Investment markets and key developments over the past week

Shares were mixed over the last week with US shares up 0.2% and Japanese shares up 1.4%, but Eurozone shares down 0.2%, Chinese shares down 0.9% and Australian shares losing 2.1% not helped by concerns that a possible December Fed tightening will reignite worries about a strong $US pressuring emerging market currencies and commodity prices. Worries about an oversupply of steel saw the iron ore price fall back below $US50/tonne which weighed on Australian miners. The global steel and iron ore glut looks like it will push the iron ore price to around $US40 in the year ahead. Bond yields rose in the US on the Fed. Soft commodity prices and heightened expectations of an RBA rate cut saw the $A fall.

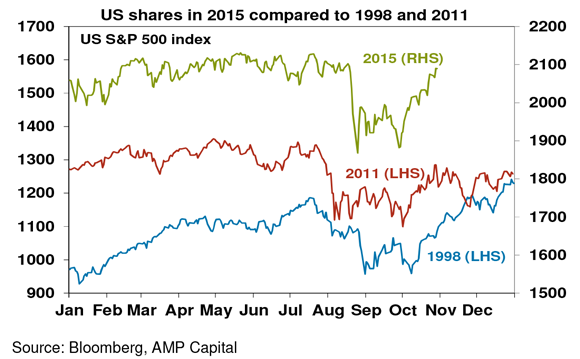

It’s been a strong October with US, Eurozone and Japanese shares up 8-10%, Chinese shares up 10.8% and Australian shares up 4.3%. After the sharp share market falls in the September quarter, October has lived up to its reputation as a “bear killer” (at least so far!). However, November is unlikely to be as strong as after rising 10% from their September lows global shares are overbought and due for a correction particularly with concerns around the Fed and the emerging world remaining. The 2011 analogy which the US share market has been following reasonably well also points to the risk of a correction in November. This is likely to impact Australian shares. But after a pull back or consolidation expect shares to resume their run up into year-end as the typical Santa Claus rally sets in.

Fed on hold, but still thinking of hiking in December. The Fed’s post meeting statement was a bit more hawkish with US consumer spending and investment seen as “solid”, less concern about global developments and a clear statement that it will decide in December whether to raise the Fed Funds rate. However, while the Fed wants to keep its options open for a December move, in deciding whether to hike or not the Fed will remain “data dependent”. The latest talk of a December hike has also reignited worries about upwards pressure on the $US putting pressure on commodities and emerging countries. So given this and recent concerns about softer US growth, a December hike is arguably still less than a 50/50 proposition. Growth in US employment costs of just 2% year on year in the September quarter and the Fed’s preferred measure of inflation stuck at just 1.3% year on year do not support the case for a December hike. I see the Fed delaying into 2016.

Meanwhile, the risk of a US debt default next month or government shutdown in December has been all but eliminated by a bi-partisan deal that will suspend the debt ceiling to March 2017 and fund the government for 2 years. US Congressional politics remains low risk for financial markets.

Not much to get excited from China’s 5th Plenum beyond the shift from a 1 child to a two child policy. Allowing all couples to have 2 children is a big move for China, but it won’t impact the labour force for 15-20 years and will still see the population decline as 2 per couple is still below replacement and it’s doubtful that all urban residents want to have more anyway. So it’s hard to see much economic impact. In terms of growth, a target to double per capita income by 2020 implies a 6.5% pa GDP growth target for the next five years which is in line with expectations and reflects China’s slowing population and productivity growth as the focus shifts from investment to consumption. Commitments to focus on innovation, increase consumption, accelerate urbanisation, improve social welfare, reform the financial system, improve social welfare and protect the environment are all welcome but in line with the direction of existing policy anyway and so don’t really change the growth outlook. In terms of the recovery in the Chinese shares we continue to see good medium term return potential in Chinese shares, particularly Chinese companies listed in HK where the H share market is trading on a forward PE of 7.6 times.

Lower than expected September quarter inflation in Australia adds to the case for another RBA rate cut. Despite a 20% plus fall in the value of the $A over the last year there is little evidence of this flowing through to higher consumer prices, apart from higher prices for overseas travel. Rather, evidence of weak pricing power is widespread consistent with ongoing demand softness. While the inflation rate is not low enough to guarantee a rate cut it adds to the case for a cut that has already been made by sub-par economic growth and the defacto monetary tightening that will otherwise flow from big bank mortgage rate hikes.

Major global economic events and implications

US economic data was on the soft side, with falls in home sales, durable goods orders, consumer confidence and the Markit services PMI contradicting the Fed’s more upbeat view on the US economy. September quarter GDP growth fell back to just 1.5% annualised. While this was due to a negative contribution to growth from inventories, with final demand remaining strong at 3%, recent indicators suggest that demand is slowing in the current quarter. More broadly real GDP growth is running at 2% year on year which is in line with average growth since the GFC and well below what would normally be seen after a major recession. What’s more nominal GDP growth is just 2.9% yoy, the September quarter Employment Cost Index at just 2% yoy shows no sign of building wage inflation pressure and the core private consumption deflator at 1.3% yoy in September remains well below the Fed’s inflation target. US growth is not bad but it’s a long way from booming and with inflation pressures remaining low the Fed needs to be cautious.

US September quarter earnings results were better. With 68% of S&P 500 companies having reported 75% have beaten earnings expectations. But only 44% have beat on sales as the strong $US and oil price fall weighs. Consensus earnings expectations for the year to the September quarter have improved though from -6.3% two weeks ago to -3.9%.

Eurozone economic confidence improved further in October, pointing to okay growth, but a slowing in private lending growth in August would be concerning the ECB as would inflation that remained well below target in October.

Japanese economic data was a bit more upbeat. September household spending was weak, but industrial production rose, the unemployment rate remains low and the jobs to applicants ratio is now at its highest since 1992. There was also good news on the inflation front with core inflation at 0.9% year on year which is its highest since 1994. There is still a way to go to reach the 2% inflation target though and so while the Bank of Japan made no change to its monetary stimulus program at its October meeting, the pressure remains for further easing.

Australian economic events and implications

Apart from lower than expected consumer price inflation, September quarter prices for exports and imports point to a further fall in the terms of trade and credit growth data showed a further slowing in lending growth to investors. Rolling three months annualised growth in lending to property investors slowed to 7.9% in the September quarter down from a peak of 11.1% in the three months to November last year. Slowing lending to investors along with a 4% fall in new home sales and weakness in auction clearance rates adds to evidence that the housing market is cooling down.

What to watch over the next week?

In the US, October employment data (Friday) will be watched very closely as a guide to whether the Fed will raise rates in December. Expect a 180,000 gain in jobs continuing the slower tone of recent months with unemployment remaining at 5.1% and wages growth around 2.3% year on year. In other data, expect the October manufacturing conditions ISM (Monday) to remain around the 50 level, the non-manufacturing ISM to remain solid at around 56.5 and a fall in the trade deficit (both Wednesday). September quarter profit results will also continue to flow.

China’s manufacturing conditions PMIs are expected to show signs of improvement, with the Caixin PMI being released Monday. Trade data (November 8th) will be watched for improvement in exports and imports.

In Australia, the RBA is expected to cut the official cash rate to 1.75% from 2% when it meets Tuesday. The case to cut is powerful as a rate cut now will head off already announced big bank mortgage rate hikes and the threat this will pose to consumer spending at a time when economic growth is weak, non-mining investment is poor, the contribution to growth from home construction looks like peaking next year, El Nino related drought risks are posing an additional threat to growth, the terms of trade is still sliding and inflation remains below target. Of course the RBA may opt to wait for more information having expressed comfort recently about current interest rate settings – which makes our call for a November cut a close one. But if there is no cut Tuesday then expect one sometime in the next few months. The risk in not cutting in November though is that the longer the RBA waits the more it may have to do next year – so easing now is likely to be the path of least regret. The RBA’s Statement of Monetary Policy (Friday) is expected to show modest downwards revisions to the growth and inflation outlook. A speech by Governor Steven’s (Thursday) will also be watched for clues on the interest rate outlook.

On the data front in Australia, expect CoreLogic RP Data dwelling price indices (Monday) to show some loss of momentum in October, building approvals (also Monday) to show a slight bounce but not enough to dispel the impression they have peaked, the trade balance to show a continued large deficit and retail sales (both Wednesday) to show a 0.4% gain.

Outlook for markets

After strong share market gains in October November is likely to see a pause or correction – perhaps driven by ongoing Fed/emerging market concerns. But markets are likely to see the normal “Santa Claus” rally into year end and the broad trend in shares is likely to remain up. Shares are cheap relative to bonds; monetary conditions are set to remain easy; this in turn should help see the global economic recovery continue; and investor sentiment remains negative such that it’s actually positive from a contrarian perspective. As such, share markets are likely resuming a broad rising trend. This includes the Australian share market, where we continue to see the ASX 200 rising to around 5500 by year end.

Low bond yields point to soft medium term returns from bonds, although government bonds remain a great portfolio diversifier.

The broad trend in the $A is likely to remain down as the Fed is likely to raise interest rates sometime in the next six months whereas the RBA is more likely to cut rates again and the trend in commodity prices remains down. This is expected to see the $A fall to $US0.60 in the next year or so.

Shane Oliver, AMP Capital

——–

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.