Introduction

Ever since commodity prices and the mining investment boom peaked 3 or 4 years ago there has been a constant chorus of doom regarding the Australian economy: the reversal of the mining boom will knock the economy into recession, house prices will crash and banks will tumble. This view was particularly prevalent amongst foreign commentators who seemed to think that resource extraction was the only thing Australians do. While this tale of doom has not happened, the economy has been a bit lacklustre: growth has been sub-par, wages growth has fallen to record lows, unemployment has drifted up and confidence readings have remained poor. Against this background, the RBA has rightly cut interest rates again. This note looks at the key implications.

Interest rates and the economy

There are good reasons for the RBA to be cutting rates further:

- Growth is too low, running at around 2.75% through last year, which is well below potential (of around 3-3.25%) and the level needed to prevent a rise in unemployment.

- Confidence is subdued, having well and truly given up the post 2013 Federal election boost.

Partly reflecting this, consumers have started to become more focused on paying down debt again, which is a sign of increasing caution and will threaten spending if sustained.

- Prices for iron ore and energy have collapsed resulting in a bigger hit to national income than expected a year ago.

- Outside the US the predominant trend globally is still towards monetary easing and this is putting pressure on the RBA. Massive quantitative easing programs in Europe and Japan are forcing smaller countries to ease unless they want to see their currencies go higher. This should really be characterised as “easing wars” as opposed to “currency wars”. To the extent it is forcing monetary easing around the world, it adds to confidence that sustained deflation can be avoided. Australia is not immune. As the RBA wanted to see a continued broad based decline in the value of the $A it had to re-join the easing party lest the $A rebounded. Our interest rates are still high globally.

- Finally, benign inflation provides flexibility for the RBA.

The main risk in cutting rates again is that it further inflates the residential property market. However, strong property price gains are largely concentrated in Sydney and the RBA sees this as more of an issue for the prudential regulator, APRA.

Overall, we see the RBA’s cut as justified and, given that there is rarely just one move, we expect another 0.25% cut taking the cash rate to 2% in the months ahead.

Reasons for optimism

However, it’s not that I am bearish on the economy. Rather it makes sense for the RBA to be taking out some insurance to make sure growth holds up and improves. There are several reasons for optimism that growth will improve:

- Borrowing rates are at generational lows. This is bad for bank depositors but the latest rate cut will save someone with a $300,000 mortgage roughly an additional $15 a week. In total Australian households have $850bn in bank deposits but owe $2050bn in debt so the household sector is a net beneficiary of lower interest rates.

- The fall in the $A is removing a major drag on growth. It needs to go down some more but this is very positive for sectors such as manufacturing, tourism, higher education, services, farming and mining.

- The collapse in oil prices has delivered huge savings to businesses and households. If petrol prices hold around current levels it means the average household will save around $19 a week from mid last year on their petrol bill.

- Stronger export volumes from completed resource projects will provide a partial offset to lower commodity prices.

Overall, we see growth picking up gradually as the year progresses to a 3-3.5% pace through next year, but the RBA’s latest rate cut and one more to come provide confidence that this will occur.

Implications for investors

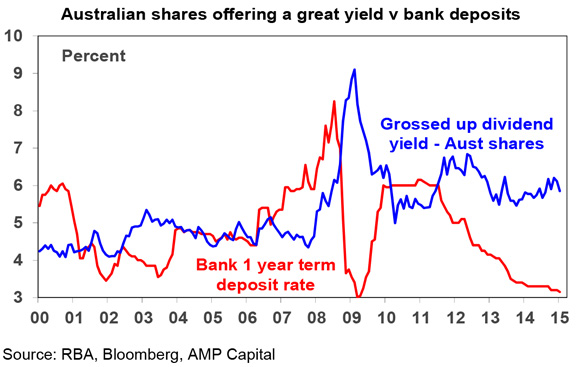

There are several implications for investors. First bank term deposit rates are becoming even less attractive and will remain low at least into next year. As a result, there is an ongoing need to consider alternative sources of yield and return.

Second, remain cautious on the $A. While the $A is nearly back to the $US0.75 level that marks fair value on the basis of relative prices, past experience tells us it can overshoot and it hasn’t fallen nearly as much against the Euro and Yen putting more pressure on for further weakness against the $US. The RBA has indicated “a lower exchange rate is likely to be needed”, and it is likely to ease further till it gets this. The $A is oversold short term and so could have a short term bounce, but expect a fall to $US0.70 by year end. So continue to favour unhedged over hedged global shares.

Dr Shane Oliver, Head of Investment Strategy and Chief Economist, AMP Capital

———–