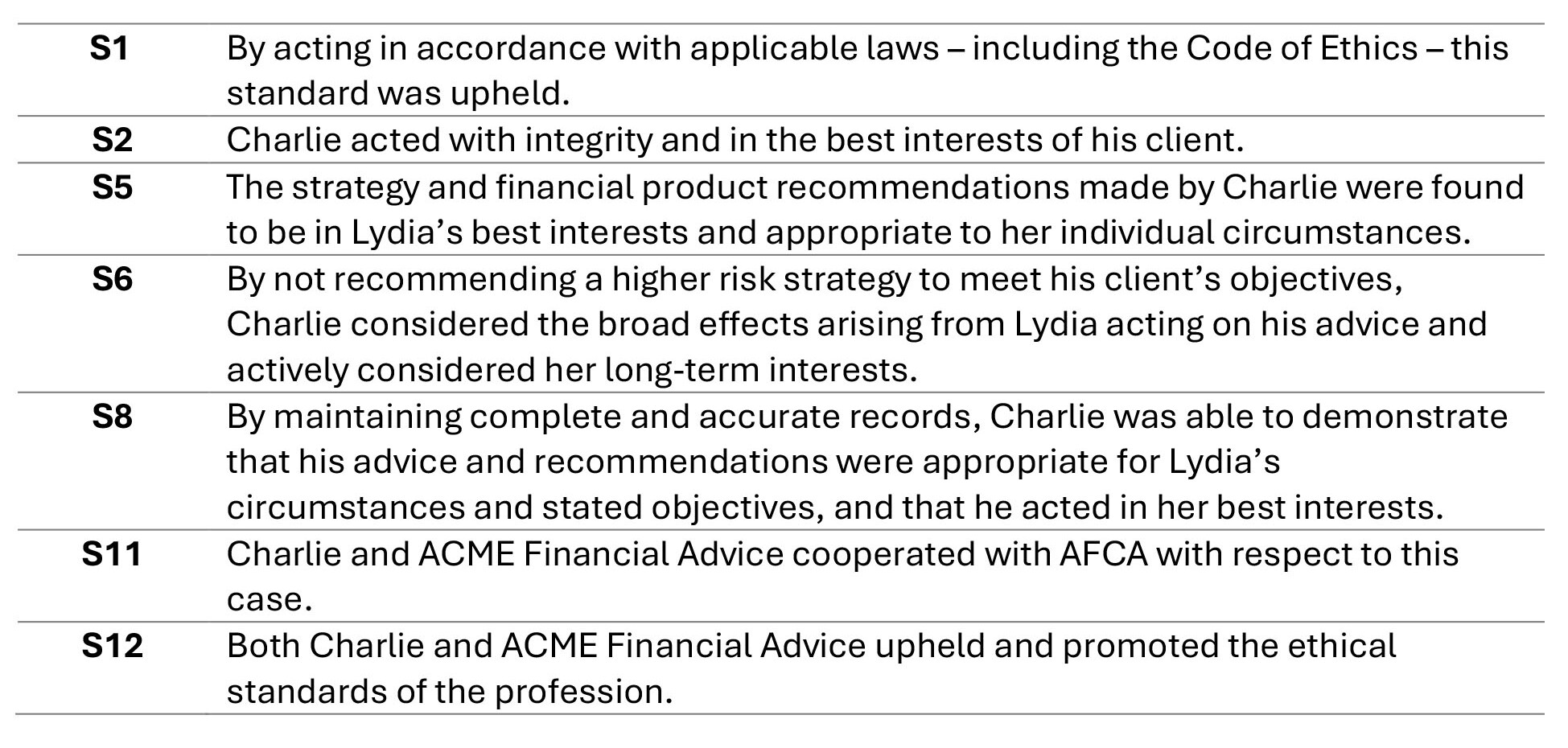

AFCA found the advice to be appropriate and determined that ACME Financial Advice was not liable for compensation. In this case, Charlie met his fiduciary duties. Specific standards in the Code of Ethics that he upheld in relation to this case include:

Case study three: A violation of fiduciary duty

The case against Simon involves a severe breach of the fiduciary relationship between a financial adviser and their client. Simon received $476,000 from his client George, specifically earmarked for investment in designated stocks.

Rather than executing George’s instructions, Simon misappropriated the funds to engage in personal trading on his own account. Following significant trading losses, he engaged in deceptive conduct by leading George to believe his investment remained intact, effectively concealing the loss.

Upon an ASIC investigation, it was determined that Simon’s actions demonstrated a fundamental lack of the integrity required for the advice profession. The regulator’s findings focused on three key areas:

Character and judgment – Simon was found to lack the necessary judgment and character to operate within the financial services industry.

Suitability – Simon was officially declared not a ‘fit and proper person’ to hold a position of financial trust.

Legal contravention – Simon’s conduct represented a flagrant misuse of client funds and a total breach of professional trust.

To protect consumers and maintain the integrity of the Australian financial system, ASIC imposed a permanent ban, prohibiting Simon from:

- Providing any form of financial service.

- Controlling any entity that carries on a financial services business.

- Performing any professional function within the industry.

This case is a reminder of the consequences of violating the duty of loyalty. Fiduciary duty is not merely a regulatory checkbox; it is a legal and ethical mandate to keep client assets separate and secure.

Transparency is required even (and especially) when losses occur; ASIC noted that deceptive reporting to hide a breach of trust is viewed as a separate and serious offense.

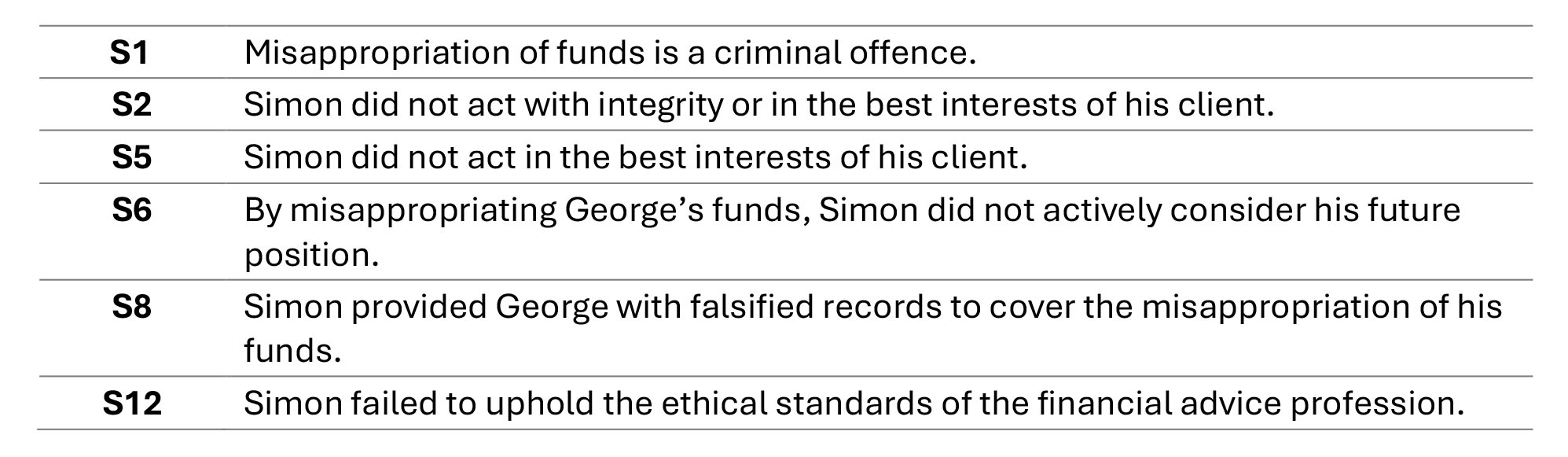

As a result of his actions, Simon potentially breached the following standards in the Code of Ethics:

Case study four: Fulfilling one’s fiduciary duty

The complainants in this case, Adam and Deanne, were growth investors with an ongoing advice relationship with ACME Financial Planning that spanned 15 years. The couple were informed investors, and both paid the highest marginal tax rate.

In 2020, the couple received advice from their adviser, Monique, that they should decrease their exposure to international equities in favour of Australian equities. The couple subsequently claimed the advice was not in their best interests and contrary to ACME Financial Planning’s own target asset allocation. As a result of the greater weighting to Australian equities, the couple claimed the portfolio underperformed by 14.7% – or $52,630 in dollar terms.

ACME Financial Planning acknowledged the allocation was contrary to its target allocation but said this was in the couple’s best interests because it provided access to tax benefits in the form of franked dividends. It also provided greater stability as it reduced foreign currency risk. The overweighting to Australian equities was clearly disclosed and explained in the Statement of Advice (SOA) that accompanied the advice.

The subsequent AFCA investigation determined that the advice Adam and Deanne received was in their best interests. Although it resulted in them having a greater exposure to Australian equities, AFCA was satisfied the rationale was clearly articulated and documented, and the reasons were not contrary to either party’s best interests.

Consequently, AFCA found in favour of Monique and ACME Financial Planning; neither party needed to compensate the client.

Clients seeking financial advice expect the advice provided will leave them in a better position. Section 961G provides that the resulting advice must be appropriate to the client. In relation to this advice, AFCA found there was a sound basis for deviating from the firm’s target asset allocation.

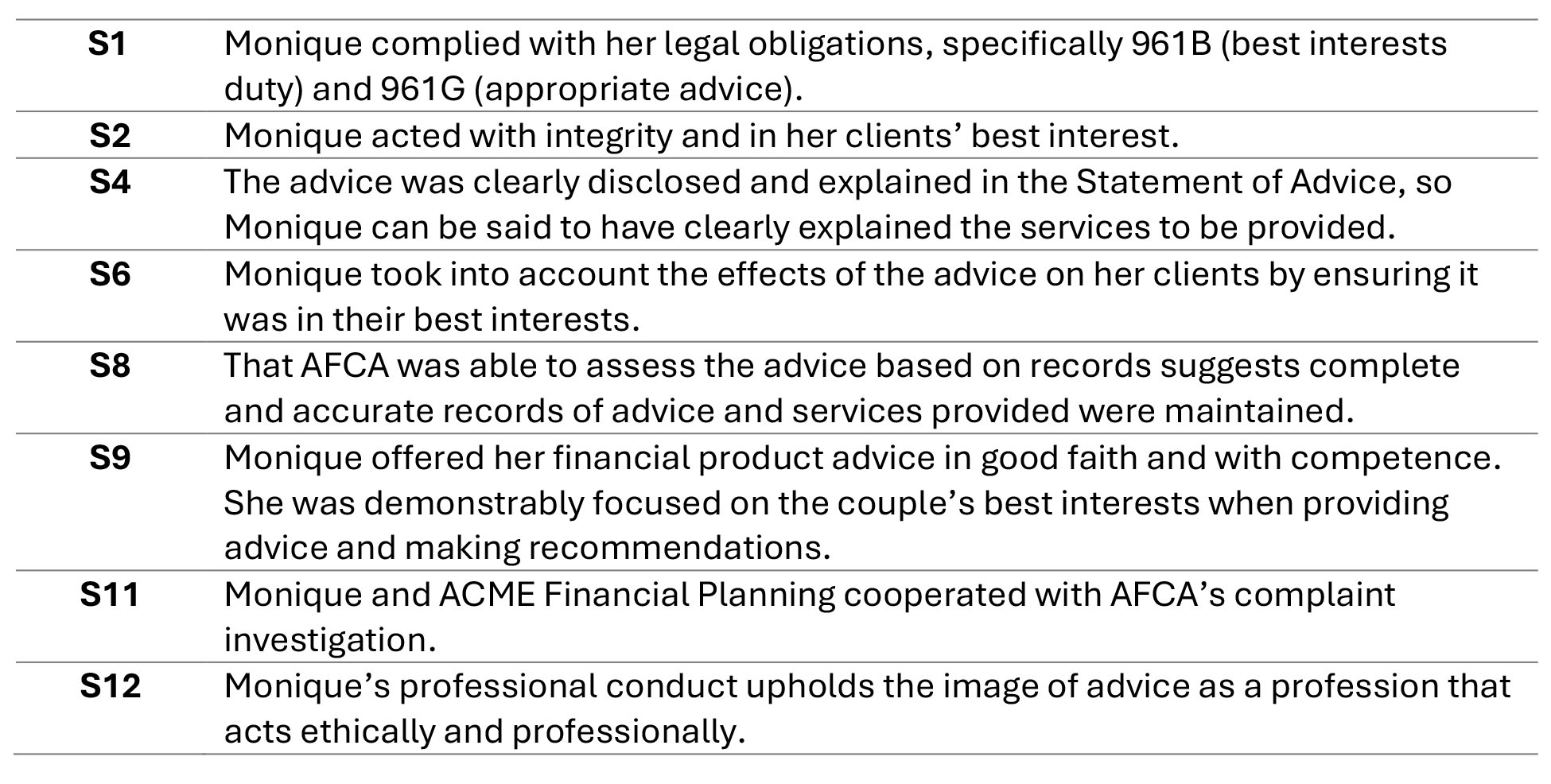

This case study demonstrated that financial adviser Monique had done the right thing. As such, she most likely complied with the following standards of the Code of Ethics:

Fiduciary duty is more than a regulatory hurdle; it is the moral and professional backbone of a sustainable financial advice practice. By centring the client’s best interests, advisers move beyond the role of a mere service provider to become a trusted partner in their clients’ life journeys. This commitment to loyalty, transparency and professional care does more than protect the public – it builds the very credibility and trust that allow a practice to flourish over the long term. In an industry where reputation is a valuable asset, upholding a rigorous fiduciary standard is not just a legal obligation, but the hallmark of professional excellence.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism & Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism & Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz