The US economy is getting a shot in the arm from a consumer sector that’s showing renewed vigor. This upswing should more than offset a stumbling energy sector, and it’s changing the script for economic growth patterns six years into the expansion.

Growth should continue…with changing patterns

The US economic outlook for 2015 remains bright—we continue to see overall real gross domestic product (GDP) growth ranging from 3.5% to 3.75%. But the pattern and composition of growth is just as important as the rate of growth, and we think a major shift is coming this year.

We expect a major rotation in economic activity toward consumer spending on goods and housing-related items, accompanied by a significant reduction in business investment from energy-related sectors. This shift signals a new stage of the business cycle and consumer-related growth that’s often seen at the beginning of an economic cycle—not one that’s nearly six years old, as the current one is.

Energy-related reversal of fortune

The decline in oil prices should be a major factor in the growth patterns we anticipate in 2015. Energy prices collapsed by 50% in the second half of last year, triggering adjustments and cutbacks in energyrelated industries. At the same time, cheaper energy boosted cash flows for consumers and businesses, especially those directly and indirectly involved in transportation sectors, which are highly energy-dependent.

The adjustments in the energy sector have been acute, with several companies already announcing cutbacks in capital spending and payrolls. This will result in a near-term hit to US real GDP growth— concentrated in the oil and gas category of nonresidential investment.

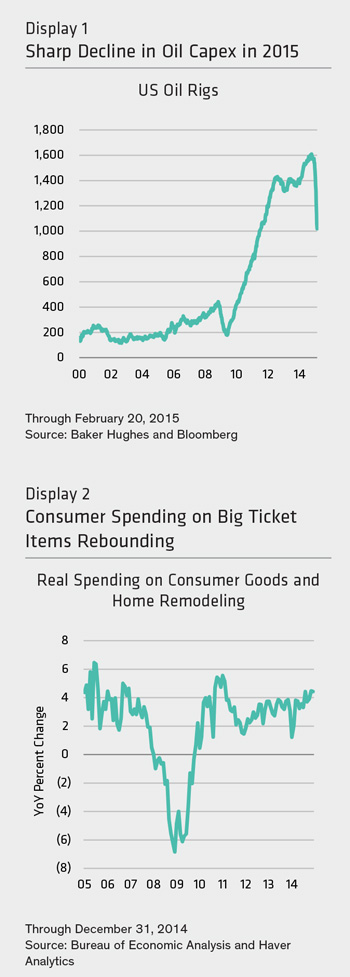

We can get some perspective on the speed and scale of the energy cutbacks from the oil rig count reported by Baker Hughes—it’s used to gauge the level of demand from oil rigs for supplies necessary to run their operations. The current rig count is around 1,000, a decline of about 40% from three months ago (Display 1). That sharp drop would likely reduce 2015 spending on oil and gas exploration by 30% to 40%, which will subtract about five percentage points from the growth rate of overall nonresidential structures spending. This will slice about 0.3% from overall US real GDP growth in 2015.

Resurgence in consumer spending

But an upswing in consumer sector activity due to a better jobs picture and opportunities should more than offset the drag on GDP from the oil and gas sector. We expect consumer spending to be bolstered by cash flow created by falling oil prices, rising real incomes tied to job creation, low inflation and rising confidence.

We’ve already seen evidence of the impact in fourth-quarter real consumer spending, which advanced by 4.2% annualized—the fastest pace in eight years. There’s also a shift under way in the economic mix toward higher-value-added products. For example, sales of light trucks, whose prices average about $10,000 more than cars, took a 56% market share in January, the highest in a decade.

There are other indicators that the US is in the early stages of a new consumer hardgoods spending cycle. Among them are strong year-over-year revenue gains of 7% to 8% by the nation’s two largest home improvement stores, Home Depot and Lowe’s. With spending on home remodeling still running at about half its share of the economy compared with the 2000s, we see significant pent-up demand.

So, a consumer revival is driving the upbeat outlook for the US economy. That represents a significant change from the pattern of growth we’ve seen to this point in the cycle. Over the past five years, the average annual growth in real consumer spending trailed overall private sector GDP growth by an average of 1% per year. This is atypical, especially for the early years of a business cycle.

In 2015, we expect overall consumer spending to rise by 3% to 3.5%. What’s more, if we add spending on home remodeling (Display 2, previous page), which is included in the residential investment component of GDP, gains should be in the 4% to 5% range.

By Joseph G. Carson, US Economist and Director—Global Economic Research, AB

——–