Risk is a word that generally tends to be thought of in a negative light. However, in the investment world risk is a necessary part of investing and cannot be separated from performance.

Assessing risk is one of the key factors in the investment process since every investment involves some level of risk. Most investors consider medium to high probability risks when making their investment choices. Low probability risks tend, perhaps understandably, to garner less attention. However, in our view, considering the impact of a variety of risks is crucial for effective risk management. It is important not only to consider high probability risks, but also low probability ones, especially where they would have a serious negative impact. This is a lesson that many investors learned when the GFC occurred and they were taken unawares.

Bonds have started to fall out of favour as investors are worrying about the end of the bond rally and rising interest rates in the medium term. However, were a low probability, high impact risk to occur, then it’s important to maintain an allocation to bonds in a diversified portfolio. If investors had had a higher allocation to traditional defensive Australian fixed income funds during the GFC, their portfolios may have been better protected. Fixed income provides superior volatility-adjusted returns (return per unit of risk) than equities, which has benefited fixed income investors during economic downturns.

In this paper, we discuss three low probability, high impact risks that Tyndall AM has been factoring into its thinking about the global macroeconomic landscape. We emphasise that we believe these events are unlikely to occur, but that the fallout if they did could be extremely severe. In such a situation, the portion of an investor’s portfolio allocated to bonds could help cushion the overall portfolio losses on the equity portion.

Is there a Canadian housing bubble and what would happen if it pops?

Interest rates across the world are at record lows and major central banks are indulging in huge quantitative easing (QE) policies. This has created a large amount of money that needs to be deployed. Following the GFC, banks globally have been reluctant to lend, particularly to small and medium-sized businesses. However, in some countries that came through the GFC relatively unscathed, banks have been willing to lend to individuals, in particular to invest in real estate.

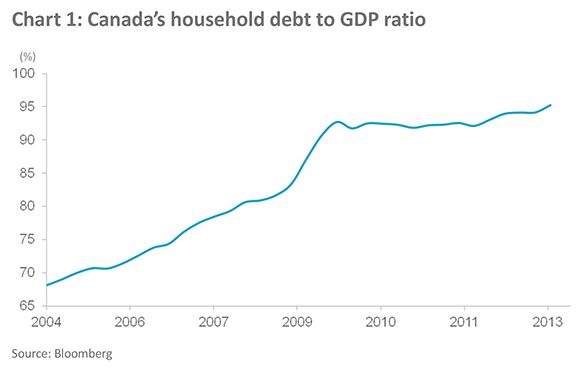

In Canada, the household debt to GDP ratio has been steadily rising, such that it now stands at almost 100% of GDP (see chart 1). According to the World Bank, the increase in this ratio since 2006 has been faster in Canada than any other country.

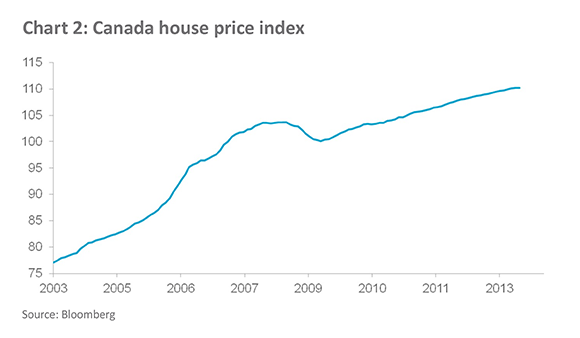

This phenomenon seems to be driven heavily by mortgage borrowing, which would explain the hefty rise in house prices over the same period (see chart 2).

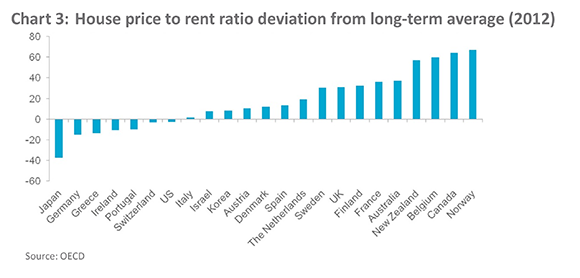

Countries that suffered severe housing market over-pricing in the lead up to the GFC, such as the US and Ireland, saw a strong correction and haven’t recovered much since then. As a result, those countries are now slightly undervalued. Countries that weathered the GFC more successfully are now the ones facing potential housing bubbles. As chart 3 shows, Canada was second only to Norway in that list as of the end of 2012 and Canada’s house prices are more than 60% higher than their long-term average. The Organisation for Economic Co-operation and Development (OECD) has ranked Canada as one of the countries most at risk of a price correction, especially if borrowing costs increase or income growth slows.

Construction projects are booming in response to demand from investors and home buyers taking advantage of record low interest rates. But analysts are warning that Canada’s housing market is due for a correction due to this overbuilding, as well as overvaluation and excessive household debt. The Bank of Canada recently noted: “The elevated level of household debt and stretched valuations in some segments of the housing market remain an important downside risk to the Canadian economy.” 2

The immediate impact of a major housing market correction would be on the Canadian banking system. However,

Canada’s banks remain relatively strong and although a slump in the housing market could create difficulties for the smaller banks, it is unlikely to have the same deadly impact in Canada as the slump in Irish property had on banks in Ireland. In addition, although Canadian banks extend globally, especially into Latin America and Asia, they are still minor players compared with major US or European banks so the knock-on effects would be more muted.

For Australian banks, the direct impact would likely be limited given that their exposure to Canadian banks is relatively low. However, the similarities between Canada and Australia could cause a severe weakening of sentiment towards Australian banks if their Canadian counterparts were to stumble. In such a case, the Australian banks’ dependency on offshore funding for a substantial part of their balance sheet could become a pressure point and the cost of funding could become elevated. Although it’s unlikely that this alone would be sufficient to cause major disruption in the Australian banking system, it could affect the credit spreads on the banks’ bonds and lead them to underperform for some time.

What are the downside risks for China?

China’s economy is no longer seeing the stellar growth that it had become accustomed to. The consensus view is that the country is unlikely to suffer a hard landing. While this is the most likely scenario, there are several issues about China that concern us: its shadow banking system, the extent and size of which is staggering; property prices in the major urban centres, which are displaying bubble-like conditions; and local government debt levels.

Shadow banks issue liabilities and hold assets, much like normal banks. However, unlike banks they lack an official lender of last resort. The International Monetary Fund (IMF) has pointed out that “a fast-growing share of credit is flowing through the less-well-supervised parts of the financial system.” 3 In fact, JP Morgan Chase & Co. estimates that from 2010 to 2012, shadow lending doubled to an estimated 36 trillion yuan or about 69% of China’s GDP. 4 The vast proportion of shadow banks’ business involves wealth management products (WMPs), which raise money from investors in large increments and for short periods. The problem with WMPs is that they have a potentially risky duration mismatch with the long-term underlying illiquid assets (such as property) they are secured against. The other issue is that those assets are not usually disclosed to investors so that they have no idea what they’re investing in. Often the banks repay maturing WMPs using money raised from new WMPs, which creates huge risk if the underlying assets were to perform poorly or default.

Another concern with shadow banks is that they are deeply intertwined with the commercial banks, which means there could be a knock-on effect if any of them fail. Shadow banks have sprung up because of the official policy of financial repression, where interest rates have been held at artificially low levels for a very long period to enable banks to keep lending to enterprises and governments, especially those engaged in building infrastructure. This drives Chinese households into WMPs in search of yield above the sub-inflation rates they are offered on bank deposits. The problem is that if enough of the riskier WMPs fail, investors might stop buying new products. Given the short-term nature of the WMPs vs. the long-term nature of the underlying assets, it could lead to a credit crunch on otherwise solvent projects.

The housing bubble issue is related to that same search for yield. China has very few investment vehicles on offer and real estate is one of those few. Prices continue to rise as a result, particularly in the larger cities, such as Shanghai, Shenzhen and Beijing. However, the pace of building may be starting to outstrip sales, particularly outside the larger cities where there is a growing stock of completed but unsold homes. The government has tried to curb this appetite for real estate, but with economic growth weakening it can’t risk leaning on the housing market too hard while it remains an engine for growth. Another concern is how indebted the property developers are, which makes them vulnerable to any downturn.

In December 2013, China announced the results of a debt audit on local governments, which included contingent liabilities and debt guarantees. The audit revealed that liabilities of local governments totalled 17.9 trillion yuan as of the end of June, compared with 10.7 trillion yuan as of the end of 2010, a 67% increase.5 Local authorities have been using debt to fuel growth, channelling money into infrastructure projects, some which may not have been particularly viable. However, given that the debt is almost all denominated in the domestic currency (yuan) and owned domestically, the central bank can prevent a crisis by deploying its unlimited liquidity supply.

The Chinese government realises that growth via such an investment-based economy is unsustainable. As a result, it is attempting to shift growth away from fixed asset investment towards domestic consumption, but this rebalancing is a delicate task. 2013 has seen repeated bouts of stress in China’s money markets as the government has attempted to tighten monetary conditions and reduce the economy’s reliance on cheap capital. By raising short-term rates and making them more volatile, the government is encouraging banks to stop relying on short-term liabilities in the interbank market to finance risky longer-term assets. Although the government doesn’t want to see a severe cash crunch, a miscalculation is possible if it doesn’t correctly predict the supply of and demand for cash when conducting monetary tightening. China needs to reform its financial sector, rein in government debt and increase consumer spending all at the same time – not an easy task.

Given how much control authorities have over the economy, for a crisis in China to emerge, it would likely be an accident, the result of an underestimation by authorities of the magnitude of one of these three issues and letting it get out of control. Any resulting slowdown would threaten stable growth in other economies. Australia in particular would be hit extremely hard by a crisis in China, so although such an occurrence might be extremely unlikely, it must be a factor in Australian investors’ thinking.

Are risks of deflation growing?

Despite the enormous amount of monetary stimulus that we have seen since the GFC from central banks globally, the developed world faces extremely low levels of inflation. Concerns have been voiced about the US, which saw inflation at a mere 1.2% in November. Following the GFC, households have been deleveraging and increasing their savings. At the same time, private sector companies have been saving much and investing little. This has created a huge pool of excess savings which is driving up current account balances, but creating deflationary tendencies. If no one is spending, prices start declining. The greater concern, however, is for several Eurozone countries due to their high unemployment, lack of competitiveness and continued private sector deleveraging.

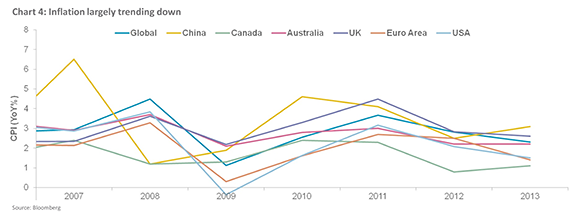

As chart 4 shows, the CPI trend is downwards for most countries, with the Eurozone showing the most worrying drop over the past year. Part of the reason for this is the resilience of the Euro, which has caused pain for the peripheral nations at a time when they need a weaker currency. Germany is still competitive despite the high Euro, but the peripheral countries need currency devaluation to help repair their economies and restore competitiveness. This has put further disinflationary pressure on the struggling bloc and led the European Central Bank (ECB) to cut its main refinancing rate to a record low 0.25% in November 2013. The ECB is rightly worried about potential deflation as it can create a downward spiral, with consumers and businesses delaying purchases in anticipation of lower prices in the future.

In a period of severe deflation, the real cost of borrowing would become prohibitive. Capital investment and other types of spending decline accordingly, adding to the economic downturn. Deflation would most likely tip the Eurozone back into a deep and prolonged recession. Another problem for the Eurozone is that the ECB can’t implement QE in the same way as the US. In fact, it’s not even clear that the ECB has full authority to do so, with the German constitutional court yet to rule on the legality of emergency measures.

Deflation would also increase the value of the Eurozone’s debt, with which it is already struggling. Households, companies and even the individual Eurozone governments could get into repayment troubles which would have a serious impact on the bloc’s banks, still the weakest link in the Eurozone’s recovery. If the tapering of QE in the US leads to a global rise in government bond yields at the same time, borrowing costs would increase further.

Were the Eurozone to sink into deflation, it would plunge Europe back into crisis, increasing the already high unemployment rate and possibly leading to a breakup of the bloc. This could affect the nascent recovery in the UK and the US, the Eurozone’s major trading partners. The ramifications of this scenario would be global given that deflationary pressures are not confined to the Eurozone but currently a potential issue for various countries globally, including the US. In such an event, with some of its major trading partners suffering, Australia could not expect to escape unscathed.

The unexpected is still worth consideration

Although the three scenarios discussed are unlikely to eventuate, if one of them did, it would have global ramifications, with knock-on effects for other countries. The GFC demonstrated how interdependent global economies have become and that the danger of widespread contagion from a disaster in one economy is high. As a result, such extreme events should play a part, albeit a small one, in an investor’s decision-making process, particularly given that the potential impact on Australia from one of these events would be large.

According to the OECD’s latest global pension statistics, Australian funds have the lowest allocation to bonds among developed nations. On the other hand, they have a high exposure to equities at a remarkable 46% of allocations. In most other OECD countries, bonds are by far the dominant asset class, with over half of pension funds investing more than 50% of their assets in bills and bonds in 2012. Australia actually has a much higher allocation to cash and term deposits than bonds. Being so underinvested in bonds and overweight bank term deposits means that diversification risk for Australian investors is heightened, since cash and term deposits don’t provide the low and often negative correlation to equities that bonds do. As a result, the impact of one of these events on Australian investors could be greater than in other countries.

As the GFC showed us, unexpected events do sometimes take financial markets and governments globally by surprise. In our view, bonds remain a valuable component of a diversified portfolio because they offer an offset to equities, which can help balance returns and reduce overall risk, particularly in down markets.

By Roger Bridges, Head of Fixed Income Strategy, Tyndall AM

———-

1 In a presentation to Ottawa Chamber of Commerce / Ottawa Business Journal: Mayor’s Breakfast Series, 27 April 2012.

2 Bank of Canada Monetary Policy Report, October 2013 (http://www.bankofcanada.ca/wp-content/uploads/2013/mpr-october2013.pdf ).

3 IMF Mission Completes the 2013 Article IV Consultation Discussions with China; Press Release No. 13/192; May 28, 2013.

4 According to a JP Morgan Chase & Co. research report, co-authored by their Chief China Economist, Zhu Haibin (http://online.wsj.com/news/articles/SB10001424052702304579404579236001885224902)

5 China National Audit Office report, 30 December 2013.

———-

Disclaimer: This document was prepared and issued by Tyndall Investment Management Limited ABN 99 003 376 252 AFSL No: 237563 (“Tyndall AM”). Tyndall AM is part of the Nikko AM group. The information contained in this document is of a general nature only and does not constitute personal advice. Nor does it constitute an offer of any financial product. It is for the use of researchers, licensed financial advisers and their authorised representatives. It does not take into account the objectives, financial situation or needs of any individual. The information in this document has been prepared from what is considered to be reliable information but the accuracy and integrity of the information is not guaranteed by the Company. Figures, charts and other data, including statistics, in these materials are current as of the date of publication unless stated otherwise. In addition, opinions expressed in these materials are as of the date of publication unless stated otherwise. The graphs, figures, etc., contained in these materials contain either past or backdated data, and make no promise of future investment returns etc. Past performance is not a reliable indicator of future performance.