Investment markets and key developments over the past week

Shares had a rough week as Greek worries continued to weigh, the back-up in global bond yields resumed, and uncertainty about the US economy and the Fed continued. Australian were hit particularly hard by the weak global lead, messy Australian economic data and the RBA’s failure to reinstate an explicit easing bias. While global shares are down less than 2% from their recent high, Australian shares have come down by around 8% since their April high. Commodity prices generally fell and the $A rose slightly.

The bond sell off has clearly resumed again led by Europe on the back of stronger than expected Eurozone inflation prompting a further unwind of deflation fears. Comments by ECB President Draghi to get used to periods of higher volatility in bonds didn’t help. Our assessment remains that the bond sell off is unlikely to go too far as global growth remains below trend, inflation is weak, the ECB will continue to be a big buyer of bonds and other countries may still have to cut interest rates again. That said the rise in Eurozone bond yields may be a sign of success as US 10 year bond yields rose through each of quantitative easing mark 1 (by 200 basis points), QE2 (by 130 basis points) and QE3 (by 140 basis points).

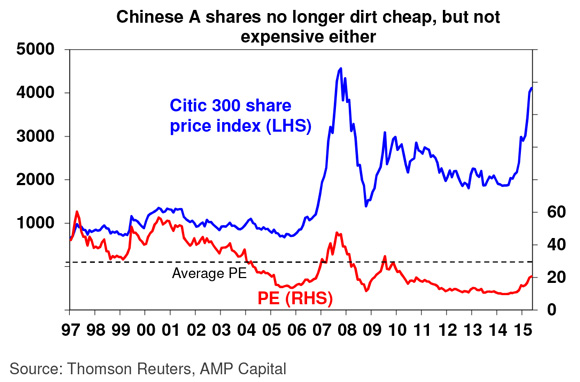

The 140% surge over 12 months and recent gyrations in Chinese shares have naturally led some to question whether it’s another bubble that may be close to ending. For example, the cover story in The Economist referred to a “mania” in China’s “overvalued” stock markets. There’s no doubt the Chinese share market has risen a bit too far too fast and parts of it, like ChiNext, do look overvalued. The easy gains are probably over and a period of correction would be healthy. However, the Shanghai composite index on an historic PE of 21 times is still below its long term average and should benefit as further monetary easing comes through. See the next chart.

In fact, The Economist’s cover story on “Flying too high – China’s overvalued stock markets” reminded me of the “Magazine Cover Indicator” which got its start from Business Week’s August 1979 cover on “The Death of Equities” which proved to be a great buying opportunity in shares. Since The Economist cover in October last year relating Europe to Monty Python’s dead parrot Eurozone shares are up 22%.

Negotiations on a “reform for funding” deal for Greece are continuing to drag on with Greece rejecting an offer from its creditors and choosing to bundle up its June 5 IMF payment to be made with other IMF payments at the end of the month. So the deadline has yet again been pushed out. Fortunately, negotiations still look to be ongoing. Our base case remains that some sort of deal will be reached in time, but given the stresses within the Greek Government and the need for any deal to be passed by various parliaments it is a close call. So a missed payment later this month remains a high risk. Such a Graccident doesn’t necessarily mean that a Grexit is inevitable but Greece will likely continue to be a source of volatility through June. Whichever way it goes though, the threat of contagion to other peripheral countries is low compared to the 2010-12 period as they are in far better shape now and the ECB is buying bonds across Europe as part of its QE program.

Major global economic events and implications

US economic data was mostly good. Personal spending in April was clearly on the weak side, but against this the ISM manufacturing conditions index rose solidly, non-manufacturing conditions indexes were a bit weaker than expected but remained at solid levels, construction activity rose strongly in April, auto sales rose to their fastest pace since 2005, the trade deficit narrowed sharply in May and labour market indicators are strong. The run of stronger data is adding to confidence that growth is rebounding in the current quarter. However, so far it’s not doing so as quickly as occurred last year and in contrast to the CPI, the core private consumption deflator – which is the Fed’s preferred measure of inflation – fell to 1.2% yoy, from 1.3%. So there’s still no reason for the Fed to hurry in raising interest rates. To this end it’s interesting to note that the IMF has effectively endorsed the position of the doves at the Fed in arguing rate hikes should be delayed until next year, not that this means the Fed will necessarily listen to the IMF.

The Eurozone also saw some good economic data, with the composite business conditions PMI revised up for May such that it remains at a reasonable level, retail sales up more than expected in April and unemployment falling more than expected. While the latter is still high at 11.1% the key is that it’s going in the right direction. On top of this inflation rose to 0.3% yoy in May and core inflation rose to 0.9% indicating that the risk of deflation is continuing to recede. However, Europe still has a long way to go to get growth and inflation back to decent levels and so it was not surprising to see ECB President Draghi reiterate the commitment to implement its quantitative easing plans in full (ie buying bonds out to September 2016).

In Japan there was a welcome rise in wages growth. However, at 0.9% yoy it still has a fair way to go before the BoJ can be confident its broken the back of deflation.

China’s official manufacturing conditions PMI rose marginally in May, albeit it’s still at the low end of the range it’s been in for the last few years. However, the slight improvement combined with a gain in average city property prices in May does add a bit to confidence that growth may be stabilising if not picking up. More policy easing is likely required though to be confident.

In India, the Reserve Bank cut interest rates again consistent with inflation being below target and growth in activity slowing in the March quarter. Further rate cuts are still likely. By contrast Brazil is continuing to hike interest rates with the policy rate reaching 13.75% reflecting high and accelerating inflation.

Australian economic events and implications

Australian economic data was messy. The good news was that March quarter GDP growth was a stronger than expected 0.9% quarter on quarter. Against this though, annual economic growth is just 2.3%, domestic demand remains very weak and data for April looks to be off to a soft start with flat retail sales, a blow out in the trade deficit and a fall in building approvals. The trade deficit blowout may be partly related to bad weather and a slump in the iron ore price to around $US45/tonne whereas it’s now back over $US60/tonne and the fall in building approvals looks like normal volatility. But Australian economic growth looks like remaining sub-par for a while yet as the investment outlook remains weak and the loss of national income due to lower commodity prices continues to impact. There is no reason to get too gloomy as the combination of low interest rates and a lower $A help rebalance the economy, but more help is likely to be required in the form of an even lower $A and possibly another interest rate cut.

While the RBA left interest rate on hold as expected and appears to retain a mild easing bias it was disappointing to see that it did not reinstate a more explicit easing bias. Doing so may have helped push the $A lower. Given the still messy economic outlook another RBA rate cut is a 50/50 proposition, with the August RBA meeting the one to watch.

Finally, there is nothing new in the latest house price data from CoreLogic RP Data. While prices fell in May this looks like a regular seasonal pattern. More fundamentally, while Sydney remains strong, annual price gains are averaging around just 2% in the other capital cities. As such, Sydney should not be seen as limiting any further monetary easing if it’s deemed necessary for the rest of the Australian economy.

What to watch over the next week?

In the US, expect May retail sales (Thursday) to show a decent 1% bounce after a period of partly weather related soft results, a slight rise in consumer sentiment (Friday) and producer price inflation (also Friday) to show a gasoline driven bounce but remain benign on a core basis.

In Europe the main focus will remain on Greece, and April data for industrial production (Friday) are expected to show a bounce back after March weakness.

In China, official economic data for May is expected to show signs of stabilisation in growth. Growth in exports and imports (Monday) is expected to improve slightly but remain negative, retail sales and industrial production are expected to pick up a bit, but investment may slow a bit further (all due Thursday) and credit and money supply growth should show a further improvement on the back of recent monetary easing.

In Australia, the NAB survey (Tuesday) will be watched to see whether the Budget had a positive impact on business confidence and it will be interesting to see whether consumer confidence (Wednesday) hangs on to its Budget related boost from last month. Meanwhile, April housing finance data (Tuesday) is likely to fall back a bit after the strong gain seen in March and jobs data (Thursday) is expected to be flat leaving the unemployment rate stuck at 6.2%.

Outlook for markets

Given the combination of seasonal weakness and uncertainties around bond yields, Greece and the Fed the next few months could remain volatile for shares. However, notwithstanding near term risks, the conditions for an end to the cyclical bull market in shares are still not in place: valuations against bonds remain good; economic growth is continuing at a not too cold but not too hot pace; and monetary conditions are set to remain easy. As such, share markets are likely to see another year of reasonable returns. My year-end target for the Australian ASX 200 index remains 6000.

Still low bond yields point to soft medium term returns from bonds, but it’s hard to get too bearish on bonds in a world of too much saving, spare capacity and deflation risk. Central banks won’t be ratifying a bond crash like in 1994, by raising interest rates aggressively.

The broad trend in the Australian dollar remains down as the Fed is still likely to raise rates later this year whereas there is a 50/50 chance that the RBA will cut again and the long term trend in commodity prices remains down. We expect a fall to $US0.70 by year end, and a probable overshoot into the $US0.60s in the years ahead.

By Shane Oliver, AMP Capital

———-