Investment markets and key developments over the past week

- Shares were mixed over the last week with US shares pushed to record highs on good data and European shares up, but Japanese and Chinese shares down on poor data and Australian shares dragged lower partly on the back of further falls in the iron ore price. Bond yields were little changed as were most commodity prices, except the iron ore price which continues to fall. While the $US was little changed, the Yen and the $A fell, with the latter not helped by the falling iron ore price and dovish comments from RBA Governor Steven’s.

- Japan back to the polls with the next sales hike likely delayed. News that Japan is back in recession is mildly disappointing and having another election next month may create a bit of short term uncertainty. However, there is no reason to change our positive view on Japan: the Q3 contraction in GDP was due to lower inventories with private final demand up slightly; the broad trend in Japan’s manufacturing conditions PMI remains gradually up; the Bank of Japan’s substantially ramped up monetary stimulus now has very strong support at the BoJ and will help over time; Prime Minister Abe will almost certainly be re-elected giving him an additional 2 years to push through reforms; and the likely delay in the next sales tax hike (to 2017) will remove a key risk hanging over next year. So the case to remain overweight Japanese shares and underweight the Yen remains strong.

- A mildly dovish message from the Fed. While the Fed may have ended QE at its last meeting, the message from that meeting’s minutes is that it is clearly conscious of the risk to the US posed by global weakness and declining inflationary expectations in the US. While our base case remains that the Fed will start to hike around mid next year, the risks are skewed (again) to it coming later.

- RBA firmly on hold, probably into second half next year. There was nothing new in the Minutes from the last RBA Board meeting and similarly a speech by Governor Stevens reinforced the message that the period of stability in interest rates has a long way to go. While the Australian economy is coping with the mining investment and terms of trade slumps reasonably well, growth is still sub-par and the combination of improved productivity growth, slow wages growth and corporate cost cutting means inflation is not an issue.

- The Australia-China free trade deal is good news for Australia – particularly for farmers and the service sector – but it will take a while to impact and as we have seen with previous free trade deals doesn’t justify upwards revisions to long term growth forecasts for Australia. Rather such deals just help ensure that long term growth remains reasonable. With FTAs with the US, Chile, NZ, Singapore, Malaysia, Thailand, Korea, Japan and now China agreed the next will be India and Indonesia so all of our major trading partners will be covered.

Major global economic events and implications

- US economic data was solid. While the Markit manufacturing PMI fell it remains strong and the New York and Philadelphia regional surveys rose, the leading index rose, jobless claims fell and strength in the NAHB home builders’ conditions index, permits to build new homes and existing home sales point to a continuation of the housing recovery. While inflation was slightly higher than expected it remains benign and below target giving the Fed plenty of flexibility on interest rates.

- The Eurozone business conditions PMIs for November disappointingly fell, resuming the downtrend that started in August. While they still point to economic growth, it’s only modest. Quite clearly the ECB will have to ramp up its quantitative easing program.

- Japanese September quarter GDP unexpectedly fell due to inventories for the second quarter in a row marking a return to recession, but a rising trend in its manufacturing conditions PMI points to a return to growth this quarter.

- Chinese business surveys for November provided mixed readings with the HSBC flash PMI falling slightly but the MNI business conditions index up solidly. The fall in the HSBC PMI was disappointing but it’s just been making random wiggles in the same 48-52 range for the last three years now so it’s hard to read too much into it. Furthermore, APEC related shutdowns may have affected production and at least new orders rose. Meanwhile, property prices continued to fall in October but at a slower rate which could be just more noise or a sign that property easing measures may be working.

Australian economic events and implications

- Australian data was light on and didn’t really change the outlook either way with a nice rise in car sales but softish readings for weekly consumer confidence and skilled vacancies.

What to watch over the next week?

- In the US, the start of the holiday shopping season on Black Friday after the Thanksgiving holiday Thursday will be watched to gauge the strength of retail sales. On the data front expect to see: Q3 GDP growth (Tuesday) revised down to 3% from the 3.5% pace initially reported; modest gains in house prices (Tuesday); a further slight rise in consumer confidence (Tuesday); a continued rising trend in durable goods orders (Wednesday); gains in pending home sales and new home sales (Wednesday); and continued benign inflation according to the core private consumption deflator (Wednesday).

- In the Eurozone, economic confidence readings (Thursday) are likely to soften in line with recent PMI readings and the November flash inflation reading (Friday) is likely to show the Eurozone getting closer to deflation not helped by recent falls in the oil price.

- Japanese data for household spending, retail sales, industrial production, housing starts and the labour market on Friday should add to confidence that growth is returning in the current quarter. Inflation data (also Friday) will likely show that after the impact of the tax hike it remains too close to deflation reinforcing the need for the BoJ’s latest monetary easing.

- In Australia, the focus will be on September quarter construction data (Wednesday) and business investment (Thursday) as guides to September quarter GDP growth. We expect continued growth in dwelling investment but business investment to have remained soft resulting in falls in both construction and the capex data. Investment intentions are likely to show a further decline in mining investment ahead but more tentative evidence that non-mining investment is bottoming out. Data for new home sales will also be released (Thursday) and credit data (Friday) is likely to show further growth, but led by lending to housing investors, which of course won’t do anything to dissuade the RBA from placing restrictions on bank lending to investors.

Outlook for markets

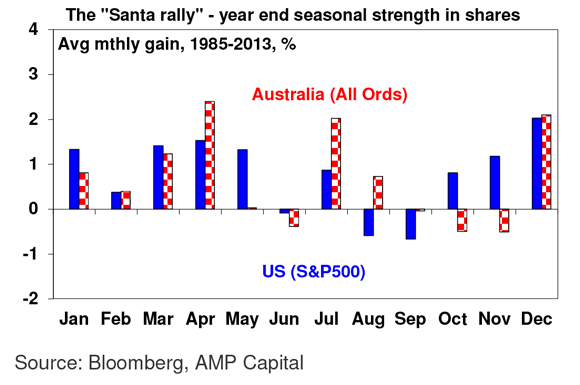

- Shares are well placed to see gains into year-end as the cyclical bull market that started in 2011 remains alive and well. November and December are both seasonally strong months for US and global shares as we run into the “Santa rally”, and seasonal strength in Australian shares usually commences in December. More fundamentally, valuations particularly against the reality of low bond yields are good, monetary policy is set to remain easy with QE in Europe and Japan replacing that in the US and rate hikes in the US and Australia being a long way off, and investor sentiment remains cautious which is positive from a contrarian perspective. Australian shares are likely to remain a relative laggard though as commodity price weakness continues to impact, but the positive global lead and the lower $A should help.

- Low bond yields will likely mean soft medium term returns from government bonds. That said, in a world of too much saving, spare capacity and low inflation it’s hard to get too bearish on bonds.

- The Australian dollar is likely to head even lower over the year ahead with the $US trending up, commodity prices on the slide and the $A still too high given Australia’s high cost base. $US0.75-0.80 is likely to be seen in the next year or so. A relatively greater fall in the $A/$US rate is partly necessary as the $A is unlikely to fall much against the Yen and Euro given their monetary stimulus programs.

By Dr Shane Oliver, Head of Investment Strategy & Chief Economist

——