The recent stabilisation in Indonesia’s currency and bond markets, together with subdued inflation and a healthy trade surplus, is paving the way for monetary easing. Moreover, a pickup in infrastructure spending bodes well for productivity growth, adding to the positive momentum.

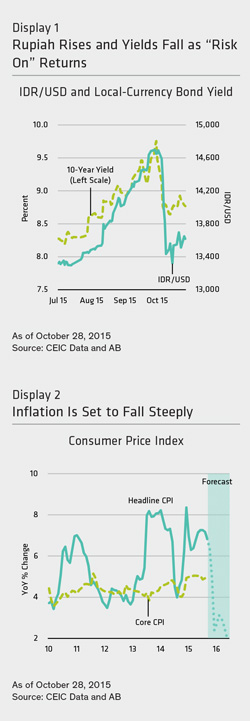

The return of risk appetite in global markets and a resultant rebound and stabilization in the Indonesian rupiah (IDR) have drastically changed policy trajectory and market expectations in Indonesia. Although Bank Indonesia (BI) kept its policy rate unchanged at its October 16 policy meeting, the overall tone of the central bank has turned almost outright dovish. With the IDR/USD exchange rate appreciating by about 7% so far in October, local-currency bond yield eased back—to the tune of some 120 basis points for 10-year government bonds from their September highs (Display 1).

Bonds rallied in response to the IDR appreciation, even though a widely anticipated drop in consumer price inflation (from November onwards) has yet to show up in latest inflation numbers.

Adding to the upbeat momentum, fiscal data have revealed some positive trends. The government’s stepped-up effort to kick-start the major infrastructure projects is starting to pay off. This may enhance President Joko “Jokowi” Widodo’s floundering leadership credentials. We think that President Jokowi’s official visit to the US this week may also pave the way for a membership to the Trans Pacific Partnership (TPP) free trade pact, which should brighten the outlook for the country’s future trade liberalization process.

BI Turns Dovish

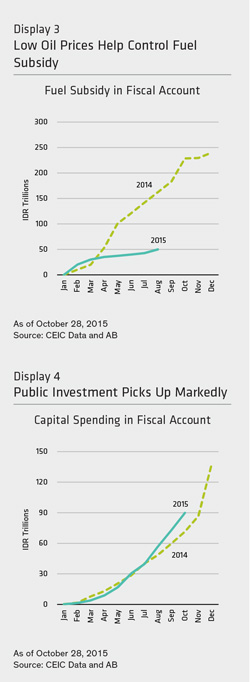

While keeping the policy rate at 7.5% at the October policy meeting, BI left little doubt that there was growing room for monetary easing thanks to the renewed macroeconomic stability. We have long argued that by December, when the November consumer price index (CPI) is released, that a rate cut would be warranted. CPI inflation is likely to fall dramatically to 4%–5% in November from 6.8% in September as a favorable “base effect” kicks in, and this would mean that real interest rates would rise despite sluggish economic growth.

Now with the IDR regaining some stability and the fact that Indonesia has been running monthly trade surpluses so far this year—with the total surplus reaching a healthy US$7.1 billion in the first nine months—the central bank should be able to ease monetary policy to support flagging growth with less worry about the risk of a major sell-off in the IDR.

The caveat, of course, is that this scenario is predicated on the expectation that the current global “riskon” sentiment stays largely unchanged at least, till the end of the year.

Headline Inflation Set to Improve

What is more certain at this juncture, though, is that CPI inflation is set to fall markedly as the base effect, owing to the elevated levels a year earlier, kicks in from November onwards.

Our analysis suggests that if the CPI merely stays at around its current level, the base effect alone will bring inflation down to 2.5% by December 2015 and 1.5% by mid-2016 (Display 2). This is not too tall an order, given the continued sluggishness of global commodity prices and the possibility that the worst of the IDR sell-off is now over. This relatively predictable base effect should give the central bank plenty of confidence about cutting rate cuts—shifting its focus from inflation to the need to stimulate growth.

Infrastructure Investment Picks Up

The virtuous circle is in motion in Indonesia. Public works spending is picking up sharply after a prolonged delay as the government’s efforts to step up project approvals and implementation are beginning to pay off (see “Indonesia’s Fiscal Performance Set to Improve” Asian Perspectives, July 31, 2015).

Monthly budget data also show that the government has been able to reallocate money saved by domestic fuel subsidy cuts, thanks to lower crude oil prices, to capital spending in order to bolster infrastructure projects. While fuel subsidies are down some 70% from a year earlier, capital spending has begun to rebound— up 17% year on year in August and 26% in October (Displays 3 and 4).

The government has disbursed only one-third of its planned infrastructure spending for this year yet, but the recent pickup in the pace of spending is certainly encouraging.

As the capex cycle gradually revives owing to expanded government expenditure, the headline fiscal deficit number will likely deteriorate. Increased capital goods imports may trim the trade surplus as well. But these are productive investments, which the economy needs for long-term productivity growth. Thus, it is only natural that the market is getting more confident about the macroeconomic environment and government policy.

By Anthony Chan, Asian Sovereign Strategist, Global Economic Research, AB

——–